|

시장보고서

상품코드

2061646

CLT(Cross Laminated Timber) 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cross Laminated Timber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

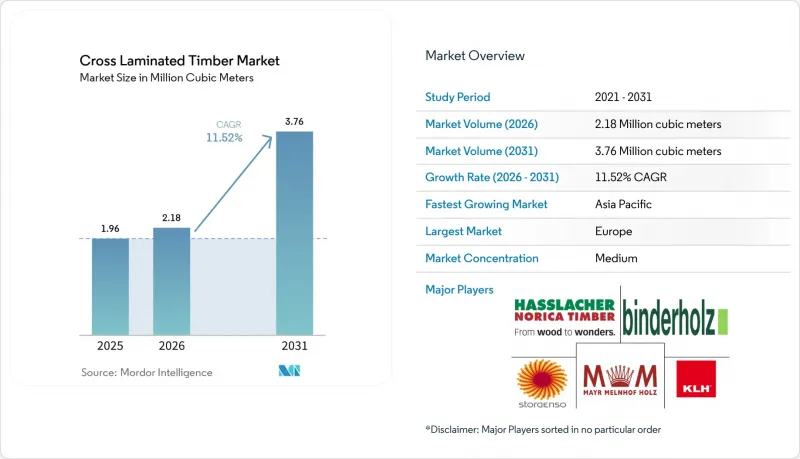

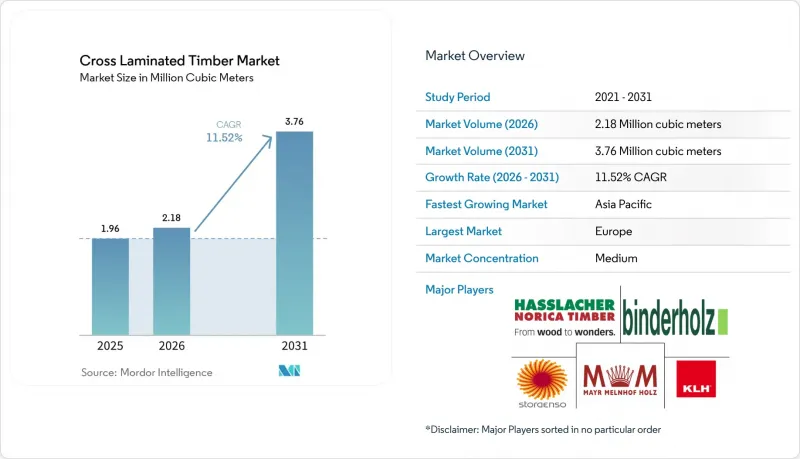

Mordor Intelligence에 의하면, CLT(Cross Laminated Timber) 시장 규모는 2025년 196만 입방미터로 평가되었고, 2026년 218만 입방미터로 추정되고, 2031년까지 376만 입방미터로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 11.52%를 나타낼 것으로 예측됩니다.

본 보고서는 접착 기술별(접착제 접착 및 기계적 체결), 원자재 유형별(스프루스, 소나무 등), 부재 유형별(벽 패널, 바닥 패널 등), 용도별(주거용 및 비주거용), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 수량(입방미터) 기준으로 제시되어 있습니다.

세계 CLT(Cross Laminated Timber) 시장 동향 및 인사이트

유럽연합(EU) 및 북미의 정부 인센티브와 저탄소 건축 기준

EU 지침 2024/1275에 따라 2028년부터 2,000제곱미터를 초과하는 건물에 대해 전 생애 주기 탄소 배출량 평가가 의무화됨에 따라, 설계자들은 철근 콘크리트 구조에 비해 지구 온난화 계수를 최대 75%까지 줄일 수 있는 목재 시스템을 우선적으로 채택하도록 권장받고 있습니다. 캘리포니아주의 ‘Buy Clean’ 2024년 개정판에 따르면, 500만 달러를 초과하는 공공 프로젝트에서 대규모 목조 건축(Mass Timber)에 환경제품선언서(EPD) 규정이 적용되어, 사실상 기준을 충족하지 못하는 공급업체는 배제되게 됩니다. 브리티시컬럼비아주의 ‘스텝 코드’는 바이오 건축물에 대해 배출 크레딧을 제공함으로써, 밴쿠버와 빅토리아의 공동주택 계획에서 CLT(교차 적층 목재)의 도입을 가속화하고 있습니다. 제조업체가 72시간 이내에 검증된 탄소 발자국 데이터를 제출할 수 있게 됨에 따라, 개발업체는 허가 신청 대기 과정에서 규정 준수 측면에서 유리한 고지를 점하고 있습니다. 그 결과 발생하는 수요가 크로스 라미네이트 소재 시장의 급속한 수요 증가를 뒷받침하고 있습니다.

모듈식 및 오프사이트 중층 건축에 대한 수요 증가

공장에서 제조된 CLT 모듈은 현장에서 필요한 인력을 30-40% 줄이고, 공사 기간을 20-25% 단축합니다. 이는 인건비가 높은 도시 지역에서 결정적인 장점이 됩니다. 스톡홀름의 한 개발 프로젝트에서는 조립식 CLT 카세트를 사용하여 11주 만에 방수·방풍 상태를 달성한 반면, 콘크리트 공법으로는 18주가 소요되어 초기 단계에서 180만 달러의 비용 절감을 실현했습니다. 독일의 모듈식 주택 생산량은 2024-2025년 18% 증가했습니다. DIN 4109 규격에 부합하는 방음 성능을 갖춘 CLT 패널을 통해 바닥 구조의 얇은 설계가 가능해졌습니다. 일본은 지방의 CLT 모듈식 주택에 대한 보조금으로 120억 엔을 편성하고, 2028년까지 5,000세대를 건설하는 것을 목표로 하고 있으며, 이는 아시아태평양의 성장을 뒷받침하고 있습니다.

러시아·우크라이나 분쟁 이후 전나무와 가문비나무 가격 변동이 EU의 비용을 끌어올렸습니다.

러시아산 목재에 대한 제재로 인해 2022년 초부터 2024년 중반에 걸쳐 중부 유럽의 가문비나무와 전나무 가격은 22-28% 급등했습니다. 이로 인해 주요 제조업체들의 EBITDA는 2.3포인트 감소했으며, 7곳의 중규모 공장이 폐쇄되거나 합병될 수밖에 없었습니다. 9-12개월간의 고정가격 입찰 요건은 위험을 가중시키고, 프로젝트 수주를 지연시키며, 교차 적층 목재(CLT) 시장의 생산 능력 확대를 저해하고 있습니다.

부문별 분석

2025년 생산량의 90.91%를 차지한 것은 접착제 접합 방식이며, 이는 6-8 MPa의 전단 강도와 전 세계 건축 기준에 부합하는 폴리우레탄 및 MUF계 접착제에 의해 뒷받침되고 있습니다. 이 부문은 연평균 성장률(CAGR) 12.16%를 나타낼 것으로 예측되며, 교차 적층 목재(CLT) 시장 규모는 건축 기준에 힘입은 고층 건축 수요와 계속해서 밀접하게 연동될 전망입니다. 또한, 순환형 경제 프로젝트에서 해체 용이성이 중시됨에 따라 기계적 체결 방식의 대체재도 확대되고 있습니다.

DLT(해체 가능 구조)의 ‘리빙 빌딩 챌린지’ 인증은 틈새 시장의 구매자들을 끌어들이고 있지만, 패널 두께가 20-25% 증가함에 따라 자재비가 15-18% 상승합니다. 리그닌 유래의 신흥 바이오 접착제는 PRG 320의 성능을 유지하면서 화석 탄소 사용량을 40-50% 줄일 수 있을 것으로 기대되며, 접착제 접합 기술의 우위를 한층 더 공고히 하고 있습니다. 기계식 체결 시스템은 광범위한 대체 수단이라기보다는 역사적 건축물의 개보수나 임시 구조물을 위한 귀중한 틈새 시장으로 남을 것입니다.

스프루스는 중부 유럽에서의 풍부한 공급과 뛰어난 강성 대 중량 비율 덕분에 2025년 출하량의 48.21%를 차지했으며, 교차 적층 목재(CLT) 시장에서 가장 큰 점유율을 확보했습니다. 소나무와 전나무가 그 뒤를 이어, 비용 효율을 중시하는 용도나 저층 건축물에 사용되고 있습니다. 더글라스 전나무는 미국 태평양 연안의 제재소들이 내진 지역용으로 이 나무의 15-20% 더 높은 전단 저항성을 활용하고 있기 때문에 연평균 성장률(CAGR) 12.60%로 성장을 지속하고, 있습니다.

더글라스 전나무 CLT는 개정된 건축 기준에서 고밀도 수종을 권장하는 오리건주와 캘리포니아주에서 보급이 확대되고 있습니다. 활엽수 CLT(주로 튤립우드)는 고유한 D급 내화 성능과 시각적 매력 덕분에 고급 부티크 프로젝트에서 높은 수요를 보이고 있습니다.

지역별 분석

유럽은 2025년 생산량의 54.33%를 차지했으며, 독일의 표준 목재 승인 기준에 따른 18미터 높이 제한과, 국내 및 수출 수요를 뒷받침하는 북유럽 국가들의 수직 통합 체제에 힘입고 있습니다. 핀란드의 2025년 생산량은 탄소중립을 향한 로드맵에 따라 수입이 증가하는 영국으로의 패널 출하로 인해 증가했습니다. 남유럽에서는 내진 보강 및 역사적 건축물의 옥상 개보수 공사에 경량 CLT 시스템이 도입되면서 급속한 성장세를 보이고 있습니다.

북미 시장 점유율은 2021년판 IBC(국제건축기준)가 18층 높이의 마스투움 건축을 허용하고 있는 미국 태평양 연안 및 캘리포니아 회랑 지역에 집중되어 있습니다. 캐나다의 ‘CleanBC’ 프로그램은 마스툼의 시범 사업에 5,000만 캐나다 달러를 배정하여 브리티시컬럼비아주 수요를 끌어올렸습니다. 성장은 여전히 제한된 내화성 접착제 선택지와 간헐적인 원자재 가격 변동으로 인해 제약을 받고 있지만, 더글라스 전나무공급 측면에서의 우위는 여전히 탄력을 유지하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 17.38%를 기록하며, CLT 시장에서 가장 빠르게 성장하고 있는 지역입니다. 일본의 개정 건축기준법에 따라, 장관의 승인 없이도 4층 높이의 CLT 구조물이 허가되게 되어, 지방의 주택 보조금 지원 및 도시 지역의 중층 프로젝트가 가능해졌습니다. 중국에서는 선전과 항저우에서 시범 건설을 통해 국산 패널이 시험되고 있으나, 접착제 인증 지연으로 인해 공급량이 제한되고 있습니다. 한국에서는 그린빌딩 크레딧이 시장 점유율 확대를 주도하고 있는 반면, 동남아시아는 습도와 관련된 내구성 비용 문제로 인해 아직 발전 단계에 머물러 있습니다. 남미와 중동은 각각 세계 시장 점유율에서 뒤처져 있지만, 2024년 브라질의 공장 투자는 해당 지역의 잠재적인 보급 가능성을 시사하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the cross laminated timber market size is projected to expand from 1.96 Million cubic meters in 2025 and 2.18 Million cubic meters in 2026 to 3.76 Million cubic meters by 2031, registering a CAGR of 11.52% between 2026 to 2031.

This report is Segmented by Bonding Technology (Adhesive-Bonded and Mechanically Fastened), Raw-Material Species (Spruce, Pine, and More), Element Type (Wall Panels, Floor Panels, and More), Application (Residential and Non-Residential), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Cubic Meters).

Global Cross Laminated Timber Market Trends and Insights

Government Incentives and Low-Carbon Building Codes in the European Union and North America

Mandatory whole-life-carbon assessments for buildings above 2,000 m2 from 2028 under EU Directive 2024/1275 are prompting specifiers to prioritize timber systems that cut global-warming potential by up to 75% versus steel-concrete frames. California's 2024 Buy Clean update extends environmental-product-declaration rules to mass-timber in public projects above USD 5 million, effectively gating non-compliant suppliers. British Columbia's Step Code offers emissions credits for bio-based structures, accelerating CLT uptake in Vancouver and Victoria multifamily schemes. Because fabricators can now deliver verified carbon footprints within 72 hours, developers gain a compliance edge in permitting queues. Resulting demand underpins the cross laminated timber market's rapid volume gains.

Growing Modular and Off-Site Mid-rise Construction Demand

Factory-built CLT modules trim on-site labor needs by 30-40% and shorten schedules 20-25%, a decisive benefit in high-wage urban centers. A Stockholm development reached weathertight status in 11 weeks using prefabricated CLT cassettes versus 18 weeks for concrete, saving USD 1.8 million in preliminaries. Germany's modular housing output climbed 18% during 2024-2025; acoustic-performing CLT panels meeting DIN 4109 standards enable thinner floor assemblies. Japan earmarked JPY 12 billion to subsidize rural CLT modular homes, targeting 5,000 units by 2028 and reinforcing Asia-Pacific growth.

Volatile Spruce and Fir Prices Post-Russia-Ukraine Conflict Raising EU Costs

Central European spruce and fir prices jumped 22-28% between early 2022 and mid-2024 following sanctions on Russian timber, trimming large fabricator EBITDA by 2.3 points and forcing seven mid-sized plants to shutter or merge. Fixed-price bid requirements of 9-12 months exacerbate risk, delaying project awards and tempering capacity expansions within the cross laminated timber market.

Other drivers and restraints analyzed in the detailed report include:

- Carbon-Pricing Escalation in Europe Favouring Low-Embodied-Carbon Cross-Laminated Timber

- Adoption of Long-Span CLT Rib / Hybrid Floor Systems (more than 12 M) Unlocking New Use-Cases

- Moisture Absorption Related Durability Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Adhesive-bonded represented 90.91% of 2025 volume, underpinned by polyurethane and MUF chemistries that deliver 6-8 MPa shear strength and global code acceptance. This segment is forecast to grow at 12.16% CAGR, keeping the cross laminated timber market size firmly aligned with code-driven high-rise demand. Mechanically fastened alternatives are also expanding as circular-economy projects prize disassembly.

DLT's Living Building Challenge credentials entice niche adopters, yet 20-25% thicker panels raise material outlays by 15-18%. Emerging bio-based adhesives derived from lignin promise 40-50% fossil-carbon reduction while retaining PRG 320 performance, reinforcing adhesive-bonded leadership. Mechanically fastened systems will remain a valuable niche for heritage retrofits and temporary structures rather than a broad substitute.

Spruce captured 48.21% of 2025 volume thanks to abundant Central European supply and favorable stiffness-to-weight attributes, securing the largest slice of cross laminated timber market share. Pine and fir follow, serving cost-sensitive or low-rise applications. Douglas-fir records a 12.60% CAGR as U.S. Pacific mills exploit its 15-20% superior shear resistance for seismic zones.

Douglas-fir CLT has gained traction in Oregon and California where updated codes favor high-density species. Hardwood CLT - principally tulipwood - commands premium boutique projects due to intrinsic Class D fire ratings and visual appeal.

Geography Analysis

Europe maintained 54.33% of 2025 volume, supported by Germany's 18-meter height allowance for standard timber approvals and Nordic vertical integration that feeds domestic and export demand. Finland's 2025 output grew owing to shipping panels to the UK, where net-zero pathways drive imports. Southern Europe shows rapid catch-up as seismic retrofits and heritage rooftop conversions adopt lightweight CLT systems.

North America's share concentrates in the United States in the Pacific and Californian corridors, where the 2021 IBC permits 18-story mass-timber buildings. Canada's CleanBC program reserved CAD 50 million for mass-timber pilots, elevating British Columbia's provincial demand. Growth is tempered by still-limited fire-rated adhesive options and intermittent feedstock volatility, yet Douglas-fir supply advantages sustain momentum.

Asia-Pacific is the fastest-growing cross laminated timber market region at 17.38% CAGR. Japan's revised Building Standard Law allows four-story CLT structures without ministerial approval, unlocking rural housing subsidies and mid-rise urban projects. China's pilot builds in Shenzhen and Hangzhou test domestic panels, but adhesive certification delays restrain volume. Green-building credits drive South Korea's share, while Southeast Asia remains nascent because of humidity-related durability costs. South America and the Middle East trail with global share apiece, though Brazil's 2024 plant investment hints at latent regional adoption.

- B&K Structures

- Binderholz GmbH

- Dold Holzwerke GmbH

- DRJ Wood Innovations

- Eugen Decker

- HASSLACHER Holding GmbH

- KLH Massivholz GmbH

- Mayr-Melnhof Holz Holding AG

- Mercer International Inc.

- Nordic Structures

- Pfeifer Group

- Schilliger Holz AG

- SmartLam

- Sterling Solutions LLC

- Stora Enso

- Structa

- XLAM INDUSTRIE

- ZUBLIN Timber GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Incentives and Low-Carbon Building Codes in the European Union and North America

- 4.2.2 Growing Modular and Off-Site Mid-Rise Construction Demand

- 4.2.3 Carbon-Pricing Escalation in Europe Favouring Low-Embodied-Carbon Cross-Laminated Timber

- 4.2.4 Adoption of Long-Span CLT Rib / Hybrid Floor Systems (more than 12 M) Unlocking New Use-Cases

- 4.2.5 AI-Driven Design for Manufacture Platforms Cutting Engineering Lead-Times

- 4.3 Market Restraints

- 4.3.1 Volatile Spruce and Fir Prices Post-Russia-Ukraine Conflict Raising EU Costs

- 4.3.2 Moisture Absorption Related Durability Risks

- 4.3.3 Limited Fire Rated Adhesive Options That Pass Annex B Tests (U.S.)

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Bonding Technology

- 5.1.1 Adhesive-Bonded

- 5.1.2 Mechanically Fastened

- 5.2 By Raw-Material Species

- 5.2.1 Spruce

- 5.2.2 Pine

- 5.2.3 Fir

- 5.2.4 Douglas-Fir

- 5.2.5 Hardwood (e.g., Tulipwood, Oak)

- 5.3 By Element Type

- 5.3.1 Wall Panels

- 5.3.2 Floor Panels

- 5.3.3 Roof Panels

- 5.3.4 Others (Elevator/Stair Cores, Bridge Decks, and Other Infrastructure)

- 5.4 By Application

- 5.4.1 Residential

- 5.4.2 Non-Residential

- 5.4.2.1 Commercial

- 5.4.2.2 Industrial / Institutional

- 5.4.2.3 Other Applications (Military Housing, Emergency Shelters, Event Structures)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 Thailand

- 5.5.1.6 Vietnam

- 5.5.1.7 Malaysia

- 5.5.1.8 Indonesia

- 5.5.1.9 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 NORDIC Countries

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 South Africa

- 5.5.5.5 Nigeria

- 5.5.5.6 Egypt

- 5.5.5.7 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes global and market-level overview, core segments, financials, strategic info, market rank/share, products and services, recent developments)

- 6.4.1 B&K Structures

- 6.4.2 Binderholz GmbH

- 6.4.3 Dold Holzwerke GmbH

- 6.4.4 DRJ Wood Innovations

- 6.4.5 Eugen Decker

- 6.4.6 HASSLACHER Holding GmbH

- 6.4.7 KLH Massivholz GmbH

- 6.4.8 Mayr-Melnhof Holz Holding AG

- 6.4.9 Mercer International Inc.

- 6.4.10 Nordic Structures

- 6.4.11 Pfeifer Group

- 6.4.12 Schilliger Holz AG

- 6.4.13 SmartLam

- 6.4.14 Sterling Solutions LLC

- 6.4.15 Stora Enso

- 6.4.16 Structa

- 6.4.17 XLAM INDUSTRIE

- 6.4.18 ZUBLIN Timber GmbH

7 Market Opportunities and Future Outlook

- 7.1 Technological Advancements and Innovations in CLT Manufacturing

- 7.2 White-space and Unmet-Need Assessment