|

시장보고서

상품코드

1851912

토크 센서 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Torque Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

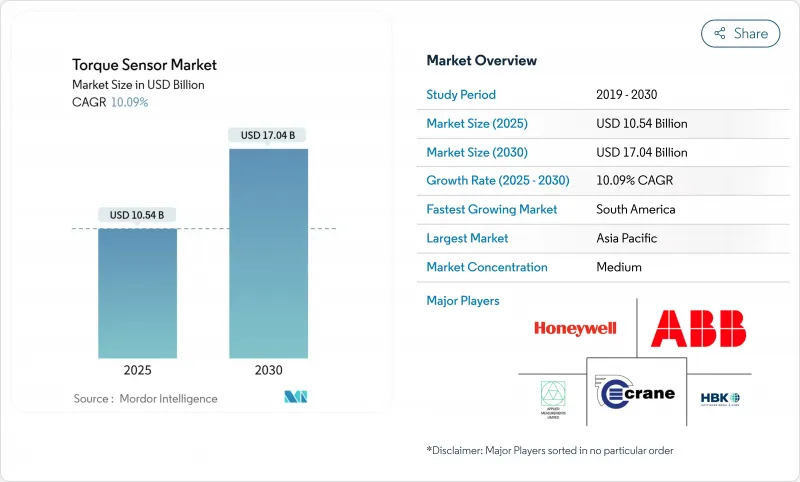

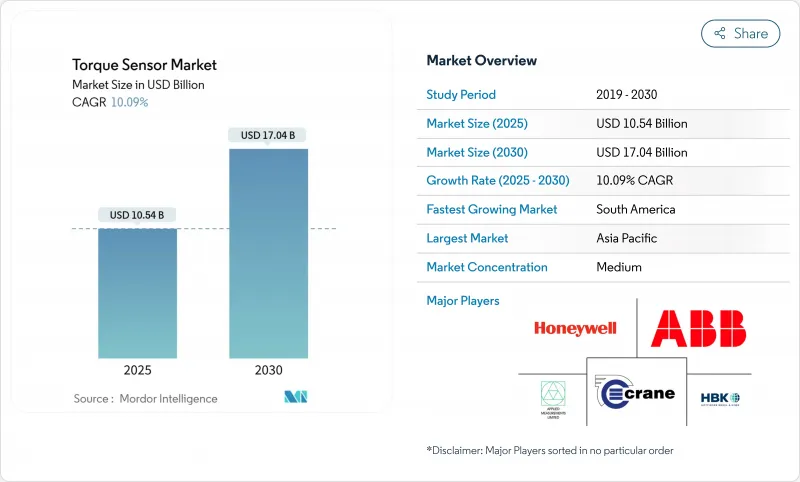

세계의 토크 센서 시장 규모는 2025년에 105억 4,000만 달러로 추정되고, 2030년에는 170억 4,000만 달러에 이를 전망이며, CAGR 10.09%로 성장할 것으로 예측됩니다.

그 기세를 뒷받침하는 것은 자동차 파워트레인의 급속한 전동화, 산업 자동화의 심화, 인프라, 에너지, 의료기기에서의 정밀 측정 요건의 엄격화입니다. 자동차의 전동화는 토크 피드백이 전동 파워 스티어링, 드라이브 트레인 제어, 첨단 운전 지원 기능에 필수적이어서 수요를 지속적으로 지원했습니다. 협동 로봇의 성장도 병행하여 진행되어 1대 당 센서 탑재량이 증가하여 e-bike 및 기타 마이크로모빌리티 플랫폼은 대량 생산 및 저비용의 기회를 늘렸습니다. 공급업체는 원시 정확도에서 전자기 간섭 내성, 무선 원격 측정, 예측 분석 플랫폼과의 통합으로 차별화를 이동했습니다. 인도와 남미의 지역 조달 이니셔티브는 중국산 희토류에 대한 의존을 완화하기 위해 노력했지만, 고품위 자기 탄성 합금 공급망에 대한 노출은 여전히 제한 요인이었습니다.

세계의 토크 센서 시장 동향 및 인사이트

파워 스티어링(EPS) 시스템의 전동화

전동 파워 스티어링의 토크 감시가 의무화되어 경기 감속 시에도 수요가 확대되었습니다. 2024년에 발행된 유럽 규제에서는 자율주행에 대응하기 위해 스티어링 토크 피드백의 지속이 의무화되었으며, 모든 EPS 유닛에 적어도 하나의 센서를 통합해야 했습니다. OEM은 기능 안전 목표를 충족하기 위해 이중 중복 설계를 채택했으며 차량당 센서 양이 실질적으로 두 배로 증가했습니다. Vitesco와 같은 공급업체는 EPS 토크 감지를 반자율 주행 차선 유지 및 운전자의 의사 예측을 위한 핵심 인에이블러로 꼽았습니다. 동일한 데이터 채널은 무선 분석에서 재사용되며 통합자의 평생 서비스 수익을 증가시킵니다. 기존의 유압식 스티어링 플랫폼이 쇠퇴함에 따라 대응 가능한 자동차 기반은 돌이킬 수 없게 EPS 아키텍처로 이동했습니다.

제조업 자동화 및 Cobot의 상승

협동 로봇은 ISO 10218의 안전 제한을 준수하기 위해 순간적인 토크 검출을 필요로 했으며, 코봇 출하량과 센서 유닛 사이에 일대일 관계가 생겼습니다. 2024년에는 전통적인 산업용 로봇을 뛰어넘는 코봇의 세계 판매량이 늘어나 전자기기, 식품, 경량 조립 라인용 EMI 내성 다축 토크 센서가 급성장했습니다. 인증 지침에 따라 중복 감지가 의무화되었으며 각 로봇의 부품 비용이 효과적으로 인상되었습니다. 폴란드의 중소기업에서 2024년의 보급률은 26%에 그쳤으며, 이는 유럽 제조업에 잠재할 수 있는 큰 가능성을 보여줍니다. 장기적인 영향은 스마트 워크셀이 섬유 공장이나 농산물 가공 공장에 보급됨에 따라 개별 자동화에만 그치지 않습니다.

자동차 양산 프로그램의 가격 감응도

OEM의 비용 절감 목표는 주요 EV 플랫폼에서 센서 가격을 단위당 50달러에 가깝게 제한하고 공급업체가 보조 기능을 제거하도록 압력을 받고 있습니다. 배터리 팩의 비용을 상쇄할 필요성으로 인해 모든 드라이브 트레인 컴포넌트에 대한 모니터링이 강화되어 플랫폼 표준화로 사양의 상품화가 진행되었습니다. 2024년 희토류 자석 공급 중단은 딜레마를 악화시켰고 인도와 남미의 자동차 제조업체들은 정확도가 떨어질 위험이 있는 대체 재료를 고려해야 했습니다. 공급업체는 모듈식 전자제품에 대항하여 프리미엄 트림을 위한 옵션 컨디셔닝 보드를 가능하게 하는 반면, 엔트리 변형을 위한 저비용 코어를 유지했습니다.

부문 분석

2024년 토크 센서 시장 점유율은 드라이브 트레인, 풍력 터빈 및 공정 제어 분야에서 회전형 유닛이 65.5%를 차지했습니다. 회전 장치는 EV 및 터빈의 폐쇄 루프 제어를 지원하는 연속적인 현장 측정을 제공합니다. 리액션 유형은 머시닝이나 배터리 셀의 랩 공정에서 자동 테스트 스탠드가 보급되었기 때문에 베이스는 작은 반면, CAGR 11.8%를 기록했습니다. 디지털 텔레메트리는 슬립 링을 제거하여 회전 설계를 향상시키고 가혹한 산업 환경에서의 신뢰성을 높였습니다.

회전 센서는 엣지 컴퓨팅 노드로 진화하여 예측 유지 보수를 위해 클라우드 대시보드로 데이터를 스트리밍합니다. 인프로세스 가공에서는 공구 마모를 나타내는 토크 스파이크를 잡는 리액션 유닛이 채용되어 항공우주 구조물의 밀링 가공에 있어서의 제로 결함 프로그램이 진전되었습니다. 토크 센서 시장은 OEM이 추적성 의무화에 대응하기 위해 구식 조립 라인을 개조함으로써 혜택을 받았으며 두 센서 카테고리 모두 병렬로 성장을 유지할 수 있도록 보장했습니다.

스트레인 게이지는 2024년에 48.3%의 매출을 유지했으며, 비용과 입증된 견고성을 지지했습니다. 그러나 SAW 센서는 13.2%의 연평균 복합 성장률(CAGR)을 기록해 EMI 내성과 무선 데이터가 가장 중요한 분야에서 점유율을 확대했습니다. 광섬유는 나노 라디안의 분해능이 프리미엄 가격을 정당화하는 실험실 및 항공우주 기관의 교정을 목표로 합니다.

2024년 SAW 혁신은 1,000℃의 온도 내성과 10마이크로미터의 변위 분해능을 달성했습니다. 이러한 능력은 가스 터빈과 후카이도 드릴링과 같은 극한 환경 시장을 개척했습니다. 따라서 토크 센서 시장은 기술의 이분화를 목격하고 있습니다. 즉, 상품화된 자동차 스티어링을 위한 저비용 스트레인 게이지와 위험 또는 미션 크리티컬한 틈새 시장을 위한 고가치의 SAW 또는 광학 장치입니다.

지역 분석

아시아태평양은 2024년 매출의 36.3%를 차지했으며, 자동차 조립, 반도체 제조, 로봇 공학의 고밀도 실장으로 주도권을 유지했습니다. 중국은 EPS 생산량을 선도하고, 일본은 고정밀 스트레인 게이지 기판을 공급하며, 한국의 전자공학은 배터리와 디스플레이 라인에 고분해능 토크 피드백을 도입했습니다. 인도는 희토류 자석의 국산화를 추진하고 2026년까지 연간 500톤의 생산 능력을 목표로 하여 이 지역 전체의 원재료 위험이 완화될 것으로 기대됩니다.

북미는 항공우주 및 방위 인티그레이터가 엔진 시험에 고온 광학 센서를 채용해 프리미엄 틈새를 유지했습니다. 미국의 EV 신흥기업은 진보된 토크 제어 루프를 필요로 하는 축류 모터를 활용하여 SAW와 자기 탄성 디바이스에 대한 수요를 끌어올렸습니다. 멕시코는 자동차 수출의 허브로서의 역할이 증가하고 있으며, 스티어링 및 드라이브 트레인 센싱 비용에 중점을 둔 중량 생산 주문이 증가했습니다.

유럽에서는 협동 로봇의 안전 기준과 자동차의 자율 주행 준비 규칙에 토크 계측을 통합하는 규제의 의무화가 꾸준히 진행되었습니다. 독일의 자동화 벤더는 센서 게이트웨이를 프로그래머블 로직 컨트롤러에 통합했으며 프랑스의 원자력 유지보수 계약자는 정전 시 턴어라운드를 가속화하기 위해 무선 토크 헤드를 채택했습니다. 브라질이 선도하는 남미는 OEM이 대규모 테스트 스탠드 계장을 필요로 하는 새로운 프레스 가공 라인과 파워트레인 라인을 설치했기 때문에 가장 빠른 11.4%의 연평균 복합 성장률(CAGR)을 기록했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 파워 스티어링(EPS) 시스템의 전동화

- 제조업에서 자동화 및 코봇의 대두

- E-bike 및 마이크로모빌리티의 생산 급증

- EV 드라이브 트레인용 축류 모터의 용도 확대

- 스마트 풍력 터빈의 온보드 토크 모니터링

- 시장 성장 억제요인

- 자동차 볼륨 프로그램의 가격 감응도

- 전자기 간섭 하에서의 신뢰성 문제

- 고등급 자탄성 합금 공급 병목

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 거시경제 요인의 영향

- 산업 밸류체인 분석

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 반응

- 회전 및 로터리

- 기술별

- 스트레인 게이지

- 자기 탄성

- 광학

- SAW(표면 탄성파)

- 기타

- 용도별

- 자동차

- 항공우주 및 방위

- 산업용 제조 로봇

- 의료 및 헬스케어

- 에너지 및 전력

- 최종 사용자 업계별

- OEM 테스트 스탠드 및 QA

- 인프로세스 모니터링

- 연구개발

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ABB Ltd

- Honeywell International Inc.

- Hottinger Bruel & Kjaer(HBK-Spectris plc)

- TE Connectivity Ltd

- Kistler Instrumente AG

- Infineon Technologies AG

- Norbar Torque Tools Ltd

- Crane Electronics Ltd

- S. Himmelstein & Company Inc.

- Datum Electronics Ltd(Indutrade AB)

- Applied Measurements Ltd

- PCB Piezotronics Inc.(MTS)

- MagCanica Inc.

- Futek Advanced Sensor Technology Inc.

- Forsentek Co. Ltd

- Bota Systems AG

- ATI Industrial Automation(Novanta)

- Althen Sensors & Controls GmbH

- Sensor Technology Ltd(TorqSense)

- Burster Prazisionsmesstechnik GmbH

- Transense Technologies plc(SAWSense)

- Interface Inc.

- Mountz Inc.

- KTR Kupplungstechnik GmbH

- OPKON Optik Elektronik Kontrol San. AS

제7장 시장 기회 및 향후 전망

AJY 25.11.19The global torque sensor market size stood at USD 10.54 billion in 2025 and is forecast to reach USD 17.04 billion by 2030, advancing at a 10.09% CAGR.

Momentum has been underpinned by the rapid electrification of vehicle powertrains, deepening industrial automation, and stricter precision-measurement requirements in infrastructure, energy and medical equipment. Automotive electrification continued to anchor demand as torque feedback became integral to electric power-steering, drivetrain control and advanced driver-assistance functions. Parallel growth in collaborative robots increased the sensor content per machine, while e-bike and other micromobility platforms multiplied high-volume, low-cost opportunities. Vendors shifted differentiation away from raw accuracy toward electromagnetic-interference resilience, wireless telemetry, and integration with predictive-analytics platforms. Supply chain exposure to high-grade magnetoelastic alloys remained a limiting factor, although regional sourcing initiatives in India and South America sought to ease dependence on Chinese rare-earth metals.

Global Torque Sensor Market Trends and Insights

Electrification of Power-Steering (EPS) Systems

Mandated torque monitoring for electric power-steering hardened demand even during economic slow-downs. European regulations issued in 2024 required continuous steering-torque feedback for autonomous-readiness, obligating every EPS unit to embed at least one sensor. OEMs adopted dual-redundant designs to satisfy functional-safety targets, effectively doubling sensor volumes per vehicle. Suppliers such as Vitesco cited EPS torque sensing as a core enabler for semi-autonomous lane-keeping and driver-intention prediction. The same data channel is reused in over-the-air analytics, increasing lifetime service revenue for integrators. As legacy hydraulic steering platforms sunset, the addressable automotive base shifted irreversibly toward EPS architectures.

Rising Automation and Cobots in Manufacturing

Collaborative robots required instantaneous torque detection to comply with ISO 10218 safety limits, creating a one-to-one relationship between cobot shipments and sensor units. Global cobot sales outpaced conventional industrial robots in 2024, inducing a steep ramp in EMI-resistant, multi-axis torque sensors destined for electronics, food and light-assembly lines. Certification guidelines enforced redundant sensing, effectively raising bill-of-materials value for each robot. Penetration remained only 26% among Polish SMEs in 2024, illustrating vast latent upside across European manufacturing. Long-term impact spans beyond discrete automation as smart work-cells propagate into textile and agri-processing plants.

Price Sensitivity in Volume Automotive Programs

OEM cost-down targets capped sensor pricing near USD 50 per unit in mainstream EV platforms, pressuring suppliers to strip auxiliary features. The need to offset battery-pack costs heightened scrutiny of every drivetrain component, with platform standardization further commoditizing specifications. Rare-earth magnet supply disruptions in 2024 exacerbated the dilemma, forcing Indian and South American automakers to weigh substitute materials that risked lower precision. Suppliers countered with modular electronics, allowing optional conditioning boards for premium trims while preserving a low-cost core for entry variants.

Other drivers and restraints analyzed in the detailed report include:

- Surge in E-Bike and Micromobility Production

- Growing Use in Axial-Flux Motors for EV Drivetrains

- Reliability Issues under Electromagnetic Interference

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rotational units captured 65.5% of torque sensor market share in 2024 on the strength of drivetrain, wind-turbine and process-control deployments. They offered continuous, in-situ measurement that supported closed-loop control in EVs and turbines. Reaction types, while smaller in base, posted an 11.8% CAGR as automated test-stands proliferated across machining and battery-cell wrap processes. Digital telemetry elevated rotational designs by removing slip rings, boosting reliability in harsh industrial settings.

Rotational sensors evolved into edge-computing nodes, streaming data to cloud dashboards for predictive maintenance. In-process machining adopted reaction units to catch torque spikes indicative of tool wear, advancing zero-defect programs in aerospace structural milling. The torque sensor market benefits as OEMs retrofit older assembly lines to meet traceability mandates, ensuring both sensor categories sustain parallel growth.

Strain-gauges retained 48.3% revenue in 2024, favored for cost and proven ruggedness. Yet, SAW sensors recorded a 13.2% CAGR and gained share where EMI immunity and wireless data mattered most. Magnetoelastic variants served sealed, non-contact duties in pump shafts, whereas optical fibers targeted lab and aerospace calibration where nano-radian resolution justified premium pricing.

SAW innovations in 2024 achieved temperature tolerance to 1,000 °C and 10 µm displacement resolution. Such capabilities unlocked extreme-environment markets like gas turbines and deep-well drilling. The torque sensor market thus witnessed technology bifurcation: low-cost strain-gauges for commoditized automotive steering, and high-value SAW or optical units for hazardous or mission-critical niches.

The Global Torque Sensor Market Report is Segmented by Product Type (Reaction Torque Sensors, Rotational/Rotary Torque Sensors), Technology (Strain-Gauge, Magnetoelastic, and More), Application (Automotive, Aerospace and Defense, and More), End-User Industry (OEM Test-Stand and QA, In-Process Monitoring, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 36.3% of 2024 revenue and sustained leadership through dense automotive assembly, semiconductor fabrication and robotics adoption. China led EPS volumes, Japan supplied precision strain-gauge substrates, and South Korea's electronics majors deployed high-resolution torque feedback in battery and display lines. India's push to localize rare-earth magnet production, with 500-tonne annual capacity targeted by 2026, promised to moderate raw-material risk across the region.

North America maintained its premium niche as aerospace and defense integrators employed high-temperature optical sensors for engine testing. US EV start-ups leveraged axial-flux motors requiring sophisticated torque control loops, bolstering demand for SAW and magnetoelastic devices. Mexico's growing role as an automotive export hub amplified mid-volume, cost-sensitive orders for steering and drivetrain sensing.

Europe advanced steadily on regulatory mandates that embedded torque measurement into collaborative robot safety standards and vehicle autonomous-readiness rules. Germany's automation vendors integrated sensor gateways into programmable-logic controllers, while France's nuclear maintenance contractors adopted wireless torque heads to accelerate outage turnarounds. South America, led by Brazil, posted the fastest 11.4% CAGR as OEMs installed new stamping and powertrain lines requiring extensive test-stand instrumentation.

- ABB Ltd

- Honeywell International Inc.

- Hottinger Bruel & Kjaer (HBK - Spectris plc)

- TE Connectivity Ltd

- Kistler Instrumente AG

- Infineon Technologies AG

- Norbar Torque Tools Ltd

- Crane Electronics Ltd

- S. Himmelstein & Company Inc.

- Datum Electronics Ltd (Indutrade AB)

- Applied Measurements Ltd

- PCB Piezotronics Inc. (MTS)

- MagCanica Inc.

- Futek Advanced Sensor Technology Inc.

- Forsentek Co. Ltd

- Bota Systems AG

- ATI Industrial Automation (Novanta)

- Althen Sensors & Controls GmbH

- Sensor Technology Ltd (TorqSense)

- Burster Prazisionsmesstechnik GmbH

- Transense Technologies plc (SAWSense)

- Interface Inc.

- Mountz Inc.

- KTR Kupplungstechnik GmbH

- OPKON Optik Elektronik Kontrol San. A.S.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification of Power-Steering (EPS) systems

- 4.2.2 Rising Automation and Cobots in Manufacturing

- 4.2.3 Surge in E-bike and Micromobility Production

- 4.2.4 Growing Use in Axial-Flux Motors for EV Drivetrains

- 4.2.5 On-board Torque Monitoring in Smart Wind Turbines

- 4.3 Market Restraints

- 4.3.1 Price Sensitivity in Volume Automotive Programs

- 4.3.2 Reliability Issues under Electromagnetic Interference

- 4.3.3 Supply Bottlenecks for High-Grade Magnetoelastic Alloys

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

- 4.9 Industry Value-Chain Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Reaction

- 5.1.2 Rotational / Rotary

- 5.2 By Technology

- 5.2.1 Strain-Gauge

- 5.2.2 Magnetoelastic

- 5.2.3 Optical

- 5.2.4 SAW (Surface Acoustic Wave)

- 5.2.5 Others

- 5.3 By Application

- 5.3.1 Automotive

- 5.3.2 Aerospace and Defense

- 5.3.3 Industrial Manufacturing and Robotics

- 5.3.4 Medical and Healthcare

- 5.3.5 Energy and Power

- 5.4 By End-User Industry

- 5.4.1 OEM Test-Stand and QA

- 5.4.2 In-Process Monitoring

- 5.4.3 Research and Development

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Honeywell International Inc.

- 6.4.3 Hottinger Bruel & Kjaer (HBK - Spectris plc)

- 6.4.4 TE Connectivity Ltd

- 6.4.5 Kistler Instrumente AG

- 6.4.6 Infineon Technologies AG

- 6.4.7 Norbar Torque Tools Ltd

- 6.4.8 Crane Electronics Ltd

- 6.4.9 S. Himmelstein & Company Inc.

- 6.4.10 Datum Electronics Ltd (Indutrade AB)

- 6.4.11 Applied Measurements Ltd

- 6.4.12 PCB Piezotronics Inc. (MTS)

- 6.4.13 MagCanica Inc.

- 6.4.14 Futek Advanced Sensor Technology Inc.

- 6.4.15 Forsentek Co. Ltd

- 6.4.16 Bota Systems AG

- 6.4.17 ATI Industrial Automation (Novanta)

- 6.4.18 Althen Sensors & Controls GmbH

- 6.4.19 Sensor Technology Ltd (TorqSense)

- 6.4.20 Burster Prazisionsmesstechnik GmbH

- 6.4.21 Transense Technologies plc (SAWSense)

- 6.4.22 Interface Inc.

- 6.4.23 Mountz Inc.

- 6.4.24 KTR Kupplungstechnik GmbH

- 6.4.25 OPKON Optik Elektronik Kontrol San. A.S.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment