|

시장보고서

상품코드

2044048

하이브리드 지상-위성 통신망 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Hybrid Terrestrial-Satellite Telecom Networks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

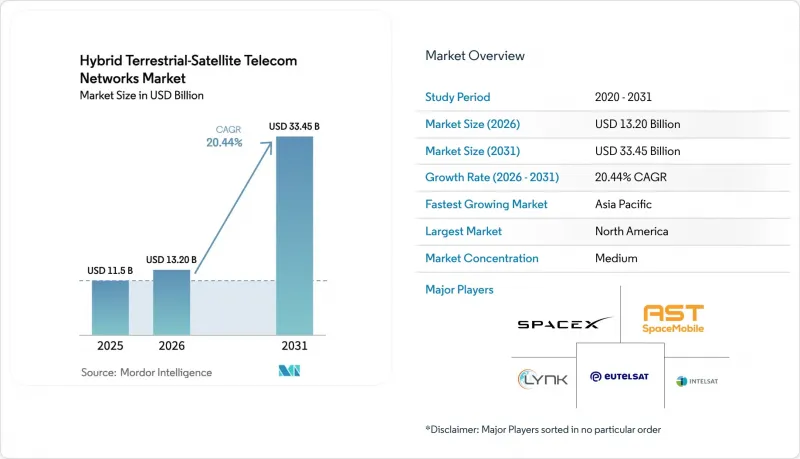

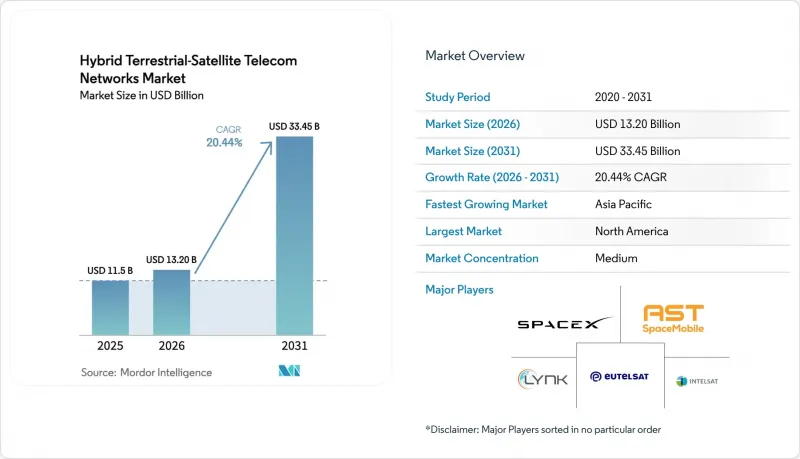

하이브리드 지상-위성 통신망 시장 규모는 2025년 115억 달러에서 2026년에는 132억 달러로 확대되어 2026년부터 2031년까지 CAGR 20.44%로 성장을 지속하여, 2031년에는 334억 5,000만 달러에 이를 것으로 예측됩니다.

3GPP Release 17의 비지상망(NTN) 표준의 발전, 2024년 이후 발사 비용의 50%에 달하는 극적인 감소, 정부 주도의 지역 광대역 구축 의무화 등으로 인해 위성 링크는 특히 광케이블 설치가 경제적으로 불가능한 지역에서의 백업 수단에서 5G 접속에 필수적인 요소로 전환되었습니다. 현재 모바일 네트워크 사업자들은 Kuiper, Starlink, AST SpaceMobile의 용량을 자사의 핵심 네트워크에 통합하여 규제상의 서비스 품질 목표를 충족하는 원활한 커버리지를 보장하고 있습니다. 그 결과, 총소유비용(TCO)을 낮추고 새로운 수익원을 창출하는 멀티 궤도 아키텍처, 엣지 게이트웨이, AI 기반 트래픽 오케스트레이션으로 자본 유입이 이동하고 있습니다. 사업자들의 열정은 수직통합형 하이퍼스케일러, 기존 GEO(정지궤도) 사업자, 그리고 신흥 LEO(저궤도) 전문 기업들 간의 치열한 경쟁으로 이어지고 있습니다. 북미는 여전히 스펙트럼 공유 및 디바이스 직결형(D2D) 시범사업의 시험장 역할을 하고 있으며, 아시아태평양에서는 차이나모바일, NTT도코모, 인도 국영 통신사업자들이 위성을 통한 5G 서비스 지역 확대 경쟁을 벌이고 있는 가운데, 설비투자 증가세가 가장 빠릅니다. 이 가장 빠른 성장세를 보이고 있습니다.

세계 하이브리드 지상-위성 통신망 시장 동향과 인사이트: 3GPP Rel-17 NTN 표준화를 위한 3GPP Rel-17 표준화

공중 인터페이스 규칙이 확정됨에 따라 스마트폰은 위성을 네이티브 무선 노드로 취급할 수 있게 되어 부피가 큰 안테나가 필요 없어지고 모뎀의 복잡성도 줄어들게 됩니다. 2025년 말까지 5,000만 대 이상의 Snapdragon X80 및 Dimension 9400 탑재 단말기가 출하될 것이며, 내장형 위성 통신 기능에 대한 소비자 수요를 입증할 것입니다. Release 18에서는 NB-IoT 및 LTE-M으로 기능이 확대되고, 센서의 전력 소비를 1와트 미만으로 낮춰 농업 및 해양 분야에서의 채택이 확대될 것으로 예측됩니다. 2026년 1월에 인증된 상호운용성 테스트를 통해 사업자 간 로밍이 작동한다는 것이 입증되었고, 통신사들은 공통 과금 프로파일을 기반으로 서비스를 개발할 수 있는 자신감을 얻게 되었습니다. 반도체 업체들이 NTN 로직을 상용 칩셋에 통합함에 따라 대량 생산에 따른 비용 절감 효과로 단말기 가격 프리미엄이 낮아지고, 중급형 모델로의 보급이 가속화될 것입니다.

정부 지원으로 진행되는 지방 광대역 사업

미국의 BEAD 프로그램은 4억 2,450만 달러의 예산을 책정하고 있으며, 1마일당 광섬유 비용이 10만 달러 이상인 지역에서는 하이브리드 설계를 의무화하고 있습니다. 이미 18개 주에서 위성-지상 입찰업체를 인증하고 있으며, LEO 링크는 일시적인 가교가 아닌 영구적인 인프라로 변모하고 있습니다. 유럽의 60억 유로 규모의 IRIS2 컨스텔레이션에는 트래픽을 EU 역내에 머물게 하고, 5G 코어와 상호 운용하도록 하는 주권 조항이 포함되어 있습니다. 인도에서는 신규 농어촌 5G 기지국의 위성 백홀 의무화로 인해 통신사업자들은 NTN 게이트웨이를 도입할 수밖에 없는 상황입니다. 한편, 중국에서는 150억 위안의 기금이 티베트와 신강에서 통합 시범사업을 지원하고 있습니다. 이러한 정책은 잠재적 수요가 확정된 계약으로 전환되어 위성 별자리 소유자와 지상 통신 사업자 모두의 수익 파이프라인을 강화하고 있습니다.

듀얼 모드 단말기 및 게이트웨이의 높은 설비 투자 비용

듀얼모드 스마트폰은 지상 전용 단말기보다 여전히 150-300달러가 비싸 평균 판매가격이 200달러 미만인 지역에서는 보급이 제한적일 수밖에 없습니다. 게이트웨이 노드는 대당 500만-1,500만 달러에 달하며, 왕복 지연을 100밀리초 미만으로 줄이기 위해서는 500-1,000km마다 설치해야 하기 때문에 통신사업자의 재정상황을 압박하고 있습니다. 블루버드만 해도 전 세계 로밍을 실현하기 위해 2억 달러 이상의 지상 인프라가 필요합니다. 자금 조달의 장애물로 인해 상용 서비스 시작이 1년 정도 늦어질 수 있으며, 이로 인해 선구자 우위가 축소되고 수익 계상이 지연될 수 있습니다.

부문 분석

2025년에는 위성, 발사 서비스, 듀얼 모드 단말기에 대한 막대한 투자에 이어 하드웨어가 전체 매출의 54.55%를 차지했습니다. 그러나 소프트웨어는 CAGR 24.50%로 다른 모든 계층을 능가할 것으로 예측됩니다. 이러한 변화로 인해 오케스트레이션 엔진, 슬라이스 컨트롤러, AI 트래픽 디렉터가 하이브리드 지상-위성 통신망 시장의 핵심 수익원으로 자리매김하고 있습니다. 퀄컴의 모뎀 펌웨어는 위성의 에페메리스(ephemeris)를 10초 미리 예측하여 핸드오프 지연을 40% 감소시켜 음성 통신의 연속성을 향상시킵니다. 이는 통신사가 프리미엄 서비스 계층을 통해 수익을 창출할 수 있는 장점입니다.

통신 사업자들이 위성 별자리와 코어를 통합하고 24시간 365일 네트워크 운영을 아웃소싱함에 따라 서비스 수익은 소프트웨어의 성장 궤도를 따라갈 것입니다. 노키아의 'Network as Code' 플랫폼을 통해 기업들은 API를 통해 주문형 위성 대역폭을 예약할 수 있으며, 연결성을 프로그래밍 가능한 리소스로 전환할 수 있습니다. 안테나와 전원 시스템은 여전히 필수적이지만, 많은 부가가치는 스펙트럼 재사용을 극대화하고 도플러 오프셋을 압축하며 실시간 규정 준수를 보장하는 코드에서 비롯됩니다. 칩셋 가격이 하락함에 따라 이익 기여도는 알고리즘과 라이프사이클 지원으로 결정적으로 이동하고 있으며, 이는 하이퍼스케일러가 커넥티비티를 클라우드 서비스와 묶는 전략적 논리를 뒷받침하고 있습니다.

2025년 매출의 38.97%를 차지했지만, 칩셋의 통합으로 진입장벽이 크게 낮아지면서 성장의 축은 이제 사용자 기기로 이동하고 있습니다. 하이브리드 지상-위성 통신망(NTN) 시장 규모 분포를 살펴보면, 사용자 기기는 2031년까지 연평균 복합 성장률(CAGR) 27.82%를 나타낼 것으로 예측되며, 이는 휴대폰 벤더들이 단일 SIM 작동을 실현하기 위해 NTN 기능을 통합하고 있음을 반영하고 있습니다. MediaTek의 Dimension 9400은 15달러 미만의 부품 비용으로 위성 메시징 기능을 추가하여 중산층 소비자 가격대에 맞게 비용 구조를 조정했습니다.

지상 인프라에는 여전히 자본이 투입되고 있으며, 특히 위성 용량을 중개하는 슬라이스 지원 독립형 5G 코어를 예로 들 수 있습니다. LEO, MEO, GEO 궤도 간 빔을 제어할 수 있는 엣지 게이트웨이가 광섬유 육상국 근처에 보급되어 유효 전송거리를 단축하고 도플러 왜곡을 감소시키고 있습니다. 아마존의 Kuiper 고객 가정 내 단말기는 299달러로 기존 GEO VSAT의 비용을 절반으로 줄이는 동시에 Wi-Fi 7을 통합하여 인구 밀도가 낮은 지역의 주택에 도입하는 것이 현실적입니다. 디바이스에 직접 연결되는 기능이 보편화됨에 따라 차별화된 성능은 위성의 총 개수가 아니라 디바이스와 기지국이 1초 미만의 간격으로 얼마나 스마트하게 궤도를 전환할 수 있느냐에 따라 결정될 것입니다.

'하이브리드 지상-위성 통신망 시장 보고서'는 구성요소(하드웨어, 소프트웨어, 서비스), 플랫폼(위성 별자리, 지상 인프라 등), 용도(긴급/재난 대응, 해상 통신 등), 최종 사용자(정부/국방기관, 해운 사업자, OEM 등), 지역별로 분류되어 있습니다. OEM 등), 지역별로 분류되어 있습니다. 시장 예측은 금액(USD)으로 표시됩니다.

지역별 분석

북미는 2025년 매출의 35.70%를 차지해, FCC의 주파수 공유 관련 마일스톤과 고비용 카운티의 하이브리드 구축을 지원하는 4억 2,450만 달러 규모의 BEAD 프로그램이 그 견인차 역할을 할 것으로 보입니다. AT&T는 Kuiper의 백홀을 광섬유로 연결하고, T-Mobile은 PCS 대역의 Direct-to-Cell을 베타 버전으로 운영하고 있으며, Verizon은 FirstNet의 비상용 드론에 위성 링크를 활용하고 있습니다. 캐나다의 Telus와 Bell은 북부 지역으로의 서비스 확대를 위해 AST SpaceMobile에 투자했고, 멕시코는 라이선싱 절차를 간소화하여 외국 위성 컨스텔레이션이 현지 파트너 없이 직접 판매할 수 있도록 함으로써 Starlink의 지방 지역 커버리지 확장을 가속화했습니다. 커버리지 확대를 가속화했습니다.

아시아태평양이 성장을 주도하고 있으며, 2031년까지 연평균 복합 성장률(CAGR)은 25.41%로 예측됩니다. 중국에서는 150억 위안의 기금이 투입되고, 국영 통신 사업자는 2027년까지 국내 위성 별자리와 SA-5G 코어 간의 상호 운용성을 검증해야 합니다. 인도의 지침은 새로 설치되는 모든 원격지 5G 기지국에 위성 백홀 지원을 의무화하고 있으며, 바르티 에어텔(Bharti Airtel)의 원웹(OneWeb)과의 제휴는 민간 통신 사업자의 추진력을 뒷받침하고 있습니다. 일본에서는 NTT도코모가 2026년 초 상용 서비스를 시작하면 소비자들은 전국 규모의 디바이스 직결형 통신을 이용할 수 있게 됩니다. 한편, 한국은 해외 공급업체에 대한 의존도를 낮추기 위해 국산 게이트웨이 기술에 2,000억 원을 투자하고 있습니다. 호주는 지역 간 연결성 강화를 위해 12억 호주달러를 투자하여 광산업과 원주민 커뮤니티를 위한 스타링크 백홀을 도입하고 있습니다.

유럽은 정책 조정을 통해 전진하고 있지만, 아직은 그 전개가 제각각입니다. 2025년에 발표된 RSPG 가이드라인은 장치에 직접 연결할 수 있는 청사진을 제시했지만, 전력 및 플럭스 제한과 장치 인증 기준은 여전히 국가마다 달라서 EU 전역에 대한 배포가 지연되고 있습니다. 60억 유로 규모의 IRIS2 프로젝트는 주권적 라우팅과 5G 코어의 통합을 보장하고 국내 제조업체와 발사 사업자를 지원하고 있습니다. 보다폰과 AST SpaceMobile은 2026년 말까지 독일, 스페인, 영국에서 서비스를 개시하여 후발주자보다 먼저 상업적 타당성을 입증할 예정입니다. 남미와 중동 및 아프리카는 도입 단계가 앞서 있지만, 브라질 규제 당국은 2025년 Kuiper와 Starlink에 라이선스를 부여했으며, 걸프협력회의(GCC) 회원국은 사막 지역을 커버하기 위해 Thuraya 및 Inmarsat와 협상을 진행하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The Hybrid Terrestrial-Satellite Telecom Networks Market size is expected to grow from USD 11.5 billion in 2025 to USD 13.20 billion in 2026 and is forecast to reach USD 33.45 billion by 2031 at 20.44% CAGR over 2026-2031. Advancing 3GPP Release 17 non-terrestrial network (NTN) standards, dramatic launch-cost reductions of approximately 50% since 2024, and government-funded rural broadband mandates have converted satellite links from backup to integral 5G access, especially where fiber remains uneconomic. Mobile network operators now embed Kuiper, Starlink, and AST SpaceMobile capacity into their cores, ensuring seamless coverage that meets regulatory service-quality targets. Capital inflows have therefore shifted toward multi-orbit architectures, edge gateways, and AI-based traffic orchestration that lower the total cost of ownership and unlock new revenue pools. Operator enthusiasm translates into vigorous competition among vertically integrated hyperscalers, traditional GEO incumbents, and emerging LEO specialists. North America remains the test bed for spectrum-sharing and direct-to-device pilots, while Asia-Pacific records the fastest capital spending as China Mobile, NTT DOCOMO, and India's state operators race to extend 5G footprints via satellites.

Global Hybrid Terrestrial-Satellite Telecom Networks Market Trends and Insights 3GPP Rel-17 NTN Standardization

Finalized air-interface rules let smartphones treat satellites as native radio nodes, eliminating bulky antennas and trimming modem complexity. More than 50 million Snapdragon X80 and Dimensity 9400 devices shipped by late 2025, proving consumer appetite for built-in satellite coverage. Release 18 pushes the capability to NB-IoT and LTE-M, lowering sensor power budgets below 1 watt and widening agricultural and maritime adoption. Interoperability tests certified in January 2026 show cross-operator roaming works, giving carriers confidence to expose services under common billing profiles. As silicon vendors integrate NTN logic into commercial chipsets, production economies drive down handset premiums, accelerating penetration in mid-tier models.

Government-Funded Rural Broadband Programs

The United States BEAD program earmarked USD 42.45 billion and requires hybrid designs where fiber costs exceed USD 100,000 per mile. 18 states already qualified satellite-terrestrial bidders, turning LEO links into permanent infrastructure rather than temporary bridges. Europe's EUR 6 billion IRIS2 constellation embeds sovereignty clauses that oblige traffic to remain on EU soil and interoperate with 5G cores. India's mandate for satellite backhaul at new rural 5G sites compels operators to deploy NTN gateways, while China's CNY 15 billion fund pilots integrations across Tibet and Xinjiang. Such policies convert latent demand into booked contracts, bolstering the revenue pipeline for constellation owners and terrestrial carriers alike.

High CAPEX for Dual-Mode Terminals and Gateways

Dual-mode smartphones still cost USD 150-300 more than terrestrial-only units, limiting uptake where average selling prices stay under USD 200. Gateway nodes, priced at USD 5-15 million each, must be installed every 500-1,000 kilometers to achieve sub-100-millisecond round-trip latency, stretching operator balance sheets. BlueBird alone will need more than USD 200 million in ground infrastructure to enable global roaming. Financing hurdles can delay commercial launches by a year, compressing first-mover advantages and slowing revenue recognition.

Other drivers and restraints analyzed in the detailed report include:

- Reusable Launch Vehicles Lowering Constellation CAPEX

- Demand for Resilient Disaster-Response Connectivity

- Complex Multi-Jurisdictional Licensing Regimes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware accounted for 54.55% of total revenue in 2025, following heavy spending on satellites, launch services, and dual-mode devices. Software, however, is forecast to outpace all other layers at a 24.50% CAGR. This swing positions orchestration engines, slice controllers, and AI traffic directors as the core profit levers of the Hybrid Terrestrial-Satellite Telecom Networks market. Qualcomm's modem firmware predicts satellite ephemeris ten seconds ahead, cutting handoff latency by 40% and improving voice continuity, an advantage operators monetize through premium service tiers.

Service revenues follow software's trajectory as operators outsource constellation-to-core integration and 24/7 network operations. Nokia's Network as Code platform allows enterprises to reserve on-demand satellite bandwidth through APIs, turning connectivity into a programmable resource. While antennas and power systems remain essential, much of the incremental value accrues to code that maximizes spectral reuse, compresses Doppler offsets, and ensures regulatory compliance in real time. As chipset prices fall, margin contribution tilts decisively toward algorithms and lifecycle support, reinforcing the strategic logic of hyperscalers bundling connectivity with cloud services.

Satellite constellations took 38.97% of 2025 billings, yet growth now pivots to user equipment as chipset integration slashes entry barriers. Hybrid Terrestrial-Satellite Telecom Networks market size allocations show user equipment tracking a 27.82% CAGR through 2031, reflecting handset vendors embedding NTN functions for single-SIM behavior. MediaTek's Dimensity 9400 adds satellite messaging at a bill-of-materials cost under USD 15, aligning cost structures with mid-tier consumer price points.

Terrestrial infrastructure still absorbs capital, particularly standalone 5G cores with slice-awareness that broker satellite capacity. Edge gateways capable of steering beams across LEO, MEO, and GEO orbits proliferate near fiber landing stations, shortening effective path length and mitigating Doppler distortion. Amazon's Kuiper customer-premises terminal, priced at USD 299, halves the cost of historic GEO VSAT while bundling Wi-Fi 7, making residential adoption practical in sparsely populated counties. As direct-to-device capability becomes mainstream, differentiated performance will arise from how smartly devices and base stations swap orbits in sub-second intervals rather than from raw satellite counts.

The Hybrid Terrestrial-Satellite Telecom Networks Market Report is Segmented by Component (Hardware, Software, and Services), Platform (Satellite Constellations, Terrestrial Infrastructure, and More), Application (Emergency and Disaster Response, Maritime Connectivity, and More), End-User (Government and Defense Agencies, Maritime Operators and OEMs, and More), and Geography. The Market Forecasts are Provided in Value (USD).

Geography Analysis

North America accounted for 35.70% of revenue in 2025, anchored by FCC spectrum-sharing milestones and the USD 42.45 billion BEAD program that subsidizes hybrid deployments in high-cost counties. The United States serves as an innovation hub as AT&T bonds Kuiper backhaul with fiber, T-Mobile runs PCS-band direct-to-cell in beta, and Verizon uses satellite links for FirstNet emergency drones. Canada's Telus and Bell invested in AST SpaceMobile to extend service across northern territories, while Mexico streamlined licensing to allow foreign constellations to sell direct without local partners, speeding Starlink's rural coverage.

Asia-Pacific leads growth, with a projected 25.41% CAGR through 2031. China's CNY 15 billion fund compels state carriers to validate interoperability between domestic constellations and SA-5G cores by 2027. India's directive requires every new remote 5G base station to support satellite backhaul, and Bharti Airtel's OneWeb alliance underscores private carrier momentum. Japan's early 2026 commercial launch by NTT DOCOMO positions consumers for nationwide direct-to-device coverage, while South Korea invests KRW 200 billion in indigenous gateway technology to reduce its reliance on foreign suppliers. Australia channels AUD 1.2 billion into regional connectivity, deploying Starlink backhaul for mining and indigenous communities.

Europe advances through policy harmonization yet remains staggered. RSPG guidelines published in 2025 set the blueprint for direct-to-device, but power-flux limits and device certification still differ per country, slowing pan-EU rollouts. The EUR 6 billion IRIS2 project guarantees sovereign routing and 5G core integration, sustaining domestic manufacturers and launch providers. Vodafone and AST SpaceMobile will activate service in Germany, Spain, and the United Kingdom by late 2026, proving commercial viability ahead of lagging markets. South America, plus the Middle East and Africa, are earlier in the curve, though Brazil's regulator licensed Kuiper and Starlink in 2025, and Gulf Cooperation Council states negotiate with Thuraya and Inmarsat to blanket desert corridors.

List of Companies Covered in this Report:

- Space Exploration Technologies Corp.

- AST SpaceMobile, Inc.

- Lynk Global, Inc.

- Eutelsat S.A.

- Intelsat S.A.

- Omnispace, LLC

- Thales Alenia Space S.A.S.

- Lockheed Martin Corporation

- Vodafone Group Plc

- AT&T Inc.

- Telefonica, S.A.

- China Mobile Limited

- NTT DOCOMO, INC.

- KVH Industries, Inc.

- Iridium Communications Inc.

- SES S.A.

- Amazon.com, Inc.

- Telesat Corporation

- Hughes Network Systems, LLC

- Qualcomm Technologies, Inc.

- MediaTek Inc.

- Cobham Satcom A/S

- Gilat Satellite Networks Ltd.

- Phasor Solutions Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 3GPP Rel-17 NTN Standardization

- 4.2.2 Government-Funded Rural Broadband Programs

- 4.2.3 Reusable Launch Vehicles Lowering Constellation CAPEX

- 4.2.4 Demand for Resilient Disaster-Response Connectivity

- 4.2.5 AI-Driven Traffic-Steering for LEO/Terrestrial Hand-Off

- 4.2.6 Spectrum-Trading Marketplaces for Idle Satellite Capacity

- 4.3 Market Restraints

- 4.3.1 High CAPEX for Dual-Mode Terminals and Gateways

- 4.3.2 Complex Multi-Jurisdictional Licensing Regimes

- 4.3.3 Doppler-Induced Latency Issues for 5G-URLLC

- 4.3.4 Power-Budget Limits on Battery IoT Nodes

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Platform

- 5.2.1 Satellite Constellations

- 5.2.2 Terrestrial Infrastructure (RAN and Core)

- 5.2.3 User Equipment (Handsets, CPE, IoT)

- 5.2.4 Edge Nodes and Gateways

- 5.3 By Application

- 5.3.1 Emergency and Disaster Response

- 5.3.2 Maritime Connectivity

- 5.3.3 Aviation IFC and ATC Backup

- 5.3.4 Rural and Remote Broadband

- 5.3.5 Internet-of-Things (Massive IoT, Critical IoT)

- 5.3.6 Defense and Security Networks

- 5.3.7 Other Applications

- 5.4 By End-User

- 5.4.1 Government and Defense Agencies

- 5.4.2 Maritime Operators and OEMs

- 5.4.3 Airlines and UAV Operators

- 5.4.4 Mobile Network Operators (MNOs)

- 5.4.5 Enterprises and SMBs

- 5.4.6 Consumers (Direct-to-Device)

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC Countries

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Space Exploration Technologies Corp.

- 6.4.2 AST SpaceMobile, Inc.

- 6.4.3 Lynk Global, Inc.

- 6.4.4 Eutelsat S.A.

- 6.4.5 Intelsat S.A.

- 6.4.6 Omnispace, LLC

- 6.4.7 Thales Alenia Space S.A.S.

- 6.4.8 Lockheed Martin Corporation

- 6.4.9 Vodafone Group Plc

- 6.4.10 AT&T Inc.

- 6.4.11 Telefonica, S.A.

- 6.4.12 China Mobile Limited

- 6.4.13 NTT DOCOMO, INC.

- 6.4.14 KVH Industries, Inc.

- 6.4.15 Iridium Communications Inc.

- 6.4.16 SES S.A.

- 6.4.17 Amazon.com, Inc.

- 6.4.18 Telesat Corporation

- 6.4.19 Hughes Network Systems, LLC

- 6.4.20 Qualcomm Technologies, Inc.

- 6.4.21 MediaTek Inc.

- 6.4.22 Cobham Satcom A/S

- 6.4.23 Gilat Satellite Networks Ltd.

- 6.4.24 Phasor Solutions Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Analyst Recommendations and Suggestions