|

시장보고서

상품코드

2065551

제약 전사적 자원 계획(ERP) : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Pharmaceutical Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

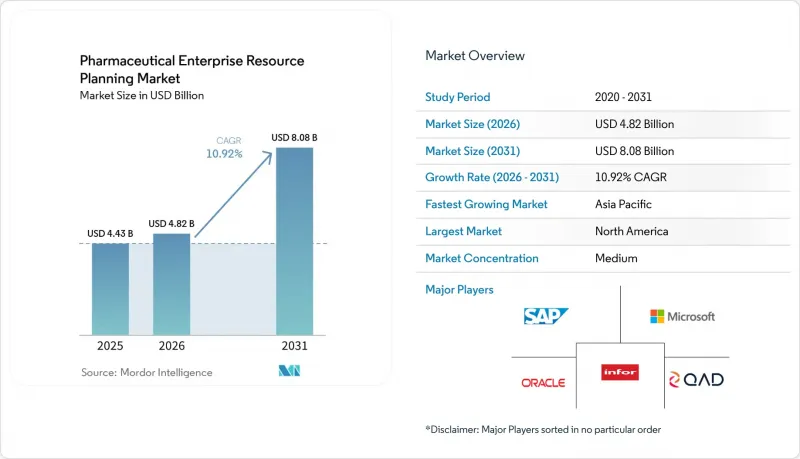

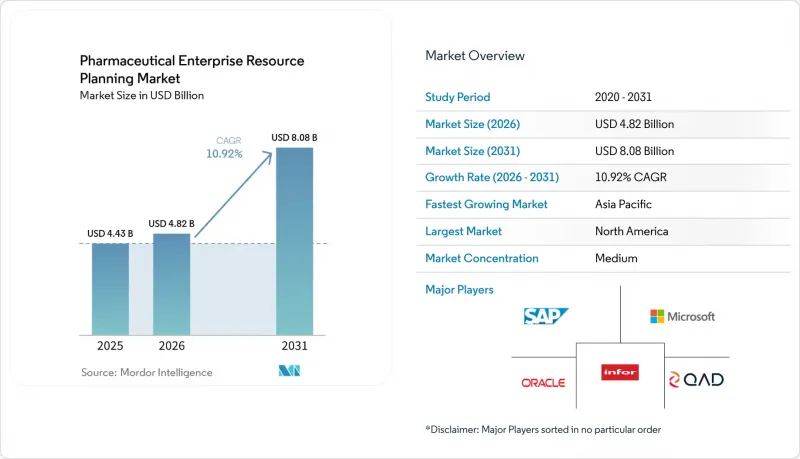

Mordor Intelligence에 의하면, 제약 전사적 자원 계획(ERP) 시장 규모는 2025년 44억 3,000만 달러로 평가되었습니다. 2026년 48억 2,000만 달러에서 2031년까지 80억 8,000만 달러에 이를 것으로 예상되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 10.92%를 나타낼 전망입니다.

본 보고서는 도입 방식(클라우드 기반 ERP, On-Premise형 ERP, 하이브리드형 ERP), 모듈(생산 관리, 품질·규제 준수 관리, 공급망 관리 등), 조직 규모(대기업, 중소기업), 최종 사용자(제약 기업, CMO 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 제약 전사적 자원 계획(ERP) 시장 동향 및 인사이트

클라우드 기반 인증 ERP 플랫폼에 대한 수요

제약 기업들은 설비 투자를 줄이고, 배치의 가시성을 실시간으로 확보하며, 검증 기간을 단축하기 위해 워크로드를 클라우드로 이전하고 있습니다. SAP, Oracle, Microsoft는 GxP 문서를 통합한 사전 검증 완료된 생명과학용 제품군을 도입하고 있으며, 이를 통해 기업은 On-Premise 환경을 유지하지 않고도 21 CFR Part 11을 준수할 수 있게 됩니다. CMO(의약품 수탁 제조 기관)는 의뢰사의 데이터를 분리하면서도 공통의 품질 관리 모듈을 공유하는 멀티테넌트형 클라우드 아키텍처를 선호하며, 이를 통해 신속한 도입과 전자 배치 기록의 표준화가 가능해집니다. 그러나 중국과 러시아의 데이터 거주 규정에 따라, 퍼블릭 클라우드상의 재무 시스템과 On-Premise 제조 실행 시스템을 결합한 하이브리드 구축을 선택할 수밖에 없습니다.

세계적인 시리얼화 마감 기한이 다가오고 있습니다.

미국의 ‘의약품 공급망 보안법(Drug Supply Chain Security Act)’은 2025년에 단계적 도입을 완료하며, 제조업체, 도매업체 및 조제업체에 대해 단위별 추적 및 추적 가능성 기능을 ERP 시스템에 통합할 것을 의무화했습니다. 유럽연합(EU)의 ‘위조 의약품 지침(Falsified Medicines Directive)’이 이탈리아와 그리스에 2027년까지의 유예 기간을 허용함에 따라, 모듈식이며 국가별로 특화된 템플릿이 유리한 ‘2단계 환경’이 조성되고 있습니다. 일련번호 부여를 통해 변조가 불가능한 감사 추적을 제공하고, 각국의 리포지토리(REUTERS.COM)와의 실시간 검증을 가능하게 하는 블록체인 기반 ERP 통합에 대한 수요가 높아지고 있습니다.

중소기업의 높은 CSV 비용

중소기업의 경우, 컴퓨터 시스템 검증(CSV) 비용이 ERP 프로젝트 예산의 최대 30%를 차지할 수 있으며, 본격적인 가동 시작일이 최대 1년 늦어질 수도 있습니다. 외부 컨설턴트의 시간당 단가는 1시간당 150-250달러로, 제한된 IT 예산에 부담을 주고 있습니다. 공급업체는 검증 문서를 공유하고 있지만, 규제 당국은 규정 준수에 대한 최종 책임은 제조업체에 있다고 주장하고 있습니다. 스폰서마다 다른 요건을 충족해야 하는 수탁 제조업체의 경우, 그 부담은 더욱 커집니다.

부문별 분석

2025년에는 클라우드 기반 솔루션이 매출의 62%를 차지했으며, 제약 전사적 자원 계획(ERP) 시장에서 이 점유율은 2031년까지 연평균 성장률(CAGR) 11.80%로 성장할 전망입니다. 하이브리드 모델은 환자 데이터 마이그레이션을 제한하는 법적 규제를 준수하면서도, GxP 적용 대상이 아닌 기능에 있어 클라우드의 확장성을 활용할 수 있게 해줍니다. 2031년까지 제약 업계 및 클라우드 도입용 전사적 자원 계획(ERP) 시장 규모가 신규 투자의 대부분을 차지할 것으로 예측됩니다. 조기 도입 기업들로부터는 On-Premise형 제품군에서 전환한 후 검증 비용이 대폭 절감되었다는 보고가 있습니다. 멀티테넌트형 클라우드를 통해 스폰서별 분리 및 신속한 온보딩이 가능해짐에 따라, 수탁 제조 조직(CMO)이 도입을 주도하고 있습니다.

데이터 현지화 규제가 여전히 엄격한 중국이나 러시아에서는 On-Premise 도입이 여전히 뿌리 깊게 남아 있습니다. 레거시 설비를 갖춘 시설의 경우 OPC-UA 연결 기능이 부족하기 때문에 퍼블릭 클라우드로의 전환 시 생산 라인 전체에 대한 재검증이 필요해져 막대한 비용이 발생할 가능성이 있습니다. 하이브리드 아키텍처를 통해 제조업체는 재무 및 인사 업무를 클라우드 서비스로 이전하는 동시에, 제조 실행 시스템을 On-Premise에서 유지할 수 있게 됩니다. 감사 추적 기록 대조를 자동화하는 벤더는 CSV 주기를 18개월에서 6개월로 단축함으로써, 규정 준수를 중시하는 기업들의 제약 시장 내 도입을 가속화하고 있습니다.

품질 및 규정 준수는 2025년 매출의 28.40%를 차지했으며, 이는 규제에 대한 중점을 반영하고 있습니다. 제약 업계 전사적 자원 계획(ERP) 시장 점유율에서 이 비율은 모든 주요 도입의 기반이 되고 있으며, 특히 DSCSA 및 EU FMD가 일련번호 부여를 요구하는 분야에서 두드러지게 나타납니다. 제조 관리 모듈은 일정 관리, 조달, 유지보수를 조정하여 여러 거점에 걸친 네트워크 전체에서 프로세스의 가시성을 제공합니다.

연구개발 모듈은 혁신적인 기업들이 제제 설계 및 임상시험 워크플로우에 AI를 통합함에 따라 연평균 성장률(CAGR) 12.60%를 나타낼 것으로 예측됩니다. 제약 전사적 자원 계획(ERP) 시장 내 연구 개발 도구 시장은 품질 관리 시장에 비하면 여전히 규모는 작지만, AI를 통해 실험 주기가 단축됨에 따라 가장 빠르게 성장하고 있습니다. 공급망 모듈은 위조가 불가능한 제품 출처 정보를 생성하는 블록체인의 시범 도입으로 인한 혜택을 누리고 있으며, 인사 관리 도구는 직원의 교육 기록을 GxP 업무와 연계함으로써 중요한 업무를 자격을 갖춘 직원만이 수행할 수 있도록 하고 있습니다.

지역별 분석

북미는 엄격한 DSCSA 규제와 혁신 지향적인 제조 인프라에 힘입어 2025년 매출의 34.90%를 차지하며 1위를 차지했습니다. 미국의 제약 전사적 자원 계획(ERP) 시장 규모는 초기 클라우드 검증 시범 프로젝트와 광범위한 AI 실험의 혜택을 받고 있습니다. 캐나다는 미국과의 지리적 근접성을 활용하여 생물학적 제제의 수탁 제조 거점으로서의 입지를 확고히 하고 있으며, 국경을 넘는 배치의 가시화가 필수적입니다.

유럽은 2위 자리를 유지하고 있습니다. EU의 위조 의약품 지침에서는 일련번호 부여가 의무화되어 있으며, 기업의 지속가능성 보고 지침에서는 스코프 3 탄소 회계가 의무화되어 있습니다. 이러한 규제 때문에 포인트 솔루션보다 통합형 ERP 제품군이 더 선호되고 있습니다. GDPR(EU 개인정보보호규정)에 따른 데이터 소재지 요건에 따라, 환자 데이터는 로컬에 호스팅하고 재무 데이터는 세계 클라우드로 이전하는 하이브리드 아키텍처가 권장됩니다.

아시아태평양은 가장 성장세가 두드러진 지역으로, 2031년까지 연평균 10.20%의 성장률이 예상됩니다. 인도의 20억 달러 규모의 인센티브 정책에 힘입어, 현지 기업들은 FDA 및 EMA의 규정 준수가 요구되는 수출 시장으로 진출하고 있습니다. 중국에서 15억 달러 규모의 인프라 확충과 중앙집권적인 조달 개혁에 힘입어, 국내 CMO들은 국제적인 GxP 기준의 도입을 추진하고 있습니다. 일본은 인력 부족을 해소하기 위해 AI를 활용한 배치 릴리스 분석의 시범 운영을 진행하고 있습니다.

남미는 거시경제의 변동으로 인해 성장세가 둔화되고 있지만, 브라질과 아르헨티나는 ERP 현대화에 선택적으로 투자하고 있습니다. 중동 및 아프리카은 여전히 개발도상국이지만, 사우디아라비아와 아랍에미리트가 수입 의존도를 낮추기 위해 현지 의약품 생산 체계를 구축하고 있어 장래성이 기대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the pharmaceutical eRP market size is projected to expand from USD 4.43 billion in 2025 and USD 4.82 billion in 2026 to USD 8.08 billion by 2031, registering a CAGR of 10.92% between 2026 and 2031.

This report is Segmented by Deployment Mode (Cloud-Based ERP, On-Premise ERP, and Hybrid ERP), Module (Manufacturing Management, Quality and Compliance Management, Supply Chain Management, and More), Organization Size (Large Enterprises, Small and Medium Enterprises), End User (Pharmaceutical Manufacturers, Cmos, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Pharmaceutical Enterprise Resource Planning Market Trends and Insights

Demand for Cloud-Based Validated ERP Platforms

Pharmaceutical manufacturers are moving workloads to the cloud to reduce capital expenditure, unlock real-time batch visibility, and cut validation timelines. SAP, Oracle, and Microsoft introduced pre-validated life sciences suites that embed GxP documentation, enabling companies to comply with 21 CFR Part 11 without maintaining on-premises environments. Contract manufacturing organizations prefer multi-tenant cloud architectures that isolate sponsor data yet share common quality modules, enabling faster onboarding and harmonized electronic batch records. However, data-residency rules in China and Russia force hybrid deployments that blend public-cloud financials with on-premise manufacturing execution systems.

Tightening Global Serialization Deadlines

The United States Drug Supply Chain Security Act completed its phased rollout in 2025, requiring manufacturers, wholesalers, and dispensers to integrate unit-level track-and-trace into their ERP systems. The European Union Falsified Medicines Directive granted Italy and Greece extensions until 2027, creating a two-speed environment that favors modular, country-specific templates. Serialization drives demand for blockchain-enabled ERP integrations that provide immutable audit trails and real-time verification against national repositories REUTERS.COM.

High CSV Costs for SMEs

Computer system validation can consume up to 30% of an ERP project budget for small and medium enterprises, extending go-live dates by up to a year. External consultants bill USD 150-250 per hour, straining limited IT budgets. Vendors offer shared validation documentation, yet regulators insist that manufacturers retain ultimate responsibility for compliance. The burden is heavier for contract manufacturers that must satisfy divergent sponsor requirements.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Contract Manufacturing Organizations

- AI-Enabled Predictive Quality and Batch-Release Analytics

- Shortage of Pharma-Savvy ERP Implementation Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based solutions accounted for 62% of revenue in 2025, and this share of the Pharmaceutical ERP market is set to grow at a 11.80% CAGR through 2031. Hybrid models satisfy jurisdictions that restrict patient data movement while unlocking cloud scalability for non-GxP functions. The Pharmaceutical ERP market size for cloud deployments is projected to command the majority of new spend by 2031. Early adopters report significantly lower validation costs after switching from on-premises suites. Contract manufacturing organizations dominate uptake because multi-tenant clouds enable sponsor segregation and rapid onboarding.

On-premises deployments persist in China and Russia, where data localization laws remain strict. Facilities with legacy equipment lack OPC-UA connectivity, so migrating to the public cloud can trigger costly re-validation of entire production lines. Hybrid architectures let manufacturers migrate financials and human resources to cloud services while retaining manufacturing execution on-site. Vendors that automate audit-trail reconciliation shorten CSV cycles from 18 months to six months, accelerating Pharmaceutical ERP market adoption among compliance-focused firms.

Quality and compliance accounted for 28.40% of 2025 revenue, reflecting the regulatory focus. This slice of the Pharmaceutical ERP market share underpins every major deployment, especially where DSCSA and EU FMD demand serialization. Manufacturing management modules orchestrate scheduling, procurement, and maintenance, offering process visibility across multi-site networks.

Research and development modules are expected to grow at a 12.60% CAGR as innovators integrate AI into formulation design and clinical-trial workflows. The Pharmaceutical ERP market for Research and Development tools, while still smaller than the quality management market, is growing fastest because AI shortens experimentation cycles. Supply chain modules benefit from blockchain pilots that create immutable product provenance, and human resources tools map employee training records to GxP tasks, ensuring only qualified staff perform critical operations.

Geography Analysis

North America led with 34.90% of 2025 revenue, driven by stringent DSCSA rules and an innovation-oriented manufacturing base. The Pharmaceutical ERP market size in the United States benefits from early cloud validation pilots and broad AI experimentation. Canada leverages proximity to the United States to position itself as a biologics contract manufacturing hub, making cross-border batch visibility a must-have.

Europe maintains second position. The EU Falsified Medicines Directive mandates serialization, and the Corporate Sustainability Reporting Directive compels Scope 3 carbon accounting. These rules favor integrated ERP suites over point solutions. Data-residency considerations under GDPR encourage hybrid architectures that host patient data locally and move financial data to global clouds.

Asia-Pacific is the fastest-growing region, expected to advance at 10.20% through 2031. India's USD 2 billion incentive propels local firms into export markets that demand FDA and EMA compliance. China's USD 1.5 billion infrastructure push and centralized procurement reforms motivate domestic CMOs to embrace international GxP standards. Japan pilots AI batch-release analytics to offset labor shortages.

South America is growing more slowly due to macroeconomic volatility, though Brazil and Argentina are investing selectively in ERP modernization. The Middle East and Africa remain nascent but promising, as Saudi Arabia and the United Arab Emirates develop local pharma manufacturing to reduce reliance on imports.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor, Inc.

- QAD Inc.

- BatchMaster Software Pvt. Ltd.

- Aptean, Inc.

- Sage Group plc

- Epicor Software Corporation

- SYSPRO (Pty) Ltd.

- IFS AB

- Acumatica, Inc.

- Oracle NetSuite LLC

- Slingshot Enterprise Business Systems, Inc.

- RxERP LLC

- Dexciss Technology Private Limited

- Blue Link Associates Limited

- Deacom, LLC

- Plex Systems, Inc.

- Workday, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition * Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for Cloud-Based Validated ERP Platforms

- 4.2.2 Tightening Global Serialization Deadlines (DSCSA, EU FMD)

- 4.2.3 Rapid Expansion of Contract Manufacturing Organizations

- 4.2.4 AI-Enabled Predictive Quality and Batch-Release Analytics

- 4.2.5 Government Incentives for Digital Pharma Plants

- 4.2.6 Growing Need for End-to-End ESG and Carbon Accounting

- 4.3 Market Restraints

- 4.3.1 High CSV (Computer System Validation) Costs for SMEs

- 4.3.2 Shortage of Pharma-Savvy ERP Implementation Talent

- 4.3.3 Cyber-Security and Data-Residency Concerns in Public Cloud

- 4.3.4 Legacy MES/LIMS Integration Complexities

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Intensity of Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Threat of Substitutes

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Bargaining Power of Buyers

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based ERP

- 5.1.2 On-Premise ERP

- 5.1.3 Hybrid ERP

- 5.2 By Module

- 5.2.1 Manufacturing Management

- 5.2.2 Quality and Compliance Management

- 5.2.3 Supply Chain Management

- 5.2.4 Financial Management

- 5.2.5 Sales and Marketing

- 5.2.6 Human Resources Management

- 5.2.7 Other Modules

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End User

- 5.4.1 Pharmaceutical Manufacturers

- 5.4.2 Contract Manufacturing Organizations

- 5.4.3 Pharmaceutical Distributors

- 5.4.4 Biotechnology Companies

- 5.4.5 Contract Research Organizations

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor, Inc.

- 6.4.5 QAD Inc.

- 6.4.6 BatchMaster Software Pvt. Ltd.

- 6.4.7 Aptean, Inc.

- 6.4.8 Sage Group plc

- 6.4.9 Epicor Software Corporation

- 6.4.10 SYSPRO (Pty) Ltd.

- 6.4.11 IFS AB

- 6.4.12 Acumatica, Inc.

- 6.4.13 Oracle NetSuite LLC

- 6.4.14 Slingshot Enterprise Business Systems, Inc.

- 6.4.15 RxERP LLC

- 6.4.16 Dexciss Technology Private Limited

- 6.4.17 Blue Link Associates Limited

- 6.4.18 Deacom, LLC

- 6.4.19 Plex Systems, Inc.

- 6.4.20 Workday, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment