|

시장보고서

상품코드

1934610

자동차 금융 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automotive Financing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

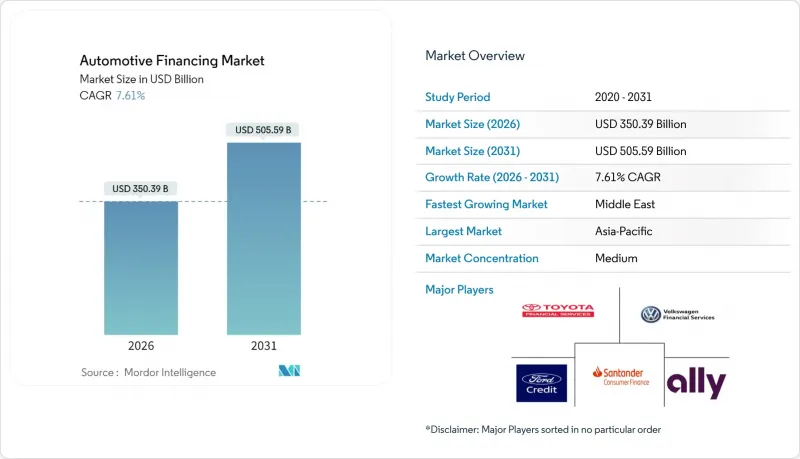

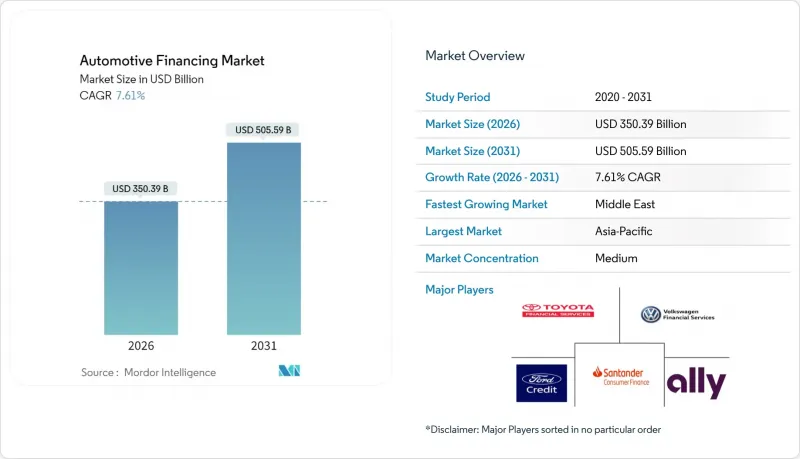

자동차 금융 시장은 2025년 3,256억 2,000만 달러에서 2026년에는 3,503억 9,000만 달러로 성장하고, 2026-2031년 CAGR 7.61%로 성장을 지속하여, 2031년까지 5,055억 9,000만 달러에 이를 것으로 예측되고 있습니다.

중고차 대출은 이미 자동차 금융 시장의 53.40%를 차지하고 있으며, 9.2%의 빠른 속도로 성장하고 있으며, 2030년까지 주요 성장 동력이 될 것으로 예측됩니다. 디지털 대출 플랫폼의 확산, 유연한 결제 구조에 대한 소비자 수요 증가, 차량 전동화 추세와 함께 기준금리가 높은 상황에서도 성장세를 유지하고 있습니다.(1) 대출기관은 분석 능력의 심화, 리스크 기반 가격 책정 확대, 온라인 자동차 소매 마켓플레이스와의 제휴를 통해 대출의 흐름을 유지하고 있습니다. 구독 패키지, 배터리 리스 등 부가가치형 모빌리티 서비스와 금융을 결합하는 능력도 은행, OEM 금융사, 핀테크 신규 진출기업에게 결정적인 경쟁 우위가 되고 있습니다.

세계 자동차 금융 시장 동향과 인사이트

급성장하는 온라인 자동차 판매 플랫폼이 즉각적인 디지털 대출을 주도하고 있습니다.

2024년 북미 딜러와 대부업체의 디지털 계약 건수는 전년 대비 급증했습니다. 소비자들은 현재 온라인 구매 과정에서 10분 이내에 실시간 대출 승인을 기대하며, 2023년에 일반적으로 1-2일 정도 걸리던 처리 기간에서 크게 단축되고 있습니다. 통합 금리 비교 위젯의 도입으로 가격 투명성이 높아져 자동 가격 책정 도구가 없는 대부업체의 수익률이 압박을 받고 있습니다. 이러한 추세는 유럽에도 확산되고 있으며, 다중 대출기관 API의 도입으로 고급차 부문의 평균 대출 실행 시간이 48% 단축되었습니다. 제조업체 금융 부문에서는 OEM의 EC 포털사이트에 자체 개발한 금융 계산 툴을 탑재하여 보험 및 유지보수 계약의 교차판매를 촉진하여 부수율과 고객 평생가치 향상으로 이어지고 있습니다.

중고차 거래 증가로 새로운 대출 수요 창출

인증 중고차 프로그램은 중고차에 대한 소비자의 인식을 바꾸고 있으며, 대출 기관은 신차에 가까운 LTV(Loan to Value) 비율과 금리를 제공할 수 있게 되었습니다. 예를 들어, 키아의 6년 풀커버 인증 중고차 보증은 2024년 키아의 미국 포트폴리오에서 중고차 판매 비율을 5% 끌어올렸습니다. 유럽에서는 공급망 혼란 이후 재고 정상화로 중고차 공급이 회복되면서 중고차 평균 융자금액이 전년 대비 14% 증가했습니다. 중고차 마켓플레이스에 즉각적인 융자 제안이 통합되면서 소비자는 딜러 방문 전에 금리를 확정할 수 있어 판매 경로가 단축되고, 융자 포기율이 감소하며, 융자 계약률이 향상되고 있습니다.

중앙은행의 금리 인상으로 순이자마진 압박을 받고 있습니다.

2025년 5월 현재 미국의 정책금리는 4.25-4.5%의 범위에서 움직이고 있습니다. 자금 조달 비용 상승으로 대출 금리 스프레드가 압박을 받아 2024년 은행의 신차 대출 잔액은 3.4% 감소했습니다. 기존 금리 경쟁력이 있는 신협은 72개월 장기 고정금리 상품 제공을 축소하여 대출자를 단기 상환 기간으로 유도하고 있습니다. 제조업체의 인센티브에 힘입은 전속 금융회사는 쇼룸의 집객을 유지하기 위해 금리 압력을 일부 흡수하여 점유율을 확대했습니다. 유럽에서는 유럽중앙은행(ECB)의 금리인상 지연으로 인해 순이자수익이 하락하고 있으며, 대출기관은 위험비용을 저신용자에게 전가하는 단계적 금리구조를 도입할 수밖에 없는 상황입니다.

부문 분석

자동차 금융 시장에서 중고차 부문은 2025년 전체 시장의 53.10%를 차지하며 9.02%의 연평균 복합 성장률(CAGR)로 전체 시장 성장률을 상회할 것으로 예상되며, 그 우위는 더욱 확대될 것으로 보입니다. 인증 중고차 프로그램은 보증 범위를 주류화하여 대출자가 거의 신차와 동등한 수준의 차량을 우량한 위험 담보로 취급할 수 있도록 하고 있습니다. 디지털 마켓플레이스는 그 규모가 더욱 확대되고 있습니다. 주요 포털사이트에 통합된 대출 위젯을 통해 신청부터 승인까지 전환율이 30% 이상 향상되었습니다. 그 결과, 중고차 부문의 자동차 금융 시장 규모는 2031년까지 2,917억 달러 이상에 달할 것으로 예측됩니다.

구매 부담 증가로 인해 일부 우량 차주들이 신차 구매를 자제하는 경향이 있습니다. 신차 평균월지불액은 2025년 초에 742달러에 달했습니다. 가격 상승에 대한 대응책으로 딜러들은 장기 대출이나 리스 플랜을 제안하고 있습니다. 그러나 마이너스 에쿼티(자산가치가 대출잔액보다 낮은 상태)에서의 대물변제율이 상승하고 있어 잔존가치 산정을 복잡하게 만들고 있습니다. 신차 채널은 46.90%의 점유율을 유지하지만, 성장 둔화에 따라 대부업체는 리스크 조정 가격 설정의 정교화 및 내연기관차(ICE) 중고차 시장 환경의 연화 속에서 재판매 가치를 보호하는 보험 상품과의 번들 판매를 고려해야 합니다.

2025년 기준 은행이 자동차 금융 시장 규모의 46.05%를 차지하고 있지만, 제조업체 금융 자회사의 추격으로 인해 은행의 우위는 감소하는 추세입니다. 제조업체 금융은 구매 프로세스 통합과 보조금 지원 APR 프로모션을 활용하여 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 8.02% 성장할 것으로 예측됩니다. 폭스바겐파이낸셜서비스는 2024년에만 1,030만 건의 신규 계약을 체결하여 시장 침투율이 34.1%로 상승했습니다. 신용협동조합의 자동차 금융 시장 점유율은 20.10% 내외로 유지되고 있으며, 회원들의 충성도와 중고차 대출에 대한 경쟁력 있는 가격 설정이 기여하고 있습니다.

비은행권 금융회사는 나머지 15.05%를 차지하며, 얼터너티브 데이터를 활용해 신용 이력이 적은 계층에 진출하고 있습니다. 저비용 디지털 모델을 통해 지점 중심 은행에 비해 대출 실행 비용을 최대 40%까지 절감할 수 있습니다. 또한, 임베디드 금융 API를 통해 EC 사업자는 자사 브랜드의 자동차 대출 서비스를 빠르게 전개할 수 있어 취급액 증가를 촉진하고 있습니다. 전통적인 은행의 경우, 수익 대비 비용 비율이 계속 엄격하게 관리될 것으로 예상되며, 광범위한 자동차 금융 산업에서 존재감을 유지하기 위해서는 심사 자동화, 서류 워크플로우의 효율화, 핀테크 전문 기업과의 제휴 등의 전략적 과제가 시급한 과제입니다.

지역별 분석

아시아태평양은 2025년에도 자동차 금융 시장의 41.00%를 차지하며 가장 영향력 있는 지역으로 남을 것입니다. 중국의 전기차 붐(2024년 신차 판매의 거의 절반을 차지할 것으로 예상)과 인도의 FAME 제도에 기반한 500억 달러 규모의 전기차 금융 로드맵이 결합되어 신용 수요의 지속적인 성장이 보장되고 있습니다. 디지털 우선의 여신심사, 실시간 신용정보 데이터, AI 기반 부정행위 방지 대책으로 기존에는 공식적인 신용기록이 없었던 대출자에게도 대출이 가능해졌습니다. 정부의 폐차 장려책 확대에 따라 융자 물량의 탄력성이 높아지고 있으며, 중국에서는 10% 보조금 제도 도입 후 6개월 만에 융자 구매가 14% 증가하였습니다.

2024년 4분기까지 자동차 대출 잔액은 1조 6,600억 달러에 이르렀고 연체율은 2.96%에 달했습니다. 대출기관은 여신기준 강화, 계약금 요구액 증가, 예측분석에 대한 투자를 통해 대손손실 방지에 힘쓰고 있습니다. 한편, 미국 자동차 금융 시장은 자금 조달 주기를 단축하고 온라인 마켓플레이스에 판매시점 금융 제공을 확대하는 혁신적인 핀테크 연계의 혜택을 누리고 있습니다. 전속 금융기관은 예측 서비스 알림을 발송하는 원격 유지보수 계약을 번들로 묶어 담보 가치 보호와 재판매 가치 향상을 도모하고 있습니다.

중동은 가장 빠르게 성장하는 지역으로 2031년까지 연평균 복합 성장률(CAGR) 10.29%로 확대될 것으로 예측됩니다. 사우디의 은행 신용대출 규모는 2025년 3월 8,272억 달러에 달했으며, 샤리아에 따른 자동차 대출 포트폴리오가 두 자릿수 성장을 지속하고 있습니다. 정부의 경제 다각화 정책이 모빌리티를 우선순위에 두면서 개인 대출과 운용리스 상품에 대한 수요가 증가하고 있습니다. 디지털화가 가속화되고 있으며, 걸프 지역에서는 신규 자동차 대출 신청의 35%가 모바일 퍼스트 플랫폼을 통해 이루어지고 있습니다. 이 지역의 자동차 금융 산업은 젊은 인구의 혜택을 받고 있으며, GCC 회원국 시민의 55% 이상이 35세 미만입니다. 이 계층이 선호하는 유연한 구독 모델이 상품 설계를 변화시키고 있습니다.

유럽의 규제 환경은 변화하고 있습니다. 영국 대법원의 미공개 수수료 관행에 대한 심사는 딜러와 대출자의 경제적 관계를 변화시키고 금리 스프레드 축소로 이어질 수 있습니다. 고가 배터리 팩의 소유권을 차량에서 분리하는 배터리 리스 프로그램이 등장하여 금융 사업자가 잔존가치 리스크를 줄일 수 있도록 돕고 있습니다. 스칸디나비아 국가들이 금융계약과 연동된 주행거리 과금형 보험을 도입한 사례는 텔레매틱스 데이터가 위험 조정 가격 설정의 기반이 될 수 있음을 보여줍니다.

남미와 아프리카에서는 정책금리 상승과 환율 변동으로 구매 의욕을 억제하는 한편, AI를 활용한 대체 신용점수가 새로운 대출자 층을 개척하고 있습니다. 지점망이 미비한 사하라 이남 아프리카에서는 모바일 머니의 통합이 대출 상환을 가속화하고 있습니다. 세계 금융기관이 이들 지역에 진출할 때 현지 소액금융기관이나 통신사의 월렛 서비스와의 제휴가 필수적이며, 여러 자금 제공업체에게 리스크를 분산하는 혼합금융 구조가 구축되어 있습니다. 자동차 금융 시장에서는 라이드셰어 운전자를 위한 자산 경량형 구독형 차량이 널리 보급되고, 향후 개인 차량 구매를 위한 공식적인 신용 이력 구축이 촉진될 것으로 예측됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.05The Automotive Finance market is expected to grow from USD 325.62 billion in 2025 to USD 350.39 billion in 2026 and is forecast to reach USD 505.59 billion by 2031 at 7.61% CAGR over 2026-2031.

Used-car financing, which already commands 53.40% of the automotive financing market, is growing at a rapid 9.2% pace and is set to remain the key growth engine through 2030. Digital origination platforms, heightened consumer appetite for flexible payment structures, and the continued electrification of vehicle fleets are together sustaining momentum even while benchmark rates remain elevated.[1]Lenders are responding by deepening analytics capabilities, widening risk-based pricing, and partnering with online auto-retail marketplaces to keep credit flowing. The ability to combine financing with value-added mobility services, such as subscription packages and battery leasing, is also becoming a decisive competitive lever for banks, OEM captives, and fintech entrants alike.

Global Automotive Financing Market Trends and Insights

Surging Online Auto-Retail Platforms Driving Instant Digital Financing

Digitized contracting volumes among dealers and lenders in North America surged year-on-year in 2024. Consumers now expect real-time credit approvals delivered inside a 10-minute online purchase journey, a dramatic acceleration from the 1-2-day turnaround common in 2023. Integrated rate-shopping widgets have heightened price transparency, squeezing margins for lenders that lack automated pricing tools. The trend is spreading to Europe, where multi-lender APIs have cut average time-to-funding by 48% in premium segments. For captive finance arms, embedding proprietary finance calculators inside OEM e-commerce portals is improving cross-selling of insurance and maintenance contracts, thereby lifting attachment rates and customer lifetime value.

Rising Used-Car Transactions Creating New Lending Volume

Certified pre-owned programs are reshaping consumer perceptions of second-hand vehicles, enabling lenders to offer loan-to-value ratios and rates closer to those on new cars. Kia's six-year bumper-to-bumper CPO warranty, for example, bolstered used-car penetration in the marque's U.S. portfolio by five percentage points in 2024. In Europe, inventory normalization after supply-chain shocks has restored late-model availability, pushing the average financed ticket size for used vehicles up 14% year-on-year. As used-car marketplaces integrate instant finance offers, origination conversion improves because consumers can lock rates before visiting a dealership, thereby shortening the sales funnel and reducing loan abandonment rates.

Central-Bank Rate Hikes Compressing Net-Interest Margins

Policy rates in the United States remain in a 4.25-4.5% corridor as of May 2025. The higher funding cost has squeezed lender spreads; new-auto loan balances at banks fell 3.4% in 2024. Credit unions, traditionally rate-competitive, cut long-term fixed offers for 72-month terms, nudging borrowers toward shorter tenors. Captive finance entities, cushioned by manufacturer incentives, absorbed part of the rate pressure to sustain showroom traffic, explaining their share gains. In Europe, the lagged pass-through of European Central Bank hikes is similarly dampening net-interest income, forcing originators to introduce tiered-rate structures that pass risk costs to lower-quality borrowers.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of EV Leasing & Subscription Models Catalyzing Finance Penetration

- Government Scrappage Incentives & Green-Finance Subsidies

- Rising Delinquency Rates Constraining Credit Appetite

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The used-vehicle slice of the automotive financing market generated 53.10% of the automotive financing market in 2025 and will continue to widen its lead because its 9.02% CAGR exceeds overall market growth. Certified pre-owned programs have mainstreamed warranty coverage, letting lenders treat near-new units more like prime-risk collateral. Digital marketplaces further amplify scale: integrated loan widgets on leading portals lift application-to-approval conversion by more than 30%. As a result, the automotive financing market size for the used-segment is projected to top USD 291.7 billion by 2031.

Affordability headwinds are steering some prime borrowers away from new vehicles; average new-car payments hit USD 742 early in 2025. To mitigate sticker shock, dealers are pitching longer-term loans and leasing packages. However, the proportion of negative-equity trade-ins is rising, complicating residual-value mathematics. Although the new-vehicle channel retains 46.90% share, its slower growth will compel lenders to refine risk-adjusted pricing and to consider bundled insurance products that protect resale values in a softening ICE resale environment.

Banks generated 46.05% of the automotive financing market size in 2025, yet captive finance arms are eroding that lead. Captives are forecast to post an 8.02% CAGR from 2026 to 2031 as they leverage purchase-journey integration and subsidized APR promotions. Volkswagen Financial Services alone wrote 10.3 million new contracts in 2024, boosting penetration to 34.1%. The automotive financing market share of credit unions hovers near 20.10%, helped by member loyalty and competitive pricing on used-vehicle loans.

Non-bank financial companies contribute the balance 15.05%, using alternative data to expand into thin-file demographics. Their low-overhead digital models cut origination expense by up to 40% versus branch-centric banks. Embedded-finance APIs also allow e-commerce players to launch branded auto-loan offerings rapidly, driving incremental volume. For traditional banks, cost-to-income ratios will remain under scrutiny, setting a strategic imperative to automate underwriting, streamline document workflows and partner with fintech specialists to stay relevant in the broader automotive finance industry.

The Automotive Financing Market Report is Segmented by Type (New Vehicle and Used Vehicle), Source Type (OEM Captive Finance, Banks, and More), Vehicle Type (Passenger Cars and Commercial Vehicles), Financing Product (Loan, Lease, and More), and Geography (North America, South America, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained a 41.00% share of the automotive financing market in 2025 and remains the most influential region. China's EV boom, with EVs capturing nearly half of new-car sales in 2024, coupled with India's USD 50 billion EV-finance roadmap under the FAME scheme, ensures prolonged credit-demand growth. Digital-first underwriting, real-time bureau data, and AI-based fraud controls enable lenders to serve borrowers who previously lacked formal credit files. As governments expand scrappage incentives, loan volume elasticity is rising; a 10% rebate in China triggered a 14% jump in financed replacement purchases in just six months.

Auto-loan balances climbed to USD 1.66 trillion by Q4 2024, even as delinquency transitions reached 2.96%. Lenders are tightening credit tiers, boosting down-payment requests, and investing in predictive analytics to pre-empt charge-offs. The automotive financing market size in the United States nonetheless benefits from innovative fintech collaborations that shorten funding cycles and extend point-of-sale loan offers into online marketplaces. Captive lenders are bundling tele-maintenance subscriptions that send predictive service reminders, protecting collateral, and improving resale values.

The Middle East is the fastest-growing territory, projected to advance at a 10.29% CAGR to 2031. Saudi banking credit reached USD 827.2 billion in March 2025, with Shariah-compliant auto-loan portfolios expanding in double digits. Government diversification agendas prioritize mobility, sparking demand for both personal loans and operating-lease products. Digitalization levels are accelerating; mobile-first platforms now account for 35% of new auto applications in the Gulf. The automotive finance industry in the region also benefits from a young demographic, more than 55% of GCC citizens are under 35, whose preference for flexible subscription models is reshaping product design.

Europe region's regulatory environment is evolving; the UK Supreme Court's review of undisclosed commission practices could alter dealer-lender economics, potentially lowering rate spreads. Battery-lease programs that detach ownership of high-value packs from the vehicle are emerging, helping finance providers de-risk residual-value exposure. Scandinavia's embrace of pay-per-kilometre insurance tied to finance contracts illustrates how telematics data can underpin risk-adjusted pricing.

South America and Africa elevated policy rates and currency volatility pose affordability challenges, yet AI-driven alternative credit scoring is unlocking new borrower pools. Mobile money integration accelerates loan payments in sub-Saharan Africa, where branch infrastructure remains thin. For global lenders, entering these regions often requires partnering with local microfinance institutions or telco wallets, creating blended-finance structures that dilute risk across multiple capital providers. The automotive financing market is expected to see wider adoption of asset-light subscription fleets for ride-hail drivers, fostering formal credit histories that can support future personal-vehicle purchases.

- Bank of America Corp.

- Ally Financial Inc.

- Hitachi Capital Corp.

- HDFC Bank Ltd.

- Bank of China

- Capital One Financial Corp.

- Wells Fargo & Co.

- Toyota Financial Services

- BNP Paribas SA

- Volkswagen Financial Services AG

- Mercedes-Benz Financial Services

- Standard Bank Group

- Mahindra Finance Ltd.

- Santander Consumer Finance

- General Motors Financial Company, Inc.

- Ford Motor Credit Co.

- Mitsubishi UFJ Lease & Finance Ltd.

- DBS Bank Ltd.

- Hyundai Capital Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Online Auto-Retail Platforms Driving Demand for Instant Digital Financing in North America

- 4.2.2 Rising Used-Car Transactions and Certified Pre-Owned Programs in Europe Creating New Lending Volume

- 4.2.3 Rapid Growth of EV Leasing and Subscription Models in Asia-Pacific Catalyzing Captive Finance Penetration

- 4.2.4 Government Scrappage Incentives and Green-Finance Subsidies Accelerating Auto Loan Originations in China and EU

- 4.2.5 OEM Captives Expanding Buy-Now-Pay-Later and Flexible Balloon Payment Products in Emerging Markets

- 4.2.6 Alternative Data and AI-Based Credit Scoring Opening Sub-prime Borrower Segments in South America

- 4.3 Market Restraints

- 4.3.1 Central-Bank Rate Hikes Compressing Net Interest Margins for Auto Lenders Since 2023

- 4.3.2 Rising Delinquency Rates in U.S. Sub-prime Auto Segment Constraining Banks' Credit Appetite

- 4.3.3 Regulatory Caps on Vehicle Loan-to-Value Ratios in India and Brazil Limiting Financing Volumes

- 4.3.4 Depreciation Risk of ICE Vehicles Undermining Residual Value Assumptions amid EV Shift

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 New Vehicle

- 5.1.2 Used Vehicle

- 5.2 By Source Type

- 5.2.1 OEM Captive Finance

- 5.2.2 Banks

- 5.2.3 Credit Unions

- 5.2.4 Non-Bank Financial Institutions

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.4 By Financing Product

- 5.4.1 Loan

- 5.4.2 Lease

- 5.4.3 Balloon Payment

- 5.4.4 Subscription

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Indonesia

- 5.5.4.6 Vietnam

- 5.5.4.7 Philippines

- 5.5.4.8 Australia

- 5.5.4.9 New Zealand

- 5.5.4.10 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Bank of America Corp.

- 6.4.2 Ally Financial Inc.

- 6.4.3 Hitachi Capital Corp.

- 6.4.4 HDFC Bank Ltd.

- 6.4.5 Bank of China

- 6.4.6 Capital One Financial Corp.

- 6.4.7 Wells Fargo & Co.

- 6.4.8 Toyota Financial Services

- 6.4.9 BNP Paribas SA

- 6.4.10 Volkswagen Financial Services AG

- 6.4.11 Mercedes-Benz Financial Services

- 6.4.12 Standard Bank Group

- 6.4.13 Mahindra Finance Ltd.

- 6.4.14 Santander Consumer Finance

- 6.4.15 General Motors Financial Company, Inc.

- 6.4.16 Ford Motor Credit Co.

- 6.4.17 Mitsubishi UFJ Lease & Finance Ltd.

- 6.4.18 DBS Bank Ltd.

- 6.4.19 Hyundai Capital Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment