|

시장보고서

상품코드

2063969

360도 피드백 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)360-Degree Feedback Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

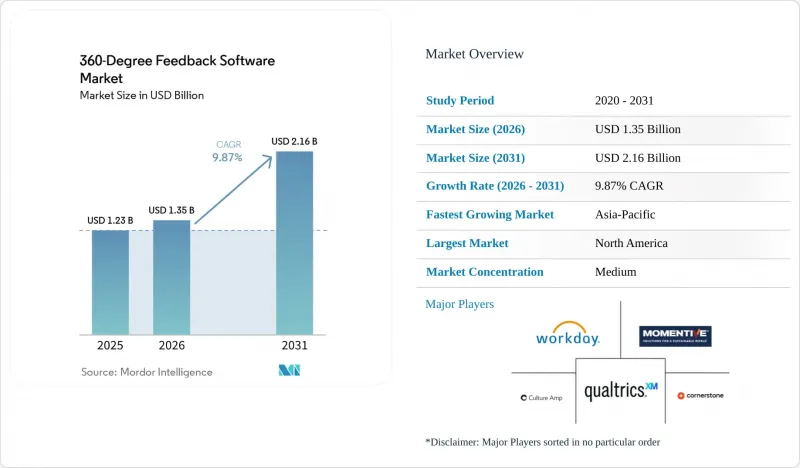

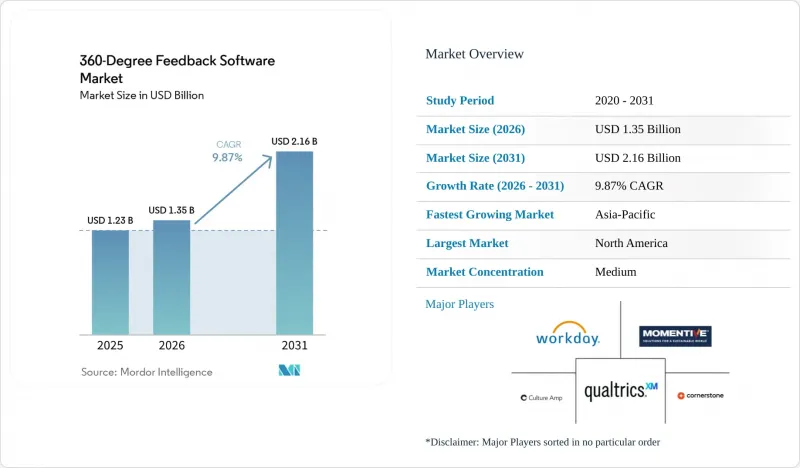

Mordor Intelligence에 의하면, 360도 피드백 소프트웨어 시장 규모는 2025년 12억 3,000만 달러에서 2026년에는 13억 5,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 9.87%로 성장을 지속하여, 2031년에는 21억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 형태(클라우드, On-Premise, 하이브리드), 기업 규모(중소기업 및 대기업), 업종(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학 등), 가격 모델(구독형 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 360도 피드백 소프트웨어 시장 동향 및 인사이트

AI를 활용한 맞춤형 피드백 워크플로우

현재 생성형 AI는 개별 능력 격차에 맞추어 질문 세트를 조정하고, 원시 평가자 데이터를 신속하게 코칭 팁으로 변환함으로써, 인사이트를 얻기까지 걸리는 시간을 몇 주에서 몇 시간으로 단축하고 있습니다. Microsoft Viva Glint, SAP SuccessFactors 및 Oracle HCM Cloud는 모두 감정 추세를 시각화하고 평가 불일치를 지적하는 능동적인 AI 기능을 출시했으며, 이에 따라 유럽 인사 팀의 48%가 2025년에 전용 AI 성과 관리 도구를 시범 도입할 것으로 예측됩니다. 실시간 개인화 및 편향성 검증을 통합하지 못하는 공급업체는 구매자들이 이러한 기능을 ‘필수 요건’으로 간주하는 경향이 강해짐에 따라 가격 경쟁에 직면할 위험이 있습니다.

지속적 성과 관리 제품군에 360도 피드백 통합

연간 평가 대신 분기별 검토가 주류를 이루게 되면서, 조직은 피드백, 목표 추적, 동료 평가를 통합된 워크플로우에 통합해야 하는 상황에 직면해 있습니다. 워크데이가 2025년에 11억 달러에 사나를 인수한 것은 AI 기반 인재 인텔리전스를 자사의 전체 HCM 제품군에 통합하기 위한 조치로 평가되며, 고도로 통합된 분석이 현재 승계 계획 및 역량 개발에 얼마나 큰 영향을 미치고 있는지를 여실히 보여주고 있습니다. 따라서 360도 피드백 소프트웨어 시장에서 솔루션 간 통합이 주요 구매 기준으로 자리 잡고 있어, 독립 벤더들은 ‘자체 개발할지, 파트너와 제휴할지’에 대한 결정을 내려야 하는 상황에 직면해 있습니다.

데이터 개인정보 보호 및 심리 측정 편향에 대한 우려

GDPR(EU 개인정보보호규정)이나 캘리포니아주 ADMT와 같은 엄격한 법규로 인해 알고리즘에 의한 의사결정의 투명성이 요구되면서, 공급업체의 규정 준수 비용이 증가하고 소송 위험이 높아지고 있습니다. 2025년 『Journal of Applied Psychology』지에 실린 기사에 따르면, 대기업의 응답 중 30%가 평가자의 편향으로 인해 왜곡된 것으로 밝혀졌으며, 구매자들은 암호화, 감사 로그, 통계적 편향 검증을 요구하고 있습니다. 이러한 안전 대책이 뒤처진 공급업체는 조달 지연이나 평판 하락이라는 위험에 직면해 있습니다.

부문별 분석

2025년, 360도 피드백 소프트웨어 시장 매출의 78.92%를 소프트웨어가 차지하며, 이는 라이선스 비용 및 구독료의 우위를 반영한 것이지만, 서비스 부문은 2031년까지 연평균 성장률(CAGR) 10.96%로 확대될 것으로 예상되어, 시장 전체의 성장률을 상회할 전망입니다. SurveyConnect의 조사에 따르면, 직원 수 5,000명 이상의 기업 인사 부서의 40%가 1개월 이내에 실용적인 대시보드를 구축하지 못하고 있으며, 이로 인해 자문 프로젝트에 대한 수요가 증가하고 있습니다. 그 결과, 각 벤더사는 현재 분기별 캘리브레이션 워크숍을 프리미엄 플랜에 포함시켜 소프트웨어 및 서비스를 하나의 구독 서비스로 통합하고 있습니다.

360도 피드백 소프트웨어 시장은 서비스 파트너들이 평가자 교육, 심리 측정을 통한 타당성 검증, 그리고 문화 변화 로드맵을 통해 수익을 창출함으로써 혜택을 보고 있습니다. 특히, GDPR(EU 개인정보보호규정)이나 의료 인증과 같이 제3자에 의한 증명이 요구되는 규제가 엄격한 업계에서는 이러한 경향이 두드러집니다. Paychex가 2025년 1월에 발표한 Paycor의 41억 달러 규모 인수에서는 연간 8,000만 달러 이상에 달할 것으로 예상되는 비용 시너지 효과 외에도, 약 74만 5,000개사에 달하는 통합 고객 기반을 대상으로 한 교차 판매 도입 및 자문 서비스와 관련된, 상당한 수익 시너지 기회가 강조되었습니다.

2025년에는 확장성, 자동 업데이트, 초기 설비 투자 절감 등을 배경으로, 360도 피드백 소프트웨어 시장 점유율의 69.14%를 클라우드 도입이 차지했습니다. 그러나 하이브리드 구성은 2031년까지 연평균 성장률(CAGR) 11.42%를 기록하며 성장하고 있으며, 이는 도입된 모델 중 가장 높은 성장률입니다. 연방 정부 직원의 기록을 국내에 보관하도록 의무화하는 UAE의 규제로 인해, 국내 데이터센터에서 호스팅되는 프라이빗 클라우드 노드에 대한 관심이 높아지고 있습니다. SAP의 2026년판 SuccessFactors는 실시간 AI를 위해 클라우드 인프라를 활용하는 한편, 보상 파일의 경우 고객이 관리하는 스토리지를 지원함으로써, 주요 벤더가 데이터 주권과 민첩성 사이의 균형을 어떻게 맞추고 있는지를 보여주고 있습니다.

하이브리드 아키텍처는 데이터 주권 관련 요구 사항과 클라우드 네이티브 플랫폼의 민첩성 및 AI 기능 간의 균형을 맞추어야 하는 금융 서비스, 의료, 정부 기관에 매력적인 선택지입니다. On-Premise 구축은 에어갭 네트워크나 엄격한 사이버 보안 프로토콜로 인해 클라우드 연결이 금지된 기존 제조 기업이나 방위 관련 기업에서 여전히 이어지고 있습니다. 다만, 벤더들이 고객 관리 데이터센터에 호스팅된 프라이빗 클라우드 인스턴스를 우선시하며 On-Premise 지원을 단계적으로 폐지하고 있기 때문에 이 부문은 축소 추세를 보이고 있습니다.

지역별 분석

북미는 2025년 매출의 39.28%를 차지하며, 포춘 500대 기업의 크로스 스위트 도입과 투명성이 높은 인재 관리 프로세스를 중시하는 컴플라이언스 환경에 힘입고 있습니다. 하이브리드 방식으로 전환하고 있는 연방 정부의 계약업체들은 계약 주기를 연장하고 있지만, 구매자가 자문 서비스나 보안 모듈을 추가함에 따라 평균 계약 금액은 상승하고 있습니다. 또한, 이 지역은 AI 기반 HR 도구의 조기 도입으로 인한 혜택을 누리고 있으며, 이를 통해 분석 중심의 의사결정이 강화되고 플랫폼 업그레이드가 가속화되고 있습니다. 또한, 강력한 벤더 생태계와 높은 HR 테크 투자 여력이 북미의 리더십을 더욱 공고히 하고 있습니다.

유럽에서는 매출 성장세가 둔화되고 있지만, GDPR(EU 개인정보보호규정)로 인해 공급업체 변경 비용이 증가하고 있어 계약 갱신률은 견조한 추세를 보이고 있습니다. Lattice의 데이터에 따르면, 유럽 기업의 51%가 분기별 평가를 실시하고 있으며, 지속적인 피드백 루프에 대한 수요가 정착되어 있습니다. 법적 감독이 엄격하기 때문에 구매자들은 명확한 감사 추적 기록과 자동 삭제 워크플로를 제공하는 플랫폼을 선호하며, 이러한 복잡성 덕분에 기존 공급업체들 시장 점유율이 유지되고 있습니다. 이러한 규제 환경은 공급업체와의 장기적인 관계를 촉진하고, 규정 준수를 충족하는 엔터프라이즈급 솔루션에 대한 수요를 높이고 있습니다. 또한, 다국어를 구사하는 인력에 대한 요구 사항으로 인해, 맞춤형으로 현지화된 플랫폼의 필요성이 더욱 커지고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 12.36%를 기록하며, 명백히 수요를 견인하는 주역으로 자리매김하고 있습니다. Darwinbox와 같은 인도 업체들은 노동법을 현지화하여 현지 언어로 된 인터페이스를 제공하는 반면, 중국의 국영 기업들은 국가 디지털화 프로그램의 일환으로 인사 관리의 현대화를 추진하고 있습니다. 일본과 한국에서는 상사에게 피드백을 제공하는 것에 대한 문화적 거부감이 여전히 남아 있기 때문에 각 벤더 기업들은 체면을 유지해야 한다는 규범을 훼손하지 않으면서도 사용자의 신뢰를 유지할 수 있도록, 익명성 보장 및 그룹 토론 형식에 투자하고 있습니다. 중소기업의 급속한 디지털화와 비용 효율성을 중시하는 SaaS 도입 역시 이 지역 전체에서 목표 시장을 확대되고 있습니다. 또한, 정부 주도의 디지털 전환(DX) 이니셔티브가 증가함에 따라 기업 내 체계적인 피드백 시스템의 도입이 가속화되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the 360-degree feedback software market size is expected to grow from USD 1.23 billion in 2025 to USD 1.35 billion in 2026 and is forecast to reach USD 2.16 billion by 2031 at 9.87% CAGR over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment (Cloud, On-Premises, and Hybrid), Organization Size (Small and Medium-Sized Enterprises, and Large Enterprises), Industry Vertical (IT and Telecom, BFSI, Healthcare and Lifesciences, and More), Pricing Model (Subscription-Based, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global 360-Degree Feedback Software Market Trends and Insights

AI-Driven Personalized Feedback Workflows

Generative AI now tailors question sets to individual competency gaps and rapidly converts raw multi-rater data into coaching prompts, slashing insight lead time from weeks to hours. Microsoft Viva Glint, SAP SuccessFactors, and Oracle HCM Cloud have all released agentic AI features that surface sentiment patterns and flag rating discrepancies, prompting 48% of European HR teams to pilot specialized AI performance tools in 2025. Vendors unable to embed real-time personalization or bias screening risk price erosion as buyers increasingly view those capabilities as table stakes.

Integration of 360-Degree Feedback into Continuous Performance Management Suites

Quarterly reviews are replacing annual appraisals, pushing organizations to converge feedback, goal tracking, and peer recognition into unified workflows. Workday's 2025 acquisition of Sana for USD 1.1 billion was framed as a move to weave AI-driven talent intelligence across its HCM suite, underscoring how tightly integrated analytics now shape succession planning and skill development. Stand-alone vendors, therefore, face a build-or-partner decision as cross-suite integration has become a primary buying criterion in the 360-degree feedback software market.

Concerns Over Data Privacy and Psychometric Bias

Strict statutes like GDPR and California ADMT now require transparency on algorithmic decision-making, elevating vendor compliance costs and amplifying litigation risk. A 2025 Journal of Applied Psychology article revealed that 30% of responses in large firms were skewed by rater bias, prompting buyers to demand encryption, audit logs, and statistical bias checks. Vendors lagging on these safeguards face procurement delays and potential reputational damage.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Hybrid and Remote Work Operating Models

- Rising Demand for Data-Driven Leadership Development Programs

- Change-Management Challenges in Traditional Hierarchical Cultures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software captured 78.92% of market revenue of the 360-degree feedback software market in 2025, reflecting the dominance of license and subscription fees, yet services are projected to expand at 10.96% CAGR through 2031, outpacing the overall market rate. SurveyConnect observed that 40% of HR teams in firms above 5,000 employees failed to create actionable dashboards within a month, catalyzing demand for advisory projects. As a result, vendors now bundle quarterly calibration workshops into premium tiers, blending software and services in one subscription.

The 360-degree feedback software market benefits as service partners monetize rater-training, psychometric validation, and culture-change roadmaps, especially in regulated verticals where GDPR or healthcare accreditation demands third-party attestation. Paychex's January 2025 announcement of its USD 4.1 billion acquisition of Paycor highlighted expected run-rate cost synergies exceeding USD 80 million, with substantial revenue synergy opportunities tied to cross-selling implementation and advisory services across a combined customer base of approximately 745,000 clients.

Cloud deployment commanded 69.14% of the 360-degree feedback software market share in 2025, driven by scalability, automatic updates, and lower upfront capital expenditure, yet hybrid configurations are growing at 11.42% CAGR through 2031, the fastest rate among deployment models. UAE regulations that require federal employee records to stay on national soil have spurred interest in private cloud nodes hosted in domestic data centers. SAP's 2026 SuccessFactors release leverages cloud infrastructure for real-time AI while supporting customer-controlled storage for compensation files, illustrating how large vendors balance sovereignty and agility.

Hybrid architectures appeal to financial services, healthcare, and government entities that must balance data sovereignty mandates with the agility and AI capabilities of cloud-native platforms. On-premises deployments persist in legacy manufacturing firms and defense contractors where air-gapped networks and stringent cybersecurity protocols prohibit cloud connectivity, though this segment is contracting as vendors phase out on-premises support in favor of private cloud instances hosted in customer-controlled data centers.

Geography Analysis

North America generated 39.28% of 2025 revenue, sustained by Fortune 500 cross-suite expansions and a compliance environment that rewards transparent talent processes. Federal contractors moving to hybrid deployments have lengthened deal cycles but lifted average contract value as buyers layer advisory and security modules. The region also benefits from early adoption of AI-enabled HR tools, which enhances analytics-driven decision-making and accelerates platform upgrades. Additionally, strong vendor ecosystems and high HR tech spending capacity continue to reinforce North America's leadership position.

Europe posts slower topline growth yet enjoys sticky renewal rates because GDPR heightens vendor switching costs. Lattice data show 51% of European firms run quarterly reviews, cementing demand for continuous feedback loops. High legal scrutiny means buyers favor platforms that provide clear audit trails and automated deletion workflows, adding complexity that protects incumbent penetration. This regulatory environment encourages long-term vendor relationships and increases demand for compliant, enterprise-grade solutions. Moreover, multilingual workforce requirements further drive the need for customizable and localized platforms.

Asia-Pacific is the clear volume driver with a 12.36% CAGR. Indian vendors such as Darwinbox localize labor codes and offer vernacular interfaces while Chinese state-owned enterprises modernize talent oversight under national digitalization programs. Cultural hesitancy toward upward feedback persists in Japan and South Korea, so vendors invest in anonymity guarantees and group discourse formats that sustain user confidence without violating face-saving norms. Rapid SME digitization and cost-sensitive SaaS adoption are also expanding the addressable market across the region. In addition, increasing government-led digital transformation initiatives are accelerating enterprise adoption of structured feedback systems.

- Culture Amp Pty Ltd

- Qualtrics LLC

- Momentive Global Inc.

- Cornerstone OnDemand Inc.

- Workday Inc.

- Inspire Software Inc.

- Leapsome GmbH

- EchoSpan Inc.

- Spidergap Ltd

- Trakstar Inc.

- Reflektive Inc.

- SurveySparrow Inc.

- EngageRocket Pte. Ltd.

- Betterworks Systems Inc.

- PeopleGoal Ltd.

- 15Five Inc.

- AssessTEAM LLC

- ClearCompany Inc.

- Synergita Software Pvt. Ltd.

- Reviewsnap, LLC

- OrangeHRM Inc.

- PeopleFluent Holdings Corp.

- Lattice HR Inc.

- Saba Software Inc.

- BambooHR LLC

- Zoho Corporation Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Driven Personalised Feedback Workflows

- 4.2.2 Integration of 360-Degree Feedback into Continuous Performance Management Suites

- 4.2.3 Expansion of Hybrid and Remote-Work Operating Models

- 4.2.4 Rising Demand for Data-Driven Leadership Development Programs

- 4.2.5 Growing Adoption Across Emerging-Market SMBs Via Freemium GTM Strategies

- 4.2.6 Increasing Regulatory Emphasis on Objective Employee Evaluations

- 4.3 Market Restraints

- 4.3.1 Concerns Over Data Privacy and Psychometric Bias

- 4.3.2 Change-Management Challenges in Traditional Hierarchical Cultures

- 4.3.3 Limited HR Tech Budgets in Micro-enterprises

- 4.3.4 Interoperability Gaps with Legacy HCM/ERP Stacks

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Small and Medium-sized Enterprises

- 5.3.2 Large Enterprises

- 5.4 By Industry Vertical

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Lifesciences

- 5.4.4 Retail and E-commerce

- 5.4.5 Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other Industry Verticals

- 5.5 By Pricing Model

- 5.5.1 Subscription-Based

- 5.5.2 Perpetual / One-Time License

- 5.5.3 Usage-Based / Pay-Per-Use

- 5.5.4 Freemium

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Egypt

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Culture Amp Pty Ltd

- 6.4.2 Qualtrics LLC

- 6.4.3 Momentive Global Inc.

- 6.4.4 Cornerstone OnDemand Inc.

- 6.4.5 Workday Inc.

- 6.4.6 Inspire Software Inc.

- 6.4.7 Leapsome GmbH

- 6.4.8 EchoSpan Inc.

- 6.4.9 Spidergap Ltd

- 6.4.10 Trakstar Inc.

- 6.4.11 Reflektive Inc.

- 6.4.12 SurveySparrow Inc.

- 6.4.13 EngageRocket Pte. Ltd.

- 6.4.14 Betterworks Systems Inc.

- 6.4.15 PeopleGoal Ltd.

- 6.4.16 15Five Inc.

- 6.4.17 AssessTEAM LLC

- 6.4.18 ClearCompany Inc.

- 6.4.19 Synergita Software Pvt. Ltd.

- 6.4.20 Reviewsnap, LLC

- 6.4.21 OrangeHRM Inc.

- 6.4.22 PeopleFluent Holdings Corp.

- 6.4.23 Lattice HR Inc.

- 6.4.24 Saba Software Inc.

- 6.4.25 BambooHR LLC

- 6.4.26 Zoho Corporation Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment