|

시장보고서

상품코드

1906971

말레이시아의 석유 및 가스 : 시장 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Malaysia Oil And Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

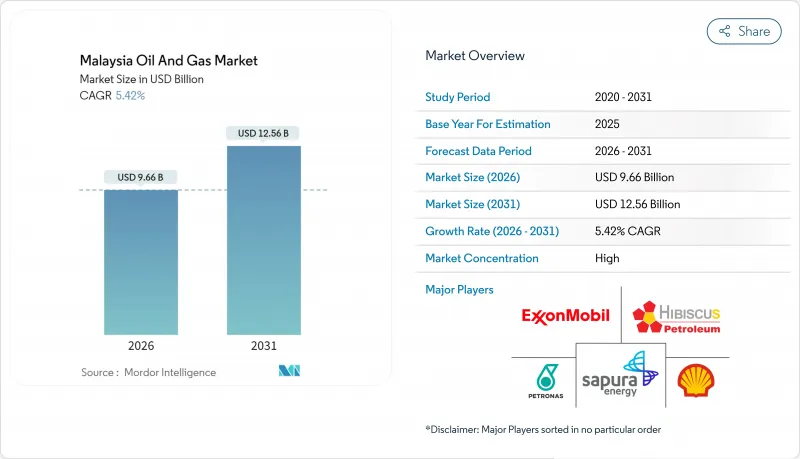

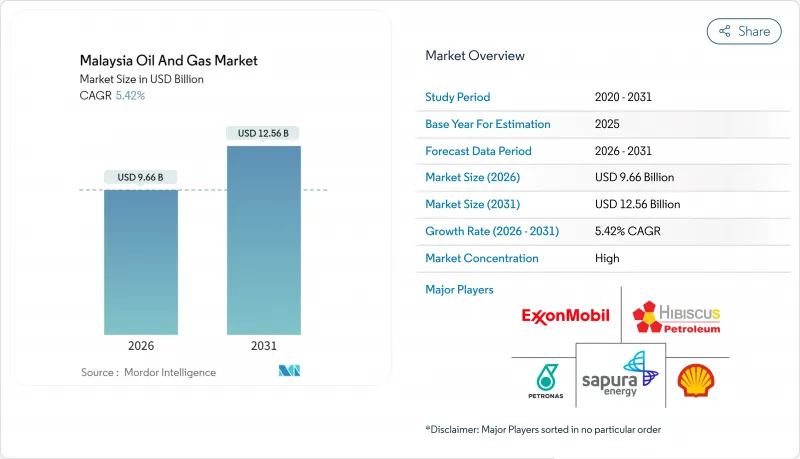

말레이시아의 석유 및 가스 시장 규모는 2026년 96억 6,000만 달러로 평가되었고, 2025년 91억 6,000만 달러에서 성장할 것으로 예측됩니다.

2031년에 125억 6,000만 달러에 이를 것으로 보이며, 2026-2031년에 걸쳐 연평균 복합 성장률(CAGR) 5.42%로 성장할 전망입니다.

말레이시아의 석유 및 가스 시장의 강력한 성장 전망은 심해 탐사, 다운스트림 석유화학 통합, 확대되는 탄소 관리 파이프라인에 대한 상당한 투자에서 비롯됩니다. 페트로나스의 통합 가치사슬 기반은 원료 공급 안정성을 확보하는 한편, 생산분배계약(PSC) 개정은 국제 파트너 유치에 계속 기여하고 있습니다. 사라왁과 사바의 해상 유전 지역은 증산량을 제공할 예정이며, 신규 LNG 공급 계약은 말레이시아의 지역 가스 허브 역할을 유지합니다. 한편, 건설적인 재정 조건과 프로젝트 준비가 완료된 반도의 인프라가 석유화학 설비 증설을 가속화하며, 말레이시아 석유·가스 시장을 동남아시아 에너지 중심지로 공고히 하고 있습니다.

말레이시아의 석유 및 가스 시장 동향과 전망

정제 석유 제품 수요 급증

동남아시아 전역에서 지역 연료 소비 회복과 새로운 모빌리티 트렌드가 정유소 가동률을 촉진하고 있습니다. 2024년 11월 상업 가동을 시작한 펭거랑 통합 단지는 일일 30만 배럴의 생산 능력을 바탕으로, 말레이시아 반도가 인도네시아, 베트남, 필리핀의 공급 부족 시장을 충족시키려는 목표를 뒷받침하고 있습니다. 페트로나스 케미컬스는 2026년 완공 예정인 연간 3만 3,000톤 규모의 화학 재활용 플랜트를 건설 중이며, 이는 다운스트림 산업에 순환 경제 관행을 도입하는 계기가 될 것입니다. 이러한 프로젝트들은 업스트림 생산자들의 원유 확보를 보장하며, 말레이시아를 단순한 원유 수출국이 아닌 가공 허브로 자리매김하게 합니다.

사라왁과 사바의 미개발 심해 매장량

랑카수카(Langkasuka) 및 라양라양(Layang-Layang) 클러스터의 개척 지역은 고사양 시추 장비, 해저 연결관, 부유식 LNG 설비가 필요한 상당한 규모의 가스 및 콘덴세이트 잠재력을 보유하고 있습니다. 말레이시아 입찰 라운드 2025(Malaysia Bid Round 2025)는 투자 촉진을 위해 5개 탐사 블록과 3개 개발 및 위험 분담 옵션(Development and Risk-sharing Option) 클러스터를 선정했습니다. 코노코필립스(ConocoPhillips)와 쉘(Shell)은 LNG 원료 공급 안정성을 극대화하기 위해 포트폴리오 자본을 가스 중심 개발 사업으로 전환했습니다. 안정적인 생산분배계약(PSC) 체계와 페트로나스의 자원 관리자로서의 역할은 발견부터 첫 가스 생산까지의 리드 타임을 단축시켜 말레이시아 석유·가스 시장의 장기적 경쟁력을 강화합니다.

원유 가격의 변동성

2024-2025년 배럴당 70-90달러 사이의 브렌트유 가격 변동은 현금 흐름 계획을 방해하고 일부 최종 투자 결정을 연기하며 차입 비용을 증가시켰습니다. 소규모 유전의 경제성은 가격 하락에 여전히 민감하며, 특히 고비용 가스 리프트나 화학 주입이 필요한 증산 기술 적용 시 더욱 그렇다. 말레이시아 석유·가스·에너지 서비스 협회의 재정 지원 요청은 시장 변동성에 대한 노출을 강조합니다. 헤징과 비용 최적화가 도움이 되지만, 지속적인 변동성은 심해 개발 및 해체 작업 추진 속도를 늦출 수 있습니다.

부문 분석

업스트림 부문은 견조한 생산 분여 계약(PSC) 활동과 페트로나스의 프로젝트 파이프라인에 의해 지원되었으며, 2025년 말레이시아 석유 및 가스 시장 규모의 74.85%를 차지했습니다. Jerun, Kasawari 및 Gumusut-Kakap 재개발 프로젝트는 자연 감산율을 상쇄하면서 안정적인 생산량을 유지하고 있습니다. 말레이시아 석유·가스 시장의 업스트림 부문 점유율 리더십은 가스 응축층이 풍부한 지질 구조와 유전 수익화를 가속화하는 유리한 재정 제도를 반영합니다.

국제 운영사들이 심해 유정 및 한계 재개발 프로젝트에서 면적을 확보함에 따라 업스트림 부문 투자 모멘텀은 2031년까지 지속될 전망입니다. 동시에, 2027년 사바-사라왁 가스 파이프라인이 폐기되면 미드스트림 사업자들은 동말레이시아 가스의 대체 수송 경로 확보라는 과제에 직면하게 됩니다. 업스트림 부문 병목 현상 해소로 증가된 콘덴세이트 물량이 펭거랑의 개질기에 공급되면, 다운스트림 업체들은 새로운 원료 공급의 혜택을 누리게 됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 정제 석유 제품에 대한 수요의 급증

- 미개발 심해 매장량(사라왁주 및 사바)

- 인센티브에 근거한 생산 분여 계약(PSC) 개정 및 재정 조건

- 아시아 LNG 수요 증가로 인한 말레이시아 수출 확대

- CCUS 및 블루 수소 프로젝트의 파이프라인

- 다운스트림 석유화학 통합 추진 모멘텀

- 시장 성장 억제요인

- 원유 가격 변동성 증가

- 글로벌 에너지 전환 투자 전환

- ESG 기반 자본 조달 제약

- 노후화된 해양 인프라 및 운영 비용 상승

- 공급망 분석

- 규제 상황

- 기술의 전망

- 원유 생산, 소비 전망

- 천연가스의 생산, 소비 전망

- 설치된 파이프라인 용량 분석

- 비재래형 자원의 설비 투자 전망(타이트 오일, 오일 샌드, 심해)

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- PESTEL 분석

제5장 시장 규모와 성장 예측

- 부문별

- 업스트림 부문

- 미드스트림 부문

- 다운스트림 부문

- 지역별

- 육상

- 해상

- 서비스별

- 건설

- 유지보수, 턴 어라운드

- 폐지 조치

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임(M&A, 파트너십, PPA)

- 시장 점유율 분석(주요 기업의 시장 순위, 점유율)

- 기업 프로파일

- Petroliam Nasional Berhad(Petronas)

- Shell plc

- Exxon Mobil Corp.

- Chevron Corp.

- BP plc

- Hibiscus Petroleum Bhd

- Sapura Energy Bhd

- Dialog Group Bhd

- MISC Berhad

- Yinson Holdings Bhd

- PTTEP(Malaysia assets)

- Repsol Exploration(Malaysia) SA

- Lundin Energy Malaysia

- Murphy Oil Corporation(Malaysia)

- Serba Dinamik Holdings

- Velesto Energy Bhd

- Malaysia Marine & Heavy Engineering

- Altus Oil & Gas Malaysia Sdn Bhd

- Petro-Excel Sdn Bhd

- Petro Teguh(M) Sdn Bhd

제7장 시장 기회와 장래의 전망

HBR 26.02.04Malaysia Oil And Gas Market size in 2026 is estimated at USD 9.66 billion, growing from 2025 value of USD 9.16 billion with 2031 projections showing USD 12.56 billion, growing at 5.42% CAGR over 2026-2031.

The strong growth outlook for the Malaysia oil and gas market stems from sizable investments in deep-water exploration, downstream petrochemical integration, and an expanding carbon management pipeline. Petronas' integrated value-chain footprint secures feedstock reliability, while Production Sharing Contract (PSC) revisions continue to attract international partners. Offshore basins in Sarawak and Sabah are set to deliver incremental volumes, and new LNG supply deals preserve Malaysia's role as a regional gas hub. Meanwhile, constructive fiscal terms and project-ready infrastructure in Peninsular Malaysia accelerate petrochemical capacity additions and reinforce the Malaysia oil and gas market as a Southeast Asian energy pivot.

Malaysia Oil And Gas Market Trends and Insights

Surging Demand for Refined Petroleum Products

Regional fuel consumption recovery and new mobility trends stimulate refinery utilization rates across Southeast Asia. The Pengerang Integrated Complex entered commercial service in November 2024 with 300,000 barrels-per-day capacity, underpinning Peninsular Malaysia's aspiration to supply deficit markets in Indonesia, Vietnam, and the Philippines. Petronas Chemicals is constructing a 33,000-tonnes-per-annum chemical recycling plant due in 2026, embedding circular-economy practices into the downstream landscape. These projects lock in crude intake for upstream producers and frame Malaysia as a processing hub rather than a pure exporter of crude.

Untapped Deep-Water Reserves in Sarawak & Sabah

Frontier acreage in the Langkasuka and Layang-Layang clusters offers sizable gas and condensate potential that requires high-spec rigs, subsea tie-backs, and floating LNG solutions. The Malaysia Bid Round 2025 listed five exploration blocks and three Development and Risk-sharing Option clusters to catalyze investment. ConocoPhillips and Shell have shifted portfolio capital toward gas-weighted developments to maximize LNG feedstock security. The stable PSC framework and Petronas' role as resource custodian shorten lead times from discovery to first gas, enhancing the long-term competitiveness of the Malaysia oil and gas market.

High Crude-Price Volatility

Brent fluctuations between USD 70-90 per barrel in 2024-2025 disrupted cash-flow planning, deferred some final investment decisions, and raised borrowing costs. Marginal field economics remain sensitive to price dips, particularly where enhanced recovery requires costly gas lift or chemical injection. The Malaysian Oil, Gas and Energy Services Council's appeal for fiscal relief underscores exposure to market swings. While hedging and cost optimization help, sustained volatility may temper the pace of deep-water and decommissioning commitments.

Other drivers and restraints analyzed in the detailed report include:

- Rising Asian LNG Demand Lifting Malaysian Exports

- Downstream Petrochemical Integration Momentum

- Global Energy-Transition Investment Shift

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The upstream segment captured 74.85% of the Malaysia oil and gas market size in 2025, buoyed by robust PSC activity and Petronas' project pipeline. Jerun, Kasawari, and Gumusut-Kakap Redevelopment sustain plateau output while offsetting natural decline rates. The Malaysian oil and gas market share leadership in upstream activities reflects a geology rich in gas-condensate plays and a supportive fiscal regime that accelerates field monetization.

Upstream investment momentum will likely continue through 2031 as international operators secure acreage in deep-water wells and marginal redevelopments. Concurrently, midstream operators face rerouting challenges once the Sabah-Sarawak Gas Pipeline retires in 2027, requiring alternative evacuation for East Malaysian gas. Downstream players benefit from new feedstock when upstream debottlenecking releases incremental condensate volumes that feed into Pengerang's reformers.

The Malaysia Oil and Gas Market Report is Segmented by Sector (Upstream, Midstream, and Downstream), Location (Onshore and Offshore), and Service (Construction, Maintenance and Turn-Around, and Decommissioning). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Petroliam Nasional Berhad (Petronas)

- Shell plc

- Exxon Mobil Corp.

- Chevron Corp.

- BP plc

- Hibiscus Petroleum Bhd

- Sapura Energy Bhd

- Dialog Group Bhd

- MISC Berhad

- Yinson Holdings Bhd

- PTTEP (Malaysia assets)

- Repsol Exploration (Malaysia) S.A.

- Lundin Energy Malaysia

- Murphy Oil Corporation (Malaysia)

- Serba Dinamik Holdings

- Velesto Energy Bhd

- Malaysia Marine & Heavy Engineering

- Altus Oil & Gas Malaysia Sdn Bhd

- Petro-Excel Sdn Bhd

- Petro Teguh (M) Sdn Bhd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for refined petroleum products

- 4.2.2 Untapped deep-water reserves (Sarawak & Sabah)

- 4.2.3 Incentive-driven PSC revisions & fiscal terms

- 4.2.4 Rising Asian LNG demand lifting Malaysian exports

- 4.2.5 CCUS & blue-hydrogen project pipeline

- 4.2.6 Downstream petrochemical integration momentum

- 4.3 Market Restraints

- 4.3.1 High crude-price volatility

- 4.3.2 Global energy-transition investment shift

- 4.3.3 ESG-driven capital access constraints

- 4.3.4 Aging offshore infrastructure & OPEX escalation

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Crude-Oil Production & Consumption Outlook

- 4.8 Natural-Gas Production & Consumption Outlook

- 4.9 Installed Pipeline Capacity Analysis

- 4.10 Unconventional Resources CAPEX Outlook (tight oil, oil sands, deep-water)

- 4.11 Porter's Five Forces

- 4.11.1 Bargaining Power - Suppliers

- 4.11.2 Bargaining Power - Buyers

- 4.11.3 Threat of New Entrants

- 4.11.4 Threat of Substitutes

- 4.11.5 Competitive Rivalry

- 4.12 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Sector

- 5.1.1 Upstream

- 5.1.2 Midstream

- 5.1.3 Downstream

- 5.2 By Location

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 By Service

- 5.3.1 Construction

- 5.3.2 Maintenance and Turn-around

- 5.3.3 Decommissioning

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Petroliam Nasional Berhad (Petronas)

- 6.4.2 Shell plc

- 6.4.3 Exxon Mobil Corp.

- 6.4.4 Chevron Corp.

- 6.4.5 BP plc

- 6.4.6 Hibiscus Petroleum Bhd

- 6.4.7 Sapura Energy Bhd

- 6.4.8 Dialog Group Bhd

- 6.4.9 MISC Berhad

- 6.4.10 Yinson Holdings Bhd

- 6.4.11 PTTEP (Malaysia assets)

- 6.4.12 Repsol Exploration (Malaysia) S.A.

- 6.4.13 Lundin Energy Malaysia

- 6.4.14 Murphy Oil Corporation (Malaysia)

- 6.4.15 Serba Dinamik Holdings

- 6.4.16 Velesto Energy Bhd

- 6.4.17 Malaysia Marine & Heavy Engineering

- 6.4.18 Altus Oil & Gas Malaysia Sdn Bhd

- 6.4.19 Petro-Excel Sdn Bhd

- 6.4.20 Petro Teguh (M) Sdn Bhd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment