|

시장보고서

상품코드

2061580

비살상 무기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Non-Lethal Weapons - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

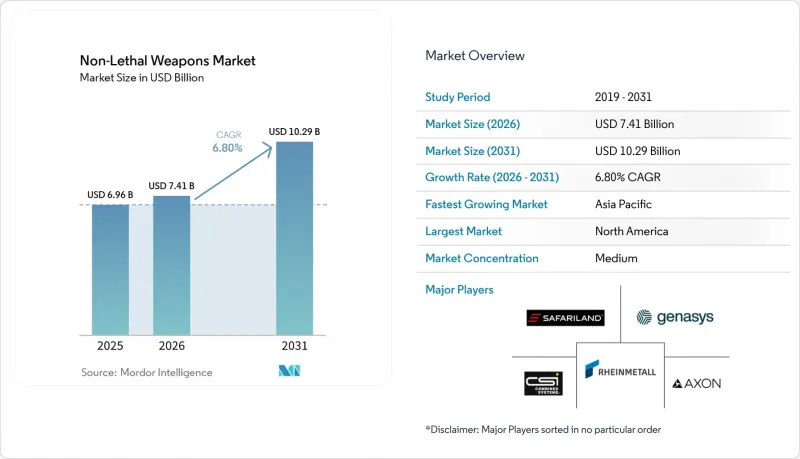

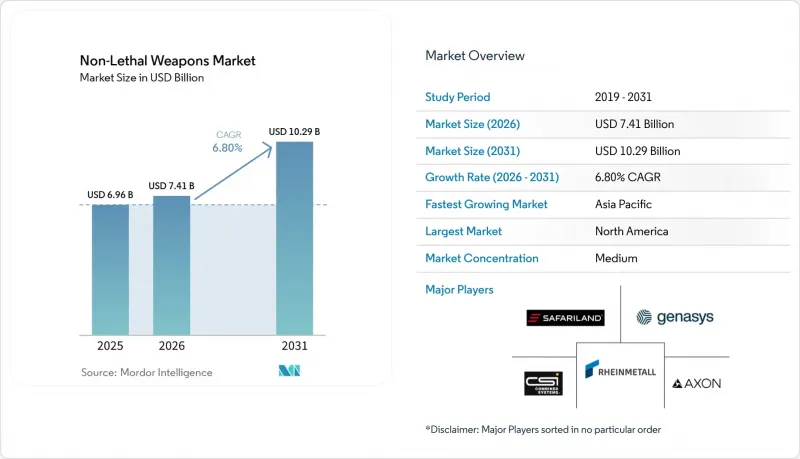

Mordor Intelligence에 의하면, 비살상 무기 시장 규모는 2025년 69억 6,000만 달러로 평가되었습니다. 2026년에는 74억 1,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 6.80%를 나타내, 2031년까지 102억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(지역 차단, 탄약 등), 최종 사용자(법 집행 기관 및 군), 사거리(단거리, 중거리, 장거리), 용도(군중 통제, 국경 경비, 개인 방어, 주변 경비), 지역(북미, 유럽, 아시아태평양, 남아프리카, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 비살상 무기 시장 동향과 분석

법 집행 기관의 현대화와 사태 수습을 위한 요청

미국 및 유럽연합(EU)의 경찰 개혁법에서는 연방 또는 EU의 자금 지원을 비례 원칙에 기반한 무력 행사 능력의 입증과 연계하도록 규정하고 있습니다. 이에 따라 각 기관은 전도성 에너지 무기, 충격탄 및 화학 자극제를 장비 목록에 추가하도록 권고받고 있습니다. 훈련 프로그램에서는 초기 대응으로 구두 설득을 우선시하고, 그 후 단계적인 비살상 조치를 취하도록 변경되었으며, 그 결과 예산이 총기 훈련에서 이러한 새로운 장비의 인증으로 재분배되고 있습니다. 대규모 경찰서에서는 방아쇠를 당길 때마다 이를 기록하고, 해당 영상을 감독관이 검토할 수 있도록 업로드하는 통합 플랫폼의 도입이 점점 더 확대되고 있습니다. 그러나 이 기능의 도입은 소규모 지방 경찰 기관에게는 여전히 재정적인 과제로 남아 있습니다. 현재 진행 중인 의무화 주기는 2028년까지 새로운 조달 기회를 이끌어갈 것으로 예상되며, 그 이후에는 갱신 프로그램이 우선시될 전망입니다. 이러한 정책 주도형 수요는 비살상 무기 시장의 주요 성장 요인으로 작용하고 있습니다.

시민들의 시위가 거세지고 군중 관리에 대한 수요가 증가하고 있습니다.

2024년부터 2025년에 걸쳐, 프랑스의 연금 반대 시위부터 칠레의 경제 시위에 이르기까지 전 세계적으로 시위가 급증하면서, 경찰 당국은 군중 통제 장비에 대한 재검토를 요구받게 되었습니다. 도시 지역의 고밀도화로 인해 전술적 기동성이 제한되는 가운데, 지휘관들은 직접적인 신체 접촉 없이 군중을 해산시키기 위해 장거리 음향 장치나 페퍼 스프레이를 탑재한 드론을 우선적으로 도입하고 있습니다. 지난 소동으로 인해 공급 부족이 발생함에 따라, 조달 기관은 고무탄, 최루탄, 방수차의 비축량을 늘렸습니다. 그러나 공중보건 옹호자들은 호흡기 및 청각에 미칠 수 있는 잠재적 위험에 대해 우려를 표명하고 있으며, 일부 시의회에서는 사용 시간을 제한하려는 움직임도 보이고 있습니다. 이러한 감시의 눈길이 쏠리고 있음에도 불구하고, 반복되는 시위 활동은 비살상 무기 시장 수요를 지속적으로 견인하고 있으며, 특히 신속한 납품이 요구되는 계약에 초점이 맞추어지고 있습니다.

특정 유형의 비살상 무기(NLW)에 대한 인권, 책임 및 규제상의 제약

국제앰네스티는 2024년 시위 도중 고무탄으로 인해 발생한 눈과 가슴 부상에 대해 보고했으며, 이에 따라 동적 충격 탄약의 전면 금지를 요구하는 목소리가 높아졌습니다. 유럽 고문방지위원회는 회원국 내에서 새로운 비살상 무기 모델을 도입할 때의 전제조건으로, 상해 임계치 시험의 실시를 제안하고 있습니다. 2025년, 미국의 지자체들은 테이저건이나 발사체의 오용으로 인해 수백만 달러 규모의 합의금을 지급해야 하는 상황에 직면했고, 이에 따라 보험사들은 보험료를 인상하거나 보상 대상에서 완전히 제외하기 시작했습니다. 그 결과, 공급업체는 인증 시험 기관 및 정보 공개 규제와 같은 복잡한 환경에 대응해야 하며, 이로 인해 비용 증가와 제품 출시 일정 지연이 발생하고 있습니다. 이러한 규제 감독의 강화로 인해, 비살상 무기 시장의 특정 부문에서 단기적인 성장 가능성이 제한받고 있습니다.

부문별 분석

2025년 기준으로, 비살상 무기 시장 점유율의 26.91%를 탄약이 차지했습니다. 그러나 지향성 에너지 플랫폼은 2031년까지 연평균 성장률(CAGR) 12.43%를 나타낼 것으로 예측되며, 전체 제품 카테고리 중 가장 높은 성장률을 보일 것으로 전망됩니다. 기존의 고무탄과 플라스틱탄은 널리 보급된 40mm 및 12게이지 발사 장치와 호환성이 있어, 일상적인 시위 진압 활동에서 여전히 주류를 이루고 있습니다. 그럼에도 불구하고, 법 집행 기관들은 빔 시스템을 전략적 업그레이드로 점점 더 중요하게 여기고 있습니다. 이러한 시스템은 발사체의 재보급 필요성을 없애고, 주변 사람들에게 우발적으로 피해를 입힐 위험을 줄여주기 때문입니다. 전기 충격 무기는 여전히 주요 사업 부문이며, Axon사의 TASER 제품군이 이를 주도하고 있습니다. 이 제품은 실시간 발사 기록과 클라우드 기반 동영상 저장 기능을 통합하여, 종합적인 증거 추적을 요구하는 감시위원회의 요구 사항을 충족합니다.

방위성이 기지 주변 경비 및 해상 차단 등의 용도로 차량 탑재형 능동 방어 장치를 승인함에 따라, 지향성 에너지 시스템의 도입이 가속화되고 있습니다. 스마트 탄약도 점차 보급되고 있으며, GPS 기능이 탑재된 최루탄이나 자가 진단 기능이 있는 섬광탄과 같은 혁신적인 기술을 통해 기존 설계의 정확성과 신뢰성 문제가 해결되고 있습니다. 또한, Byrna와 같은 신규 진출기업들은 총기 소지 허가가 필요 없는 이산화탄소 구동식 휴대용 발사 장치를 도입하고 있어, 이를 통해 일반인이나 소규모 기관의 이용 기회가 확대되고 있습니다. 그 결과, 제품 포트폴리오는 저비용의 키네틱(물리적) 솔루션과 프리미엄급 전자식 또는 빔식 옵션이라는 두 가지 명확한 범주로 구분되어 있으며, 각각은 광범위한 비살상 무기 시장에서 특정 사용자의 요구를 충족시키고 있습니다.

법 집행 기관은 2025년 예상 매출의 64.90%를 차지했습니다. 그러나 군사 부문은 도시 작전 교리에 따라 확장 가능한 부대에 대한 수요가 증가하고 있는 것을 배경으로, 2031년까지 연평균 성장률(CAGR) 7.12%를 달성할 것으로 예측됩니다. 보병 부대나 헌병대에 배치되는 비살상 무기 시장은 비례의 원칙에 따른 대응이 요구되는 평화유지 활동이나 이민·국경 문제가 급증할 때 확대됩니다. 미국 및 나토(NATO)군은 순찰 차량에 능동 방어 시스템과 음향 경보 장치를 탑재하고 있습니다. 동시에, 특수작전부대는 인질 구출 작전에서 저섬광형 기만 수류탄의 사용을 표준화하고 있습니다.

방위 분야의 조달 과제는 매우 중대하며, 내환경성 향상, 사이버 보안 강화, 그리고 다군종 간 상호 운용성이 요구되고 있습니다. 그러나 플랫폼이 시험을 통과하면, 조달 계약은 일반적으로 5년에서 7년의 예산 주기에 걸쳐 공급업체의 안정적인 수익을 보장합니다. 국토안보 부문에서는 국경 경비 활동에 군용 등급의 빈백탄이나 페퍼볼탄을 도입함으로써, 민수용과 군수용의 경계가 점점 더 모호해지고 있으며, 이중용도 개념이 지지받고 있습니다. 또한, 민간 경비 및 교정 시설 부문에서는 소형 전기 충격 장치나 자극성 가스 장치에 대한 틈새 수요가 존재하며, 이러한 제품들은 폐쇄적인 환경에서의 소송 위험을 줄이는 데 기여하고 있어 고객 기반의 다각화로 이어지고 있습니다.

지역별 분석

북미는 미국 연방·주·지방 자치단체의 각 기관에 의한 지속적인 조달에 힘입어, 2025년 예상 매출의 36.95%를 차지했습니다. 이 기관들은 전도성 에너지 무기를 클라우드 기반 증거 관리 시스템과 함께 도입하여, 국토안보부(DHS)를 통해 정기적으로 탄약을 발주하고 있습니다. 캐나다는 계속해서 미국의 무력 행사 지침을 준수하며, 전국적인 테이저 총 도입을 추진하고 있습니다. 한편, 멕시코 연방경찰은 카르텔 단속 작전을 위해 스펀지 수류탄과 OC 스프레이를 확보하고 있습니다. 이 지역은 경찰관 1인당 장비 예산이 세계 최고 수준입니다. 그러나 많은 대규모 경찰서가 초기 구매에서 정기적인 업데이트로 전환함에 따라 성장세가 둔화되고 있으며, 단기 연평균 성장률(CAGR)은 세계 평균보다 낮습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 7.17%를 나타낼 것으로 예측되며, 이는 모든 지역 중 가장 높은 성장률입니다. 이러한 성장은 중국, 인도, 일본, 한국의 근대화 노력에 힘입어 이루어지고 있으며, 특히 기동대 장비와 국경 장벽 기술에 중점을 두고 있습니다. 2025년, 중국 공안부는 물대포차와 전기 충격봉을 일괄 발주하여 홍콩과 신장에 배치했습니다. 인도 중앙예비경찰대는 시위가 빈번히 발생하는 지역에서 사용하기 위해 최루가스와 페퍼볼 비축량을 보충했습니다. 한편, 일본과 한국은 공항 주변과 해군 기지에 장거리 음향 장치를 설치했습니다. 국내 조달 규제와 가격에 대한 민감성이 여전히 유럽 및 미국 공급업체들 시장 진출을 제한하고 있습니다. 그러나 아시아태평양의 비살상 무기 잠재 시장은 도시 지역의 인구 밀도 증가와 국경을 초월한 긴장 고조로 인해 확대되고 있습니다.

유럽, 남미, 중동 및 아프리카가 나머지 시장 점유율을 차지하고 있습니다. 유럽에서는 유럽연합(EU)의 엄격한 ‘비례의 원칙’에 따라 충격 에너지를 기록하는 스마트 탄약에 대한 수요가 지속되고 있습니다. 그러나 새로운 REACH 화학물질 규제로 인해 CS 가스 및 OC 가스의 판매가 주춤하고 있습니다. 남미에서는 브라질이 판매량 1위를 차지하고 있으며, 2026년 FIFA 월드컵을 앞두고 경기장 경비를 강화하기 위해 군경에 고무탄과 섬광탄을 배치하고 있습니다. 중동에서는 걸프협력회의(GCC) 회원국들이 주변 경비 예산을 증액하고, 치명적인 수단에 의존하지 않고 석유 터미널을 보호하기 위해 mm파 능동 방어 트럭과 음향 위협 타워를 도입하고 있습니다. 아프리카는 여전히 신흥 시장이며, 유엔 평화유지군이 나이지리아와 사헬 지역에서 테이저건과 최루가스 드론을 도입하고 있는 만큼, 비살상 무기 시장에 장기적인 성장 기회가 열리고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the non-lethal weapons market size is expected to grow from USD 6.96 billion in 2025 to USD 7.41 billion in 2026 and is forecasted to reach USD 10.29 billion by 2031 at an 6.80% CAGR over 2026-2031.

This report is Segmented by Product Type (Area Denial, Ammunition, and More), End User (Law Enforcement and Military), Range (Short, Medium, and Long), Application (Crowd Control, Border Security, Personal Self-Defense, and Perimeter Security), and Geography (North America, Europe, Asia-Pacific, South Africa, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Non-Lethal Weapons Market Trends and Insights

Law-Enforcement Modernization and De-Escalation Mandates

Police reform statutes in the US and the European Union (EU) now link federal or bloc funding to demonstrated use of proportional-force capabilities. This has prompted agencies to expand their inventories to include conducted-energy weapons, impact rounds, and chemical irritants. Training programs now prioritize verbal engagement as the initial response, followed by staged less-lethal measures, leading to a reallocation of budgets from firearms training to certification on these new tools. Larger departments are increasingly adopting integrated platforms that record every trigger pull and upload footage for supervisory review, a feature that remains financially challenging for smaller rural agencies. The ongoing mandate cycle is anticipated to drive new procurement opportunities through 2028, after which replacement programs are expected to take precedence. This policy-driven demand serves as a key growth driver for the non-lethal weapons market.

Rising Civil Unrest and Crowd-Management Demand

Global demonstrations surged during 2024-2025, ranging from pension protests in France to economic marches in Chile, prompting police forces to reevaluate their crowd-control equipment. Urban density restricts tactical maneuverability, leading commanders to prioritize long-range acoustic devices and pepper-spray drones to disperse crowds without direct physical engagement. Procurement agencies increased stockpiles of rubber bullets, tear-gas canisters, and water cannons after earlier unrest led to supply shortages. However, public health advocates have raised concerns about potential respiratory and auditory harm, leading some city councils to impose restrictions on deployment hours. Despite this scrutiny, recurring protests continue to drive demand in the non-lethal weapons market, with a focus on rapid-delivery contracts.

Human-Rights, Liability, and Regulatory Constraints on Specific NLW Classes

Amnesty International reported eye and chest injuries caused by rubber bullets during demonstrations in 2024, leading to calls for comprehensive bans on kinetic impact munitions. The European Committee for the Prevention of Torture has proposed injury-threshold testing as a prerequisite for introducing any new less-lethal weapon models into service within member states. In 2025, US municipalities faced multi-million-dollar settlements stemming from the misuse of tasers and projectiles, prompting insurers to raise premiums or exclude coverage altogether. As a result, vendors must navigate a complex landscape of approval laboratories and disclosure regulations, which increase costs and delay product launch timelines. This heightened regulatory oversight has constrained the short-term growth potential for certain segments of the non-lethal weapons market.

Other drivers and restraints analyzed in the detailed report include:

- Dual-Use Adoption in Defense, Homeland Security, and Border Operations

- Technology Advances: Directed Energy, Acoustic-Hailing, Smart Munitions

- Effectiveness Variability and Training Gaps Across Agencies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ammunition accounted for 26.91% of the non-lethal weapons market share in 2025. However, directed-energy platforms are projected to grow at a CAGR of 12.43% through 2031, marking the fastest growth among all product categories. Legacy rubber and plastic rounds continue to dominate daily riot control operations due to their compatibility with widely deployed 40 mm and 12-gauge launchers. Nonetheless, law enforcement agencies increasingly view beam systems as a strategic upgrade, as these systems eliminate the need for projectile resupply and reduce the risk of accidental harm to bystanders. Electroshock weapons remain a key segment, supported by Axon's TASER product line, which integrates real-time firing logs with cloud-based video storage, meeting oversight boards' demands for comprehensive evidence trails.

The adoption of directed-energy systems is accelerating as defense ministries approve vehicle-mounted Active Denial units for applications such as base perimeter security and maritime interdiction. Smart munitions are also gaining traction, with innovations like GPS-enabled tear-gas canisters and self-diagnosing flash-bangs addressing the accuracy and reliability issues of earlier designs. Additionally, new market entrants, such as Byrna, are introducing CO2-powered handheld launchers that do not require firearms licenses, thereby expanding access for civilians and smaller agencies. As a result, product portfolios are diverging into two distinct categories: low-cost kinetic solutions and premium electronic or beam-based options, each catering to specific user needs within the broader non-lethal weapons market.

Law enforcement organizations accounted for 64.90% of the projected 2025 revenue. However, the military segment is expected to achieve a 7.12% CAGR through 2031, driven by the growing need for scalable forces under the urban operations doctrine. The non-lethal weapons market allocated to infantry and gendarmerie units expands during peacekeeping missions or migrant-border surges, which require proportional engagement. The US and NATO forces have integrated active-denial systems and acoustic-hailing devices into patrol vehicles. At the same time, special operations teams have standardized the use of low-flash diversionary grenades for hostage rescue operations.

Procurement challenges in the defense sector are significant, requiring ruggedization, cybersecurity enhancements, and multi-service interoperability. However, once platforms pass testing, procurement contracts typically span five- to seven-year budget cycles, ensuring stable vendor revenue. Homeland security branches increasingly blur the line between civil and military applications by adopting military-grade bean-bag and pepper-ball rounds for border patrol operations, supporting the dual-use concept. Additionally, private security and corrections sectors contribute niche demand for compact electroshock and irritant devices, which help mitigate litigation risks in confined environments, thereby diversifying the customer base.

Geography Analysis

North America accounted for 36.95% of the projected 2025 revenue, driven by consistent procurement from US federal, state, and municipal agencies. These agencies bundle conducted-energy weapons with cloud-evidence suites and place recurring ammunition orders through the Department of Homeland Security (DHS). Canada continues to follow US use-of-force protocols, advancing nationwide taser deployments, while Mexican federal police procure sponge grenades and OC sprays for cartel-interdiction operations. The region benefits from the highest per-officer equipment budgets globally. However, growth is slowing as many large departments transition from initial purchases to cyclical upgrades, keeping the near-term CAGR below the global average.

The Asia-Pacific region is expected to grow at a 7.17% CAGR through 2031, the fastest among all regions. This growth is fueled by modernization initiatives in China, India, Japan, and South Korea, focusing on riot police equipment and border barrier technologies. In 2025, China's Ministry of Public Security bulk-ordered water-cannon vehicles and electroshock batons, deploying them in Hong Kong and Xinjiang. India's Central Reserve Police Force updated tear-gas and pepper-ball inventories for use in protest-prone areas. Meanwhile, Japan and South Korea installed long-range acoustic devices at airport perimeters and naval bases. Domestic sourcing regulations and price sensitivity continue to limit Western vendors' market penetration. However, the addressable market for non-lethal weapons in the Asia-Pacific is expanding due to increasing urban population density and cross-border tensions.

Europe, South America, and the Middle East and Africa collectively account for the remaining market share. In Europe, the European Union's strict proportional-force doctrine sustains demand for smart munitions that log impact energy. However, new REACH chemical regulations are slowing sales of CS and OC agents. In South America, Brazil leads in volume, equipping military police with rubber rounds and flash-bangs to secure stadiums ahead of the 2026 FIFA World Cup. In the Middle East, Gulf Cooperation Council states are increasing perimeter security budgets and purchasing millimeter-wave active denial trucks and acoustic-hailing towers to protect oil terminals without resorting to lethal measures. Africa remains an emerging market, with UN peacekeeping missions introducing tasers and tear-gas drones in Nigeria and the Sahel, creating long-term growth opportunities for the non-lethal weapons market.

- Axon Enterprise, Inc.

- Safariland, LLC

- Combined Systems, Inc.

- United Tactical Systems, LLC

- Rheinmetall AG

- FN HERSTAL (FN Browning Group)

- Condor Non-Lethal Technologies (EDGE Group PJSC)

- Genasys Inc.

- Byrna Technologies Inc.

- Pacem Solution International, LLC

- Sage Control Ordnance, Inc.

- NonLethal Technologies, Inc.

- Lamperd Less Lethal, Inc.

- Lightfield Ammunition Corporation

- Mace Security International, Inc.

- Zarc International, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Law-enforcement modernization and de-escalation mandates

- 4.2.2 Rising civil unrest and crowd-management demand

- 4.2.3 Dual-use adoption in defense, homeland security, and border operations

- 4.2.4 Technology advances: directed energy, acoustic hailing, smart munitions

- 4.2.5 Litigation and insurance pressures favoring less-lethal force options

- 4.2.6 Evidence ecosystem integration (bodycams, auto-reporting) accelerates CEW procurement

- 4.3 Market Restraints

- 4.3.1 Human-rights, liability, and regulatory constraints on specific NLW classes

- 4.3.2 Effectiveness variability and training gaps across agencies

- 4.3.3 Environmental and chemical restrictions on irritants and carriers

- 4.3.4 Public pushback on acoustic/energy devices over health impacts

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Area Denial

- 5.1.1.1 Anti-vehicle

- 5.1.1.2 Anti-personnel

- 5.1.2 Ammunition

- 5.1.2.1 Rubber Bullets

- 5.1.2.2 Wax Bullets

- 5.1.2.3 Plastic Bullets

- 5.1.2.4 Bean Bag Rounds

- 5.1.2.5 Sponge Grenade

- 5.1.3 Explosives

- 5.1.3.1 Flash Bang Grenades

- 5.1.3.2 Sting Grenades

- 5.1.4 Gases and Sprays

- 5.1.4.1 Water Cannons

- 5.1.4.2 Scent-based Weapons

- 5.1.4.3 Tear Gas

- 5.1.4.4 Pepper Spray

- 5.1.5 Directed Energy Weapons

- 5.1.6 Electroshock Weapons

- 5.1.1 Area Denial

- 5.2 By End User

- 5.2.1 Law Enforcement

- 5.2.2 Military

- 5.3 By Range

- 5.3.1 Short (Less than 30 m)

- 5.3.2 Medium (30 to 100 m)

- 5.3.3 Long (Greater than 100 m)

- 5.4 By Application

- 5.4.1 Crowd Control

- 5.4.2 Border Security

- 5.4.3 Personal Self-Defense

- 5.4.4 Perimeter Security

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Axon Enterprise, Inc.

- 6.4.2 Safariland, LLC

- 6.4.3 Combined Systems, Inc.

- 6.4.4 United Tactical Systems, LLC

- 6.4.5 Rheinmetall AG

- 6.4.6 FN HERSTAL (FN Browning Group)

- 6.4.7 Condor Non-Lethal Technologies (EDGE Group PJSC)

- 6.4.8 Genasys Inc.

- 6.4.9 Byrna Technologies Inc.

- 6.4.10 Pacem Solution International, LLC

- 6.4.11 Sage Control Ordnance, Inc.

- 6.4.12 NonLethal Technologies, Inc.

- 6.4.13 Lamperd Less Lethal, Inc.

- 6.4.14 Lightfield Ammunition Corporation

- 6.4.15 Mace Security International, Inc.

- 6.4.16 Zarc International, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment