|

시장보고서

상품코드

1934581

미국의 석유 및 가스 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Oil And Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

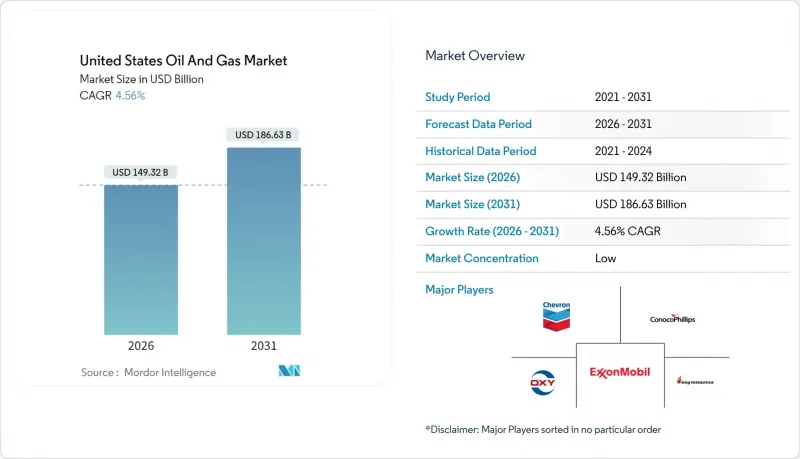

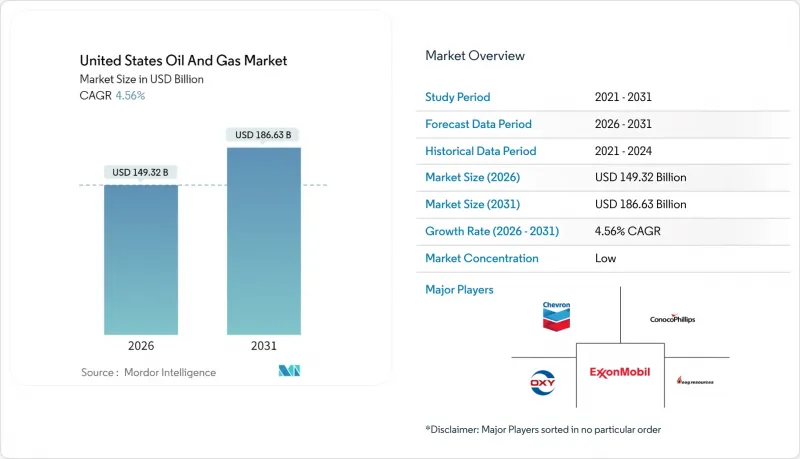

2026년 미국의 석유 및 가스 시장 규모는 1,493억 2,000만 달러로 추정되며, 2025년 1,428억 1,000만 달러에서 성장하여 2031년에는 1,866억 3,000만 달러에 달할 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 4.56%에 달할 것으로 예상됩니다.

타이트 오일층에서의 견조한 시추 생산성, 멕시코만 지역의 액화천연가스(LNG) 플랜트의 빠른 증설, 성숙한 유역에 대한 꾸준한 기술 보급이 이러한 확장을 뒷받침하고 있습니다. 수출 중심의 성장이 내수를 능가하는 구조적 변화가 두드러지고 있으며, 2028년까지 150억 입방피트/일 규모의 신규 LNG 액화 용량이 계획되어 있습니다. 업스트림부문에 대한 재투자는 제한적이지만, 효율성 향상으로 인해 시추장비 수가 감소하는 상황에서도 생산량은 증가하고 있습니다. 한편, 대규모 합병으로 파미안 분지의 광구가 중앙집중화되어 공유 인프라를 통한 비용절감 실현. 이를 통해 손익분기점의 회복력이 강화되고 있습니다.

미국의 석유 및 가스 시장 동향과 인사이트

Permian Basin의 타이트 오일 생산성 향상

첨단 완성 설계와 AI 가이드 시추를 통해 2024년 퍼미안 분지 생산량은 하루 630만 배럴에 달하며, 리그 수가 감소했음에도 불구하고 미국 전체 성장량의 60%를 차지했습니다. 더 긴 횡갱, 더 높은 프로판 충진량, 실시간 파쇄 최적화를 통해 유정당 회수량 증가와 동시에 비용을 절감하고 있습니다. 엑손모빌의 파이오니어 통합은 표준화된 실행과 공유 인프라를 통해 15%의 생산성 향상을 목표로 하고 있습니다. 독립 시추업체들도 경쟁에서 살아남기 위해 비슷한 전략을 채택하고 있습니다. 따라서 효율성 추구가 생산량 증가의 기반이 되어 미국의 석유 및 가스 시장을 가격 변동으로부터 보호하고 있습니다.

급증하는 LNG 수출 능력

새로운 멕시코만 연안의 액화 플랜트 그룹은 국내 공급을 세계 가격 프리미엄과 연결하여 수요 구조를 변화시키고 있습니다. 벤처 월드의 플라크민스 터미널은 2024년 연간 2,000만 톤의 생산능력을 추가할 예정이며, 골든패스(Golden Pass)가 연간 1,560만 톤의 생산능력을 추가할 예정입니다. 수출 급증은 애팔래치아 분지와 헤인즈빌 분지의 시추를 촉진하고, 150억 달러 규모의 신규 파이프라인이 생산량을 남쪽으로 운송할 것입니다. 세계 시장과의 연계성 강화는 헨리허브의 계절적 가격 변동성을 완화하고, 생산자와 미드스티림 사업자의 미래 예측 가능성을 높임과 동시에 미국의 석유 및 가스 시장의 확장을 더욱 촉진할 것입니다.

EPA OOOOb/c에 따른 메탄 배출량 규제 준수 비용

2024년부터는 설정된 기준치를 초과하는 메탄 배출량에 대해 톤당 900달러부터 과징금이 적용되며, 2026년까지 1,500달러까지 인상됩니다. 모니터링 및 복구 프로그램의 추가는 일반적인 셰일 유정의 운영 비용을 배럴당 2-4달러 증가시켜 중소규모의 생산자에게 특히 큰 영향을 미칩니다. 컴플라이언스 대응의 필요성으로 인해 지속적인 누출 감지 기술 등의 신속한 도입과 산업 재편이 가속화되면서 미국의 석유 및 가스 시장의 비용 구조가 변화하고 있습니다.

부문 분석

2025년 기준 업스트림 부문은 미국의 석유 및 가스 시장 규모의 71.85%를 차지할 것으로 예상되며, 2031년까지 연평균 4.84%의 CAGR을 기록할 것으로 전망됩니다. 미드스티림부문은 파이프라인 증설과 LNG 터미널 건설에 힘입어 18.40%를 차지했고, 다운스트림 정제 부문은 생산능력 한계와 배출규제 강화 속에서 9.75%를 유지했습니다. 현재 사업자는 유가 60달러에서 15% 이상의 내부수익률을 목표로 하고 있으며, 고수익 셰일 횡단광구 및 선별된 장기 프로젝트에 자본을 집중하고 있습니다. 코노코필립스의 윌로우 개발 프로젝트는 이러한 전환을 상징하며, 30년 분량의 매장량으로 단기 사이클의 셰일 프로젝트에서는 보기 드문 현금 흐름의 지속성을 제공합니다. 시추 효율성과 체계적인 재투자를 통해 업스트림 부문은 미국의 석유 및 가스 시장에서 지속적인 성장의 중심이 되고 있습니다.

업스트림 부문의 우위는 빠른 생산성 향상으로 손익분기점을 배럴당 40달러 미만으로 유지하고 있는 것에 기인합니다. 미드스티림 부문은 LNG의 성장이 저장 및 운송 수요를 견인하는 기회가 풍부한 분야이지만, 자본 규율이 투기적 프로젝트를 억제하고 있습니다. 다운스트림 부문의 수익률은 재생 디젤과의 경쟁과 규제 대응 비용 상승으로 인해 축소되는 추세입니다. 이러한 추세와 함께 미국의 석유 및 가스 시장의 수익 동향에 대해 업스트림 부문이 특히 큰 영향력을 행사하는 구조가 강화되고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.02.27The United States Oil And Gas Market size in 2026 is estimated at USD 149.32 billion, growing from 2025 value of USD 142.81 billion with 2031 projections showing USD 186.63 billion, growing at 4.56% CAGR over 2026-2031.

Robust drilling productivity in tight-oil plays, the rapid build-out of Gulf Coast LNG trains, and steady technology diffusion into mature basins underpin this expansion. Structural change is evident as export-oriented growth outpaces domestic demand, with 15 billion cubic feet per day of new LNG liquefaction slated by 2028. Upstream reinvestment remains disciplined, yet efficiency gains allow production to rise even as rig counts fall. Meanwhile, mega-mergers concentrate Permian Basin acreage, unlocking shared infrastructure savings that strengthen breakeven resilience.

United States Oil And Gas Market Trends and Insights

Tight-oil Productivity Gains in the Permian

Advanced completion designs and AI-guided drilling lifted Permian Basin output to 6.3 million barrels per day in 2024, representing 60% of total US growth despite a leaner rig fleet. Longer laterals, higher proppant loading, and real-time frac optimization push recovery per well higher while trimming costs. ExxonMobil's integration of Pioneer aims for a further 15% uplift through standardized execution and shared infrastructure. Independent drillers mirror these tactics to remain competitive. Efficiency, therefore, anchors continued output gains that fortify the US oil and gas market against price swings

Surging LNG Export Capacity

New Gulf Coast liquefaction trains reshape demand by linking domestic supply to global price premia. Venture Global's Plaquemines terminal added 20 million tpa capacity in 2024, with Golden Pass to follow at 15.6 million tpa. The export surge boosts Appalachian and Haynesville drilling, while USD 15 billion of new pipelines funnel volumes south. Closer alignment with world markets tempers seasonal Henry Hub volatility, strengthening forward visibility for producers and midstream players, and reinforcing expansion in the US oil and gas market.

Methane-fee Compliance Costs Under EPA OOOOb/c

Beginning in 2024, methane emissions exceeding set thresholds incur fees starting at USD 900 per metric ton and rising to USD 1,500 by 2026. Added monitoring and repair programs raise operating costs by USD 2-4 per barrel for typical shale wells, hitting smaller producers hardest. Compliance demands speed consolidation and quick adoption of technology, such as continuous leak detection, to alter cost structures within the US oil and gas market.

Other drivers and restraints analyzed in the detailed report include:

- AI-driven Seismic Analytics for Marginal Well Recovery

- IRA 45Q & 45V Tax Credits Lowering CCS Costs

- Water-stress Limits on Permian Fracturing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Upstream claimed 71.85% of the US oil and gas market size in 2025 and is on track for a 4.84% CAGR to 2031. Midstream captured 18.40%, buoyed by pipeline additions and LNG terminal build-outs, while downstream refining held 9.75% amid capacity limits and tighter emissions rules. Operators now target internal rates above 15% at USD 60 oil, steering capital toward high-return shale laterals and select long-cycle projects. ConocoPhillips' Willow development illustrates the shift, with 30-year reserves offering cash-flow depth rare in short-cycle shale projects. Drilling efficiency and disciplined reinvestment keep the upstream segment at the center of continued gains in the US oil and gas market.

Upstream's dominance rests on rapid productivity gains that hold costs near sub-USD 40 per barrel breakevens. Midstream remains an opportunity-rich sector as LNG growth drives storage and takeaway needs, yet capital discipline tempers speculative projects. Downstream margins are tightening amid competition from renewable diesel and the cost of regulatory upgrades. Together, these dynamics reinforce the upstream sector's outsized influence on revenue trends within the US oil and gas market.

The United States Oil and Gas Market Report is Segmented by Sector (Upstream, Midstream, and Downstream), Location (Onshore and Offshore), and Service (Construction, Maintenance and Turn-Around, and Decommissioning). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Exxon Mobil Corp.

- Chevron Corp.

- ConocoPhillips Co.

- EOG Resources Inc.

- Occidental Petroleum Corp.

- Pioneer Natural Resources Co.

- Phillips 66 Co.

- Valero Energy Corp.

- Marathon Petroleum Corp.

- Hess Corp.

- Devon Energy Corp.

- BP PLC

- Shell PLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tight-oil productivity gains in the Permian

- 4.2.2 Surging LNG export capacity -(new Gulf Coast trains)

- 4.2.3 AI-driven seismic analytics for marginal well recovery

- 4.2.4 IRA 45Q & 45V tax credits lowering CCS costs

- 4.2.5 Corporate green-bond funding for midstream build-out

- 4.2.6 Niche petro-feedstock demand from advanced plastics

- 4.3 Market Restraints

- 4.3.1 Methane-fee compliance costs under EPA OOOOb/c

- 4.3.2 Growing state-level setback rules (e.g., CO, NM)

- 4.3.3 Water-stress limits on Permian fracturing

- 4.3.4 Persistent WTI-Brent discount hurting exports

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Crude-Oil Production & Consumption Outlook

- 4.8 Natural-Gas Production & Consumption Outlook

- 4.9 Installed Pipeline Capacity Analysis

- 4.10 Unconventional Resources CAPEX Outlook (tight oil, oil sands, deep-water)

- 4.11 Porter's Five Forces

- 4.11.1 Bargaining Power - Suppliers

- 4.11.2 Bargaining Power - Buyers

- 4.11.3 Threat of New Entrants

- 4.11.4 Threat of Substitutes

- 4.11.5 Competitive Rivalry

- 4.12 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Sector

- 5.1.1 Upstream

- 5.1.2 Midstream

- 5.1.3 Downstream

- 5.2 By Location

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 By Service

- 5.3.1 Construction

- 5.3.2 Maintenance and Turn-around

- 5.3.3 Decommissioning

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Exxon Mobil Corp.

- 6.4.2 Chevron Corp.

- 6.4.3 ConocoPhillips Co.

- 6.4.4 EOG Resources Inc.

- 6.4.5 Occidental Petroleum Corp.

- 6.4.6 Pioneer Natural Resources Co.

- 6.4.7 Phillips 66 Co.

- 6.4.8 Valero Energy Corp.

- 6.4.9 Marathon Petroleum Corp.

- 6.4.10 Hess Corp.

- 6.4.11 Devon Energy Corp.

- 6.4.12 BP PLC

- 6.4.13 Shell PLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment