|

시장보고서

상품코드

2063564

심부전 POC 및 LOC 장치 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Heart Failure POC And LOC Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

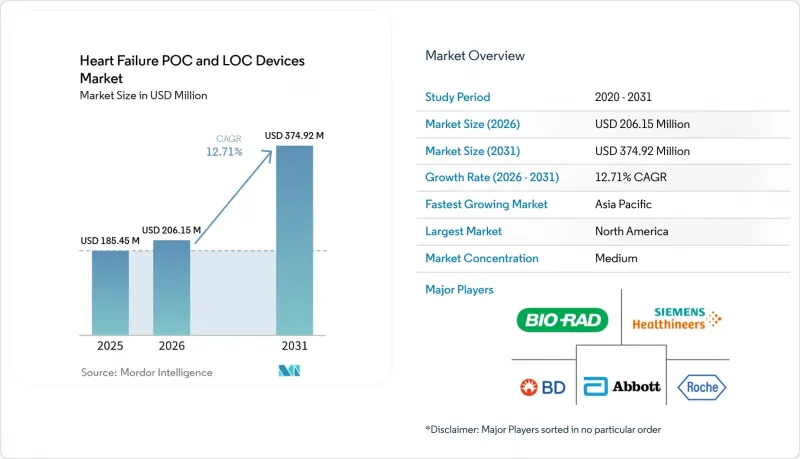

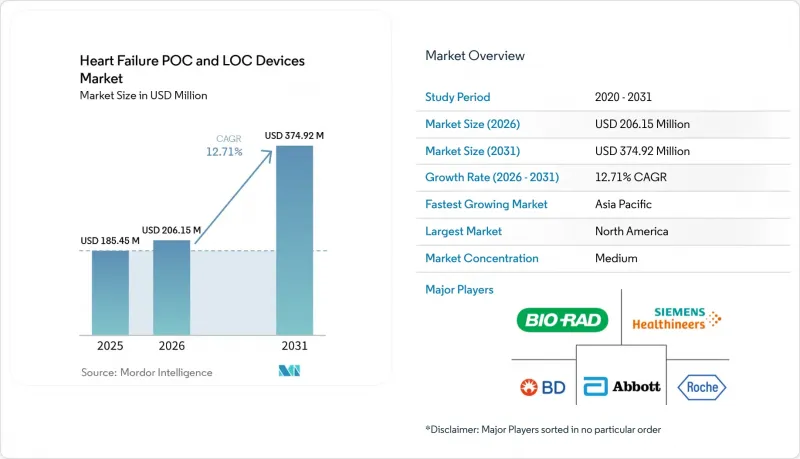

심부전 POC 및 LOC 장치 시장 규모는 2025년 1억 8,545만 달러로 평가되었고, 2026년에는 2억 615만 달러로 추정되고, 2026-2031년 CAGR 12.71%로 성장을 지속할 전망이며, 2031년에는 3억 7,492만 달러에 이를 것으로 예측됩니다.

본 보고서는 기기 유형별(현장 진단(POC) 기기 등), 검사 유형별(단백질체학, 대사체학, 유전체학), 플랫폼별(면역형광 판독기 등), 최종 사용자별(병원 및 통합 의료 네트워크, 1차 진료 및 일반 진료 클리닉 등), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 심부전 POC 및 LOC 장치 시장 동향과 인사이트

응급의학과 및 1차 진료 분야에서 지침에 기반한 나트륨 이뇨 펩타이드 검사 도입

현재 진단학회는 환자가 도착한 지 1시간 이내에 BNP 또는 NT-proBNP 검사 결과를 제시할 것을 요구하고 있지만, 중앙검사실에서는 성수기에는 이를 달성하는 경우가 드뭅니다. 미국 심장학회도 2025년에 이 방침에 동의함으로써, 사실상 응급실에서 검사 대상이 되는 환자 수를 두 배로 늘렸습니다. 영국의 지침에서는 일반의에게 환자를 의뢰하기 전에 NT-proBNP 검사를 통해 심부전을 배제하도록 지시하고 있으며, 이에 따라 1차 진료 현장에서의 도입이 가속화되고 있습니다. 이러한 정책에 따라 병원에서는 검사를 중앙 검사실에서 분류 구역으로 이관해야 하며, 진료소에서 근무하는 임상의들에게는 휴대용 리더기 도입이 권장되고 있습니다. ISO 15189 및 EU IVDR 규격에 대한 적합성을 인증받을 수 있는 공급업체는 시장 진출이 가속화되고, 입찰 참가 자격도 확대되고 있습니다.

아시아태평양 지역의 의료 시스템이 POCT 인프라에 투자

아시아태평양 지역 각국 정부는 분산형 진단을, 진료 경로를 단축하고 검사실 간 역량 격차를 해소하기 위한 비용 대비 효과가 높은 방법으로 보고 있습니다. 중국은 2025년에 현립 병원에 심장 바이오마커 분석 장비를 도입하기 위해 120억 위안(17억 달러)을 예산에 편성했습니다. 인도의 ‘아유슈만 바라트’ 프로그램은 검사 결과를 국가 건강 기록 시스템에 업로드할 수 있는 연결형 기기를 권장하고 있습니다. 일본은 2025년에 NT-proBNP의 보험 급여 상한선을 검사 1회당 1,800엔(12달러)으로 인상하여, 병원의 투자 회수 기간을 절반으로 단축했습니다. 한국은 2025년, POCT용 BNP 검사 비용을 중앙 검사실과 동일한 수준으로 조정하여, 기존에 존재하던 비용상의 불이익을 해소했습니다. 이러한 인센티브 덕분에, 기기 보급률이 여전히 유럽과 미국에 미치지 못하는 아시아태평양에 대한 판매업체들의 집중이 가속화되고 있습니다.

BNP 대 NT-proBNP : 측정 변동성 및 약물 간섭의 위험

사큐비트릴·발살탄은 BNP를 억제하지만, NT-proBNP는 억제하지 않기 때문에 측정값에 불일치가 발생하여 환자의 분류를 오도할 가능성이 있습니다. 현재 순환기학회는 치료 중인 환자에게 NT-proBNP 검사를 권장하고 있지만, 시약의 화학적 성질이 단순하기 때문에 많은 저비용 POC 플랫폼에서는 BNP 검사만 제공합니다. 미국심장협회는 임상의들에게 ARNI 사용 내역을 기록하고 BNP 기준치를 조정할 것을 권고하고 있으며, 이러한 복잡성으로 인해 시간 단축의 이점이 상쇄되고 있습니다. IFCC의 초기 표준화 작업에도 불구하고, 플랫폼 간 변동폭은 여전히 최대 20%에 달할 전망입니다. 제조업체는 새로운 보편적 기준에 맞추어 분석법의 재교정을 수행해야 하지만, 이 과정은 2028년까지 길어질 가능성이 있습니다.

부문별 분석

2025년 기준으로, 단백질체학 검사는 심부전 POC 및 LOC 장치 시장 점유율 51.4%를 차지했습니다. 이는 주로 트리아지 알고리즘 전반에 걸쳐 BNP 및 NT-proBNP의 사용이 정착되었기 때문입니다. 대사체학 패널은 연평균 성장률(CAGR) 13.67%로 성장하고 있습니다. 이는 세라마이드 및 아실카르니틴 바이오마커를 통해 환자의 22%가 고위험군으로 재분류되어, 기기 치료의 조기 시작이 촉진되기 때문입니다. 단백질체학 검사는 여전히 광범위한 보험 적용과 의사들의 익숙한 사용 방식이라는 이점을 누리고 있지만, 전문 심부전 센터의 임상의들은 예후를 미세하게 조정하기 위해 대사체학 검사 패널을 처방하기 시작했습니다. 각 제조업체들은 두 가지 분석 대상 물질을 단일 카트리지에 통합하기 위한 경쟁을 벌이고 있으며, 이를 통해 지침 준수와 예후 예측 능력 향상을 동시에 달성할 수 있을 것으로 보입니다. 유전체 검사는 보험사가 이를 종종 임상시험 단계로 간주하기 때문에 여전히 시험적인 사용에 그치고 있지만, 임상시험에서 양호한 결과가 나오면 2028년까지 보험 적용 범위가 확대될 가능성이 있습니다.

대사체학의 확대는 공급업체 간의 역학 관계도 변화시키고 있습니다. 지질 오믹스 분야의 전문 지식을 갖춘 스타트업 기업들은 분석 장비 설치 공간을 확보하기 위해 기존 플랫폼 소유주들과 제휴하고 있습니다. 한편, 병원 검사실에서는 질조정생존년(QALY)당 대사 오믹스 검사 비용을 이식형 혈역학 모니터와 비교 검토하고 있습니다. 만약 보험 환급 격차가 해소된다면, 첨단 치료 과정에서 대사 오믹스용 카트리지가 단일 마커 검사를 대체할 가능성이 있습니다. 그때까지는 심부전용 POC(현장 검사) 및 LOC(현장 검사) 기기 시장에서 단백질체학 검사 시장 규모는 새로운 분야를 계속해서 압도하겠지만, 그 성장률은 대사 오믹스의 성장 곡선에는 미치지 못할 것입니다.

2025년에는 마이크로유체 디지털 면역 분석 시스템이 플랫폼 매출의 46.40%를 차지했으며, 소량의 검체에서도 뛰어난 분석 감도를 보여주었습니다. 병원에서는 간호사의 작업 절차를 최소화하면서 15분 미만의 처리 시간을 실현하기 위해 이러한 시스템을 도입하고 있습니다. 한편, 면역형광 분석기는 도입 비용이 저렴하고 더 폭넓은 감염증 검사 항목을 수행할 수 있어 연평균 성장률(CAGR) 13.32%로 성장하고 있습니다. 마이크로플루이딕스 플랫폼을 활용한 심부전 POC(현장 진단) 및 LOC(현장 검사) 기기 시장 규모는 꾸준히 확대될 것으로 예상되지만, 초저 검출 한계보다 초기 도입 비용의 저렴함을 우선시하는 지역 진료소에서는 형광 시스템에 시장 점유율을 빼앗길 것으로 보입니다.

벤더의 로드맵을 통해 두 기술의 융합을 엿볼 수 있습니다. 지멘스는 시간당 30건의 검사를 처리할 수 있는 능력과 자동 품질 관리(QC) 기능을 겸비한 화학발광식 벤치탑 분석 장치를 출시했습니다. 콴테릭스(Quantex)는 단일 분자 어레이를 채택한 휴대용 리더기의 CE-IVD 인증을 획득함으로써, 마이크로플루이딕스 기술을 과거 형광법이 독점하던 가격대로 끌어올렸습니다. 설비 투자 예산이 빠듯한 상황에서 카트리지의 최소 구매 수량과 연계된 플랫폼 임대 계약이 일괄 구매를 대체해 가고 있으며, 이를 통해 공급업체에는 지속적인 수익이 발생하고, 구매자에게는 초기 비용 절감으로 이어지고 있습니다. 관리자들이 시약 소비율이나 임상 핵심 성과 지표(KPI)를 추적할 수 있는 대시보드를 요구함에 따라, 클라우드 분석과의 통합이 각 제품의 차별화를 더욱 강화할 것입니다.

지역별 분석

2025년, 북미는 전 세계 매출의 46.25%를 차지했습니다. 이는 메디케어의 검사당 환급액이 24달러로 인상되고, 메디케어 어드밴티지 플랜의 사전 승인 제도가 폐지된 데 따른 것입니다. 2024년부터 2025년에 걸쳐 여러 장비가 CLIA 면제 인증을 획득함에 따라, 미국 의사 진료소 내 검사실에서는 BNP 검사가 확대되었습니다. 캐나다에서는 지방 응급의료 부서에서 POC 프로그램의 시범 운영이 진행되고 있지만, 주별 예산 격차로 인해 전면적인 도입은 지연되고 있습니다. 멕시코의 사립 병원들은 프리미엄 응급 서비스를 차별화하기 위해 분석 장비를 도입하고 있지만, 중앙 검사실 인프라가 도시 지역에 집중되어 있어 공공 부문에서의 도입은 더딘 실정입니다.

아시아태평양은 가장 빠르게 성장하는 지역으로, 2031년까지 연평균 성장률(CAGR) 13.48%를 나타낼 것으로 전망됩니다. 중국의 현립 병원에 대한 지원 정책에 힘입어, 심장·대사용 복합 분석 장치의 대량 발주가 촉진되고 있습니다. 인도의 조달 규정에 따르면, Ayushman Bharat Digital Health 네트워크로 데이터를 전송하는 클라우드 연결형 리더기가 우선적으로 채택되고 있습니다. 일본에서는 NT-proBNP 검사의 보험 급여액이 1회당 12달러로 인상됨에 따라 투자 회수 기간이 절반으로 단축되었고, 중규모 병원의 설비 투자 예산을 확보할 수 있게 되었습니다. 한국, 호주, 동남아시아에서도 비슷한 경향이 나타나고 있으며, 의사 부족 문제를 해소하고 환자의 통원 거리를 단축하기 위해 분산형 진단이 중시되고 있습니다.

유럽은 성숙한 시장이지만, 성장 속도는 완만합니다. ESC 지침에 따르면, 응급실 도착 후 60분 이내에 BNP 또는 NT-proBNP를 측정해야 하며, 이것이 카트리지에 대한 꾸준한 수요를 뒷받침하고 있습니다. 그러나 EU IVDR 준수로 인해 검증 비용이 증가하고 제품 출시가 지연됨에 따라, 공급업체의 규제 대응 일정이 장기화되고 있습니다. 독일은 1인당 분석기 보급률에서 선두를 달리고 있지만, 영국에서는 NHS의 자금 조달 주기에 맞추어 도입이 진행되고 있습니다. 중동 및 아프리카 및 남미는 여전히 초기 단계에 있으며, 걸프 지역 국가들과 브라질의 유력한 사립 병원들이 도입을 주도하고 있지만, 대규모 공공 입찰은 드문 임베디드니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the heart failure pOC and lOC devices market size is expected to grow from USD 185.45 million in 2025 to USD 206.15 million in 2026 and is forecast to reach USD 374.92 million by 2031 at 12.71% CAGR over 2026-2031.

This report is Segmented by Device Type (Point-Of-Care (POC) Devices, and More), Test Type (Proteomic, Metabolomic, Genomic), Platform (Immunofluorescence Readers, and More), End User (Hospitals & IDNs, Primary Care & GP Clinics, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Heart Failure POC And LOC Devices Market Trends and Insights

Guideline-Backed Natriuretic Peptide Testing Adoption in ED and Primary Care

Diagnostic societies now require BNP or NT-proBNP results within 1 hour of patient arrival, which central laboratories rarely achieve during peak periods . U.S. cardiology bodies echoed this stance in 2025, effectively doubling the pool of patients eligible for testing in emergency departments. Primary-care uptake is accelerating following the United Kingdom guidance instructing general practitioners to rule out heart failure with NT-proBNP before making referrals. These policies require hospitals to relocate assays from the core lab to triage bays and encourage office-based clinicians to install handheld readers. Vendors that can certify devices to ISO 15189 and EU IVDR standards are enjoying faster market clearance and wider tender eligibility.

APAC Health-System Investments in POCT Infrastructure

Asia-Pacific governments view decentralized diagnostics as a cost-effective way to shorten referral pathways and address uneven laboratory capacity. China earmarked CNY 12 billion (USD 1.7 billion) in 2025 to outfit county hospitals with cardiac biomarker analyzers. India's Ayushman Bharat program favors connected devices that upload results to the national health records system. Japan raised the NT-proBNP reimbursement ceiling to JPY 1,800 (USD 12) per test in 2025, halving payback periods for hospitals. South Korea matched central-lab fees for POC BNP in 2025, eliminating historical cost penalties. These incentives accelerate the distributor's focus on APAC, where device penetration still trails that of the West.

BNP vs NT-proBNP Assay Variability and Drug Interference Risks

Sacubitril-valsartan suppresses BNP but not NT-proBNP, generating discordant readings that can misclassify patients. Cardiology societies now favor NT-proBNP for treated patients, yet many low-cost POC platforms offer only BNP because of simpler reagent chemistry. The American Heart Association advises clinicians to record ARNI use and adjust BNP cutoffs, adding complexity that erodes time savings. Cross-platform variability of up to 20% persists despite early harmonization work by the IFCC. Manufacturers must recalibrate assays to emerging universal standards, a process that could stretch into 2028.

Other drivers and restraints analyzed in the detailed report include:

- Microfluidic/Digital LOC NT-proBNP Assays Enabling Finger-Stick Workflows

- Operational Gains from Rapid NP Testing

- Competition from Point-of-Care Ultrasound and Integrated Care Pathways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Proteomic assays captured a 51.4% Heart Failure POC and LOC Devices market share in 2025, largely due to entrenched use of BNP and NT-proBNP across triage algorithms. Metabolomic panels are climbing at a 13.67% CAGR because ceramide and acylcarnitine signatures reclassify 22% of patients into higher-risk strata, prompting earlier device therapy initiation . Proteomic testing still benefits from widespread reimbursement and physician familiarity, but clinicians at specialty heart-failure centers are beginning to order metabolomic panels for prognostic fine-tuning. Manufacturers are racing to combine both analyte classes on single cartridges, which could unify guideline compliance with incremental prognostic power. Genomic assays remain in pilot use because payers frequently deem them investigational, yet successful trial outcomes could unlock coverage by 2028.

Metabolomic expansion is also reshaping supplier dynamics. Startups with lipidomics expertise partner with established platform owners to secure analyzer shelf space, while hospital labs benchmark metabolomic cost per quality-adjusted life-year against implantable hemodynamics monitors. If reimbursement parity emerges, metabolomic cartridges could displace single-marker assays in advanced-care pathways. Until then, the Heart Failure POC and LOC Devices market size for proteomic testing will continue to dwarf newer segments, though its growth will trail the metabolomic curve.

Microfluidic digital immunoassay systems accounted for 46.40% of platform revenue in 2025, demonstrating superior analytical sensitivity at low sample volumes. Hospitals deploy them to achieve sub-15-minute turnaround while minimizing nurse handling steps. Immunofluorescence readers, however, are expanding at a 13.32% CAGR because they cost less to acquire and can run a broader menu of infectious-disease tests. The Heart Failure POC and LOC Devices market size for microfluidic platforms is forecast to rise steadily but will concede share to fluorescence systems in community clinics that prioritize upfront affordability over ultralow limits of detection.

Vendor road maps reveal convergence. Siemens launched a chemiluminescence benchtop analyzer that combines 30-test hourly throughput with automatic QC. Quanterix obtained CE-IVD for a handheld reader using single-molecule arrays, pushing microfluidics into price points once reserved for fluorescence. As capital budgets tighten, platform leases bundled with cartridge minimums are replacing outright purchases, generating recurring revenue for suppliers and lower initial outlays for buyers. Integration with cloud analytics will further differentiate offers, as administrators seek dashboards that track reagent burn rates and clinical key performance indicators.

Geography Analysis

North America accounted for 46.25% of global revenue in 2025, supported by Medicare reimbursement rising to USD 24 per test and the elimination of prior authorizations for Medicare Advantage plans. U.S. physician-office laboratories expanded BNP testing after multiple devices earned CLIA-waived status in 2024-2025. Canada pilots POC programs in rural emergency departments, though budget variability among provinces slows full rollout. Mexico's private hospitals adopt analyzers to differentiate premium emergency services, but public-sector uptake lags because central-lab infrastructure is concentrated in urban hubs.

Asia-Pacific is the fastest-growing region and will post a 13.48% CAGR through 2031. China's county-hospital stimulus spurs volume orders for combined cardiac and metabolic analyzers. India's procurement rules favor cloud-connected readers that feed data into the Ayushman Bharat Digital Health network. Japan's reimbursement hike to USD 12 per NT-proBNP test halves payback periods and unlocks capital budgets in mid-size hospitals. South Korea, Australia, and Southeast Asia replicate the pattern, emphasizing decentralized diagnostics to alleviate physician shortages and reduce patient travel distances.

Europe holds a mature but slower-growing position. ESC guidelines require BNP or NT-proBNP within 60 minutes of ED arrival, anchoring steady cartridge demand. However, compliance with the EU IVDR raises validation costs and delays launches, stretching vendor regulatory timelines. Germany leads per-capita analyzer density, while the United Kingdom aligns adoption with NHS funding cycles. Middle East & Africa and South America remain early-stage, with flagship private hospitals in the Gulf and Brazil pioneering placements, but large public tenders are scarce.

- Abaxis, Inc.

- Abbott Laboratories

- Acon Laboratories

- Beckton Dickinson

- bioMerieux S.A.

- Bio-Rad Laboratories

- BioTelemetry

- Boston Scientific

- Danaher

- Roche

- GE Healthcare

- Instrumentation Laboratory

- Koninklijke Philips

- Masimo

- Medtronic

- Nexus Dx, Inc.

- QuidelOrtho

- Shenzhen EDAN Instrument Co., Ltd.

- Siemens Healthineers

- Trinity Biotech

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Guideline-Backed Natriuretic Peptide Testing Adoption In ED And Primary Care (HF Triage and Rule-Out)

- 4.2.2 Operational Gains from Rapid NP Testing (Shorter ED LOS, Lower Costs, Faster Disposition)

- 4.2.3 CLIA-Waived BNP Availability Enabling Decentralized US Testing (Urgent Care, Physician Office)

- 4.2.4 APAC Health-System Investments in POCT Infrastructure Accelerating Adoption

- 4.2.5 Microfluidic/Digital LOC NT-Probnp Assays Enabling Fingerstick, Near-Patient Workflows

- 4.2.6 Rise of Prognostic Markers (Sst2) And Multi-Marker HF Panels in POC Pathways

- 4.3 Market Restraints

- 4.3.1 Mixed/Neutral RCT Evidence on Triage Outcomes for Routine NP POCT In Prehospital/ED Settings

- 4.3.2 Moderate-Complexity Status of Many NT-proBNP POC Assays Limits Decentralization and Staffing Flexibility

- 4.3.3 BNP vs NT-proBNP Assay Variability and Drug (ARNI) Interference Risks Complicate Interpretation

- 4.3.4 Competition From Point-Of-Care Ultrasound (POCUS) And Integrated Care Pathways Reduces Incremental Value in Some ED Cohorts

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Point-of-Care (POC) Devices

- 5.1.2 Lab-on-Chip (LOC) Devices

- 5.2 By Test Type

- 5.2.1 Proteomic testing

- 5.2.2 Metabolomic testing

- 5.2.3 Genomic testing

- 5.3 By Platform

- 5.3.1 Immunofluorescence readers

- 5.3.2 Benchtop chemiluminescence POC

- 5.3.3 Microfluidic digital immunoassay

- 5.4 By End User

- 5.4.1 Hospitals & IDNs

- 5.4.2 Primary Care & GP Clinics

- 5.4.3 Diagnostic Centers

- 5.4.4 EMS Providers

- 5.4.5 Retail Clinics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Abaxis, Inc.

- 6.3.2 Abbott Laboratories

- 6.3.3 ACON Laboratories, Inc.

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 bioMerieux S.A.

- 6.3.6 Bio-Rad Laboratories, Inc.

- 6.3.7 BioTelemetry, Inc.

- 6.3.8 Boston Scientific Corporation

- 6.3.9 Danaher Corporation

- 6.3.10 F. Hoffmann-La Roche Ltd

- 6.3.11 GE HealthCare

- 6.3.12 Instrumentation Laboratory

- 6.3.13 Koninklijke Philips N.V.

- 6.3.14 Masimo Corporation

- 6.3.15 Medtronic plc

- 6.3.16 Nexus Dx, Inc.

- 6.3.17 QuidelOrtho Corporation

- 6.3.18 Shenzhen EDAN Instrument Co., Ltd.

- 6.3.19 Siemens Healthineers AG

- 6.3.20 Trinity Biotech PLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment