|

시장보고서

상품코드

2064374

직원 웰빙 플랫폼 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Employee Wellbeing Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

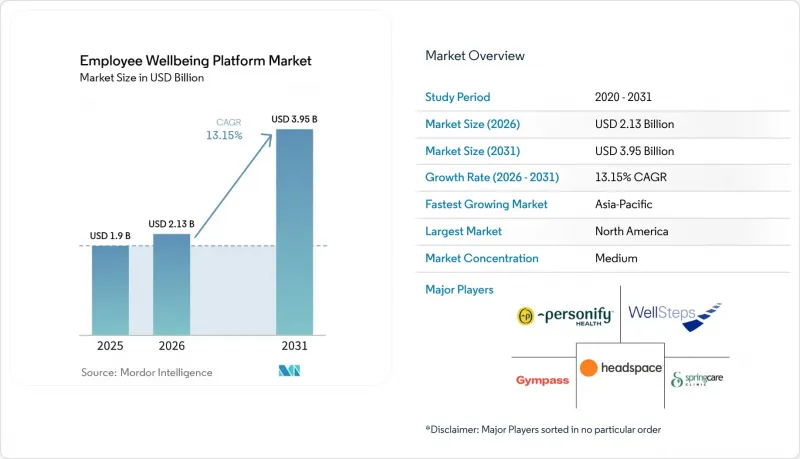

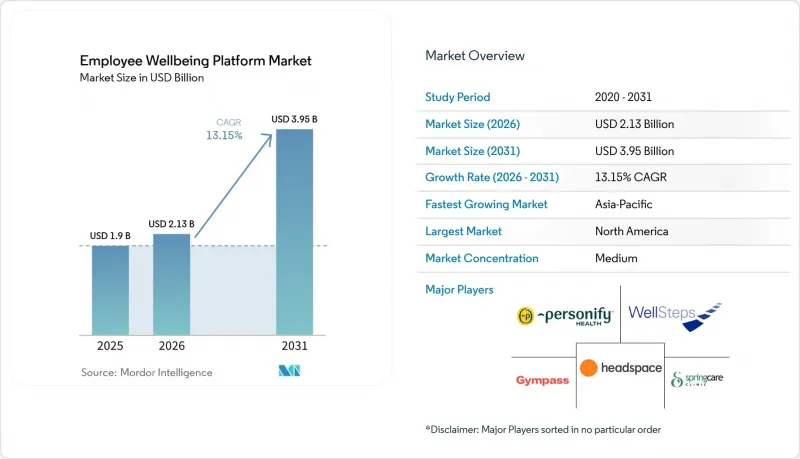

Mordor Intelligence에 의하면, 직원 웰빙 플랫폼 시장 규모는 2025년에 19억 달러로 평가되었고, 2026년에 21억 3,000만 달러로 추정되며, 2031년까지 39억 5,000만 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 13.15%로 성장할 것으로 전망됩니다.

본 보고서는 웰빙 모듈별(건강 위험 평가 및 스크리닝 등), 배포 방식별(클라우드 기반, 온프레미스), 기업 규모별(대기업 및 중소기업), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), 의료 및 생명과학, 소매업 및 전자상거래 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 직원 웰빙 플랫폼 시장 동향 및 고찰

지식 근로자 및 현장 업무 종사자의 직장 스트레스와 번아웃 증가

스트레스 증가는 직원 웰빙 플랫폼 시장에서 여전히 가장 강력한 단기 성장 요인으로 자리 잡고 있습니다. 이는 고용주가 근로 조건과 관련된 건강 피해의 실태를 그 어느 때보다 명확하게 인식하게 되었기 때문입니다. 2026년 4월 보고서에 따르면, 매년 84만 명 이상의 사망이 직장의 심리사회적 위험과 관련되어 있으며, 이에 따른 경제적 손실은 전 세계 GDP의 1.37%에 달할 전망입니다. 2026년 1월 조사에 따르면, 영국 성인의 91%가 전년도에 높은 수준 또는 극심한 스트레스를 경험했으며, 근로자의 35%는 여전히 직속 상사에게 스트레스를 털어놓는 데 거부감을 느끼고 있어, 이는 사적인 디지털 채널의 필요성을 뒷받침해 줍니다. 또한, 전 세계 데이터를 통해 고용주가 지출 결정 시 정신 건강을 핵심 요소로 삼는 이유도 밝혀졌습니다. 우울증과 불안 장애로 인해 매년 120억 노동일 분의 손실이 발생하며, 이는 1조 달러의 생산성 손실로 이어지기 때문입니다. 직원 웰빙 플랫폼 시장이 확대되고 있는 이유는 구매자들이 번아웃을 더 이상 추상적인 문화적 문제로만 보지 않고, 위험 요소를 파악하며, 직원들을 돌봄으로 이끌고, 프로그램 활용을 비즈니스 성과로 연결할 수 있는 도구를 점점 더 많이 찾고 있기 때문입니다.

의료비 청구, 결근, 프레젠티즘 비용 절감을 원하는 고용주들의 요구

직원 웰빙 플랫폼 시장은 직장에서의 건강 상태 악화에 따른 숨겨진 비용을 보다 직접적으로 파악하려는 고용주들의 지지도 얻고 있습니다. 2025년 조사에 따르면, 미국 고용주가 부담하는 번아웃으로 인한 비용은 직원 1인당 연간 3,999달러에서 2만 683달러로 추정되며, 그 부담의 89%는 결근이 아닌 프레젠티즘(출근은 했지만 생산성이 저하된 상태)에서 비롯된 것으로 나타났습니다. 이러한 비용 구성이 중요한 이유는 플랫폼의 평가 기준이 복리후생 이용률에서 돌봄 서비스 이용 현황, 생산성, 단기 장애 경향에 대한 측정 가능한 변화로 전환되고 있기 때문입니다. 따라서 고용주들은 플랫폼이 보험금 청구 부담을 줄이고 생산성 저하를 억제하는 데 도움이 된다는 증거를 요구하고 있으며, 컨텐츠 라이브러리나 기본적인 웰니스 프로그램 및 과제만 제공하는 업체의 경우 시장 진입 장벽이 높아지고 있습니다. 실제로, 직원 웰빙 플랫폼 시장에서 우위를 점하고 있는 공급업체는 직원 참여도를 검증 가능한 가치로 전환할 수 있는 기업입니다. 왜냐하면 구매자는 계약 갱신 주기나 비용 재검토 시에도 통용될 수 있는 재무 부서가 납득할 만한 실적을 원하기 때문입니다.

지속적인 직원 참여도 저하와 ROI 입증 간의 격차

직원 웰빙 플랫폼 시장에서 가장 큰 상업적 제약 요인은 여전히 플랫폼의 이용 가능성과 직원들의 정기적인 이용 사이의 격차에 있습니다. 2025년 하반기에는 고용주의 지출이 계속 증가했음에도 불구하고, 자사의 웰니스 프로그램을 ‘좋다’고 평가한 직원은 29%에 그쳐, 2022년의 41%에서 감소했습니다. 또한, 2026년 3월에는 기존의 직원 지원 모델의 경우 이용률이 보통 5%에서 10%에 그쳤으며, 많은 새로운 플랫폼에서도 월간 참여율을 30% 이상 유지하는 데 여전히 어려움을 겪고 있다는 점이 지적되었습니다. 이 상한선은 갱신 시의 사업 타당성을 약화시킵니다. 왜냐하면 이용률이 낮으면 보험금 청구 감축이나 생산성 향상을 설득력 있게 입증하기 어려워지기 때문입니다. 참여도와 재무적 성과를 연결 짓지 못하는 공급업체는 고용주가 지출을 억제할 때 예산의 재량적 배분에 관한 논의로 되돌아갈 가능성이 높아집니다. 이 문제는 직원 웰빙 플랫폼 시장의 성장을 둔화시킬 것입니다. 왜냐하면 성장은 도입률뿐만 아니라, 고용주가 직원들이 서비스 시작 후에도 계속 이용할 것이라고 믿는지 여부에 달려 있기 때문입니다.

부문별 분석

2025년, 정신 건강 및 스트레스 관리는 직원 웰빙 플랫폼 시장의 26.41%를 차지했으며 가장 큰 모듈이 되었습니다. 이는 고용주들이 치료받지 않은 정신 건강 문제와 노동 생산성 저하 사이에 직접적인 연관성이 있다고 보고 있기 때문입니다. 이 견해는 다른 많은 모듈보다 더 확실한 근거에 의해 뒷받침되고 있습니다. 2024년 보고서에 따르면, 우울증과 불안 장애는 매년 120억 노동일의 손실과 1조 달러의 생산성 손실을 초래하고 있으며, 이것이 고용주들이 이 분야를 지속적으로 우선시하는 이유를 설명해 줍니다. 직원 웰빙 플랫폼 시장에서 이 모듈은 임상적으로 지도되는 치료, 코칭, 디지털 트리아지로 이어지는 명확한 경로를 제공하며, 구매자가 성과 측면에서 지출을 정당화하기 쉽다는 장점도 있습니다.

‘금융 웰빙’은 가장 빠르게 성장하고 있는 분야로, 2026-2031년 연평균 성장률(CAGR) 15.92%를 기록하며 확대될 것으로 전망됩니다. 이는 직원의 경제적 부담이 실적, 이직률, 복리후생 이용에 점점 더 큰 영향을 미치고 있기 때문입니다. 고용주들은 특히 부채 부담, 인플레이션에 대한 민감성, 의료비 본인 부담에 대한 우려가 직원들에게 무겁게 짓누르고 있는 상황에서 신체 활동이나 영양 관리를 넘어서는 지원 범위를 확대되고 있습니다. 이러한 변화로 인해 공급업체들은 정신 건강 및 신체 건강 서비스 외에도 가계 관리 지원, 부채 관련 상담, 복리후생 활용 지원 등을 제공해야 하는 상황에 놓여 있습니다. 피트니스 및 신체 활동, 영양·체중 관리, 건강 위험 평가 모듈 역시 여전히 중요하지만, 만성 질환 관리 및 약물 복용 지원과 연계된 복리후생 프로그램과의 경쟁에 직면해 있습니다. 수면의 건강과 사회적 유대감을 다루는 다른 모듈들도 주목을 받고 있습니다. 이는 직원 웰빙 플랫폼 업계가 단순히 업무 부담에만 초점을 맞추는 것이 아니라, 회복, 고립, 일상적인 스트레스 노출 등을 포함하는 번아웃에 대한 보다 종합적인 관점으로 전환하고 있기 때문입니다.

2025년 기준으로 클라우드 기반 솔루션의 도입 비중은 직원 웰빙 플랫폼 시장의 71.23%를 차지했으며, 이러한 우위는 노동력의 분포와 서비스형 소프트웨어(SaaS)가 제공하는 실질적인 이점을 모두 반영하고 있습니다. 고용주가 클라우드 서비스를 선호하는 이유는 업데이트 관리가 용이하고, 지점 간 사용자 액세스 확장이 간편하며, 고도로 맞춤화된 온프레미스 환경에 비해 인사 시스템과의 통합이 더 간단하기 때문입니다. 이 모델은 신속한 도입, 사내 IT 부서의 부담 경감, 그리고 사무실이나 원격 환경을 불문하고 직원들이 보다 일관되게 접근할 수 있다는 점에서 현재의 구매 경향에도 부합합니다. 직원 웰빙 플랫폼 시장에서 클라우드 도입은 각 지역에 온프레미스 인프라를 구축하지 않고도 광범위한 서비스 범위를 원하는 조직에게 표준이 되고 있습니다.

온프레미스 배포는 데이터 취급 규정이 더욱 엄격하고 내부 통제가 여전히 필수 요건으로 남아 있는 정부 기관, 국방 분야, 규제 대상 금융 서비스의 일부 분야에서 여전히 그 역할을 수행하고 있습니다. 그럼에도 불구하고 하이브리드 아키텍처는 가장 역동적인 아키텍처로 부상하고 있으며, 다국적 기업들이 도달 범위 확대와 기밀 데이터에 대한 보다 엄격한 관리를 동시에 추구하는 가운데, 2031년까지 연평균 성장률(CAGR) 14.38%를 기록하며 성장할 것으로 전망됩니다. 하이브리드 구성을 통해 공급업체는 직원을 위한 경험을 단순하게 유지하면서도, 특정 기록이 어디에서 처리되거나 저장될지에 대해 구매자에게 더 많은 결정권을 부여할 수 있습니다. 이러한 균형은 데이터 주권 및 직원의 데이터 권리가 선정 후 법적 심사의 대상이 될 뿐만 아니라, 구매 시 협의 사항의 일부로 포함되는 유럽에서 중요합니다. 그 결과, 직원 웰빙 플랫폼 업계는 여전히 클라우드 제공을 기반으로 하고 있지만, 성장은 국경을 초월한 위험을 완화하고 내부 승인 주기를 단축하는 아키텍처에서 점점 더 많이 비롯되고 있으며, 도입 형태는 더욱 다층적으로 변하고 있습니다.

지역별 분석

북미는 2025년에 직원 웰빙 플랫폼 시장 점유율의 37.92%를 차지했으며, 최대 지역 시장이 되었습니다. 이는 해당 지역 전체에서 고용주가 제공하는 의료보험과 인건비 관리가 밀접하게 연관되어 있기 때문입니다. 미국은 여전히 핵심 시장이며, 미국 소비자들은 의료비 부담, 정신 건강 서비스 이용 편의성, 일상적인 생산성 지원이라는 측면에서 가치를 입증할 수 있는 플랫폼을 선호하는 경향이 있습니다. 이러한 추세에 따라 공급업체들은 기존의 웰니스 컨텐츠에 그치지 않고, 케어 내비게이션, 만성 질환 지원, 복리후생 워크플로우와의 보다 직접적인 통합 등을 포함하도록 서비스 제공 범위를 확대해야 하는 상황에 직면해 있습니다. 캐나다 역시 직원 웰빙 플랫폼 시장에서 중요한 위치를 차지하고 있습니다. 이는 피보험자 수와 의료 서비스 제공업체의 서비스 범위를 확대하는 인수를 통해 시장 규모가 커지고 있기 때문입니다. 2025년 5월, 5억 캐나다 달러(부채 충당금 공제 후 순액 기준 3억 5,000만 달러) 규모의 인수가 이루어진 것은 인수 측이 보다 광범위한 서비스의 깊이와 다국적 기업에 대한 지원을 요구하는 가운데, 지역적 규모의 중요성이 점점 더 커지고 있음을 보여줍니다.

멕시코에서는 고용주들이 심리사회적 위험에 관한 법적 의무를 이행함에 따라 규정 준수 중심의 단계로 전환되고 있으며, 이로 인해 초대형 기업 외에도 현지 구매자층이 확대되고 있습니다. 이 점은 중요합니다. 왜냐하면 이 지역의 동향은 더 이상 미국의 대기업이나 다국적 기업의 본사에 국한되지 않고, 보다 손쉬운 도입과 현지화된 지원을 필요로 하는 중견 기업들도 점점 더 많이 포함되고 있기 때문입니다. 따라서 북미의 직원 웰빙 플랫폼 시장은 성숙한 기업 수요와 규제 및 노동력 안정화와 연계된 새로운 도입 경로가 결합된 형태를 띠고 있습니다. 아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 2026년부터 2031년까지 연평균 성장률(CAGR) 16.73%로 확대될 것으로 예상되며, 많은 공급업체에게 가장 중요한 성장 동력이 되고 있습니다. 인도의 성장은 공식적인 규정 준수 변경은 물론, 예방 의료, 긱 워커에 대한 지원, 디지털 서비스 제공에 대한 고용주의 관심에 힘입고 있지만, 제품의 심도나 ROI 측정과 관련해서는 구매자마다 여전히 차이가 나타나고 있습니다.

아시아태평양 전체의 상황은 사무직 근로자와 현장 근로자 모두에게 뿌리 깊게 존재하는 번아웃 위험에 힘입어, 동남아시아, 일본, 한국, 호주, 뉴질랜드에서 수요가 높은 수준을 유지하고 있습니다. 2026년 3월, 호주에서 잇달아 발생한 인수 사례는 벤더들이 이 지역을 통합이나 플랫폼 규모 확대를 정당화할 수 있을 만큼 충분한 시장 규모를 갖춘 곳으로 보고 있음을 보여줍니다. 한편, 유럽은 규제가 더 엄격한 수요 환경에 놓여 있어, 데이터 처리, 직원과의 협의, GDPR(EU 개인정보보호규정) 준수 등의 요건이 제품의 다양성과 마찬가지로 공급업체 선정의 중요한 요소로 작용하고 있습니다. 이로 인해 지역별 데이터 처리, 공식적인 개인정보 보호 문서, 그리고 현지 상황에 더 부합하는 도입 모델을 제공할 수 있는 공급업체에게 실질적인 시장 진입 기회가 생겨나고 있습니다. 유럽 이외의 지역에서는 웰빙 도구가 광범위한 인재 개발 의제의 일부로 자리 잡으면서 중동의 중요성이 커지고 있습니다. 한편, 아프리카에서는 도입이 아직 초기 단계에 머물러 있어, 직원 웰빙 플랫폼 시장의 초기 수요층을 구축하기 위해 보험사, 다국적 기업 및 디지털 직원 지원 서비스에 대한 의존도가 높아지고 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the employee wellbeing platform market size is projected to be USD 1.90 billion in 2025, USD 2.13 billion in 2026, and reach USD 3.95 billion by 2031, growing at a CAGR of 13.15% from 2026 to 2031.

This report is Segmented by Wellbeing Module (Health Risk Assessment and Screening, and More), Deployment Model (Cloud-Based and On-Premises), Enterprise Size (Large Enterprises and Small and Medium-Sized Enterprises), End-User Industry Vertical (BFSI, Healthcare and Life Sciences, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Employee Wellbeing Platform Market Trends and Insights

Rising Workplace Stress And Burnout Across Knowledge And Frontline Roles

Rising stress remains the strongest near-term growth driver in the employee wellbeing platform market, as employers now face a much clearer record of harm tied to work conditions. In April 2026, it was reported that more than 840,000 deaths each year were linked to psychosocial workplace risks, with annual economic losses equal to 1.37% of global GDP. In January 2026, surveys showed that 91% of UK adults experienced high or extreme stress in the previous year, and 35% of workers remained uncomfortable disclosing their stress to line managers, which strengthens the case for private digital pathways. Global data has also shown why employers place mental health near the center of spending decisions, since depression and anxiety cause 12 billion lost working days each year and result in USD 1 trillion in lost productivity. The employee well-being platform market is benefiting because buyers no longer see burnout as an abstract cultural issue and increasingly want tools that can identify risk, guide members into care, and connect program use with business outcomes.

Employer Demand To Reduce Healthcare Claims, Absenteeism, And Presenteeism Costs

The employee well-being platform market is also gaining support from employers seeking a more direct handle on the hidden costs of poor health at work. A 2025 study estimated burnout costs to U.S. employers at USD 3,999 to USD 20,683 per worker each year, and 89% of that burden came from presenteeism rather than absence. That cost mix matters because it shifts platform evaluation away from benefit participation and toward measurable change in care use, productivity, and short-term disability patterns. Employers are therefore asking for proof that a platform can help lower claims pressure and reduce lost output, which is raising the bar for vendors that only offer content libraries or basic wellness challenges. In practice, the stronger vendors in the employee wellbeing platform market are those that can translate engagement into auditable value, since buyers want a finance-ready case that holds up during renewal cycles and cost reviews.

Low Sustained Employee Engagement And ROI Proof Gaps

The largest commercial restraint in the employee well-being platform market remains the gap between platform availability and regular employee use. In late 2025, only 29% of employees rated their company's wellness programs as good, down from 41% in 2022, even though employer spending continued to rise. In March 2026, it was also noted that older employee assistance models typically achieved only 5% to 10% utilization, and many newer platforms still struggle to maintain monthly engagement above 30%. That ceiling weakens the business case at renewal because low usage makes it harder to credibly demonstrate reductions in claims or improvements in productivity. Vendors that cannot connect engagement with finance-grade outcomes are more likely to fall back into discretionary budget discussions when employers tighten spending. This issue slows the employee wellbeing platform market because growth depends not only on adoption, but also on whether employers believe employees will keep using the service after launch.

Other drivers and restraints analyzed in the detailed report include:

- Hybrid And Distributed Work Models Favoring Digital-First Wellbeing Delivery

- AI, Analytics, And Wearables Enabling Personalized Interventions And Measurable Outcomes

- Sensitive Workforce Health Data Privacy And Cybersecurity Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mental health and stress management accounted for 26.41% of the employee wellbeing platform market in 2025, making it the largest module, as employers see a direct connection between untreated mental health issues and lost work output. A stronger evidence base than many other modules supports that position. In 2024, it was reported that depression and anxiety lead to 12 billion lost working days every year and cost USD 1 trillion in productivity, which helps explain why employers keep prioritizing this part of the offer. In the employee wellbeing platform market, this module also benefits from a clearer pathway to clinically guided therapy, coaching, and digital triage, making it easier for buyers to justify spend in terms of outcomes.

Financial well-being is the fastest-growing module and is projected to expand at a 15.92% CAGR from 2026 to 2031, because employee financial strain increasingly affects performance, retention, and benefit use. Employers are broadening the scope of support beyond physical activity and nutrition, especially where debt pressure, inflation sensitivity, and out-of-pocket healthcare concerns weigh on the workforce. This change is pushing vendors to offer budgeting support, debt guidance, and benefit navigation alongside mental and physical health services. Fitness and physical activity, nutrition and weight management, and health risk assessment modules still matter, but they face more competition from benefit programs tied to chronic condition management and medication support. Other modules, including sleep health and social connection, are also gaining attention as the employee wellbeing platform industry moves toward a fuller view of burnout that includes recovery, isolation, and daily stress exposure, rather than focusing solely on workload.

Cloud-based deployment held 71.23% of the employee wellbeing platform market share in 2025, and that lead reflects both workforce distribution and the practical advantages of software delivered as a service. Employers prefer cloud delivery because updates are easier to manage, user access is simpler to extend across locations, and integration with HR systems is more straightforward than in heavily customized local environments. This model also aligns with current buying patterns of faster rollouts, lighter internal IT lift, and more consistent employee access across offices and remote settings. In the employee wellbeing platform market, cloud deployment has become the standard for organizations seeking broad coverage without building local infrastructure in each geography.

On-premises deployment still has a place in parts of government, defense, and regulated financial services where data-handling rules are stricter and internal controls remain a hard requirement. Even so, hybrid deployment is emerging as the most dynamic architecture and is projected to grow at a 14.38% CAGR through 2031, as multinational employers seek both reach and tighter control over sensitive data. Hybrid configurations let vendors keep the employee-facing experience simple while giving buyers more say over where certain records are processed or stored. That balance matters in Europe, where data sovereignty and employee data rights have become part of the buying conversation, not just an issue for legal review after selection. The result is a more layered deployment picture in which the employee wellbeing platform industry still runs on cloud delivery, but growth increasingly comes from architectures that reduce cross-border risk and shorten internal approval cycles.

Geography Analysis

North America held 37.92% of the employee wellbeing platform market share in 2025, making it the largest regional market, as employer-sponsored healthcare and workforce cost management are closely linked across the region. The United States remains the anchor market, and its buyer behavior favors platforms that can show value in terms of medical cost pressure, mental health access, and daily productivity support. That pattern has pushed vendors to broaden their offerings beyond classic wellness content to include care navigation, chronic condition support, and more direct integration with benefits workflows. Canada is also important to the employee wellbeing platform market because scale is rising through acquisitions that expand covered lives and provider reach. In May 2025, a CAD 500 million acquisition (USD 350 million net of assumed debt) showed that regional scale is becoming increasingly important as buyers seek broader service depth and multinational support.

Mexico is moving into a more compliance-driven phase as employers respond to psychosocial risk obligations, which is widening the local buyer pool beyond very large organizations. This matters because the regional story is no longer limited to large U.S. employers and multinational headquarters, and it increasingly includes medium-sized employers that need easier deployment and localized support. The employee well-being platform market in North America, therefore, combines mature enterprise demand with newer adoption paths tied to regulation and workforce stabilization. Asia-Pacific is the fastest-growing region, projected to expand at a 16.73% CAGR from 2026 to 2031, making it the most important growth corridor for many vendors. Growth in India is being supported by formal compliance changes and by employer interest in preventive health, gig worker support, and digital service delivery, even though product depth and ROI measurement remain uneven across buyers.

The broader Asia-Pacific picture is strengthened by persistent burnout exposure across both office and frontline workforces, which keeps demand elevated across Southeast Asia, Japan, South Korea, Australia, and New Zealand. In March 2026, multiple acquisitions in Australia showed that vendors see the region as large enough to justify consolidation and platform scale-building. Europe presents a more regulated demand environment, where data handling, employee consultation, and GDPR expectations shape vendor selection as much as product breadth. That creates a practical opening for providers that can offer regional data processing, formal privacy documentation, and a more localized deployment model. Outside Europe, the Middle East is gaining relevance as well-being tools become part of broader workforce development agendas, while Africa remains earlier in adoption and depends more heavily on insurers, multinationals, and digital employee assistance services to build the first layer of demand in the employee well-being platform market.

- Personify Health, Inc.

- Wellable LLC

- Gympass US, LLC

- Modern Life, Inc.

- Spring Care, Inc.

- Lyra Health, Inc.

- Headspace Inc.

- Unmind Ltd

- Kyan Health AG

- WellSteps, LLC

- yuMuuv OU

- Burnalong, Inc.

- WellRight, Inc.

- ADURO, Inc.

- MediKeeper, Inc.

- CoreHealth Technologies Inc.

- BetterUp, Inc.

- OpenUp B.V.

- With Juno Ltd

- Thrive Global Holdings, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Workplace Stress and Burnout Across Knowledge and Frontline Roles

- 4.2.2 Employer Demand to Reduce Healthcare Claims, Absenteeism, and Presenteeism Costs

- 4.2.3 Hybrid and Distributed Work Models Favoring Digital-First Wellbeing Delivery

- 4.2.4 AI, Analytics, and Wearables Enabling Personalized Interventions and Measurable Outcomes

- 4.2.5 Psychosocial Risk Governance Turning Wellbeing Metrics Into Procurement Criteria

- 4.2.6 GLP-1 and Chronic Condition Benefit Management Expanding Platform Scope

- 4.3 Market Restraints

- 4.3.1 Low Sustained Employee Engagement and ROI Proof Gaps

- 4.3.2 Sensitive Workforce Health Data Privacy and Cybersecurity Concerns

- 4.3.3 Works Council Reviews and Data Localization Slowing Multicountry Rollouts

- 4.3.4 HCM Suite Bundling and AI Feature Copycats Compressing Standalone Platform Budgets

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS, VALUE (USD)

- 5.1 By Wellbeing Module

- 5.1.1 Health Risk Assessment and Screening

- 5.1.2 Mental Health and Stress Management

- 5.1.3 Fitness and Physical Activity

- 5.1.4 Nutrition and Weight Management

- 5.1.5 Financial Wellbeing

- 5.1.6 Other Wellbeing Modules

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End User Industry Vertical

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Retail and E-commerce

- 5.4.4 Industrial Manufacturing

- 5.4.5 Government and Public Sector

- 5.4.6 Education

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia and New Zealand

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Personify Health, Inc.

- 6.4.2 Wellable LLC

- 6.4.3 Gympass US, LLC

- 6.4.4 Modern Life, Inc.

- 6.4.5 Spring Care, Inc.

- 6.4.6 Lyra Health, Inc.

- 6.4.7 Headspace Inc.

- 6.4.8 Unmind Ltd

- 6.4.9 Kyan Health AG

- 6.4.10 WellSteps, LLC

- 6.4.11 yuMuuv OU

- 6.4.12 Burnalong, Inc.

- 6.4.13 WellRight, Inc.

- 6.4.14 ADURO, Inc.

- 6.4.15 MediKeeper, Inc.

- 6.4.16 CoreHealth Technologies Inc.

- 6.4.17 BetterUp, Inc.

- 6.4.18 OpenUp B.V.

- 6.4.19 With Juno Ltd

- 6.4.20 Thrive Global Holdings, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment