|

시장보고서

상품코드

1851129

교육용 로봇 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Educational Robot - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

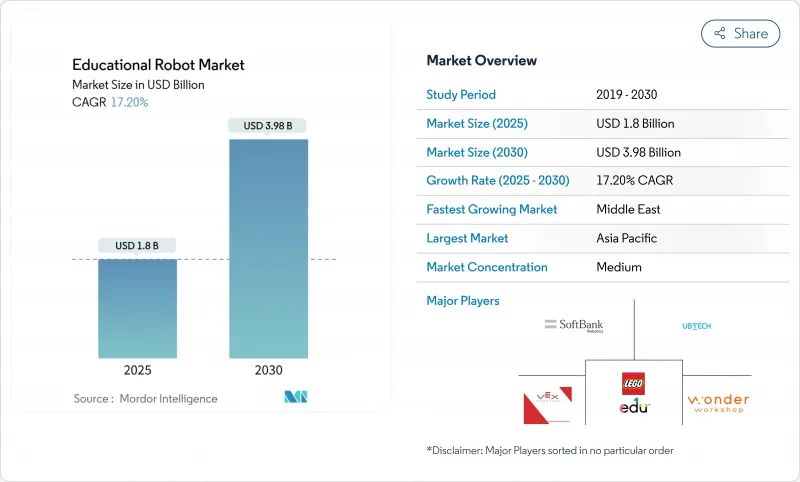

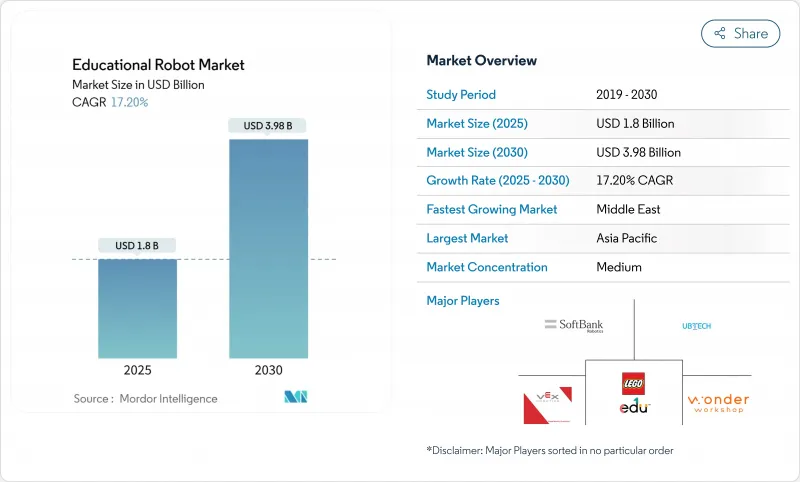

교육용 로봇 시장 규모는 2025년에 18억 달러로 추정되고, 2030년에는 39억 8,000만 달러에 이를 것으로 예상되며, 예측 기간 중 CAGR은 17.2%로 활황을 보이고 있습니다.

대규모 언어 모델 AI의 급속한 통합으로 교실 로봇은 컨텐츠와 페이스를 실시간으로 조정하는 적응 학습 컴패니언으로 변모하고 있습니다. 하드웨어 가격은 하락하고 있으며, 특히 중국에서 만든 서보 모터와 센서는 예산에 제약이 있는 학교에 대한 액세스를 넓히고 있습니다. 동아시아, 유럽, 북미의 정책 입안자들은 국가의 STEM 과제에 로봇 공학을 통합하여 확실한 수요 파이프라인을 구축하고 있습니다. 한편, 벤처캐피탈은 특별지원 교육, 다국어 컨텐츠 격차, 또는 Robots-as-a-Service 모델을 타겟으로 하는 신흥기업으로 유입되어 경쟁 역학을 재구성하고 있습니다.

세계의 교육용 로봇 시장 동향 및 인사이트

동아시아에서 유아 언어 지도용 AI 대응 소셜 로봇의 채용

대규모 언어 모델 NLP 엔진을 탑재한 로봇이 실시간으로 발음을 교정하고 어린이의 감정적인 신호에 따라 난이도를 조정하는 문화적으로 적응한 언어 레슨을 제공합니다. 관리된 연구에서는 교사 주도의 드릴에 비해 28% 빠르게 어휘가 늘어 34% 높은 정착률을 기록하고 있습니다. 게시자는 새로운 AI 모델을 깜박이기만 하면 동일한 하드웨어를 여러 언어로 이식할 수 있습니다. 이 확장성은 투자자를 매료시키고 지방 자치단체가 교실에 도입을 조성하도록 촉구하며 교육용 로봇 시장의 성장 루프를 강화하고 있습니다. 커리큘럼을 따라 분석 대시보드를 번들하는 공급업체는 프리미엄 가격을 획득하고 있습니다.

유럽 유치원에서 고등학교까지 학교에서 로봇 공학 커리큘럼의 의무화

유럽의 교육부는 현재 초등 및 중등 교육의 전학년에서 로봇 공학의 능력을 요구하고 있으며, 산발적인 시험적 프로그램이 항목별 예산 배분으로 바뀌고 있습니다. 학교는 지도와 평가가 모두 가능한 로봇을 추구하고 있으며, 벤더는 학생과의 상호 작용을 기록하고 과제를 자동 채점하는 안전한 데이터 수집 모듈을 통합하도록 촉구하고 있습니다. 하드웨어 차별화는 희박해지고 있으며, 대신에 컨텐츠의 충실도, 교사 연수 패키지, GDPR(EU 개인정보보호규정)에 준거한 클라우드 아키텍처가 계약 체결의 결정수가 되고 있습니다. 이 정책 전환은 커리큘럼 출판사가 로봇 제조업체와 레슨 플랜을 공동 개발하는 계기로 되어 에코시스템의 록인을 강화하고 교육기관의 스위칭 비용을 인상하고 있습니다.

교실에서 연속 사용시 배터리 팩의 높은 고장률

열대 기후에서는 리튬 이온의 열화가 가속되고, 교실에서의 부하가 걸리면 1년 이내에 38%의 팩이 고장납니다. 고장수리의 사이클은 학교 예산에 부담을 주고 수업 계획에 지장을 초래하기 때문에 구입 의욕이 감퇴합니다. 공급업체는 독이 사용 가능한 경우 DC로 전환하는 하이브리드 전원 아키텍처와 열을 방산하는 수동 냉각 하우징을 지원합니다. 특히 5년간의 라이프사이클 비용을 규정하는 정부 입찰에서는 배터리를 교체하는 설계가 조달 기준으로 부상하고 있습니다. 45°C 환경용 셀을 인증하는 기업은 경쟁 우위를 얻고 있습니다.

부문 분석

2024년 교육용 로봇 시장에서는 비휴머노이드 모델이 68%를 차지했으며, 그 지위는 견고한 단순성과 엔트리 레벨 가격으로 획득되었습니다. Code & Go Mouse와 같은 교실에서 애용되는 모델은 일상적인 취급을 견디고 코딩 개념의 목적을 대규모로 달성합니다. 그러나 휴머노이드 플랫폼은 학교가 특히 자폐증 프로그램에서 더 강력한 참여를 관찰하고 있기 때문에 CAGR 23.4%로 가속하고 있습니다. 조기 채용자는 로봇이 얼굴의 LED와 관절의 컴플라이언스에 의해 감정을 비추는 것으로 더 높은 주의력을 얻을 수 있다고 보고하고 있습니다. 그러므로 휴머노이드의 교육용 로봇 시장 규모는 부품 비용의 감소로 인해 가격 차이가 줄어들고 그 차이의 일부가 줄어들 것으로 예측됩니다.

대규모 언어 모델의 통합을 통해 휴머노이드는 대본이 없는 대화와 동적 피드백을 제공할 수 있습니다. 듀엣 시스템을 사용한 2025년 시험 운영은 숙련도 점수와 얼굴 인식에서 얻은 참여 지표를 연결하여 필요한 경우에만 교사가 개입할 수 있도록 했습니다. 공급업체는 현재 휴머노이드에 언어, 사회성 및 정동 학습, 특별 지원 치료를 위한 커리큘럼을 플러그인하여 출하하고 있습니다. 자본 비용은 여전히 높지만 Robots-as-a-Service와 같은 자금 조달 체계가 도입 장벽을 낮추고 휴머노이드는 틈새 시장에서 충격이 큰 환경에서 빠르게 점유율을 확대합니다.

하드웨어는 2024년 매출의 74%를 차지했는데, 이는 로봇의 구체적인 특성으로 인해 섀시, 센서, 프로세서 및 전원 시스템은 여전히 필수적입니다. 컴포넌트의 혁신은 소형 AI 가속기와 부품 비용을 줄이는 저가형 서보에 집중되어 있습니다. 동시에 서비스 분야도 CAGR 25%로 성장하고 있습니다. 학교가 유지 보수, 소프트웨어 업데이트 및 교사 교육을 다루는 구독 번들로 축발을 옮기기 때문입니다. 공급업체는 월별 요금을 정당화하기 위해 예측 가능한 예산 및 지속적인 기능 업데이트를 강조합니다.

적응 학습 알고리즘, 클라우드 분석 및 컴플라이언스 모듈이 조달을 결정합니다. 그 결과, 하드웨어 마진이 압축되고 기업은 평생 소프트웨어 라이선스를 번들하거나 서비스 계약에 완전히 축발을 옮길 것입니다. 이 시프트는 인센티브를 재구성하고 단발 매출이 아니라 갱신이 수익의 원동력이 되기 때문에 제조업체는 AI의 반복적인 개선에 투자합니다. 지구의 경우, 종량 과금 모델은 설비 투자를 필요로 하지 않으며 교실 비품이 최신 상태로 유지됩니다.

지역 분석

중국, 일본, 한국을 중심으로 아시아태평양이 2024년 수익의 38%를 차지하며 선두에 섰습니다. 베이징의 14차 5개년 계획에서는 로봇 공학의 혁신에 4,520만 달러가 계상되고, 도쿄의 신 로봇 전략에서는 국내 산업의 유지에 4억 4,000만 달러가 투입됩니다. 한국에서는 노동자 1만명당 1,012대라는 높은 로봇 밀도가 숙련 노동자의 풀과 교육 분야의 수용성을 창출하고 있습니다. 심천에 본사를 둔 공급업체는 저비용 부품 키트를 수출하고, 세계 부품표를 압축하며, 아시아 제조업의 교육용 로봇 시장에 대한 영향력을 높이고 있습니다.

중동은 2030년까지 연평균 복합 성장률(CAGR)이 22%로 가장 빠르게 성장할 전망입니다. 사우디아라비아의 Future Intelligence Program은 30,000명의 학생들에게 AI를 교육할 예정이며, SAMAI 이니셔티브는 100만명의 시민을 대상으로 합니다. 기업의 CSR 예산은 공립학교 로봇 실험실을 맡아 조달 병목 현상을 피합니다. 아랍에미리트(UAE)(UAE)은 미국과 아시아의 칩 제조업체와의 제휴를 깊게 해, 공급망의 자립을 목표로 하는 것과 동시에, 두바이와 아부다비를 아랍어의 커리큘럼에 최적화된 다언어 교육 로봇의 실험장으로서 자리매김하고 있습니다.

북미는 성숙하면서도 확대의 일로를 걷습니다. 백악관의 2024 CoSTEM 보고서는 NSF의 로봇 공학 보조금 7,000만 달러와 국방부가 지원하는 1,300개 이상의 FIRST 팀을 확인했습니다. 대학과 산업계의 컨소시엄은 프로토타입에서 교실까지의 사이클을 가속화하고, 텔레프레즌스 로봇은 지방 지구에서의 교사 부족을 다루고 있습니다. GDPR(EU 개인정보보호규정)이 없는 데이터 구조는 클라우드 중심의 분석을 가능하게 하고 유럽에 비해 도입 기간을 단축합니다.

유럽에서는 로봇 교육 커리큘럼이 필수화되어 안정적인 수요가 유지되고 있지만, GDPR(EU 개인정보보호규정)에 대응함으로써 통합 비용이 상승합니다. Horizon Europe는 1억 8,350만 달러를 로봇 공학 연구 개발에 할당하고 독일의 High-Tech Strategy는 3억 6,920만 달러를 교육 용도로 채택하고 있습니다. 공급업체는 데이터 주권 요구 사항을 충족하므로 장치에서 처리를 통합합니다. 북유럽 국가들은 로봇과 학생의 상호작용마다 의사결정 트리를 기록하는 설명 가능한 AI 모듈을 시험적으로 도입하여 타국이 추종하는 벤치마크를 설정하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 동아시아에서 유아용 언어 지도에 대한 AI 대응 소셜 로봇의 도입

- 유럽의 유치원부터 고등학교까지의 학교에서 로봇 공학 커리큘럼의 의무화

- 정부 출자의 STEM 이니셔티브(미국 NSF DRK-12 등)가 대학에서의 조달 촉진

- 중국의 교육 등급 서보 모터 및 센서의 ASP 하락

- 북미에서의 원격 및 하이브리드 학습의 급증이 텔레프레즌스 교육 로봇 견인

- 중동 공립학교의 로보틱스 연구소를 후원하는 기업 CSR 예산

- 시장 성장 억제요인

- 교실에서의 연속 사용에서 배터리 팩의 높은 고장율(열대 지역)

- 비라틴 문자권에서 휴머노이드 로봇용 다언어 컨텐츠 라이브러리의 한계

- EU에서 클라우드 연결 로봇의 GDPR(EU 개인정보보호규정) 주도형 데이터 프라이버시 대응 비용

- 아프리카 농촌에서 공인 로봇 공학 강사의 부족

- 밸류체인 및 공급망 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 투자 분석(자금 조달, Manda, VC 동향)

제5장 시장 규모 및 성장 예측

- 유형별

- 휴머노이드

- 비휴머노이드

- 컴포넌트별

- 하드웨어

- 소프트웨어

- 서비스

- 교육 레벨별

- 프리 프라이머리(유치원)

- 초등교육

- 중등교육

- 고등교육

- 특별교육

- 학습 모드 및 용도별

- 코딩 및 STEM

- 어학 학습

- AI 및 로보틱스 조사

- 특별 지원 요법

- 텔레프레즌스 및 원격지도

- 최종 사용자별

- 학교

- 대학 및 대학

- 직업 훈련 기관

- 에드텍 기업

- 특별 교육 센터

- Maker 스페이스 및 로보틱스 클럽

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 북유럽 국가

- 기타 유럽

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 동남아시아

- 기타 아시아태평양

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임(파트너십, 커리큘럼 제휴, CSR 실험실)

- 시장 점유율 분석

- 기업 프로파일

- SoftBank Robotics Corp.

- UBTECH Robotics Inc.

- Hanson Robotics Ltd.

- Lego Education(The Lego Group)

- Wonder Workshop Inc.

- Robotis Co., Ltd.

- VEX Robotics Inc.

- Makeblock Co., Ltd.

- Sphero Inc.

- Modular Robotics(Cubelets)

- Blue Frog Robotics

- Aisoy Robotics

- Sanbot Innovation(Qihan)

- PAL Robotics

- Probotics America

- Robobuilder Co., Ltd.

- Dash Robotics(Kamigami)

- RobotLAB Inc.

- DJI RoboMaster

- Ozobot and Evollve Inc.

- Fischertechnik GmbH

- RoboTerra Inc.

- Roborisen(e-Bo)

- RoboSense(Edu)

제7장 시장 기회 및 향후 전망

AJY 25.11.12The educational robot market size stands at USD 1.8 billion in 2025 and is forecast to reach USD 3.98 billion by 2030, reflecting a brisk 17.2% CAGR during the period.

Rapid integration of large-language-model AI is turning classroom robots into adaptive learning companions that adjust content and pacing in real time. Hardware prices are falling-especially for China-sourced servomotors and sensors-broadening access for budget-constrained schools. Policymakers in East Asia, Europe, and North America are embedding robotics in national STEM agendas, creating assured demand pipelines. Meanwhile, venture capital is flowing to startups that target special education, multilingual content gaps, or Robots-as-a-Service models, reshaping competitive dynamics.

Global Educational Robot Market Trends and Insights

Adoption of AI-enabled Social Robots for Early-Childhood Language Tutoring in East Asia

Robots equipped with large-language-model NLP engines now deliver culturally adaptive language lessons that correct pronunciation in real time and adjust difficulty based on a child's emotional cues. Controlled studies record 28% faster vocabulary gains and 34% higher retention than teacher-led drills. Publishers are porting the same hardware to multiple languages simply by flashing new AI models, enabling manufacturers to chase diverse markets without redesign costs. This scalability is enticing investors and encouraging local governments to subsidize classroom deployments, thereby reinforcing the growth loop for the educational robot market. Suppliers that bundle curriculum-aligned analytics dashboards are capturing premium pricing because schools value quantifiable progress tracking.

Mandatory Robotics Curriculum in K-12 Schools across Europe

European ministries of education now require robotics competencies throughout primary and secondary grades, which has turned sporadic pilot programs into line-item budget allocations. Schools increasingly solicit robots that can both teach and assess, prompting vendors to integrate secure data-collection modules that record student interactions and auto-grade tasks. Hardware differentiation is fading; instead, content depth, teacher-training packages and GDPR-compliant cloud architectures decide contract awards. The policy shift is also inspiring curriculum publishers to co-develop lesson plans with robot makers, tightening ecosystem lock-in and raising switching costs for institutions.

High Failure Rates of Battery Packs in Continuous Classroom Use

In tropical climates, lithium-ion degradation accelerates, with 38% of packs failing within a year under classroom load. Break-fix cycles strain school budgets and disrupt lesson plans, dampening purchase enthusiasm. Suppliers respond with hybrid power architectures that switch to direct current when docks are available and with passive cooling housings to dissipate heat. Battery-swap designs are emerging as a procurement criterion, especially in government tenders that stipulate five-year life-cycle costs. Companies that certify cells for 45 °C environments gain a competitive edge.

Other drivers and restraints analyzed in the detailed report include:

- Government-Funded STEM Initiatives Fueling University Procurement

- Falling ASP of Education-grade Servo Motors & Sensors in China

- Limited Multilingual Content Libraries for Humanoid Robots

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Non-humanoid models retained 68% of the educational robot market in 2024, a position earned through rugged simplicity and entry-level pricing. Classroom favorites such as the Code & Go Mouse withstand daily handling and fulfill coding-concept objectives at scale. Yet, humanoid platforms are accelerating at a 23.4% CAGR as schools observe stronger engagement, especially in autism programs. Early adopters report higher attention spans when robots mirror emotions via facial LEDs and compliant joints. The educational robot market size for humanoids is therefore forecast to close part of the gap as falling part costs narrow the price delta.

Large-language-model integration lets humanoids deliver unscripted dialogue and dynamic feedback. A 2025 pilot using the Duet system linked proficiency scores to facial-recognition-derived engagement metrics, enabling teachers to intervene only when needed. Suppliers now ship humanoids with plug-in curricula for language, social-emotional learning, and special-needs therapy. Although capital costs remain higher, financing schemes such as Robots-as-a-Service lower adoption barriers, positioning humanoids for rapid share gains in niche, high-impact settings.

Hardware accounted for 74% of 2024 revenue due to the tangible nature of robots-chassis, sensors, processors and power systems remain indispensable. Component innovation centers on compact AI accelerators and low-cost servos that reduce bill-of-materials outlays. Simultaneously, the services segment is growing at 25% CAGR as schools pivot to subscription bundles covering maintenance, software updates and teacher training. Vendors highlight predictable budgeting and continual feature refreshes to justify monthly fees.

Software, while a smaller slice, is the value engine: adaptive-learning algorithms, cloud analytics and compliance modules now decide procurement. As a result, hardware margins compress, and firms bundle lifetime software licences or pivot entirely to service contracts. This shift realigns incentives-manufacturers invest in iterative AI improvements because renewals, not one-off sales, drive revenue. For districts, the pay-as-you-go model frees capex and ensures that classroom fleets stay current.

Educational Robots Market Report is Segmented by Type (Humanoid, Non-Humanoid), Component (Hardware, Software and Services), Education Level (Primary Education, Secondary Education, Higher Education and More), Learning Mode / Application (Coding and STEM, Language Learning, Special-Needs Therapy and More), End User (Schools, Universities and Colleges, and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led with 38% revenue in 2024, anchored by China, Japan and South Korea. Beijing's 14th Five-Year Plan earmarks USD 45.2 million for robotics innovation, while Tokyo's New Robot Strategy deploys USD 440 million to sustain its domestic industry. High robot density-1,012 units per 10,000 workers in Korea-creates a skilled labor pool and a receptive education sector. Shenzhen-based suppliers export low-cost component kits, compressing global bill-of-materials and elevating Asia's manufacturing influence on the educational robot market.

The Middle East records the fastest CAGR at 22% to 2030. Saudi Arabia's Future Intelligence Program intends to train 30,000 students in AI, and the SAMAI initiative targets 1 million citizens. Corporate CSR budgets underwrite robotics labs in public schools, sidestepping procurement bottlenecks. The UAE deepens alliances with US and Asian chipmakers, seeking supply-chain independence and positioning Dubai and Abu Dhabi as testing grounds for multilingual educational robots optimized for Arabic curricula.

North America remains a mature yet expanding arena. The White House's 2024 CoSTEM report confirms USD 70 million in NSF robotics grants and over 1,300 Department of Defense-backed FIRST teams. University-industry consortia accelerate prototype-to-classroom cycles, and telepresence robots address teacher shortages in rural districts. GDPR-free data regimes allow cloud-centric analytics, shortening deployment times relative to Europe.

Europe's mandatory robotics curricula sustain steady demand, but GDPR compliance raises integration costs. Horizon Europe assigns USD 183.5 million to robotics R&D, and Germany's High-Tech Strategy channels USD 369.2 million into educational applications. Vendors embed on-device processing to satisfy data-sovereignty requirements. Nordic countries pilot explainable-AI modules that log decision trees for every robot-student interaction, setting a benchmark others may follow.

- SoftBank Robotics Corp.

- UBTECH Robotics Inc.

- Hanson Robotics Ltd.

- Lego Education (The Lego Group)

- Wonder Workshop Inc.

- Robotis Co., Ltd.

- VEX Robotics Inc.

- Makeblock Co., Ltd.

- Sphero Inc.

- Modular Robotics (Cubelets)

- Blue Frog Robotics

- Aisoy Robotics

- Sanbot Innovation (Qihan)

- PAL Robotics

- Probotics America

- Robobuilder Co., Ltd.

- Dash Robotics (Kamigami)

- RobotLAB Inc.

- DJI RoboMaster

- Ozobot and Evollve Inc.

- Fischertechnik GmbH

- RoboTerra Inc.

- Roborisen (e-Bo)

- RoboSense (Edu)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of AI-enabled Social Robots for Early-Childhood Language Tutoring in East Asia

- 4.2.2 Mandatory Robotics Curriculum in K-12 Schools across Europe

- 4.2.3 Government-funded STEM Initiatives (e.g., US NSF DRK-12) Fueling University Procurement

- 4.2.4 Falling ASP of Education-grade Servo Motors and Sensors in China

- 4.2.5 Surge of Remote/Hybrid Learning Driving Telepresence Teaching Robots in North America

- 4.2.6 Corporate CSR Budgets Sponsoring Robotics Labs in Middle-East Public Schools

- 4.3 Market Restraints

- 4.3.1 High Failure Rates of Battery Packs in Continuous Classroom Use (Tropical Regions)

- 4.3.2 Limited Multilingual Content Libraries for Humanoid Robots in Non-Latin Script Nations

- 4.3.3 GDPR-Driven Data-privacy Compliance Costs for Cloud-connected Robots in EU

- 4.3.4 Shortage of Certified Robotics Instructors in Rural Africa

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Investment Analysis (Funding, MandA, VC Trends)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Humanoid

- 5.1.2 Non-humanoid

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Education Level

- 5.3.1 Pre-primary (Kindergarten)

- 5.3.2 Primary Education

- 5.3.3 Secondary Education

- 5.3.4 Higher Education

- 5.3.5 Special Education

- 5.4 By Learning Mode / Application

- 5.4.1 Coding and STEM

- 5.4.2 Language Learning

- 5.4.3 AI and Robotics Research

- 5.4.4 Special-needs Therapy

- 5.4.5 Telepresence and Remote Instruction

- 5.5 By End User

- 5.5.1 Schools

- 5.5.2 Universities and Colleges

- 5.5.3 Vocational Institutes

- 5.5.4 Ed-Tech Companies

- 5.5.5 Special-education Centers

- 5.5.6 Maker Spaces and Robotics Clubs

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Nordics

- 5.6.3.6 Rest of Europe

- 5.6.4 Middle East

- 5.6.4.1 United Arab Emirates

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 Turkey

- 5.6.4.4 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 Asia-Pacific

- 5.6.6.1 China

- 5.6.6.2 Japan

- 5.6.6.3 South Korea

- 5.6.6.4 India

- 5.6.6.5 Southeast Asia

- 5.6.6.6 Rest of Asia-Pacific

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (Partnerships, Curriculum Alliances, CSR Labs)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)}

- 6.4.1 SoftBank Robotics Corp.

- 6.4.2 UBTECH Robotics Inc.

- 6.4.3 Hanson Robotics Ltd.

- 6.4.4 Lego Education (The Lego Group)

- 6.4.5 Wonder Workshop Inc.

- 6.4.6 Robotis Co., Ltd.

- 6.4.7 VEX Robotics Inc.

- 6.4.8 Makeblock Co., Ltd.

- 6.4.9 Sphero Inc.

- 6.4.10 Modular Robotics (Cubelets)

- 6.4.11 Blue Frog Robotics

- 6.4.12 Aisoy Robotics

- 6.4.13 Sanbot Innovation (Qihan)

- 6.4.14 PAL Robotics

- 6.4.15 Probotics America

- 6.4.16 Robobuilder Co., Ltd.

- 6.4.17 Dash Robotics (Kamigami)

- 6.4.18 RobotLAB Inc.

- 6.4.19 DJI RoboMaster

- 6.4.20 Ozobot and Evollve Inc.

- 6.4.21 Fischertechnik GmbH

- 6.4.22 RoboTerra Inc.

- 6.4.23 Roborisen (e-Bo)

- 6.4.24 RoboSense (Edu)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis