|

시장보고서

상품코드

2065605

미국의 인비저블 치열교정 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Invisible Orthodontics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

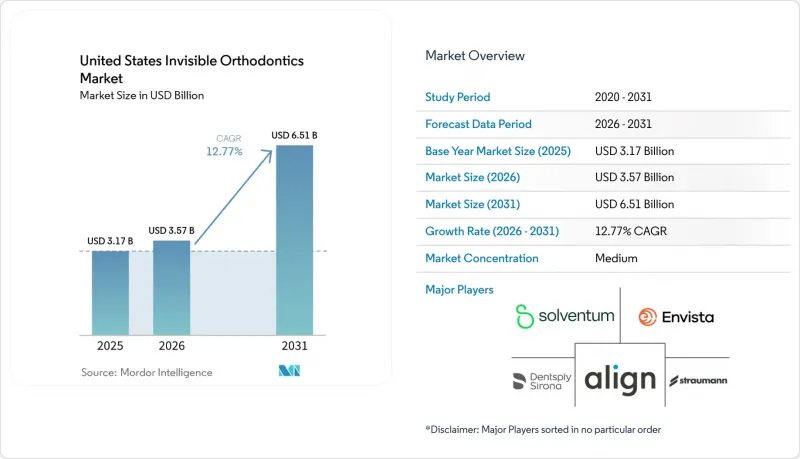

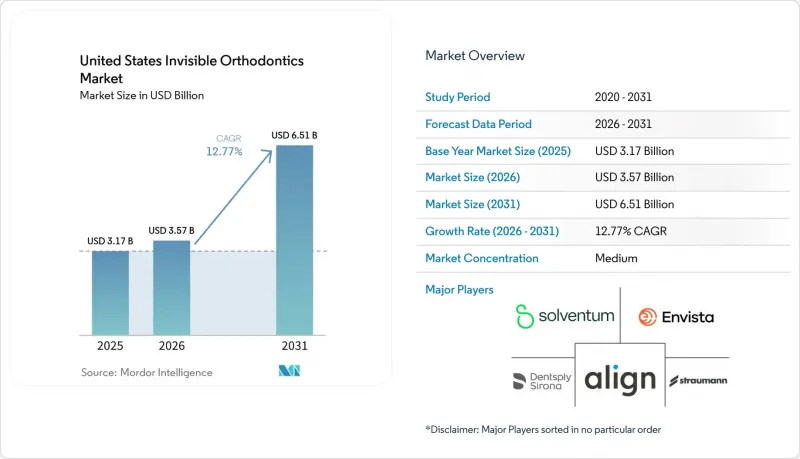

Mordor Intelligence에 의하면, 미국 인비저블 치열교정 시장 규모는 2025년에 31억 7,000만 달러로 평가되었고 2026년 35억 7,000만 달러에서 2031년까지 65억 1,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 12.77%를 나타낼 전망입니다.

본 보고서는 제품별(클리어 얼라이너, 세라믹 브라켓, 설측 교정 장치, 리테이너), 소재별(폴리우레탄 필름, PETG, 폴리카보네이트), 연령대별(성인, 10대, 소아), 진료 환경별(단독 진료소, 그룹 진료소/DSO, 병원), 제공업체별(치열교정의사, 일반 치과의사), 판매 채널별(오프라인, 온라인)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 인비저블 치열교정 시장 동향과 인사이트

성인의 부정교합으로 인한 불편함과 심미성을 중시하는 수요

미국의 인비저블 치열교정 시장에서 잠재적 환자 수는 현재의 치료 건수를 훨씬 웃돌고 있습니다. AAO(미국 치열교정의사협회)의 추산에 따르면, 2024년에는 미국 내 AAO 회원들을 통해 191만 명의 성인이 치료를 받은 것으로 나타났으며, 이는 성인 대상 치료가 이미 대규모이자 활발한 수익원이 되고 있음을 뒷받침하고 있습니다. 또한, AAO의 ‘2024년 치열교정 업계 동향 소비자 조사’에 따르면, 성인 교정 환자의 64%는 치열교정 전문의가, 22%는 일반 치과의사가, 14%는 통신 판매 채널이 담당하고 있으며, 이는 감독 하에 이루어지는 치료가 여전히 강점임을 보여줍니다. 직장인들은 편의성이나 일정의 유연성, 자기 부담에 대한 의지뿐만 아니라 외모에 대한 우려도 중요하게 여기게 되면서, 눈에 잘 띄지 않는 치료법을 선택하는 경향이 강해지고 있습니다. 또한, 치료 시작 건수의 상당 부분은 리테이너 착용을 중단한 후 다시 치료를 받기 위해 돌아온 재발 환자들로부터 발생하고 있습니다. 이러한 꾸준한 환자층은 신규 환자 확보가 어려워진 상황에서도, 미국의 인비저블 치열교정 시장에서 안정적인 진료 건수를 유지하는 데 기여하고 있습니다.

AI를 활용한 치료 계획, 구강 내 스캔 및 디지털 워크플로우

인공지능(AI)은 교정 치료에서 가장 시간이 많이 소요되는 과정 중 하나인 치료 계획 수립 및 확인에 걸리는 시간을 단축하고 있습니다. Align Technology사에 따르면, ‘ClinCheck Live Plan’은 해당 증례에 대해 의사가 즉시 사용할 수 있는 초기 치료 계획을 최단 15분 만에 생성할 수 있다고 합니다. 이를 통해 스캔 데이터 수집부터 임상의의 확인까지 걸리는 시간이 단축됩니다. 2026년 5월 『PLOS One』지에 게재된 무작위 대조 시험에서는 앵글 분류 I급 부정교합을 가진 환자 140명을 대상으로, AI를 활용한 디지털 워크플로가 기존의 고정식 교정 장치에 비해 PAR 점수 감소 측면에서 우수한 결과를 보였습니다. 설정 과정을 신속하게 진행함으로써, 사례당 소요되는 부수적인 노력이 줄어듭니다. 이는 기술자나 코디네이터의 인원을 그만큼 늘리지 않고도 가동률 향상을 목표로 하는 여러 거점을 보유한 그룹에게 있어 가장 중요한 점입니다. 또한, 디지털 워크플로는 지점 간 일관성을 높이기 때문에 재현 가능한 치료 프로토콜을 원하는 DSO(치과 서비스 조직)에 유용합니다. 미국의 눈에 잘 띄지 않는 치열교정 시장에서 우수한 소프트웨어, 스캐너와의 통합, 품질 관리 시스템을 갖춘 업체들이 장치 그 자체를 넘어선 경쟁 우위를 확보해 가고 있습니다.

높은 본인 부담금과 성인 대상 보험 적용 범위의 미비

미국의 인비저블 치열교정 시장에서 합리적인 가격은 여전히 가장 뚜렷한 수요 제약 요인으로 작용하고 있습니다. CMS(미국 의료보험 및 의료보조 서비스 센터)는 각 주가 2027년 EHB(필수 건강 혜택) 벤치마크 플랜에 성인 치과 서비스를 포함하는 것을 허용하는 규정을 최종 확정했으나, 치열교정 보장은 벤치마크 범주에 명시적으로 추가되지 않았기 때문에 향후 혜택 설계에 대해서는 여전히 불확실성이 남아 있습니다. 투명 교정 치료의 본인 부담금은 여전히 보통 3,000-8,000달러에 달하며, 이는 많은 치과 보충 보험이 제공하는 보상 한도를 훨씬 초과합니다. 교정 치료의 평생 상한액이 1,000-2,000달러이므로, 치료비의 대부분은 환자가 부담하게 되며, 그 결과 임상적 필요성보다 자금 조달이 결정적인 요인이 되는 경우가 종종 있습니다. 이러한 비용 구조로 인해 대상층은 훨씬 더 광범위함에도 불구하고, 이용은 소득이나 신용도가 높은 가구에 편중되어 있습니다. 제3자를 통한 대출이나 치과 병원의 자체 할부 계획은 그 격차를 어느 정도 해소하는 데 도움이 되지만, 가격 장벽을 완전히 없애지는 못하며, 환자와 치과 병원 모두에게 상환 위험을 높일 가능성도 있습니다.

부문별 분석

2025년, 클리어 얼라이너는 미국의 인비저블 교정 시장 점유율의 86.31%를 차지했으며, 이 부문은 탈부착이 가능한 투명 교정 장치에 집중된 양상을 유지했습니다. Align Technology사는 2025년 투명 교정기 매출이 32억 달러, 전 세계 출하 건수가 260만 건이었습니다고 보고했으며, 이는 업계를 선도하는 플랫폼의 규모와 성숙도를 입증하는 것입니다. 2026년 1분기, 알라인사는 68만 5,700케이스를 출하하여 전년 동기 대비 6.7% 증가했으나, 북미의 출하량은 보합세를 보였습니다. 이러한 경향은 미국 내 시장 확대가 단순한 네트워크 확장보다는 의료 제공업체의 활용도 심화 및 사례 확보율 향상에 중점을 두고 있음을 보여줍니다. 미국의 눈에 잘 띄지 않는 치열교정 시장 전체에서 클리어 얼라이너는 환자의 기대와 경쟁적 위치를 모두 정의하는 존재이기 때문에 여전히 이 시장의 주역으로 자리 잡고 있습니다.

세라믹 브라켓 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 15.38%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 제품 하위 부문이 될 것입니다. 임상의가 보다 직접적인 토크 제어가 필요한 경우나, 얼라이너의 예측 가능한 성능 범위를 벗어난 수준의 힘이 필요한 증례에서 세라믹 브라켓의 역할은 여전히 중요합니다. Ormco사는 AAO 2026에서 더 많은 교정용 브라켓 시스템에 디지털 본딩을 확대 적용했습니다. 이는 브라켓 제조업체들이 얼라이너 시장에 자리를 내어주는 것이 아니라, 워크플로우의 현대화를 추진하고 있음을 보여줍니다. 설측 교정 장치는 인비저블 효과를 극대화하고자 하며, 더 높은 비용과 제한된 치료 기관 선택지를 감수할 수 있는 성인들에게 있어, 규모는 작지만 여전히 프리미엄한 선택지로 자리 잡고 있습니다. 리테이너 역시 전략적으로 중요한 위치를 계속 차지하고 있습니다. 왜냐하면, 치료가 완료된 모든 사례가 치료 후의 재구매 수익으로 이어질 가능성이 있으며, 그로 인해 제품의 평생 가치는 초기 치료 수익만으로는 추정할 수 없을 정도로 높아지기 때문입니다.

2025년에는 폴리우레탄 및 코폴리에스테르로 제작된 다층 필름이 매출의 75.24%를 차지했으며, 이로 인해 미국 투명 교정 시장의 소재 구성은 고성능 다층 필름에 편중된 상태가 유지되었습니다. Align Technology의 SmartTrack 플랫폼은 이러한 기준을 확립하는 데 기여하고 있으며, 관련 다층 폴리머 시트의 구조는 여전히 특허로 보호받고 있습니다. 『Orthodontics and Craniofacial Research』지에 게재된 연구에 따르면, PETG와 열가소성 폴리우레탄은 치아 부위나 얼라이너의 두께에 따라 강성 특성이 다르게 나타난다는 사실이 밝혀졌습니다. 이 증거는 재료 선정이 단순한 조달상의 선택이 아니라, 치료 효과에 관한 판단이라는 견해를 뒷받침하고 있습니다. 그 결과, 확립된 다층 시스템은 미국의 인비저블 치열교정 시장에서 여전히 임상적 우위를 유지하고 있습니다.

PETG는 가성비가 뛰어난 입지를 구축하고자 하는 신생 브랜드들의 사용 확대에 힘입어, 2026년부터 2031년까지 연평균 성장률(CAGR) 15.52%를 기록하며 성장할 것으로 전망됩니다. PETG는 투명성, 가공성, 비용 면에서 실용적인 균형을 제공하며, 완전히 저가 시장으로 전환하지 않으면서도 접근성을 확대하고자 하는 브랜드에게 매력적인 선택지가 되고 있습니다. 직접 인쇄용 수지 재료도 논의의 대상이 되기 시작했습니다. 이는 향후 열성형 공정을 생략하고, 치과 내에서 주문형 생산을 가능하게 할 가능성이 있기 때문입니다. 2025년 10월, ‘Primeprint Direct Aligner’가 K250739로 FDA 승인을 획득했고, 2026년에 임상 평가가 실시됨에 따라 이 개념은 실용화에 한 걸음 더 가까워졌습니다. 그렇긴 하지만, 아직 초기 단계입니다. 따라서, 미국의 인비저블 치열교정 업계는 최상층에 프리미엄 다층 필름, 중간층에 PETG, 그리고 향후 병원 내 생산 옵션으로 인쇄용 수지를 배치한 다층 소재 구조로 전환되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the united states invisible orthodontics market size was valued at USD 3.17 billion in 2025 and is estimated to grow from USD 3.57 billion in 2026 to reach USD 6.51 billion by 2031, at a CAGR of 12.77% during the forecast period (2026-2031).

This report is Segmented by Product (Clear Aligners, Ceramic Braces, Lingual Braces, Retainers), Material (Polyurethane Films, PETG, Polycarbonate), Age Group (Adults, Teens, Children), Care Setting (Standalone, Group Practices/DSOs, Hospitals), Provider Type (Orthodontists, General Dentists), and Sales Channel (Offline, Online). The Market Forecasts are Provided in Terms of Value (USD).

United States Invisible Orthodontics Market Trends and Insights

Adult Malocclusion Burden and Aesthetics-Led Demand

The addressable patient base in the United States invisible orthodontics market is much larger than current treatment volumes. The AAO estimated 1.91 million adults were treated by AAO members in the United States in 2024, which confirms that adult care is already a large and active revenue pool. The AAO's 2024 Orthodontic Landscape Consumer Study also showed that orthodontists treated 64% of adult orthodontic patients, dentists treated 22%, and mail-order channels treated 14%, which points to continued strength in supervised care. Working adults are increasingly choosing less visible treatment, because appearance concerns now sit alongside convenience, schedule flexibility, and willingness to self-finance. A meaningful share of case starts is also coming from relapse patients who stopped retainer wear and later returned to treatment. That recurring pool supports steady case replenishment inside the United States invisible orthodontics market even when first-time patient acquisition becomes harder.

AI Planning, Intraoral Scanning, and Digital Workflows

Artificial intelligence is reducing one of the slowest steps in orthodontic care, which is the time required to build and review case setups. Align Technology stated that ClinCheck Live Plan can generate initial doctor-ready plans in as little as 15 minutes for eligible cases, which shortens the gap between scan capture and clinician review. A randomized controlled trial published in PLOS One in May 2026 found superior PAR score reductions for AI-assisted digital workflows versus conventional fixed appliances in 140 patients with Angle Class I malocclusion. Faster setup reduces the marginal labor required per case, and that matters most for multi-location groups trying to raise utilization without adding equal numbers of technicians and coordinators. Digital workflows also improve consistency across locations, which is valuable for DSOs that want repeatable treatment protocols. In the United States invisible orthodontics market, vendors with stronger software, scanner integration, and quality control are gaining an advantage that extends beyond the appliance itself.

High Out-of-Pocket Cost and Adult Coverage Gaps

Affordability remains the clearest demand constraint in the United States invisible orthodontics market. CMS finalized a rule that allows states to include adult dental services in 2027 EHB benchmark plans, but orthodontic coverage was not explicitly added to the benchmark categories, which leaves real uncertainty around future benefit design. Clear aligner treatment still routinely costs USD 3,000 to USD 8,000 out of pocket, which is far above the support offered by many supplemental dental plans. Lifetime orthodontic maximums of USD 1,000 to USD 2,000 leave most of the treatment bill with the patient, so financing often becomes the deciding factor rather than clinical need. That cost profile skews utilization toward households with stronger income and credit access, even though the addressable pool is much wider. Third-party financing and in-house installment plans help close some of the gap, but they do not remove the price barrier and can add repayment risk for both patients and practices.

Other drivers and restraints analyzed in the detailed report include:

- Hybrid Remote Monitoring Improves Case Throughput

- DSO and Group-Practice Scaling Accelerates Aligner Penetration

- Tighter Scrutiny of Mail-Order Aligners and In-Person Exam Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clear aligners held 86.31% of the United States invisible orthodontics market share in 2025, which kept the category tightly centered on removable transparent appliances. Align Technology reported USD 3.2 billion in clear aligner revenue in 2025 and 2.6 million global case shipments, which confirmed the scale and maturity of the leading platform. In Q1 2026, Align shipped 685.7 thousand cases, up 6.7% year over year, while North American volumes remained stable. That pattern shows that U.S. expansion is now leaning more on deeper provider utilization and stronger case conversion than on simple network expansion. Across the United States invisible orthodontics market, the product story still begins with clear aligners because they define both patient expectations and competitive positioning.

Ceramic braces are projected to grow at a 15.38% CAGR from 2026 to 2031, which makes them the fastest-growing product sub-segment. Their role remains important in cases where clinicians want more direct torque control or force levels that fall outside predictable aligner performance. Ormco expanded digital bonding to more orthodontic bracket systems at AAO 2026, which showed that bracket manufacturers are modernizing workflow rather than giving ground to aligners. Lingual braces remain a small but premium option for adults who want maximum discretion and accept a higher cost and narrower provider base. Retainers also remain strategically important because every finished case can convert into repeat post-treatment revenue, which keeps product lifetime value higher than initial treatment revenue alone suggests.

Polyurethane and co-polyester multilayer films accounted for 75.24% of revenue in 2025, which kept the material base of the United States invisible orthodontics market tilted toward premium multilayer performance. Align Technology's SmartTrack platform helped establish that benchmark, and related multilayer polymer sheet constructions remain protected by patent coverage. Research published in Orthodontics and Craniofacial Research showed that PETG and thermoplastic polyurethane differ in stiffness behavior by tooth region and aligner thickness. That evidence supports the view that material selection is a treatment-performance decision rather than a simple sourcing choice. As a result, established multilayer systems still hold the clinical lead in the United States invisible orthodontics market.

PETG is projected to grow at a 15.52% CAGR from 2026 to 2031, driven by broader use among challenger brands that want a performance-value position. PETG offers a practical balance of transparency, processability, and cost, which makes it attractive for brands trying to widen access without moving fully downmarket. Direct-print resin materials are also starting to enter the discussion, because they could eventually remove the thermoforming step and support on-demand in-office production. FDA clearance for Primeprint Direct Aligner under K250739 in October 2025 and subsequent clinical evaluation activity in 2026 moved that concept closer to real use, even though it is still early. The United States invisible orthodontics industry is therefore moving toward a layered material structure with premium multilayer films at the top, PETG in the middle, and printed resins as a future in-house production option.

List of Companies Covered in this Report:

- Align Technology

- American Orthodontics Corporation

- Bausch Health Companies Inc. (OraFit)

- Candid Care Co.

- ClearPath Orthodontics

- Dentsply Sirona

- DynaFlex

- Envista Holdings Corporation (Ormco)

- G&H Orthodontics

- Great Lakes Dental Technologies

- Henry Schein

- Straumann Group

- OrthoFX, Inc.

- SCHEU-DENTAL GmbH

- Shanghai Smartee Denti-Technology Co., Ltd.

- Solventum Corporation

- TP Orthodontics

- Zendura Dental (Bay Materials LLC)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adult Malocclusion Burden and Aesthetics-Led Demand

- 4.2.2 AI Planning, Intraoral Scanning, and Digital Workflows

- 4.2.3 Hybrid Remote Monitoring Improves Case Throughput

- 4.2.4 Selective Expansion of Adult Orthodontic Benefits and Financing Access

- 4.2.5 DSO And Group-Practice Scaling Accelerates Aligner Penetration

- 4.2.6 Reduced-Wear-Time and Pediatric-Interceptive Innovations Expand Candidacy

- 4.3 Market Restraints

- 4.3.1 High Out-of-Pocket Costs and Adult Coverage Gaps

- 4.3.2 Tighter Scrutiny of Mail-Order Aligners and In-Person Exam Requirements

- 4.3.3 Challenger-Brand Churn Undermines Trust and Channel Stability

- 4.3.4 Staffing and Training Bottlenecks in In-House Digital Production

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Clear Aligners

- 5.1.2 Ceramic Braces

- 5.1.3 Lingual Braces

- 5.1.4 Retainers

- 5.2 By Material

- 5.2.1 Polyurethane / co-polyester multilayer films

- 5.2.2 PETG

- 5.2.3 Polycarbonate

- 5.2.4 Other thermoplastics

- 5.3 By Age Group

- 5.3.1 Adults

- 5.3.2 Teens

- 5.3.3 Children and mixed dentition

- 5.4 By Care Setting

- 5.4.1 Standalone orthodontic practices

- 5.4.2 Group practices, DSOs, and OSOs

- 5.4.3 Hospitals and academic dental centers

- 5.4.4 Other dental clinics

- 5.5 By Provider Type

- 5.5.1 Orthodontists

- 5.5.2 General dentists

- 5.6 By Sales Channel

- 5.6.1 Offline

- 5.6.2 Online

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Align Technology Inc.

- 6.3.2 American Orthodontics Corporation

- 6.3.3 Bausch Health Companies Inc. (OraFit)

- 6.3.4 Candid Care Co.

- 6.3.5 ClearPath Orthodontics

- 6.3.6 Dentsply Sirona Inc.

- 6.3.7 DynaFlex

- 6.3.8 Envista Holdings Corporation (Ormco)

- 6.3.9 G&H Orthodontics

- 6.3.10 Great Lakes Dental Technologies

- 6.3.11 Henry Schein, Inc.

- 6.3.12 Institut Straumann AG

- 6.3.13 OrthoFX, Inc.

- 6.3.14 SCHEU-DENTAL GmbH

- 6.3.15 Shanghai Smartee Denti-Technology Co., Ltd.

- 6.3.16 Solventum Corporation

- 6.3.17 TP Orthodontics, Inc.

- 6.3.18 Zendura Dental (Bay Materials LLC)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment