|

시장보고서

상품코드

2072492

인비저블 치열교정 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Invisible Orthodontics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

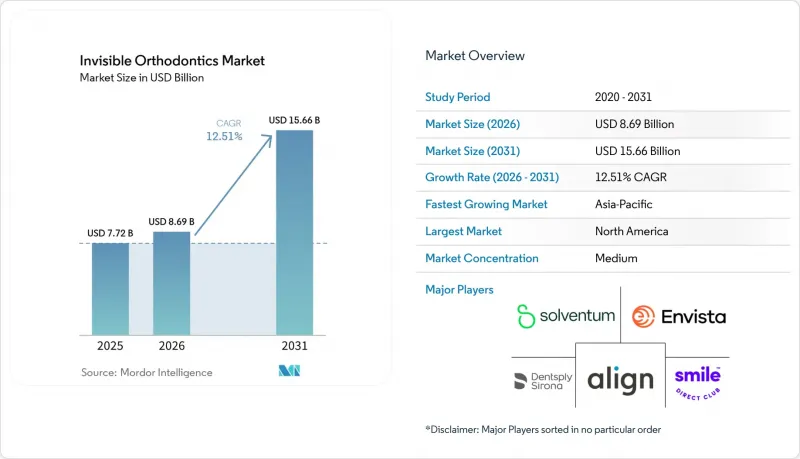

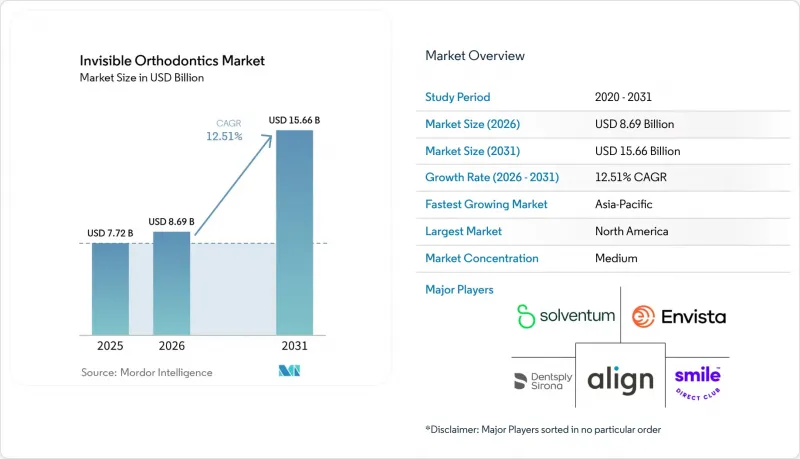

Mordor Intelligence에 의하면, 인비저블 치열교정 시장 규모는 2025년에 77억 2,000만 달러로 평가되었습니다. 2026년 86억 9,000만 달러에서 2031년까지 156억 6,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 12.51%를 나타낼 전망입니다.

본 보고서는 제품별(세라믹 브라켓, 인비저블 치열교정 장치 등), 소재별(열가소성 폴리우레탄(TPU), PETG 등), 환자 그룹별(성인, 10대, 소아), 최종 사용자(치과·교정치과 클리닉 등), 판매 채널(치과 의사 주도의 병원 내 치료 및 통신 판매/온라인), 지역(북미 등)별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러)으로 표시되어 있습니다.

세계의 인비저블 치열교정 시장 동향 및 분석

부정교합의 유병률과 심미 의식

세계 인구의 절반 이상이 어떤 형태의 부정교합을 가지고 있으며, 그 내역은 클래스 I이 51.9%, 클래스 II가 23.8%, 클래스 III이 6.5%를 나타낼 전망입니다. 소셜 미디어를 통한 노출로 인해, 치열교정는 단순한 임상적 개입이 아닌 라이프스타일 향상을 위한 수단으로 재정의되었습니다. 호주에서는 2024년에 청소년의 31.7%가 치열교정 서비스를 받았으며, 그중 80.6%가 민간 클리닉을 선택한 것으로 나타나, 미적 개선을 위해 본인 부담으로 투자하려는 의지가 높음을 알 수 있습니다. Align Technology사는 누적 2,010만 건 이상의 사례를 치료해 왔으며, 전문가들이 일상적인 화상 통화에 자연스럽게 어우러지는 보이지 않는 교정 치료를 요구함에 따라 성인 환자 수는 계속 증가하고 있습니다. “"눈에 띄지 않는" 이러한 솔루션에 대한 선호도가 많은 도시 시장에서 인비저블 치열교정기나 설측 교정 장치가 기존의 금속 브라켓을 대체한 이유를 설명해 줍니다.

AI를 활용한 3D 설계 및 프린팅이 맞춤화를 가속화합니다.

콘빔 CT 스캔에 대한 인공지능 기반 분할 기술은 현재 0.92를 넘는 다이스 유사 계수를 달성하고 있으며, 수동으로 랜드마크를 설정하는 데 소요되는 시간을 최대 20% 단축하여 소규모 치과 병원의 처리 능력을 향상시키고 있습니다. Tera Harz TC-85 등의 수지를 사용한 얼라이너의 직접 3D 프린팅을 통해 열성형 공정이 불필요해졌으며, 제조 기간을 10일에서 48시간으로 단축했습니다. LuxCreo사와 Angelalign사는 2025년 10월, ActiveMemory 형상 회복성 폴리머를 발표하며, 필요한 공정을 거의 절반으로 줄일 수 있다고 주장하고 있습니다. 이러한 업무 흐름의 효율화를 통해 진료 시간을 확보함으로써, 클리닉은 직원을 증원하지 않고도 더 많은 환자를 진료할 수 있게 됩니다. 납기 단축과 정밀도 향상은 환자 만족도를 높여, 결과적으로 재방문 및 소개, 소셜 미디어를 통한 추천으로 이어집니다.

높은 치료비와 제한된 보험 급여

북미에서는 일반적인 인비저블 치열교정기 치료 비용이 3,000-8,000달러이지만, 보험 급여 상한선이 여전히 2,000달러 전후에 머물러 있다는 점을 고려하면, 소득 중위값 이하인 가구에게는 큰 부담이 되고 있습니다. 인도나 인도네시아에서는 1인당 GDP가 4,000달러 미만이기 때문에 경제적 격차가 더욱 심각하며, 교정 치료는 도시 지역의 고소득층 소비자로만 제한되어 있습니다. 무이자 할부 계획은 있지만, 치료 기간이 18개월을 초과하면 채무 불이행 위험이 높아집니다. 보다 광범위한 접근을 가능하게 하려면, 1건당 제조 비용을 1,500달러 미만으로 억제해야 하며, 이를 위해서는 더 대규모의 프린트 팜, 자동화, 그리고 더 저렴한 원료가 필요합니다.

부문별 분석

2025년 매출의 70.56%를 클리어 얼라이너가 차지해, 인비저블 치열교정 시장이 탈부착 가능한 트레이를 중심으로 형성되어 있음을 뒷받침했습니다. 한편, 설측 교정 장치는 CAD/CAM을 통한 맞춤형 제작으로 인해 진료실 내 조정이 줄어들기 때문에 고정식 교정 장치 중 가장 높은 연평균 성장률(CAGR) 18.25%를 나타낼 것으로 예측됩니다. 세라믹 브라켓은 내구성이 필요하면서도 눈에 잘 띄지 않는 점을 중요시하는 10대 청소년들 사이에서 틈새 수요를 차지하고 있는 반면, 진공 성형 리테이너는 치료 후 유지 관리 단계에서 주류를 이루고 있습니다. 소프트웨어를 활용한 교정 장치 배치의 자동화로 인해 노동 집약도가 낮아짐에 따라, 설측 교정 시스템 시장 규모는 급속히 확대될 전망입니다. LightForce사의 직접 3D 프린팅 방식 세라믹 브라켓은 전체 치료 기간을 40% 단축시켜 주기 때문에 치료 건수 확대를 중시하는 치과에 매력적인 제품입니다.

또한, 병원 내 밀링이 주류를 이루게 됨에 따라, 구성 부품의 비용 절감도 설측 교정 시스템에 호재가 되고 있습니다. 다층 구조의 얼라이너 설계(단단한 외피와 부드러운 내층의 조합)를 통해 힘의 분산이 개선되고, 치료의 예측 가능성이 높아지며, 조정 횟수가 줄어들고 있습니다. 리테이너도 진화하고 있습니다. 초기 비용은 비싸지만, 환자의 치료 순응도 문제를 해소할 수 있는 접착형 리테이너의 도입이 확대되고 있습니다. 이러한 변화는 인비저블 치열교정 시장이 더 이상 단일한 주류 치료법에 의존하는 것이 아니라, 맞춤형 솔루션의 폭넓은 선택지에 의해 뒷받침되게 될 것임을 시사합니다.

열가소성 폴리우레탄은 탄성 기억 특성으로 인해 응력 완화를 억제하고 일정한 힘을 지속적으로 발휘할 수 있기 때문에 2025년에는 47.53%의 시장 점유율을 차지했습니다. PETG는 원자재 비용이 저렴하고 열성형성이 뛰어나, 연평균 성장률(CAGR) 20.85%로 급성장할 것으로 예상되어 대규모 프린트 업체들에게 매력적인 소재로 자리 잡고 있습니다. 폴리카보네이트는 경직성으로 인한 불편함 때문에 시장 점유율이 점차 줄어들고 있지만, Zendura FLX와 같은 독자적인 배합 제품은 14일간의 착용 주기를 통해 초기 투명도의 92%를 유지하고 있으며, 이는 일반 PETG의 78%를 상회하는 수치입니다. 공장에서 스크랩률을 낮추기 위해 노력함에 따라, PETG와 관련된 인비저블 치열교정 시장 규모는 확대될 것으로 예측됩니다.

ActiveMemory 폴리머는 체온에 의해 트레이의 형태를 원래대로 되돌리는 형상 회복 메커니즘을 도입하고 있으며, 이를 통해 고정력이 실질적으로 2배로 증가하고 공정 수를 절반으로 줄일 가능성도 있습니다. 직접 프린팅용 수지는 여전히 비용 및 생체적합성 측면에서 제약을 받고 있지만, 복잡한 증례에서도 당일 납품이 가능하기 때문에 도심 지역의 부티크 클리닉에게는 경쟁 우위가 됩니다. 원료의 다양화가 진행됨에 따라, 인비저블 치열교정 시장은 착용 기간, 광학적 투명도, 생체 적합성에 따라 더욱 세분화될 것입니다.

지역별 분석

북미는 2025년 매출의 43.13%를 차지했으며, 청소년의 교정 치료 보급률이 60%를 넘어섰고, 고용주가 자금을 지원하는 보험 플랜을 통해 성인의 이용이 확대되고 있는 점이 이를 뒷받침했습니다. Align사는 2025년 1분기에 전 세계적으로 64만 2,000건 이상의 치료 사례를 출하했으며, 이 중 약 55%가 이 지역에서 발생한 것으로, 인비저블 치열교정법에 중점을 둔 치료법의 성숙도가 지속적으로 높아지고 있음을 보여줍니다. 최근 시퀀셜 얼라이너에 관한 ADA(미국치과의사협회) 기준이 발표됨에 따라 소규모 실험실의 규정 준수 비용이 증가했고, 그 결과 공급이 자금력이 있는 제조업체로 쏠리는 경향이 있습니다. 캐나다에서는 유리한 보험 규정 덕분에 점진적인 성장이 예상되는 한편, 미국에서 멕시코로 향하는 국경 간 치과 관광이 해당 지역의 진료 건수를 끌어올리고 있습니다.

아시아태평양은 중국이나 인도와 같은 인구 대국에서 치열교정 보급률이 여전히 5% 미만에 그치고 있는 만큼, 세계 최고 수준인 연평균 성장률(CAGR) 21.81%를 나타낼 것으로 전망됩니다. Angelalign은 현지 언어를 지원하는 소프트웨어와 미국 브랜드보다 30% 저렴한 가격을 강점으로 삼아, 국내 시장 점유율을 확대하는 동시에 수익 다각화를 도모하기 위해 미국에도 거점을 개설했습니다. 스트라우만사는 2024년 3분기 중국에서 구강 스캐너 판매가 호조를 보였습니다고 밝혔습니다. 디지털 스캔은 얼라이너 치료의 첫 단계이므로, 이는 선행 지표가 됩니다. 2024년 1억 4,701만 달러 규모의 호주 시장은 연평균 성장률(CAGR) 28.67%를 달성했으며, 이는 보험 보장이 충실하다는 점과 심미 치과 치료가 문화적으로 중요하게 여겨지고 있다는 점을 모두 반영하고 있습니다.

유럽은 10%대 중반의 점유율을 차지하고 있으며, 독일, 영국, 프랑스가 판매량을 주도하고 있습니다. 공적·민간 보험의 혼합 제도에 따라 사춘기 환자에게는 보조금이 지급되고 있으며, 유연한 지출 메커니즘이 보급됨에 따라 성인의 이용도 증가하고 있습니다. 스트라우만사가 2024년에 Dr.Smile을 매각한 것은 MDR(의료기기 규정)로 인한 규정 준수 비용의 급등을 배경으로, 전문의 채널로의 회귀를 도모하기 위한 전환점이 되었습니다. 스페인이나 이탈리아 등 남유럽 시장은 기저가 낮기 때문에 더 높은 성장률을 보이고 있습니다. 라틴아메리카와 중동은 각각 시장 점유율은 작지만, 강력한 성장이 눈에 띄는 지역이 있습니다. 브라질에서는 연간 약 140만 건의 교정 치료가 시작되고 있으며, GCC 국가들에서는 높은 가처분 소득에 힘입어 고액의 지출이 지속되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the invisible orthodontics market size was valued at USD 7.72 billion in 2025 and is estimated to grow from USD 8.69 billion in 2026 to reach USD 15.66 billion by 2031, at a CAGR of 12.51% during the forecast period (2026-2031).

This report is Segmented by Product (Ceramic Braces, Clear Aligners, and More), Material (Thermoplastic Polyurethane (TPU), PETG, and More), Patient Group (Adult, Teenager, and Children), End User (Dental & Orthodontics Clinics, and More), Sales Channel (Dentist-Led In-Office and Mail-Order/Online), and Geography (North America, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Invisible Orthodontics Market Trends and Insights

Prevalence of Malocclusion & Aesthetic Consciousness

More than half of the global population presents some form of malocclusion, with Class I at 51.9%, Class II at 23.8%, and Class III at 6.5%. Social-media visibility has reframed orthodontics as a lifestyle enhancement rather than solely a clinical intervention. In Australia, 31.7% of adolescents obtained orthodontic services in 2024, and 80.6% chose private clinics, illustrating a willingness to self-finance esthetic upgrades. Align Technology has treated over 20.1 million cumulative cases, and adult volume continues to climb as professionals seek discreet correction that blends into daily video calls. The preference for "stealth" solutions explains why clear aligners and lingual braces have displaced traditional metal brackets in many urban markets.

AI-Driven 3D Planning & Printing Accelerate Customization

Artificial-intelligence segmentation of cone-beam CT scans now achieves Dice similarity coefficients above 0.92, cutting manual landmarking time by up to 20% and raising throughput for small practices. Direct 3D printing of aligners from resins such as Tera Harz TC-85 eliminates thermoforming, slashing production from 10 days to 48 hours. LuxCreo and Angelalign unveiled ActiveMemory shape-recovery polymers in October 2025, claiming to trim required stages by nearly half. Such workflow economies free chair time, allowing clinics to accept more cases without proportional staff hires. Faster turnaround and greater precision reinforce patient satisfaction, thereby fueling repeat referrals and social-media endorsements.

High Treatment Cost & Limited Reimbursement

In North America, a typical clear-aligner program costs USD 3,000-8,000, leaving a significant gap for households below median income given that insurance caps still hover near USD 2,000. India and Indonesia face an even sharper affordability divide, where per-capita GDP rests under USD 4,000, relegating orthodontics to upper-income urban consumers. Zero-interest installment plans do exist but carry higher default risk when treatment exceeds 18 months. Broader access hinges on bringing per-case manufacturing costs below USD 1,500, which will require larger print farms, automation, and cheaper feedstocks.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Orthodontic Insurance Cover in OECD Markets

- Tele-Orthodontics & Remote Monitoring Broaden Access

- Shortage of Trained Orthodontists in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clear aligners generated 70.56% of 2025 revenue, reinforcing the centrality of removable trays in the invisible orthodontics market. Lingual braces, however, are projected to log an 18.25% CAGR, the fastest among fixed appliances, as CAD/CAM customization reduces chair-side adjustments. Ceramic brackets hold a niche among teens who need durability but value some discretion, while vacuum-formed retainers rule post-treatment phases. The invisible orthodontics market size for lingual systems is poised to expand sharply as software-guided bracket placement lowers labor intensity. Direct 3D-printed ceramic brackets from LightForce shorten overall active treatment by 40%, appealing to practices focused on throughput.

Lingual systems also benefit from declining component costs as in-house milling becomes mainstream. Multi-layered aligner designs-stiff outer shells paired with softer inner layers-introduce better force distribution, improving predictability and reducing refinements. Retainers evolve too: bonded variants that remove patient-compliance risk are gaining adoption despite their higher upfront price. These shifts suggest that the invisible orthodontics market will no longer hinge on a single dominant modality but rather on a palette of custom-fit solutions.

Thermoplastic polyurethane occupied 47.53% share in 2025 because its elastic memory counters stress relaxation and maintains constant force delivery. PETG is forecast to surge at 20.85% CAGR owing to lower raw-material cost and superior thermoformability, making it attractive for large-scale print farms. Polycarbonate has ceded ground due to stiffness-related discomfort, while proprietary blends like Zendura FLX retain 92% of initial transparency over a 14-day wear cycle, outpacing generic PETG's 78%. The invisible orthodontics market size tied to PETG is projected to widen as factories seek scrap-rate reductions.

ActiveMemory polymers introduce shape-recovery mechanics that reset tray geometry at body temperature, effectively doubling force sustainability and potentially halving the number of stages. Direct-print resins still face cost and biocompatibility constraints, yet they enable same-day delivery for complex cases, a competitive edge for urban boutique clinics. As feedstock diversity widens, the invisible orthodontics market will segment further by wear-cycle length, optical clarity, and biocompatibility.

Complete Report Scope:

- By Product

- Clear Aligners

- Single-layer PETG

- Multi-layer TPU

- Ceramic Braces

- Poly-crystalline

- Mono-crystalline

- Lingual Braces

- CAD/CAM customised

- Standard brackets

- Retainers

- Vacuum-formed clear retainers

- Bonded retainers

- Clear Aligners

- By Material

- Thermoplastic Polyurethane (TPU)

- PETG

- Polycarbonate

- Others (PP, PVC, Co-polyesters)

- By Patient Group

- Adults

- Teenagers

- Children

- By End User

- Dental & Orthodontic Clinics

- Hospitals

- Direct-to-Consumer Platforms

- By Sales Channel

- Dentist-led in-office

- Mail-Order / Online

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America generated 43.13% of 2025 revenue, buoyed by orthodontic penetration above 60% among adolescents and rising adult adoption in employer-funded plans. Align shipped over 642,000 cases globally in Q1 2025, and roughly 55% originated from this region, illustrating sustained maturity of invisibility-focused modalities. Recent publication of ADA standards for sequential aligners raises compliance costs for smaller labs, thus tilting supply toward well-capitalized manufacturers. Canada adds incremental growth through favorable insurance provisions, whereas U.S. cross-border dental tourism to Mexico boosts regional case volume.

Asia-Pacific is forecast to deliver a 21.81% CAGR, the highest globally, since orthodontic penetration remains under 5% in populous countries like China and India. Angelalign benefits from localized software and price points 30% below U.S. brands, growing its domestic share while also opening a U.S. facility to diversify revenue. Straumann noted brisk intraoral-scanner sales in China during Q3 2024, a leading indicator because digital scanning is the entry point for aligner treatment. Australia's market, valued at USD 147.01 million in 2024, demonstrates 28.67% CAGR potential, reflecting both strong insurance reimbursement and cultural emphasis on cosmetic dentistry.

Europe holds a mid-teen share, with Germany, the United Kingdom, and France dominating volumes. Public-private insurance hybrids subsidize adolescent cases, and adult uptake rises as flexible spending mechanisms become common. Straumann's divestiture of Dr.Smile in 2024 marked a pivot back toward professional channels amid MDR-driven compliance costs. Southern European markets like Spain and Italy show faster percentage growth from lower bases. Latin America and the Middle East each hold smaller slices but reveal pockets of strength: Brazil records roughly 1.4 million orthodontic case starts annually, and GCC nations sustain premium spending fueled by high disposable income.

- Align Technology

- American Orthodontics

- Angelalign Technology Inc.

- Avinent Group

- Byte by Dentsply Sirona

- Candid Co.

- ClearPath Orthodontics

- DB Orthodontics

- Dentsply Sirona

- Envista

- G&H Orthodontics

- Great Lakes Dental Technologies

- Henry Schein

- Straumann Group

- SCHEU-DENTAL GmbH

- Smartee Denti-Technology

- SmileDirectClub

- Solventum Corporation

- Sunshine Smile GmbH (DrSmile)

- TP Orthodontics

- WonderSmile

- Zendura Dental

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Prevalence of malocclusion & aesthetic consciousness

- 4.2.2 AI-driven 3-D planning & printing accelerate customisation

- 4.2.3 Expansion of orthodontic insurance cover in OECD markets

- 4.2.4 Tele-orthodontics & remote monitoring broaden access

- 4.2.5 Bio-resorbable & smart polymer aligners shorten wear cycles

- 4.2.6 Employer-funded dental benefits in EMs lift adult uptake

- 4.3 Market Restraints

- 4.3.1 High treatment cost & limited reimbursement

- 4.3.2 Shortage of trained orthodontists in EMs

- 4.3.3 Regulatory clamp-down on DTC aligner business models

- 4.3.4 Patent expiries driving price erosion & margin squeeze

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Clear Aligners

- 5.1.1.1 Single-layer PETG

- 5.1.1.2 Multi-layer TPU

- 5.1.2 Ceramic Braces

- 5.1.2.1 Poly-crystalline

- 5.1.2.2 Mono-crystalline

- 5.1.3 Lingual Braces

- 5.1.3.1 CAD/CAM customised

- 5.1.3.2 Standard brackets

- 5.1.4 Retainers

- 5.1.4.1 Vacuum-formed clear retainers

- 5.1.4.2 Bonded retainers

- 5.1.1 Clear Aligners

- 5.2 By Material

- 5.2.1 Thermoplastic Polyurethane (TPU)

- 5.2.2 PETG

- 5.2.3 Polycarbonate

- 5.2.4 Others (PP, PVC, Co-polyesters)

- 5.3 By Patient Group

- 5.3.1 Adults

- 5.3.2 Teenagers

- 5.3.3 Children

- 5.4 By End User

- 5.4.1 Dental & Orthodontic Clinics

- 5.4.2 Hospitals

- 5.4.3 Direct-to-Consumer Platforms

- 5.5 By Sales Channel

- 5.5.1 Dentist-led in-office

- 5.5.2 Mail-Order / Online

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Align Technology Inc.

- 6.3.2 American Orthodontics

- 6.3.3 Angelalign Technology Inc.

- 6.3.4 Avinent Group

- 6.3.5 Byte by Dentsply Sirona

- 6.3.6 Candid Co.

- 6.3.7 ClearPath Orthodontics

- 6.3.8 DB Orthodontics

- 6.3.9 Dentsply Sirona

- 6.3.10 Envista Holdings (Ormco)

- 6.3.11 G&H Orthodontics

- 6.3.12 Great Lakes Dental Technologies

- 6.3.13 Henry Schein Inc.

- 6.3.14 Institut Straumann AG

- 6.3.15 SCHEU-DENTAL GmbH

- 6.3.16 Smartee Denti-Technology

- 6.3.17 SmileDirectClub

- 6.3.18 Solventum Corporation

- 6.3.19 Sunshine Smile GmbH (DrSmile)

- 6.3.20 TP Orthodontics

- 6.3.21 WonderSmile

- 6.3.22 Zendura Dental

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment