|

시장보고서

상품코드

2065430

아시아태평양의 복리후생 기술 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Asia-Pacific Benefits Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

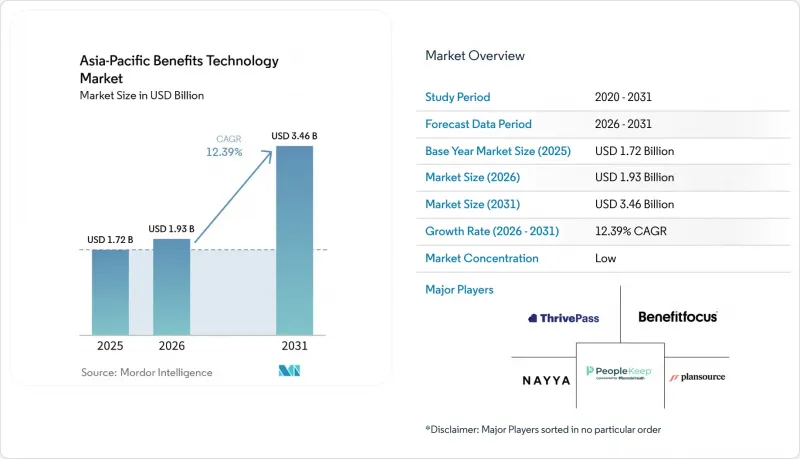

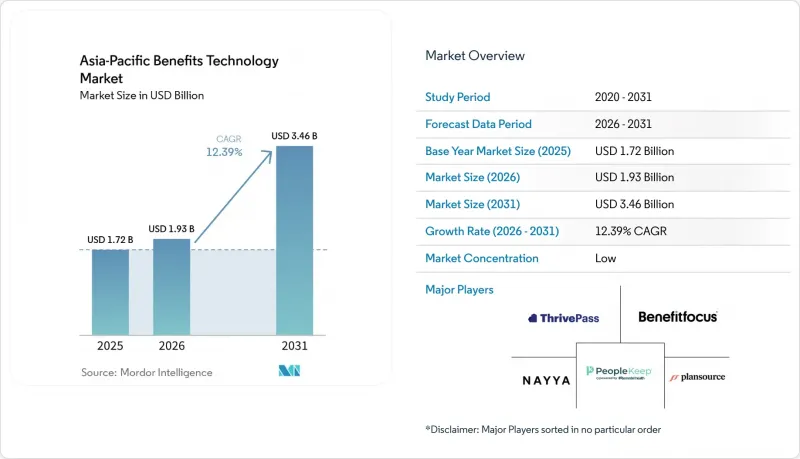

Mordor Intelligence에 의하면, 아시아태평양의 복리후생 기술 시장 규모는 2025년 17억 2,000만 달러로 평가되었습니다. 2026년에는 19억 3,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 12.39%로 성장을 지속하여, 2031년에는 34억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어, 서비스), 용도(복리후생 관리 등), 도입 형태(클라우드, On-Premise, 하이브리드), 조직 규모(대기업, 중소기업), 최종 사용자 산업(BFSI 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 복리후생 기술 시장 동향 및 인사이트

클라우드 기반 인사·복리후생 시스템의 현대화

아시아태평양의 복리후생 기술 시장에서 많은 고용주들에게 클라우드 전환은 장기적인 계획에서 업무상의 필요성으로 변화하고 있습니다. 고용주는 인사(HR), 급여 계산, 복리후생 등의 각 기능을 반복적으로 맞춤 설정할 필요 없이, 여러 국가에 걸친 조직 구조를 지원할 수 있는 통합 시스템으로 전환하려고 하고 있습니다. 이러한 변화가 중요한 이유는 클라우드 플랫폼을 통해 복리후생 담당 팀이 서로 다른 시장에 걸친 이용 패턴, 플랜 가입 현황 및 관리상의 예외 사항을 통합적으로 파악할 수 있게 되기 때문입니다. 또한, 아시아태평양의 복리후생 기술 시장은 기존의 HR 소프트웨어 라이프사이클보다 훨씬 빠르게 진화하고 있습니다. 이는 모바일 중심의 많은 직원들이 복리후생 서비스를 부차적인 데스크톱 옵션이 아닌 주요 채널로서 디지털 방식으로 이용하고 있기 때문입니다. 이를 명확히 보여주는 사례로, 스미토모 금속광산이 Works Human Intelligence사의 통합 플랫폼 ‘COMPANY’를 도입하여, 분산되어 있던 기존 체제를 대체하고 약 7,000명의 그룹 직원을 단일 HR 기반으로 통합한 것을 들 수 있습니다.

가입 절차·규정 준수·급여 계산 연동 자동화

아시아태평양의 복리후생 기술 시장에서 자동화는 주요 성장 동력으로 자리 잡고 있습니다. 이는 해당 지역 내에서 법규가 크게 다르며, 변경 시기도 각기 다르기 때문입니다. 고용주는 가입 절차, 수급 자격 판정, 급여 계산 및 보고를 하나의 연계된 프로세스로 처리해야 하는 경우가 많지만, 여전히 많은 기업이 이러한 업무를 서로 연계되지 않은 시스템이나 수작업에 의한 인계를 통해 수행하고 있습니다. 임금 상한선, 기여금 규정 및 현지 신고 요건이 국가마다 다르며, 연중 다른 시기에 갱신되는 경우, 이러한 운영 모델은 어려워집니다. 따라서 아시아태평양의 복리후생 기술 시장에서는 대조 작업을 사내 팀에 맡기는 대신, 현지 법규를 제품에 반영한 플랫폼에 대한 수요가 증가하고 있습니다. Ramco Systems사는 고용주들이 수작업량을 줄이고 급여 계산 및 복리후생 업무 흐름을 연계하려는 가운데, 다국적 급여 계산 업무와 AI를 활용한 검증의 중요성이 커질 것이라고 지적했습니다. 기업들이 컴플라이언스 분야의 자동화와 효율화를 점점 더 우선시함에 따라, 이 시장은 앞으로도 계속 발전할 것으로 예측됩니다.

건강 및 급여 데이터와 관련된 데이터 개인정보 보호 및 사이버 보안 위험

데이터 개인정보 보호는 아시아태평양의 복리후생 기술 시장에 큰 걸림돌이 되고 있습니다. 이는 건강 및 급여 데이터가 고용주, 보험사, 급여 계산 업체 간에 공유되는 경우가 많은 시스템을 거치기 때문입니다. 이 지역에는 통일된 개인정보 보호 체계가 존재하지 않기 때문에 공급업체는 데이터 처리, 저장, 통지 및 전송 관행을 국가별로 조정해야 합니다. 따라서 플랫폼이 국경을 넘어 확장되기 위해서는 암호화, 접근 제어, 데이터 저장소 설계, 감사 대응 체계 등 제품에 대한 최소 기준이 강화되고 있습니다. 소규모 SaaS 공급업체의 경우, 매출이 지역 규모에 도달하기 전에 현지화 및 보안에 대한 투자가 증가하기 때문에 더 험난한 여정이 됩니다. 다국적 기업의 경우, 개인정보 보호 관련 심사가 계약 조건과 마찬가지로 아키텍처 결정에도 영향을 미치게 되면서 구매 주기가 길어지고 있습니다.

부문별 분석

2025년 아시아태평양의 복리후생 기술 시장에서 소프트웨어가 62.45%의 점유율을 차지했으며, 이 지역에서는 여전히 플랫폼 라이선스가 최대 수익원으로 자리 잡고 있는 것으로 나타났습니다. 이러한 주도적 지위는 가입 절차, 규정 준수 관리, 직원의 접근 권한, 급여 시스템과의 연동 측면에서 소프트웨어 주도형 제공 모델이 수행하는 중요한 역할을 반영하고 있습니다. 동시에, 고객들이 장기간에 걸친 사내 프로젝트 없이도 도입 및 현지화가 가능한 플랫폼을 점점 더 요구함에 따라 시장의 중심이 변화하고 있습니다. 현재 아시아태평양의 복리후생 기술 시장에서는 소프트웨어는 물론, 다국어, 다통화 및 각국의 법 제도를 아우르는 심도 있는 도입 역량을 갖춘 공급업체가 높이 평가받고 있습니다.

서비스 분야는 2031년까지 연평균 성장률(CAGR) 15.02%로 확대될 것으로 예측되며, 소프트웨어 분야를 웃도는 속도로 성장할 전망입니다. 이는 도입, 통합, 자문 및 지원 업무의 가치가 현재 높아지고 있음을 뒷받침합니다. 이러한 변화는 소프트웨어 수요의 부진을 반영한 것이 아니라, 많은 고용주들이 이미 다양한 제품 옵션을 보유하고 있음에도 불구하고 여러 국가에 걸친 실행에 어려움을 겪고 있다는 사실을 반영한 것입니다. 따라서, 특히 급여 계산이나 복리후생 데이터를 서로 다른 시스템 간에 대조해야 하는 경우, 도입 및 통합 서비스가 아시아태평양의 복리후생 기술 업계의 주요 수요 동력이 되고 있습니다. 법규제의 지역적 변경으로 인해 고용주는 기존의 연계 체계를 그대로 유지할 수 없게 되었고, 급여 및 복리후생 체계를 갱신할 수밖에 없게 되었기 때문에 그 필요성은 더욱 시급해졌습니다. Ramco Systems의 다국적 급여 계산 및 AI 기반 검증에 대한 노력은 강력한 통합 능력이 없다면 제품만으로는 불충분하다는 이러한 광범위한 서비스 수요를 반영하고 있습니다.

2025년, 아시아태평양의 복리후생 기술 시장에서 복리후생 관리는 28.16%를 차지하며 가장 큰 용도 부문이 되었습니다. 이러한 위치는 타당합니다. 왜냐하면 가입 절차, 수급 자격 확인, 보험사 및 서비스 제공업체와의 연계는 여전히 모든 고용주가 이 제도를 도입하는 데 있어 기초가 되고 있기 때문입니다. 고용주는 일반적으로 보다 전문적인 모듈로 전환하기 전에 이러한 업무 흐름을 디지털화합니다. 이를 통해 고용주가 복리후생 제도의 광범위한 현대화 초기 단계에 있더라도, 경영진에게는 폭넓은 도입 기반이 확보되어 있습니다.

고용주들이 획일적인 프로그램에서 직원 주도형 선택 모델로 전환함에 따라, 유연한 복리후생/맞춤형 플랫폼 시장은 2031년까지 연평균 성장률(CAGR) 14.28%를 기록하며 성장할 것으로 전망됩니다. 이러한 변화는 의사결정 지원, 헬스 네비게이션, 그리고 보다 구체적인 복리후생 관련 소통에 대한 수요 증가에 힘입어 가속화되고 있습니다. 2025년 Aon의 조사 연구에 따르면, 다국적 기업 직원 대다수는 현행 제도를 대신해 보다 정교한 맞춤형 서비스를 원하고 있는 것으로 나타났습니다. 이는 선택지 설계(초이스 아키텍처)가 플랫폼 로드맵의 핵심으로 자리 잡고 있는 이유를 설명하는 한 가지 요인이 되고 있습니다. 또한, 아시아태평양의 복리후생 기술 시장에서는 복리후생 선택, 웰빙, 커뮤니케이션 도구의 융합이 진행되고 있어, 이에 따라 많은 공급업체들이 개별 모듈을 판매하는 대신, 표창 및 참여 유도 기능을 묶어 제공합니다. CDP Group의 ‘C-Benefits’ 플랫폼은 이러한 방향성을 잘 보여주는 대표적인 사례로, 2025년 기준으로 1,000개 이상의 기업과 80만 명의 직원을 대상으로 상업 보험, 건강 관리, 유연한 복리후생 및 표창 서비스를 통합했습니다. 개인화와 통합에 대한 관심이 높아짐에 따라, 복리후생 기술 시장에서 더 많은 혁신이 촉진될 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the asia-Pacific benefits technology market size is expected to grow from USD 1.72 billion in 2025 to USD 1.93 billion in 2026 and is forecast to reach USD 3.46 billion by 2031 at 12.39% CAGR over 2026-2031.

This report is Segmented by Component (Software, and Services), Application (Benefits Administration, and More), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Banking, Financial Services, and Insurance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Benefits Technology Market Trends and Insights

Cloud-Based HR and Benefits Stack Modernization

Cloud migration has moved from a long-range plan to an operating need for many employers in the Asia-Pacific benefits technology market. Employers are trying to bring HR, payroll, and benefits functions onto unified systems that can support multi-country configurations without repeated custom builds. That shift matters because cloud platforms give benefit teams a single view of usage patterns, plan uptake, and administrative exceptions across different markets. The Asia-Pacific benefits technology market is also moving faster than older HR software cycles because many mobile-native workforces are accessing benefits digitally as their main channel rather than as a secondary desktop option. A clear example came when Sumitomo Metal Mining selected Works Human Intelligence's integrated COMPANY platform to unify around 7,000 group employees on a single HR foundation, replacing fragmented legacy arrangements.

Automation of Enrollment, Compliance, and Payroll Connectivity

Automation has become a major growth engine for the Asia-Pacific benefits technology market because statutory rules differ widely across the region and change on separate timelines. Employers often need one connected process for enrollment, eligibility, payroll calculation, and reporting, but many still run those tasks through disconnected systems or manual handoffs. That operating model becomes difficult when wage ceilings, contribution rules, and local filing requirements differ by country and are updated at different times of year. The Asia-Pacific benefits technology market is therefore seeing stronger demand for platforms that embed local statutory logic into the product, rather than leaving reconciliation work to internal teams. Ramco Systems highlighted that multi-country payroll operations and AI-supported verification are becoming more important as employers try to reduce manual effort and move toward connected payroll and benefits workflows. The market is expected to continue evolving as organizations increasingly prioritize automation and efficiency in compliance.

Data Privacy and Cybersecurity Exposure in Health and Payroll Data

Data privacy is a meaningful drag on the Asia-Pacific benefits technology market because health and payroll data move through systems that are often shared across employers, insurers, and payroll operators. The region does not operate under a single privacy framework, so vendors must adjust their data-handling, storage, notification, and transfer practices country by country. That raises the minimum product standard for encryption, access control, residency design, and audit readiness before a platform can scale across borders. Smaller SaaS vendors face a harder path because localization and security investment rise before revenue reaches regional scale. For multinational employers, the result is a slower buying cycle because privacy reviews now affect architectural decisions as much as contract terms.

Other drivers and restraints analyzed in the detailed report include:

- Mobile-First Self-Service and Benefits Experience Demand

- SME Adoption of Low-Cost SaaS Benefits Platforms

- Legacy HRIS and Payroll Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 62.45% of the Asia-Pacific benefits technology market share in 2025, indicating that platform licenses still accounted for the largest revenue base in the region. That leadership reflects the strong role of software-led delivery models for enrollment, compliance management, employee access, and payroll connectivity. At the same time, the commercial center of gravity is shifting as customers increasingly need platforms that can be implemented and localized without lengthy internal projects. The Asia-Pacific benefits technology market is now rewarding vendors that can pair software with deployment depth across languages, currencies, and statutory frameworks.

Services are projected to expand at a 15.02% CAGR through 2031, faster than the software component, underscoring the value now in implementation, integration, advisory, and support work. The shift does not reflect weak software demand; it reflects the fact that many employers already have product options and instead struggle with execution across multiple countries. That is why implementation and integration services have become a core demand driver for the Asia-Pacific benefits technology industry, especially where payroll and benefits data must be reconciled across separate systems. Regional changes to statutory rules have added urgency, as employers have had to update payroll-benefit logic rather than leave older links in place. Ramco Systems' work around multi-country payroll and AI-based verification reflects this broader service demand, where the product alone is not enough without strong integration capability.

Benefits administration accounted for 28.16% of the Asia-Pacific benefits technology market in 2025, making it the largest application layer. That position is logical because enrollment, eligibility checks, and carrier or provider connectivity remain the foundation for every employer deployment. Employers usually digitize those workflows before they move into more specialized modules. This gives the administration layer a broad installed base, even when employers are still early in wider benefits modernization.

Flexible benefits and personalization platforms are projected to grow at a 14.28% CAGR through 2031 as employers move away from one-size-fits-all programs and toward employee-choice models. The shift is being reinforced by rising demand for decision support, health navigation, and more targeted benefit communication. A 2025 Aon research study found that many employees in multinational firms would trade their current arrangements for greater personalization, which helps explain why choice architecture is moving to the center of platform roadmaps. The Asia-Pacific benefits technology market is also seeing convergence among benefits selection, wellbeing, and communication tools, which is why many vendors now bundle recognition and engagement functions rather than sell isolated modules. CDP Group's C-Benefits platform exemplifies this direction by combining commercial insurance, health management, flexible benefits, and recognition services for more than 1,000 enterprises and 800,000 employees in 2025. The growing emphasis on personalization and integration is expected to drive further innovation in the benefits technology market.

List of Companies Covered in this Report:

- Benefitfocus.com, Inc.

- Businessolver

- PlanSource Benefits Administration, Inc.

- bswift LLC

- Benefex Limited

- Employee Navigator

- PeopleKeep, Inc.

- ThrivePass, Inc.

- Darwinbox Digital Solutions Pvt. Ltd.

- Employment Hero Pty Ltd

- Bargain Technologies Private Limited

- Mednefits Singapore Pte. Ltd.

- Nayya Health, Inc.

- Forma Inc.

- League, Inc.

- Thanks Ben LTD

- SME HCI Limited

- Yu Life Ltd.

- Plum Benefits Insurance Brokers Pvt Ltd

- Invoq Loop Insurance Brokers Pvt Ltd

- Get Paz Insurance Brokers Pvt Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-Based HR and Benefits Stack Modernization

- 4.2.2 Automation of Enrollment, Compliance, and Payroll Connectivity

- 4.2.3 Mobile-First Self-Service and Benefits Experience Demand

- 4.2.4 SME Adoption of Low-Cost SaaS Benefits Platforms

- 4.2.5 Medical Inflation-Led Benefits Cost Optimization

- 4.2.6 Cross-Border Statutory Benefits Fragmentation Across Asia-Pacific

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cybersecurity Exposure in Health and Payroll Data

- 4.3.2 Legacy HRIS and Payroll Integration Complexity

- 4.3.3 Budget Rebalancing Delaying Net-New Module Purchases

- 4.3.4 Low Utilization Signal Quality in Wellbeing and Mental Health Benefits

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration Services

- 5.1.2.2 Consulting and Advisory Services

- 5.1.2.3 Support and Maintenance Services

- 5.2 By Application

- 5.2.1 Benefits Administration

- 5.2.2 Compensation and Rewards Management

- 5.2.3 Employee Recognition and Engagement Platforms

- 5.2.4 Benefits Communication and Employee Portals

- 5.2.5 Flexible Benefits / Personalization Platforms

- 5.2.6 Other Applications

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Based

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-Sized Enterprises

- 5.5 By End-User Industry

- 5.5.1 Banking, Financial Services, and Insurance

- 5.5.2 IT and Telecommunications

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Manufacturing

- 5.5.5 Retail and E-Commerce

- 5.5.6 Public Sector and Education

- 5.5.7 Other End-User Industries

- 5.6 By Geography

- 5.6.1 China

- 5.6.2 Japan

- 5.6.3 India

- 5.6.4 South Korea

- 5.6.5 Australia and New Zealand

- 5.6.6 Southeast Asia

- 5.6.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Benefitfocus.com, Inc.

- 6.4.2 Businessolver

- 6.4.3 PlanSource Benefits Administration, Inc.

- 6.4.4 bswift LLC

- 6.4.5 Benefex Limited

- 6.4.6 Employee Navigator

- 6.4.7 PeopleKeep, Inc.

- 6.4.8 ThrivePass, Inc.

- 6.4.9 Darwinbox Digital Solutions Pvt. Ltd.

- 6.4.10 Employment Hero Pty Ltd

- 6.4.11 Bargain Technologies Private Limited

- 6.4.12 Mednefits Singapore Pte. Ltd.

- 6.4.13 Nayya Health, Inc.

- 6.4.14 Forma Inc.

- 6.4.15 League, Inc.

- 6.4.16 Thanks Ben LTD

- 6.4.17 SME HCI Limited

- 6.4.18 Yu Life Ltd.

- 6.4.19 Plum Benefits Insurance Brokers Pvt Ltd

- 6.4.20 Invoq Loop Insurance Brokers Pvt Ltd

- 6.4.21 Get Paz Insurance Brokers Pvt Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment