|

시장보고서

상품코드

2065446

컨택센터 분야 인력 관리(WFM) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Workforce Management (WFM) In Contact Centers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

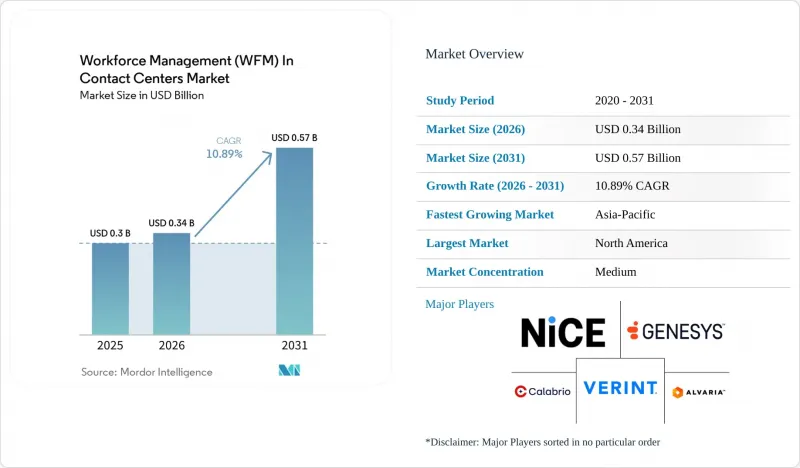

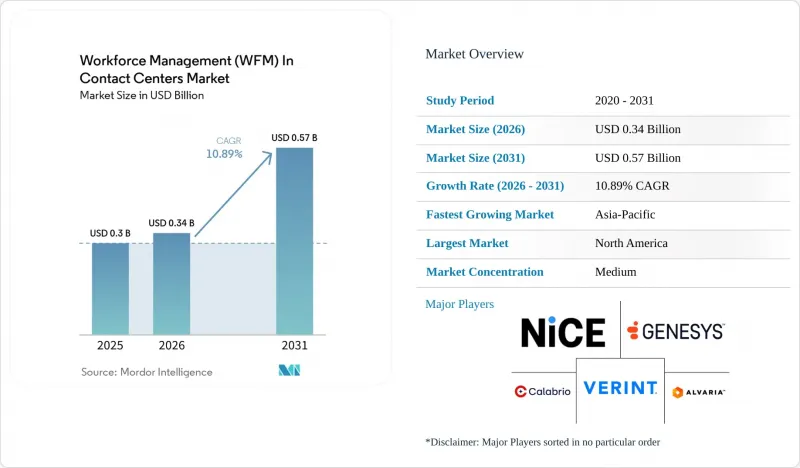

컨택센터 분야 인력 관리(WFM) 시장 규모는 2025년에 3억 달러로 평가되었습니다. 2026년 3억 4,000만 달러에서 2031년까지 5억 7,000만 달러로 확대되어 예측 기간(2026-2031년) CAGR은 10.89%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 모델(클라우드, On-Premise, 하이브리드), 기업 규모(대기업 및 중소기업), 최종 사용자 산업 분야(은행, 금융서비스 및 보험(BFSI), IT 및 통신, 의료, 소매 및 전자상거래, 여행·호텔업 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 컨택센터 분야 인력 관리(WFM) 시장 동향 및 인사이트

AI를 활용한 예측 및 스케줄링 도입

AI 기반 예측은 컨택센터 분야 인력 관리(WFM) 시장에서 조달 주기의 후반부에 추가되는 선택적 기능이 아니라, 핵심 구매 요건으로 자리 잡고 있습니다. NICE사에 따르면, 컨택트 센터에서 AI 기반의 예측 및 스케줄링을 통해 예측 오차를 기존의 ±20% 범위에서 ±5-8%로 줄일 수 있으며, 이로 인해 인력 배치 비용과 서비스 성과에 직접적인 영향을 미칩니다고 합니다. 이러한 개선은 기획팀의 일상 업무 역할도 변화시키고 있습니다. 플랫폼이 정형화된 모델 작업의 상당 부분을 처리해 주는 덕분에, 애널리스트는 해석, 예외 처리 및 운영상의 의사 결정에 더 많은 시간을 할애할 수 있게 되었기 때문입니다. Verint사는 대규모 언어 모델 워크로드를 위해 자사의 로드맵을 Amazon Web Services 및 Amazon Bedrock과 연계함으로써, 향후 24개월 동안 고객의 예측 정확도가 최대 50% 향상될 가능성이 있다고 밝혔습니다. 이로 인해 컨택트 센터의 인력 관리 시장 전반에 걸친 기준이 높아지고 있습니다. 구매자들은 더 이상 단순히 기능 목록의 확충뿐만 아니라, 구체적인 정확도의 향상을 기대하게 되었기 때문입니다. 2026년 『International Journal of Intelligent Systems and Applications in Engineering』지에 게재된 동료 심사를 거친 연구에서도, 실시간 수요 예측과 운영 데이터에 대한 자연어 기반 접근을 통해 인력 계획이 정적 계획에서 지속적인 운영 관리로 전환되고 있음이 밝혀졌습니다.

클라우드 네이티브형 CCaaS로의 전환이 가속화되고 있습니다.

컨택트 센터 시장에서 인력 관리(WFM)의 가장 뚜렷한 성장 요인 중 하나는 클라우드 전환입니다. 이는 WFM 시스템 교체가 대부분의 경우 컨택 센터 플랫폼 전체의 업데이트와 병행하여 이루어지기 때문입니다. NICE사는 클라우드 기반 인력 관리 솔루션을 AI를 활용한 예측, 스케줄링 및 업무 중 관리를 지속적으로 업데이트하며 제공하는 수단으로 자리매김하고 있으며, 이는 기업들이 현재 컨택 센터 소프트웨어 전반에 요구하는 운영 모델과 부합합니다. Aspect사의 2025년 마이그레이션 가이드라인 역시, 일상 업무에 지장을 주지 않으면서 핵심 WFM 워크로드를 레거시 환경에서 마이그레이션하기 위한 현실적인 방안으로 단계적인 클라우드 도입을 제시하고 있습니다. 이 전환 경로가 중요한 이유는 컨택트 센터 시장의 인력 관리 분야에서 구매자가 구형 인프라를 갱신하고, 상호작용 데이터, 인력 배치 로직, 실시간 자동화를 보다 긴밀하게 통합함으로써 이점을 얻을 수 있기 때문입니다. 2026년 3월 Aspect Software와 Five9가 체결한 제휴는 실시간 상담원 상태 데이터와 자동화된 주간 인력 배치 조정을 통해, 각 벤더들이 WFM을 클라우드 상호작용 플랫폼과 더욱 긴밀하게 연계하고 있음을 보여주는 사례였습니다. 클라우드 생태계를 도입하는 기업이 늘어남에 따라, 플랫폼 선택이 도입 라이프사이클 전반에 걸쳐 기업이 따르게 될 WFM의 방향을 점점 더 좌우하고 있습니다.

레거시 스택 통합의 복잡성

많은 대규모 컨택트 센터가 여전히 ACD, WFM 도구, QA 플랫폼, 인사 시스템 간의 고도로 맞춤화된 연결에 의존하고 있기 때문에 레거시 시스템의 통합은 컨택센터 분야 인력 관리(WFM) 분야에서 여전히 가장 뿌리 깊은 장벽 중 하나로 남아 있습니다. 아스펙트사의 클라우드 전환 지침이 단계적 전환을 지원하는 이유는 많은 조직이 일정 수립, 규정 준수, 보고서 작성에 차질을 빚을 위험을 감수하지 않고서는 모든 인력 관리 프로세스를 한 번에 전환할 수 없기 때문입니다. NICE사 역시 예측, 스케줄링, 일일 관리, 채널 수준 계획과의 폭넓은 연동을 플랫폼의 핵심 축으로 삼고 있으며, 이는 구매자들이 현재 분산된 업무 워크플로우의 통합을 얼마나 중요하게 여기는지를 반영하고 있습니다. 그 어려움은 기술적인 측면에만 그치지 않습니다. 기존의 규칙 세트에는 오랜 기간에 걸친 초과근무 정책, 각 거점별 관행, 규정 준수 관련 논리가 포함되어 있는 경우가 많기 때문에 이를 새로운 시스템에서 정확하게 재현해야 하기 때문입니다. 그로 인해 계약 체결이 지연되고, 컨택트 센터 인력 관리 시장 전반, 특히 여러 거점이나 사업 부서를 보유한 대기업의 경우 도입 작업이 장기화되고 맙니다. 따라서 조달 팀이 도입 위험을 주요 판단 기준으로 삼는 경우, 더 강력한 커넥터와 마이그레이션 서비스, 그리고 상세한 설정 기능을 갖춘 공급업체가 유리한 입장에 있습니다.

부문별 분석

2025년 컨택트 센터의 인력 관리(WFM) 시장에서 소프트웨어가 68.34%를 차지했으며, 서비스 수요가 증가하는 상황에서도 플랫폼이 여전히 지출의 주요 초점으로 남아 있음을 보여주고 있습니다. 직원 스케줄링 및 인력 최적화 부문은 소프트웨어 매출의 32.56%를 차지하며, 현재 매출 구성에서 가장 큰 비중을 차지하는 소프트웨어 하위 부문입니다. AI에 대한 투자를 통해 계획의 정확도를 높이고 관리자의 업무 가시성을 향상시키는 도구에 대한 구매자들의 관심이 높아짐에 따라, 인력 분석 및 예측, 그리고 근태 관리도 여전히 중요한 위치를 차지하고 있습니다. NICE사는 컨택 센터를 위한 AI 기반 일정 수립, 예측, 시뮬레이션을 핵심으로 하는 인력 관리 제품군을 제공하고 있으며, 이는 기업 구매자들이 현재 소프트웨어 분야에서 기대하는 기능의 충실도를 반영하고 있습니다. 또한, 컨택트 센터 업계의 인력 관리 소프트웨어 분야는 셀프 서비스 이용 및 일정 투명성 향상에 대한 수요가 증가함에 따라 혜택을 보고 있으며, 특히 하이브리드 근무 방식의 확산으로 인해 일정 변경이 빈번해진 것이 그 요인으로 꼽힙니다.

이 서비스는 컨택 센터 시장의 인력 관리(WFM) 분야에서 가장 빠르게 성장하고 있는 분야로, 2026년부터 2031년까지 연평균 성장률(CAGR) 12.34%를 나타낼 것으로 전망됩니다. 이는 소프트웨어 판매 후에도 구매자가 점점 더 많은 지원을 필요로 하고 있음을 보여줍니다. 현재 많은 도입 사례에서 기업이 플랫폼의 가치를 극대화하기 위해서는 설정, 통합, 거버넌스 구축 및 지속적인 최적화 지원이 필요합니다. 이는 운영 규칙이 복잡하고, 사내 WFM 전문 지식이 여러 클라이언트 프로그램에 분산되기 쉬운 대규모 BPO 환경에서 특히 중요한 과제로 대두되고 있습니다. Assembled사가 2025년 8월에 출시한 ‘Support Orchestration’은 단일 운영 뷰 내에서 AI 에이전트, 인력 팀, BPO 파트너 간의 균형을 조정하도록 설계되었으며, 소프트웨어 자체와 마찬가지로 도입 및 운영 설계가 중요시되는 서비스 중심의 환경을 시사하고 있습니다. 컨택트 센터 시장에서 워크포스 관리(WFM)가 성숙해짐에 따라, 강력한 도입 및 사후 지원 팀을 보유한 벤더는 라이선스 수익에만 의존하는 공급업체보다 더 많은 가치를 창출할 가능성이 높을 것으로 보입니다.

2025년 컨택트 센터 시장의 워크포스 관리(WFM) 부문에서 클라우드가 63.21%를 차지했으며, 이는 구매자들이 확장 가능한 제공 방식과 신속한 제품 업데이트를 선호한다는 사실을 뒷받침합니다. 클라우드의 매력은 운영상의 마찰이 줄어든다는 점뿐만이 아닙니다. 기존의 On-Premise 환경에 비해, WFM 플랫폼을 통해 컨택 센터, CRM, 인사 시스템에서 제공하는 실시간 데이터를 보다 손쉽게 활용할 수 있게 된다는 점에도 있습니다. NICE는 클라우드 기반 인력 관리를 예측, 스케줄링, 일일 관리, 옴니채널 제어를 단일 환경에서 지원하는 보다 광범위한 운영 스택의 일부로 자리매김하고 있습니다. 이 아키텍처가 중요한 이유는 현재 컨택 센터 시장의 인력 관리가 더욱 신속한 출시 주기와 보다 광범위한 고객 경험 기술 스택과의 긴밀한 통합에 의존하고 있기 때문입니다. 실용적인 관점에서 볼 때, 기업이 정기적인 AI 업데이트나 분산된 팀을 통한 보다 간편한 접근을 원할 경우, 클라우드는 기본 모델로 자리 잡고 있습니다.

하이브리드 모델은 2026년부터 2031년에 걸쳐 연평균 성장률(CAGR) 10.92%를 기록하며 성장하고 있으며, 시장에서 가장 빠르게 성장하는 모델로 자리매김하고 있습니다. 이러한 경향은 의료, 정부 기관, BFSI(은행 및 금융 및 보험) 분야의 구매자들이 가능한 한 클라우드 분석 및 계획 로직을 도입하면서도, 일부 데이터와 프로세스 제어를 유지하기 위해 여전히 On-Premise 인프라를 필요로 하고 있음을 반영합니다. Aspect사의 2025년 마이그레이션 지침에서는 중요도가 낮은 WEM 워크로드부터 시작하여, 그 후에 핵심 기능을 마이그레이션하는 단계적 접근 방식을 제시하고 있으며, 이는 하이브리드 환경이 단순한 과도기적 단계가 아니라 의도적인 아키텍처라는 점을 뒷받침하고 있습니다. 규제가 엄격한 환경에서는 On-Premise형 도구가 여전히 중요하지만, 남아 있는 전환 과제 중 가장 어려운 것은 오래된 감사 규정, 거버넌스 모델 및 내부 승인 체계가 쉽게 변경되지 않기 때문에 진행 속도가 가장 느린 경향이 있습니다. 따라서 컨택센터 분야 인력 관리(WFM) 분야에서는 양극화되는 경향이 나타나고 있습니다. 전반적인 도입률 면에서는 클라우드가 선두를 달리고 있는 반면, 규제와 운영상의 실용성이 모두 중요시되는 분야에서는 하이브리드 방식이 가장 강력한 성장세를 보이고 있습니다.

지역별 분석

2025년, 북미는 컨택센터 분야 인력 관리(WFM) 시장 점유율의 42.17%를 차지하며, 지역별로는 가장 큰 기여도를 보였습니다. 이 지역은 잘 갖춰진 컨택 센터 인프라, 확립된 구매 주기, 그리고 노동 규정 준수 및 업무상 책임성을 뒷받침하는 스케줄링 기록에 대한 높은 수요라는 이점을 누리고 있습니다. 미국은 대기업의 고객센터와 주요 공급업체가 집중되어 있어 여전히 핵심 시장으로서의 위상을 유지하고 있습니다. 한편, 캐나다에서는 이중 언어 서비스 요건이 점점 더 복잡해지고 있으며, 멕시코에서는 니어쇼어 서비스 사업의 확장을 통해 성장을 뒷받침하고 있습니다. 컨택센터 분야 인력 관리(WFM) 시장에서도 북미 수요는 운영 중인 업무를 중단하지 않고 레거시 환경을 현대화해야 할 필요성에 의해 형성되고 있으며, 그로 인해 대부분의 도입 사례에서 마이그레이션과 서비스 지원이 계속해서 핵심적인 위치를 차지하고 있습니다.

유럽은 2025년에 2위를 차지했으며, 이는 영국, 독일, 프랑스, 북유럽 국가들의 성숙한 컨택트 센터 운영에 힘입은 결과입니다. 이 지역에서는 인력 관리에 대한 수요가 높고 규제 환경이 더욱 엄격해지면서, 감사 가능성의 중요성이 커지는 한편, AI를 활용한 기능을 도입하는 데 더 많은 노력이 필요하게 됩니다. 따라서 서유럽의 구매자들은 데이터 처리에 대한 기대와 최신 예측·분석 도구에 대한 접근성을 모두 충족시킬 수 있는 하이브리드 아키텍처에 더 큰 관심을 보이고 있습니다. 이러한 추세는 컨택센터 분야 인력 관리(WFM) 시장에 있어 중요한 의미를 지닙니다. 왜냐하면, 컴플라이언스 심사가 조달 프로세스의 주요 요소가 될 경우, 지역적 인프라와 견고한 거버넌스를 갖춘 공급업체가 더 효과적으로 경쟁할 수 있기 때문입니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 2026년부터 2031년까지 연평균 성장률(CAGR) 12.14%를 나타낼 것으로 전망됩니다. 이는 BPO(비즈니스 프로세스 아웃소싱)의 수용 능력과 ‘클라우드 퍼스트’ 도입 관행이 도입 가속화를 뒷받침하고 있는 인도와 필리핀에서의 지속적인 확장이 주도하고 있습니다. 이 지역은 많은 시장에서 새로운 컨택 센터 시설이 구축되어 있다는 장점이 있어, 레거시 기술 부채가 많은 지역에 비해 플랫폼 교체나 클라우드 기반 구축이 용이합니다. 일본, 한국, 호주에서는 엔터프라이즈 수준 수요가 예상되며, 특히 호주의 경우 노동력 관련 규정 준수의 복잡성이 두드러지기 때문에 공급업체들은 보다 전문적인 계획 지원 체계를 구축해야 할 필요에 직면해 있습니다. Nimbus사는 이러한 환경에 대응하기 위해 소프트폰과의 통합 및 규정 준수를 중시하는 인력 관리를 핵심으로 하는 컨택 센터 플랫폼을 제공하고 있으며, 현지 노동법 및 운영 규정이 제품 설계에 어떤 영향을 미치는지를 반영하고 있습니다. 남미, 중동 및 아프리카는 매출 규모 면에서는 여전히 작지만, 니어쇼어 BPO 활동, 정부의 디지털화 프로그램, 서비스 사업의 확장이 컨택센터 분야 인력 관리(WFM) 분야에서 새로운 기회를 지속적으로 창출하고 있기 때문에 여전히 중요한 시장으로 남아 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the workforce management (WFM) in contact centers market was valued at USD 0.30 billion in 2025 and is estimated to grow from USD 0.34 billion in 2026 to USD 0.57 billion by 2031, at a CAGR of 10.89% during the forecast period (2026-2031).

This report is Segmented by Component (Software, and Services), Deployment Model (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (BFSI, IT and Telecom, Healthcare, Retail and E-Commerce, Travel and Hospitality, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Workforce Management (WFM) In Contact Centers Market Trends and Insights

AI-Driven Forecasting and Scheduling Adoption

AI-led forecasting has become a core buying requirement in the workforce management (WFM) in contact centers market, rather than an optional feature added late in a procurement cycle. NICE states that AI-based forecasting and scheduling in contact centers can narrow forecasting error from the typical legacy range of +-20% to +-5-8%, thereby directly affecting staffing costs and service performance. That improvement is also changing the day-to-day role of planning teams because the platform handles more of the routine model work, while analysts spend more time on interpretation, exception handling, and operational decisions. Verint linked its roadmap to Amazon Web Services and Amazon Bedrock for large language model workloads, and the company said customers may see up to 50% better forecasting accuracy over the next 24 months. This raises the standard for the wider workforce management market in contact centers, as buyers now expect tangible accuracy gains, not just broader feature lists. A 2026 peer-reviewed study in the International Journal of Intelligent Systems and Applications in Engineering also found that real-time demand prediction and natural-language access to operational data are moving workforce planning away from static planning toward continuous operational control.

Rising Cloud-Native CCaaS Migration

Cloud migration is one of the clearest growth drivers for the workforce management (WFM) in contact centers market, as WFM replacements often occur alongside broader contact center platform renewals. NICE describes cloud-based workforce management as a way to deliver AI-powered forecasting, scheduling, and intraday management with continuous updates, which matches the operating model enterprises now want from broader contact center software. Aspect's 2025 transition guidance also points to phased cloud adoption as a practical route for moving core WFM workloads away from legacy environments without disrupting day-to-day operations. That migration path matters because workforce management in the contact center market benefits when buyers replace outdated infrastructure and seek tighter integration between interaction data, staffing logic, and real-time automation. The March 2026 partnership between Aspect Software and Five9 demonstrated how vendors are tying WFM more closely to cloud interaction platforms through real-time agent-state data and automated intraday staffing adjustments. As more enterprises commit to cloud ecosystems, platform choice increasingly shapes the WFM pathway they follow throughout the deployment lifecycle.

Legacy Stack Integration Complexity

Legacy integration remains one of the most persistent barriers in the workforce management (WFM) in contact centers market because many large contact centers still rely on deeply customized connections between ACDs, WFM tools, QA platforms, and HR systems. Aspect's cloud transition guidance supports phased migration precisely because many organizations cannot move all workforce processes at once without risking disruption to scheduling, adherence, and reporting. NICE also positions its platform around broad integration with forecasting, scheduling, intraday management, and channel-level planning, which reflects how much buyers now care about unifying disconnected operational workflows. The difficulty is not only technical, because legacy rule sets often contain years of overtime policies, site practices, and compliance logic that need to be accurately rebuilt in the new system. That slows deal conversion and extends deployment work across the workforce management in contact centers market, especially in large enterprises with multiple sites and business units. Vendors with stronger connectors, migration services, and deeper configuration are therefore better placed when procurement teams see implementation risk as the main decision point.

Other drivers and restraints analyzed in the detailed report include:

- Omnichannel and Asynchronous Workload Complexity

- Agent Flexibility and Retention Prioritization

- Data Privacy and Algorithmic Governance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 68.34% of the workforce management (WFM) in contact centers market in 2025, underscoring that platforms remain the primary focus of spending even as service demand rises. Employee scheduling and labor optimization accounted for 32.56% of software revenue, making it the largest software sub-segment in the current revenue mix. Workforce analytics and forecasting, along with time and attendance management, also remain important, as AI investment is boosting buyer interest in tools that improve planning accuracy and give supervisors better operational visibility. NICE positions its workforce management suite around AI-powered scheduling, forecasting, and simulation for contact centers, which reflects the feature depth enterprise buyers now expect from the software layer. The software side of workforce management in the contact center industry also benefits from growing demand for self-service access and clearer schedule transparency, particularly as hybrid work has made schedule changes more frequent.

Services are the fastest-growing component of the workforce management (WFM) in contact centers market, with a 12.34% CAGR during 2026-2031, indicating that buyers increasingly need help after the software sale. Many deployments now require configuration, integration, governance setup, and ongoing optimization support before enterprises can realize the full value of the platform. This is especially relevant in large BPO environments where operational rules are complex and in-house WFM expertise is often stretched across several client programs. Assembled's August 2025 launch of Support Orchestration, built to balance AI agents, human teams, and BPO partners in a single operating view, points to a service-heavy environment where rollout and operating design matter as much as the software itself. As workforce management (WFM) in the contact center market matures, vendors with strong implementation and post-deployment teams are likely to capture more value than providers that rely solely on license revenue.

Cloud accounted for 63.21% of the workforce management (WFM) in contact centers market in 2025, underscoring buyers' preference for scalable delivery and faster product updates. The appeal of the cloud is not only lower operational friction; it also enables WFM platforms to more easily use real-time data from contact centers, CRM, and HR systems than in older on-premises environments. NICE presents cloud-based workforce management as part of a broader operating stack that supports forecasting, scheduling, intraday management, and omnichannel control in one environment. That architecture matters because workforce management in the contact center market now depends on faster release cycles and closer integration with the wider customer experience technology stack. In practical terms, cloud has become the default model where enterprises want regular AI updates and simpler access for distributed teams.

Hybrid is expanding at a 10.92% CAGR during 2026-2031, which makes it the fastest-growing deployment model in the market. The pattern reflects buyers in healthcare, government, and BFSI that still need some data or process controls to remain on local infrastructure while adopting cloud analytics and planning logic where possible. Aspect's 2025 migration guidance outlined a phased approach that begins with less critical WEM workloads before moving core functions later, supporting the idea that hybrid is a deliberate architecture rather than merely a temporary stage. On-premises tools remain relevant in highly regulated settings, but the hardest remaining migrations are also the slowest because old audit rules, governance models, and internal approval structures do not change quickly. The workforce management (WFM) in contact centers market, therefore, shows a split pattern: cloud leads overall adoption, while hybrid captures the strongest growth, where regulation and operational pragmatism both matter.

Geography Analysis

North America accounted for 42.17% of the workforce management (WFM) in contact centers market share in 2025, making it the largest regional contributor. The region benefits from dense contact center infrastructure, established buying cycles, and high demand for scheduling records that support labor compliance and operational accountability. The United States remains the anchor market because large enterprise contact centers and major vendors are concentrated there, while Canada adds complexity through bilingual service requirements, and Mexico supports growth through expanding nearshore service operations. Within the workforce management (WFM) market in the contact centers market, North American demand is also shaped by the need to modernize legacy environments without disrupting live operations, which keeps migration and service support central to most deployments.

Europe ranked second in 2025, supported by mature contact center operations across the United Kingdom, Germany, France, and the Nordic countries. The region combines strong demand for workforce control with a tighter regulatory environment, which raises the value of auditability while also extending deployment effort for AI-enabled functions. Western European buyers are therefore showing greater interest in hybrid architectures that can balance data handling expectations with access to newer forecasting and analytics tools. This pattern is meaningful for the workforce management (WFM) market in the contact centers market because vendors with regional infrastructure and stronger governance can compete more effectively when compliance reviews are a major part of procurement.

Asia-Pacific is the fastest-growing region, with a 12.14% CAGR during 2026-2031, led by continued expansion in India and the Philippines, where BPO capacity and cloud-first deployment practices support faster adoption. The region benefits from newer contact center estates across many markets, making platform replacement and cloud-based rollouts easier than in regions with greater legacy technical debt. Japan, South Korea, and Australia add enterprise-grade demand, with Australia standing out for workforce compliance complexity that has pushed vendors to build more specialized planning support. Nimbus positions its contact center platform around softphone integration and compliance-focused workforce management for this environment, reflecting how local labor and operating rules can shape product design.CLOUD. South America, the Middle East, and Africa remain smaller in revenue terms, but they remain relevant because nearshore BPO activity, government digitization programs, and expanding service operations continue to create new opportunities for workforce management (WFM) in contact centers market.

- NICE Ltd.

- Genesys Cloud Services, Inc.

- Verint Systems Inc.

- Calabrio, Inc.

- Alvaria, Inc.

- Five9, Inc.

- Talkdesk, Inc.

- Assembled, Inc.

- Playvox, Inc.

- Content Guru Inc.

- Peopleware GmbH

- Eleveo a.s.

- UJET, Inc.

- SESTEK A.S.

- JaMocha Tech Pvt. Ltd.

- nimbus Trading Co Pty Ltd.

- Nextiva, Inc.

- InVision AG

- Pipkins, Inc.

- ZOOM International s.r.o.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Cloud-Native CCaaS Migration

- 4.2.2 AI-Driven Forecasting and Scheduling Adoption

- 4.2.3 Omnichannel and Asynchronous Workload Complexity

- 4.2.4 Agent Flexibility and Retention Prioritization

- 4.2.5 Human and AI-Agent Capacity Planning Convergence

- 4.2.6 WFM as the Orchestration Layer Across CCaaS, CRM, HR, and QA

- 4.3 Market Restraints

- 4.3.1 Legacy Stack Integration Complexity

- 4.3.2 Data Privacy and Algorithmic Governance Burden

- 4.3.3 Fragmented Scheduling Rules Across In-House and Outsourced Teams

- 4.3.4 Agent Pushback Against Intraday Automation and Perceived Fairness Risks

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Employee Scheduling and Labor Optimization

- 5.1.1.2 Time and Attendance Management

- 5.1.1.3 Workforce Analytics and Forecasting

- 5.1.1.4 Leave and Absence Management

- 5.1.1.5 Task and Execution Management

- 5.1.1.6 Employee Self-service and Communication

- 5.1.2 Services

- 5.1.1 Software

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By End-user Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 IT and Telecom

- 5.4.3 Healthcare

- 5.4.4 Retail and E-commerce

- 5.4.5 Travel and Hospitality

- 5.4.6 Government and Public Sector

- 5.4.7 Outsourced Contact Centers and BPOs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Southeast Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 NICE Ltd.

- 6.4.2 Genesys Cloud Services, Inc.

- 6.4.3 Verint Systems Inc.

- 6.4.4 Calabrio, Inc.

- 6.4.5 Alvaria, Inc.

- 6.4.6 Five9, Inc.

- 6.4.7 Talkdesk, Inc.

- 6.4.8 Assembled, Inc.

- 6.4.9 Playvox, Inc.

- 6.4.10 Content Guru Inc.

- 6.4.11 Peopleware GmbH

- 6.4.12 Eleveo a.s.

- 6.4.13 UJET, Inc.

- 6.4.14 SESTEK A.S.

- 6.4.15 JaMocha Tech Pvt. Ltd.

- 6.4.16 nimbus Trading Co Pty Ltd.

- 6.4.17 Nextiva, Inc.

- 6.4.18 InVision AG

- 6.4.19 Pipkins, Inc.

- 6.4.20 ZOOM International s.r.o.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment