|

시장보고서

상품코드

2064467

항체 발견용 AI 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Antibody Discovery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

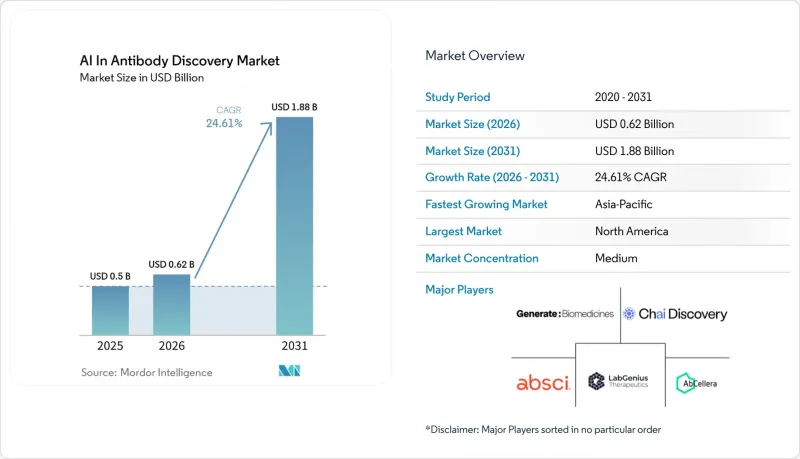

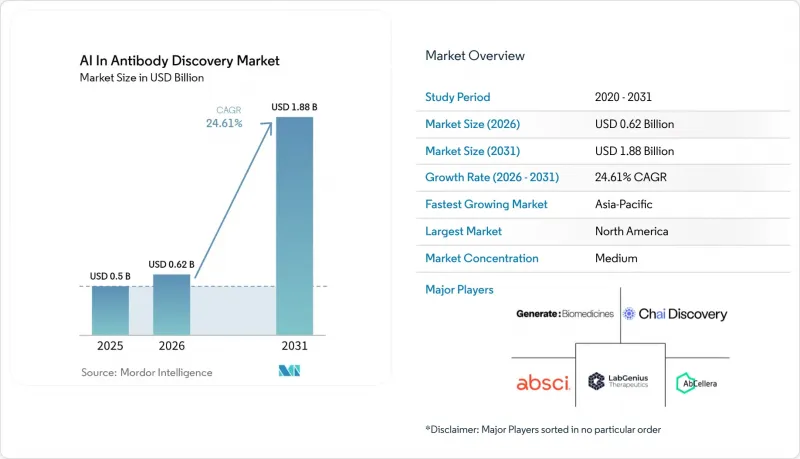

Mordor Intelligence에 의하면, 항체 발견용 AI 시장 규모는 2025년 5억 달러로 평가되었고, 2026년에는 6억 2,000만 달러로 추정되고, 2026-2031년 CAGR 24.61%로 성장을 지속할 전망이며, 2031년까지 18억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제공 형태별(소프트웨어 플랫폼, 기타), 기술별(구조 예측, 기타), 용도별(데 노보 항체 설계, 기타), 항체 모달리티별(단일클론 항체, 기타), 치료 분야별(종양학, 기타), 최종 사용자별(제약 회사, 기타), 지역별(북미, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 항체 발견용 AI 시장 동향 및 인사이트

기존 신약 개발 비용 구조가 플랫폼 전환을 촉구하고 있습니다.

기존 방식의 항체 신약 개발에서 발생하는 비용 부담이 자금 사정의 악화로 인해 정당화하기 어려워짐에 따라, 항체 신약 개발 분야의 AI 시장은 성장세를 보이고 있습니다. Absci의 보고서에 따르면, AI를 활용한 프로그램의 경우 프로그램당 투자액을 5,000만 달러 이상에서 1,500만 달러 가까이까지 절감하고, 개발 기간을 4-6년에서 약 2년으로 단축할 수 있다고 합니다. 전임상 단계에서의 탈락률은 역사적으로 90%를 초과해 왔으며, 이는 초기 신약 개발 투자의 대부분이 임상적 성과로 이어지지 않고 있음을 의미합니다. GPCR, 이온 채널, 멀티패스 막 단백질과 같은 초기 단계의 대상 분류에서는 이러한 압박이 더욱 심해지고 있습니다. 이러한 분야에서는 저온 전자현미경(cryo-EM)의 처리 능력 한계로 인해, 기존 연구에서 활용할 수 있는 구조 정보가 여전히 제한적이기 때문입니다. 항체 신약 개발 분야의 AI 시장에서 이는 기존 경쟁사들이 항원을 완전히 규명하기 전에 까다로운 프로그램을 완료할 수 있는 플랫폼에 실질적인 ‘선점자’의 기회를 제공합니다. 또한, 이것이 구매자가 좁은 범위의 소프트웨어 이용에서 벗어나, 더 많은 신약 개발 위험과 프로그램 주도권을 떠안게 되는 광범위한 플랫폼으로 전환하고 있는 이유를 설명해 줍니다.

차세대 바이오로직스와 정밀 의학에 대한 수요가 증가함에 따라 AI의 설계 영역이 확대되고 있습니다.

또한, 보다 복잡한 바이오의약품 및 종양학과 면역학 분야의 정밀의학(precision medicine) 활용 사례로 향하는 명확한 파이프라인의 전환 역시 시장을 견인하고 있습니다. 2025년 초까지 전 세계적으로 12종 이상의 이중 특이성 항체가 규제 당국의 승인을 받았으며, 200종 이상의 이중 특이성 항체가 종양학 및 면역학 분야에서 활발한 임상시험 단계에 접어들었습니다. 이러한 파이프라인 구성으로 인해, 설계상의 과제는 기존 방식의 스크리닝이 효율적으로 처리할 수 있는 범위를 넘어섰습니다. 왜냐하면 친화도, 약물 동태, 제조 가능성에 대해 여러 결합 암을 동시에 최적화해야 하기 때문입니다. 항체 신약 개발 분야의 AI 시장에서는 정밀 의학에 대한 수요가 이러한 변화를 뒷받침하고 있습니다. 왜냐하면 새로운 프로그램은 기존 방식으로는 제대로 다루기 어려웠던, 선택성이 더 높은 사이토카인 수용체, 공동자극 채널, 면역학 관련 영역을 표적으로 삼고 있기 때문입니다. 따라서, 네이티브 다중 특이성 설계 기능을 갖추지 못한 플랫폼은 향후 거래 흐름에서 가장 빠르게 성장하는 부문에서 뒤처질 위험에 직면해 있습니다.

데이터 부족이 모델의 일반화 능력을 구조적으로 제한하고 있습니다.

시장은 여전히 근본적인 데이터 문제에 직면해 있습니다. 왜냐하면, 공개된 구조 데이터의 포괄성만으로는 대상 클래스 전체에 걸친 광범위한 일반화를 수행하기에는 불충분하기 때문입니다. 『Frontiers in Immunology』지는 2025년 5월 기준으로 Protein Data Bank(PDB)에 수록된 공개 항체 구조는 1만 건 미만이며, 약 800가지 유형의 고유 항원에 걸친 VHH 복합체는 2,000건에 불과하다고 지적하고 있습니다. 이러한 데이터 부족은 고르지 않게 나타나는데, 일반적인 종양학 표적에 대해서는 풍부한 주석이 있는 반면, GPCR, 이온 채널, 희귀질환의 항원에 대해서는 여전히 데이터가 부족한 실정입니다. 2025년 11월 도쿄대학이 실시한 벤치마크에서 AlphaFold3가 항체-항원 복합체에서 DockQ >=0.80을 달성한 성공률은 고작 11%에 그쳤으며, 이는 공개 모델에게 이종 이합체의 기하학적 구조가 얼마나 어려운 과제인지를 여실히 보여주고 있습니다. 항체 신약 개발 분야의 AI 시장에서 이러한 상황은 단순한 모델 확장에 비해, 실험실을 통한 독자적인 데이터셋 생성의 가치를 더욱 높여주고 있습니다. 또한, 계산 비용 증가, 학제 간 인재에 대한 수요 증가, 물리적 검증 속도가 디지털 설계에 뒤처지면서 특허 취득이 어려워지는 등의 문제도 발생하고 있습니다.

부문별 분석

2025년 기준으로 소프트웨어 플랫폼은 항체 발견용 AI 시장 점유율의 38.31%를 차지했으나, 디스커버리 서비스는 2031년까지 연평균 성장률(CAGR) 26.38%로 확대될 것으로 전망됩니다. 이러한 세부 내역은 시장이 당초에는 도구와 인터페이스를 통해 상용화되었습니다가, 이후 결제를 프로그램의 성과와 더 밀접하게 연계하는 계약 형태로 전환되기 시작했음을 보여줍니다. 디스커버리 서비스는 대규모 사내 시스템을 구축하는 것보다 발견 위험을 플랫폼 파트너에게 전가하는 것을 선호하는 구매자들로부터 혜택을 보고 있습니다. 따라서, 항체 발견용 AI 시장은 단순한 도구 이용에서 벗어나, 대상 선정, 서열 생성, 검증 지원을 포함하는 보다 종합적인 아웃소싱 모델로 전환되고 있습니다. 바이엘(Bayer)에 따르면, 2026년 1월 기준으로 크래들(Cradle)은 전 세계 상위 25개 제약사 중 6곳과 50건 이상의 진행 중인 연구개발 프로그램에 도입되어 있으며, 이는 단순한 라이선싱 계약보다 더 깊은 서비스 관계가 지속가능성이 더 높다는 견해를 뒷받침하는 것입니다.

통합 플랫폼 파트너십과 데이터 모델 라이선싱은 현재로서는 규모가 아직 작지만, 가치 창출 방식을 변화시킨다는 점에서 모두 전략적으로 중요한 위치를 차지하고 있습니다. 전자의 모델은 마일스톤 연계형 공동 개발 구조를 통해 이익을 분배하기 때문에 플랫폼의 인센티브를 파트너의 성과와 더욱 밀접하게 연계시킬 수 있습니다. 후자의 모델은 선별된 데이터셋과 모델 가중치를 독립적인 지적 재산으로 수익화함으로써, 기존 CRO 모델에서는 제공되지 않았던 수익원을 항체 발견용 AI 시장에 창출합니다. 기반 모델의 우위를 뒤집기가 점점 더 어려워짐에 따라, 데이터 및 모델 라이선싱이 상용 스택 내에서 가장 높은 수익률을 기록하는 부문으로 부상할 가능성이 있습니다.

2025년 기준으로, 항체 발견용 AI 시장 규모 중 구조 예측이 33.24%를 차지했으나, 생성형 AI와 단백질 언어 모델은 2031년까지 연평균 성장률(CAGR) 28.52%로 성장할 것으로 전망됩니다. 이러한 수익 구성은 구조 예측이 거의 모든 하류 설계 및 최적화 작업의 기반 계층으로 계속 자리 잡고 있다는 사실을 반영하고 있습니다. 특히, 기존의 신약 개발 워크플로우를 처음부터 재구축하는 것이 아니라 AI를 기존 워크플로우에 통합하려는 팀에게는 여전히 가장 확립된 기술적 진입로입니다. 그러나 항체 발견용 AI 시장은 현재 예측을 뛰어넘는 변화를 겪고 있습니다. 왜냐하면 주요 과제는 더 이상 ‘어떤 구조가 존재하는가’에 그치지 않고, ‘어떤 배열을 만들어야 하는가’로 옮겨가고 있기 때문입니다. Chai-2가 발표한 20%의 적중률에 비해, 기존 베이스라인이 0.1% 수준에 머무르고 있다는 사실은 생성형 접근 방식이 왜 성능에 대한 기대치를 재정의하고 있는지를 보여줍니다.

머신러닝과 딥러닝은 리드 최적화, 개발 가능성 평가, 순위 결정과 같은 과제에서 여전히 의미 있는 상업적 가치를 지니고 있습니다. 이러한 업무에서 구매자는 전체 프로세스를 변경하지 않으면서도 측정 가능한 성과를 기대하고 있습니다. 자연어 처리(NLP)와 지식 그래프 역시 대상 관계 매핑 및 문헌 통합 분야에서 그 범위는 제한적이긴 하지만 유용한 역할을 확립해 가고 있습니다. 랩오토메이션과 연동된 폐쇄 루프 AI는 설계와 분석 주기를 별개의 단계로 다루는 것이 아니라 단일 시스템으로 통합하기 때문에 장기적으로 볼 때 여전히 가장 혁신적인 기술 분야로 남아 있습니다. 항체 개발 시장에서 AI를 도입함에 따라, 병목 현상이 인간의 분석 단계에서 시약의 흐름, 로봇의 처리 능력, 실험실 운영 조정 단계로 이동하게 되며, 이에 따라 비용 구조가 변화합니다.

지역별 분석

2025년, 북미는 항체 발견용 AI 시장 점유율 43.44%를 차지했으며, 지역별 수요에서 1위를 유지했습니다. 이 지역은 AI를 기반으로 하는 바이오테크 기업들이 밀집해 있고, 경험이 풍부한 자본 배분자들이 있으며, 단백질 공학 및 머신러닝 연구를 지원하는 공공 과학 자금의 혜택을 받고 있습니다. 이러한 조합 덕분에 구매자, 자금 제공업체, 기술 파트너가 이미 동일한 생태계에 집중되어 있어, 북미는 항체 발견용 AI 시장에 있어 강력한 상업 거점으로 자리매김하고 있습니다. 또한, 제약 기업들이 소규모 시범 계약만으로 AI를 검증하는 데 그치지 않고, 보다 장기적인 공동 개발 체제에 전념하는 여러 차례에 걸친 파트너십 구축도 뒷받침하고 있습니다. 따라서 북미는 벤치마크를 통한 차별화, 특허 전략, 마일스톤 기반 수익 모델을 위한 주요 실증의 장으로 자리매김하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 26.22%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 지역 클러스터가 될 것입니다. 중국과 일본은 서로 다른 모델을 통해 이러한 성장을 주도하고 있는데, 중국은 정책 지원을 받은 AI 바이오의약품에 대한 투자와 대규모 국내 컴퓨팅 인프라 확충에 의존하고 있는 반면, 일본은 산학 협력을 중점적으로 추진하고 있습니다. 아시아태평양에서 항체 개발에 활용되는 AI 시장이 확대되고 있는 것은 현지 기업들이 더욱 강력한 항체 데이터셋과 더욱 충실한 컴퓨팅 환경, 그리고 지역에 특화된 개발 인프라를 구축하고 있기 때문입니다. 또한, 데이터 주권도 실용적인 우위로 자리 잡고 있습니다. 이는 독자적인 배열 데이터를 관리되는 국내 환경 내에서 보유할 수 있는 경우, 규제 대상인 제약 부문의 공동 연구가 더 원활하게 진행될 수 있기 때문입니다. 이 지역의 연구 생태계는 현재 추격자의 입장에서 벗어나고 있으며, 벤치마크의 진행 상황을 고려할 때 예측 기간 동안 미국 플랫폼과의 경쟁이 더욱 직접적으로 전개될 것으로 보입니다.

유럽은 여전히 중요한 중견 지역이며, 주로 독일과 영국에 의해 지탱되고 있습니다. 이들 국가에서는 대형 제약 그룹들이 AI를 활용한 신약 개발을 단순한 실험적 부가 기능으로 분리하지 않고, 핵심 연구개발(R&D)에 통합하고 있습니다. 2026년 1월 바이엘(Bayer)이 크래들(Cradle)과 체결한 다년간의 제휴는 유럽의 유서 깊은 제약 기업이 소규모 탐색적 시범 사업에 지출을 국한하지 않고, AI를 활용한 단백질 및 항체 공학에 사업 예산을 투자하고 있음을 보여줍니다. 또한, 유럽의 항체 개발 분야 AI 시장은 무세포 시스템 및 폐쇄형 습식 실험실 통합에 대한 초기 노력의 혜택을 받고 있으며, 이는 해당 지역의 공정 관리 및 중개과학 분야의 강점과 부합합니다. 남미, 중동 및 아프리카는 여전히 초기 단계에 있으며, 활동은 독립형 플랫폼 구축보다는 학술 기관 및 수탁 제조의 확대에 중점을 두고 있습니다. 그럼에도 불구하고, AI 신약 개발 서비스를 제공하는 세계 CRO의 등장으로 현지 수요가 점차 형성되기 시작했으며, 2027년 이후에는 측정 가능한 지역 시장 점유율로 이어질 가능성이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the aI in antibody discovery market size is expected to grow from USD 0.5 billion in 2025 to USD 0.62 billion in 2026 and is forecast to reach USD 1.88 billion by 2031 at 24.61% CAGR over 2026-2031.

This report is Segmented by Offering (Software Platforms, and More), Technology (Structure Prediction, and More), Application (De Novo Antibody Design, and More), Antibody Modality (Monoclonal Antibodies, and More), Therapeutic Area (Oncology, and More), End User (Pharmaceutical Companies, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In Antibody Discovery Market Trends and Insights

Conventional Discovery Economics Force a Platform Pivot

The AI in antibody discovery market is gaining force because the cost burden of conventional antibody discovery has become difficult to justify in a tighter capital environment. Absci reported that AI-guided programs can lower per-program investment from more than USD 50 million to nearly USD 15 million and reduce development time from 4-6 years to roughly 2 years. Preclinical attrition has historically exceeded 90%, which means most early discovery spending has not translated into clinical return. The pressure is even stronger in early target classes such as GPCRs, ion channels, and multi-pass membrane proteins, where cryo-EM throughput still limits the structural information available for conventional studies. In the AI in antibody discovery market, that creates a practical first-mover window for platforms that can close difficult programs before traditional competitors fully characterize the antigen. It also explains why buyers are moving from narrow software use toward broader platform relationships that can carry more discovery risk and more program ownership.

Rising Demand for Next-Generation Biologics and Precision Medicine Expands AI's Design Surface

The market is also being lifted by a clear pipeline shift toward more complex biologics and toward precision medicine use cases in oncology and immunology. By early 2025, more than 12 bispecific antibodies had received regulatory approval worldwide, and more than 200 bispecifics were in active clinical trials across oncology and immunology. That pipeline mix expands the design problem beyond what traditional screening can manage efficiently, because multiple binding arms must be optimized at the same time for affinity, pharmacokinetics, and manufacturability. In the AI in antibody discovery market, precision medicine demand is reinforcing that shift because newer programs are targeting more selective cytokine receptors, co-stimulatory pathways, and immunology adjacencies that older methods handled poorly. Platforms that lack native multispecific design capability are therefore at risk of being excluded from the fastest-growing parts of future deal flow.

Data Scarcity Structurally Limits Model Generalization

The market still faces a basic data problem, because public structural coverage remains too thin for broad generalization across target classes. Frontiers in Immunology noted that the Protein Data Bank contained fewer than 10,000 publicly available antibody structures and close to 2,000 VHH complexes across nearly 800 unique antigens as of May 2025. That scarcity is uneven, because common oncology targets have richer annotations while GPCR, ion-channel, and rare-disease antigens remain underrepresented. A November 2025 benchmark from the University of Tokyo showed that AlphaFold3 achieved only an 11% success rate at DockQ >= 0.80 for antibody-antigen complexes, which underlines how difficult heterodimer geometry still is for public models. In the AI in antibody discovery market, this makes proprietary dataset generation through wet-lab campaigns more valuable than simple model scaling. It also raises the cost of compute, increases the premium for cross-disciplinary talent, and makes patent enablement harder when physical validation trails digital design.

Other drivers and restraints analyzed in the detailed report include:

- AI Opens GPCR and Ion-Channel Antibody Programs

- Antibody-Specific Foundation Models Improve Hit Quality and Pull More Collaboration Spend

- Wet-Lab Triage Bottleneck Constrains Throughput Gains

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software Platforms accounted for 38.31% of the AI in antibody discovery market share in 2025, while Discovery Services is projected to expand at a 26.38% CAGR through 2031. That mix shows how the market first commercialized through tools and interfaces, then began moving toward contracts that tie payment more closely to program delivery. Discovery Services is benefiting from buyers who prefer to shift discovery risk onto platform partners rather than build large internal stacks. The AI in antibody discovery market is therefore moving away from simple tool access and toward fuller outsourcing models that include target work, sequence generation, and validation support. Bayer said Cradle was being deployed across 6 of the top 25 global pharma companies and more than 50 active R&D programs as of January 2026, which supports the view that deeper service relationships are becoming more durable than license-only arrangements.

Integrated Platform Partnerships and Data and Model Licensing remain smaller today, but both carry strategic weight because they change how value is captured. The first model spreads upside through milestone-linked co-development structures, which can align platform incentives more closely with partner outcomes. The second model monetizes curated datasets and model weights as standalone intellectual property, which gives the AI in antibody discovery market a revenue layer that traditional CRO models did not offer. As foundation model leadership becomes harder to displace, data and model licensing may emerge as the highest-margin part of the commercial stack.

Structure Prediction held 33.24% of the AI in antibody discovery market size in 2025, while Generative AI and Protein Language Models is set to grow at a 28.52% CAGR through 2031. That revenue split reflects the fact that structure prediction remains the base layer for nearly every downstream design and optimization task. It is still the most established technical entry point, especially for teams that are adding AI into existing discovery workflows rather than rebuilding those workflows from the start. The AI in antibody discovery market is now shifting beyond prediction, though, because the main question is no longer just what structure exists but what sequence should be created. Chai-2's disclosed 20% hit rate versus a conventional baseline near 0.1% shows why generative approaches are resetting performance expectations.

Machine Learning and Deep Learning still hold meaningful commercial value in lead optimization, developability scoring, and ranking tasks where buyers want measured gains without changing the full process. Natural Language Processing and Knowledge Graphs are also building a narrower but useful role in target relationship mapping and literature synthesis. Closed-loop AI with Lab Automation remains the most disruptive long-run technology layer because it couples design and assay cycles into one system rather than treating them as separate steps. In the AI in antibody discovery market, that changes the cost structure by shifting the bottleneck from human analysis toward reagent flow, robotic throughput, and lab orchestration.

Geography Analysis

North America held 43.44% of the AI in antibody discovery market share in 2025, which kept it in the lead across regional demand. The region benefits from a dense group of AI-native biotechs, experienced capital allocators, and public science funding that supports protein engineering and machine learning work. That combination gives the AI in antibody discovery market a strong commercial center in North America because buyers, funders, and technical partners are already concentrated in the same ecosystem. It also supports multi-round partnership behavior, where pharma companies commit to longer co-development structures instead of testing AI through small pilot contracts only. North America therefore remains the main proving ground for benchmark differentiation, patent strategy, and milestone-based revenue models.

Asia-Pacific is projected to grow at a 26.22% CAGR through 2031, making it the fastest-growing regional cluster. China and Japan are driving that rise through different models, with China leaning on policy-backed AI biopharmaceutics investment and larger domestic compute build-out, while Japan is leaning more on corporate-academic collaboration. The AI in antibody discovery market is expanding in Asia-Pacific because local players are building stronger antibody datasets, stronger compute access, and more region-specific development infrastructure. Data sovereignty is also becoming a practical advantage, since regulated pharmaceutical collaborations are more likely to move forward when proprietary sequence data can remain under controlled domestic environments. The region's research ecosystems are now moving beyond follower status, and their benchmark progress suggests that competition with U.S. platforms will become more direct over the forecast period.

Europe remains a meaningful mid-tier region, supported mainly by Germany and the United Kingdom, where large pharma groups are putting AI discovery into core R&D instead of isolating it as an experimental add-on. Bayer's multi-year partnership with Cradle in January 2026 showed that established pharma companies in Europe are committing operating budgets to AI-assisted protein and antibody engineering rather than limiting spend to small exploratory pilots. The AI in antibody discovery market also benefits in Europe from early work in cell-free systems and closed-loop wet-lab integration, which fits the region's strength in process discipline and translational science. South America and the Middle East and Africa remain early-stage areas, with activity centered more on academic institutes and contract manufacturing expansion than on independent platform creation. Even so, the presence of global CROs offering AI discovery services is starting to build local demand that can turn into measurable regional share after 2027.

- AbCellera

- Absci

- Alloy Therapeutics

- Antiverse

- BigHat Biosciences

- Chai Discovery

- Cradle

- Etcembly

- EVQLV

- Generate:Biomedicines

- Harbour BioMed

- Infinimmune

- Insilico Medicine

- LabGenius Therapeutics

- MAbSilico

- MOLCURE

- Nabla Bio

- Nona Biosciences

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Conventional Discovery Cost and Attrition Pressure

- 4.2.2 Rising Demand for Next-Generation Biologics

- 4.2.3 Precision Medicine Demand in Oncology and Immunology

- 4.2.4 Expanding Pharma-AI Collaboration Budgets

- 4.2.5 AI Opening GPCR and Ion-Channel Antibody Programs

- 4.2.6 Antibody-Specific Foundation Models Improving Hit Quality

- 4.3 Market Restraints

- 4.3.1 Scarcity of Labeled Antibody Data

- 4.3.2 High Compute and Interdisciplinary Talent Cost

- 4.3.3 Wet-Lab Triage Bottleneck for AI-Generated Libraries

- 4.3.4 Patentability and Enablement Pressure on AI-Generated Antibodies

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Offering

- 5.1.1 Software Platforms

- 5.1.2 Discovery Services

- 5.1.3 Integrated Platform Partnerships

- 5.1.4 Data and Model Licensing

- 5.2 By Technology

- 5.2.1 Structure Prediction

- 5.2.2 Generative AI and Protein Language Models

- 5.2.3 Machine Learning and Deep Learning

- 5.2.4 Natural Language Processing and Knowledge Graphs

- 5.2.5 Closed-loop AI with Lab Automation

- 5.3 By Application

- 5.3.1 Target Identification and Validation

- 5.3.2 Epitope Mapping and Binder Screening

- 5.3.3 De novo Antibody Design

- 5.3.4 Lead Optimization and Engineering

- 5.3.5 Developability and Manufacturability Prediction

- 5.4 By Antibody Modality

- 5.4.1 Monoclonal Antibodies

- 5.4.2 Bispecific Antibodies

- 5.4.3 Multispecific Antibodies

- 5.4.4 Antibody-Drug Conjugates

- 5.4.5 Nanobodies and Single-domain Antibodies

- 5.5 By Therapeutic Area

- 5.5.1 Oncology

- 5.5.2 Autoimmune and Inflammatory Diseases

- 5.5.3 Infectious Diseases

- 5.5.4 Neurology

- 5.5.5 Metabolic Diseases

- 5.5.6 Rare Diseases

- 5.6 By End User

- 5.6.1 Pharmaceutical Companies

- 5.6.2 Biotechnology and Platform Companies

- 5.6.3 CROs and CDMOs

- 5.6.4 Academic and Research Institutes

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 AbCellera

- 6.3.2 Absci

- 6.3.3 Alloy Therapeutics

- 6.3.4 Antiverse

- 6.3.5 BigHat Biosciences

- 6.3.6 Chai Discovery

- 6.3.7 Cradle

- 6.3.8 Etcembly

- 6.3.9 EVQLV

- 6.3.10 Generate:Biomedicines

- 6.3.11 Harbour BioMed

- 6.3.12 Infinimmune

- 6.3.13 Insilico Medicine

- 6.3.14 LabGenius Therapeutics

- 6.3.15 MAbSilico

- 6.3.16 MOLCURE

- 6.3.17 Nabla Bio

- 6.3.18 Nona Biosciences

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment