|

시장보고서

상품코드

2066423

소형 위성 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Small Satellite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

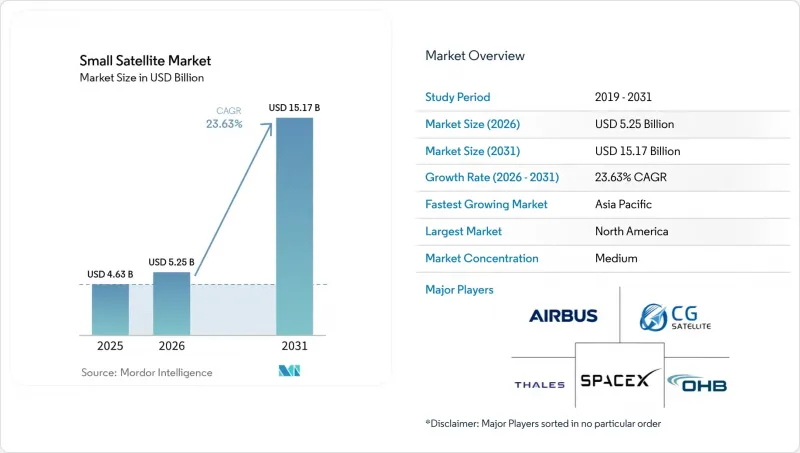

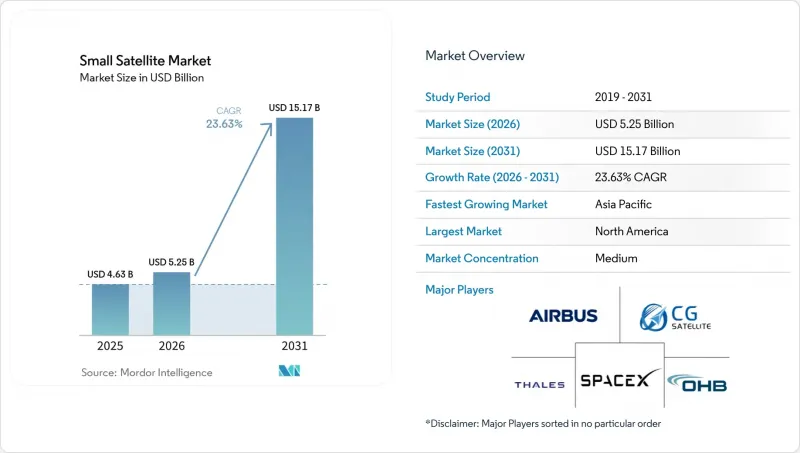

Mordor Intelligence에 의하면, 소형 위성 시장 규모는 2025년 46억 3,000만 달러로 평가되었습니다. 2026년에는 52억 5,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 23.63%로 성장을 지속하여, 2031년에는 151억 7,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 용도(통신, 지구관측, 항법, 우주 관측, 기타), 궤도(LEO, MEO, GEO), 최종 사용자(상업용, 정부·민간, 군사), 위성 질량(펨토 위성, 피코 위성, 나노 위성 등), 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 소형 위성 시장 동향 및 인사이트

재사용형 발사 비용의 급격한 감소

스페이스X가 선구자 역할을 한 재사용형 발사 시스템의 도입으로, 우주 진출 비용이 대폭 절감되었습니다. Rocket Lab이나 SpaceX와 같은 업체들이 제공하는 재사용 가능한 1단 로켓은 탑재체 질량과 발사 비용 사이에 기존에 존재하던 상관관계를 깨뜨렸습니다. 재사용형 로켓은 여러 번 발사할 수 있으며, 1회 발사당 최대 70%의 비용 절감을 실현하고 있습니다. 스페이스X는 저궤도(LEO)로의 발사 비용을 1kg당 약 2,700-3,000달러까지 낮췄습니다. 대조적으로, 기존의 일회용 로켓은 1Kg당 1만 달러 이상이 드는 경우가 많아, 재사용의 경제적 이점이 부각되고 있습니다. 2025년에는 ‘일렉트론’이 21회, ‘팔콘 9’가 90회 이상의 임무를 수행함에 따라, 위성 군집 소유자들은 1년을 기다릴 필요 없이 매달 발사 일정을 예약할 수 있게 되었습니다. 발사 빈도가 증가함에 따라 설계자는 18개월마다 센서를 교체할 수 있게 되어, 위성군의 기술 수준을 최신 상태로 유지할 수 있게 됩니다. 또한, 1Kg당 비용 절감은 중복성 확보를 촉진하여 서비스 가동률 향상으로 이어집니다. 인도 및 일본의 수출신용기관이 새로운 발사체에 자금을 지원하고 있어, 전 세계적으로 1Kg당 5,000달러 미만으로 가격이 하락하는 압력이 발생하고 있습니다. 이러한 비용 효율성 향상은 위성 사업자의 진입 장벽을 낮추고, 위성 군집의 구축을 가속화하며, 소형 위성 시장의 성장을 뒷받침하고 있습니다.

LEO 광대역 메가 콘스텔레이션의 급속한 성장

스페이스X(SpaceX)나 원웹(OneWeb)과 같은 기업들이 주도하는 LEO 광대역 메가 콘스텔레이션의 급속한 성장은 소형 위성 시장을 견인하는 중요한 요인이 되고 있습니다. 아마존 쿠이퍼는 7,727기의 위성 운용 허가를 취득했으며, 2025년 말까지 210기의 위성을 궤도에 투입했습니다. 스페이스X는 2026년 초 위성 수를 7,000기 이상으로 늘리고, 연간 매출 60억 달러 이상을 기록하며 소비자 대상 직접 서비스의 경제성을 입증했습니다. 634기의 위성을 보유한 OneWeb은 소비자 간의 가격 경쟁을 피하기 위해 기업 고객을 타겟으로 삼고 있습니다. 일반적으로 전 세계에 서비스를 제공한 최초의 통신사가 지역별 판매 계약을 따내게 되며, 이를 통해 고객을 자사 단말기에 묶어두게 됩니다. 라이선싱도 중요한 요소입니다. 미국과 영국의 라이선스 발급 절차는 다른 많은 지역보다 신속하게 진행되기 때문에 이 지역의 사업자들은 선점 우위를 점하고 있습니다. 이러한 광범위한 네트워크를 구축하려면 수백 기에서 수천 기에 이르는 소형 위성을 배치해야 하며, 이에 따라 제조 수요와 발사 빈도가 증가하고, 특히 서비스가 미치지 않는 외딴 지역의 세계 연결성을 포함한 하류 서비스에 대한 수요도 증가할 것입니다.

주파수 라이선싱의 병목 현상

주파수 대역 라이선싱의 병목 현상은 소형 위성 시장에 큰 제약 요인으로 작용하고 있습니다. 사업자는 각국의 규제 당국으로부터 승인을 획득하는 한편, 국제전기통신연합(ITU) 등의 기구를 통해 국제적인 조정을 이루어 나가야 합니다. 미국 연방통신위원회(FCC)는 2025년에 지상국 신청 처리 대기 건수를 절반으로 줄였지만, 연방 정부의 주파수 대역 이용자들과의 조정에는 여전히 최대 2년이 소요됩니다. 또한, ITU의 출력 밀도 제한에 따라 WRC-27에서 새로운 규정이 합의될 때까지 위성군의 처리량은 제한된 상태로 유지될 것입니다. 단말기 제조업체들은 명확한 위성 군 배치 일정이 확정되지 않는 한 V-BAND 장비의 양산에 착수할 수 없어, 하드웨어 비용 절감이 지연되고 있습니다. 스타링크와 같이 조기에 Ku 대역 및 Ka 대역의 인가를 취득한 사업자는 시기적 측면에서 우위를 점하고 있습니다. 이러한 절차는 대개 시간이 오래 걸리고 복잡하며, 이용 가능한 주파수 대역이 제한적이라는 점이 위성군 구축을 더욱 지연시키고, 규정 준수 비용을 증가시키며, 불확실성을 야기하고 있습니다. 이 과제는 시기적절한 시장 진입을 목표로 하는 신규 진입 사업자에게 특히 두드러집니다.

부문별 분석

지구관측 분야는 계속해서 성장하고 있으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 24.71%를 나타낼 것으로 전망됩니다. 2025년에는 통신 분야가 소형 위성 시장 점유율의 45.25%를 차지했으나, 지구관측 분야가 통신 분야의 우위를 넘어설 것으로 예측됩니다. Planet Labs와 ICEYE는 농업 및 보험 업계의 고객들이 실시간으로 활용할 수 있는 고해상도 데이터와 SAR(합성개구레이더) 데이터를 제공합니다. 지구관측 서비스 분야에서 소형 위성 시장 규모 확대를 주도하고 있는 것은 원본 이미지 데이터가 아니라, 경보 정보를 수익화하는 분석 플랫폼입니다. 통신 분야는 여전히 스타링크(Starlink)와 같은 대규모 위성군에 의존하고 있지만, 북미 소비자 시장에서의 보급이 정체 상태에 접어들면서 성장세가 둔화되고 있습니다. 분석 서비스 제공업체는 국방, 해양, 재난 대응 분야의 사용자를 대상으로 제품을 맞춤화하여 더 높은 이익률을 확보하고 있습니다.

한편, 항법용 페이로드에서는 재밍 대책의 일환으로 LEO 신호에 대한 검증이 진행되고 있습니다. 과학적인 우주 관측 임무는 필수적이지만, 자금이 제한적이어서 여전히 틈새 분야로 남아 있습니다. 용도 구성을 살펴보면, 대용량 소비자용 광대역과 고부가가치 데이터 서비스로 나뉘어 있으며, 각각이 위성 설계에 서로 다른 영향을 미치고 있습니다.

2025년에는 저지연을 중시하는 인터넷 위성 군집의 주도 하에, LEO가 소형 위성 시장 규모의 42.75%를 차지했습니다. MEO는 위치 측정·항법·시간 동기화(PNT) 임무가 수천 대의 위성을 필요로 하지 않으면서도 커버리지와 생존성 간의 균형을 맞출 수 있기 때문에 연평균 성장률(CAGR) 24.83%를 나타낼 것으로 예측됩니다. ESS 등의 방위 계약에서는 GEO의 지연 현상을 피하면서도 LEO의 공기 저항을 회피하기 위해, MEO에 배치된 보호용 통신 중계기가 설치되어 있습니다. GEO 사업자들은 전기 추진 시스템과 유연한 페이로드로의 개조를 추진하고 있지만, 고객들이 100밀리초 미만의 지연 시간을 요구하고 있어 여전히 시장 점유율을 잃고 있습니다. 희소한 GEO 궤도를 둘러싼 규제 분쟁으로 인해 신흥국들은 LEO를 대체할 수단으로 눈을 돌리고 있습니다. MEO 중계기와 LEO 사용자 링크를 결합한 하이브리드형 위성군이 타협안으로 등장하여, 투자 위험을 각 궤도에 분산시키고 있습니다.

지역별 분석

2025년에는 스타링크의 확장 속도와 미국 국방부의 분산형 아키텍처에 대한 투자 덕분에 북미가 53.77%의 점유율로 1위를 차지했습니다. 안드로메다 계약은 14개사에 발주를 분산시켜 공급망의 다양화와 경쟁을 촉진하고 있습니다. 로켓랩의 18억 5,000만 달러 규모의 미수주 잔액은 가격 압박에도 불구하고 수직 통합이 어떻게 이익률을 확보하고 있는지를 여실히 보여주고 있습니다. 캐나다의 테레스앳은 극지방을 커버하는 298기의 위성 네트워크를 구축 중이며, 대륙 전체에 걸친 서비스 제공 범위를 확대되고 있습니다.

아시아태평양은 중국의 ‘국망(Guowang)’ 위성군과 인도의 ‘NewSpace India Limited’가 현지 생산을 확대함에 따라 연평균 성장률(CAGR) 24.63%로 성장할 것으로 전망됩니다. Chang Guang Satellite Technology사는 동남아시아 및 아프리카 전역에 고해상도 데이터를 경쟁력 있는 가격으로 판매하고 있습니다. 인도는 PSLV의 생산량을 확대하고 있으며, 이를 통해 지역 스타트업 기업들이 해외 발사 대기 목록을 피할 수 있게 되었습니다. 일본은 정밀 제조 기술을 활용해 전기 추진용 부품을 공급하고 있는 반면, 호주의 간소화된 라이선스 제도는 지상국 투자자들을 끌어들이고 있습니다.

유럽은 조달 체계의 분산과 주파수 조정 지연으로 인해 제약을 받고 있음에도 불구하고, 15-18%의 안정적인 시장 점유율을 유지하고 있습니다. OneWeb은 634기의 위성 군 배치 작업을 완료했으며, 기업용 통신 서비스 제공을 목표로 하고 있습니다. ESA의 3개 위성으로 구성된 CO2M 프로그램은 EU의 탄소국경조정메커니즘을 지원하며, 지구관측 수요를 기후 정책과 연계하고 있습니다. 중동의 정부계 펀드는 서유럽 국가들과의 합작 사업을 통해 국내 플랫폼을 지원하고 있습니다. 남미에서는 브라질의 BNDES가 국내 제조업에 자금을 지원하고 있어 꾸준한 성장이 나타나고 있는 반면, 사테로직사의 우루과이 공장에서는 농업 분석용 35kg 용량의 버스가 출하되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the small satellite market size is expected to grow from USD 4.63 billion in 2025 to USD 5.25 billion in 2026 and is forecast to reach USD 15.17 billion by 2031 at a 23.63% CAGR over 2026-2031.

This report is Segmented by Application (Communication, Earth Observation, Navigation, Space Observation, and Others), Orbit (LEO, MEO, and GEO), End-User (Commercial, Government and Civil, and Military), Satellite Mass (Femtosatellites, Picosatellites, Nanosatellites, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Small Satellite Market Trends and Insights

Reusable-launch cost collapse

The adoption of reusable launch systems, initiated by SpaceX, has substantially reduced the cost of space access. Reusable first stages from operators such as Rocket Lab and SpaceX have broken the historic link between payload mass and launch expense. Reusable rockets can be launched multiple times, achieving cost savings of up to 70% per launch. The SpaceX company has lowered the cost, equating to around USD 2,700 to USD 3,000 per kilogram to LEO. In contrast, traditional expendable rockets often cost more than USD 10,000 per kilogram, underscoring the financial benefits of reusability. Electron flew 21 times in 2025, and Falcon 9 surpassed 90 missions, so constellation owners can book monthly slots instead of waiting a year. Faster cadence means designers can update sensors every 18 months, keeping fleets technologically current. Lower cost per kilogram also encourages redundancy, which improves service uptime. Export-credit agencies in India and Japan finance new launch vehicles, adding global price pressure below USD 5,000 per kg. This cost efficiency reduces entry barriers for satellite operators, expedites constellation deployment, and supports growth in the small satellite market.

LEO Broadband Mega-Constellations Boom

The rapid growth of LEO broadband mega-constellations, driven by companies such as SpaceX and OneWeb, is a significant factor propelling the small satellite market. Amazon Kuiper gained a 7,727-satellite license and placed 210 craft by late 2025. SpaceX exceeded 7,000 satellites in early 2026 and earned more than USD 6 billion in annual revenue, validating the economics of direct-to-consumer services. OneWeb, with 634 satellites, targets enterprise users to sidestep consumer price wars. The first network to achieve global coverage usually wins regional distribution deals, locking customers into proprietary terminals. Regulations also matter; the US and UK licensing processes move faster than those in many other regions, giving their operators a head start. These extensive networks necessitate the deployment of hundreds to thousands of small satellites, increasing manufacturing demand, launch frequency, and downstream services, including global connectivity, particularly in underserved and remote areas.

Spectrum-licensing bottlenecks

Spectrum-licensing bottlenecks are a significant restraint on the small satellite market. Operators are required to obtain approvals from national regulators and coordinate internationally through organizations such as the International Telecommunication Union. The FCC halved its Earth-station backlog in 2025, yet coordination with federal spectrum users still takes up to two years. ITU power flux density limits hold back fleet throughput until new rules are agreed at WRC-27. Terminal makers hesitate to mass-produce V-band equipment without clear constellation timelines, slowing hardware cost reduction. Operators with earlier Ku- or Ka-band approvals, such as Starlink, enjoy a timing advantage. These processes are often lengthy and complex, and limited spectrum availability further delays constellation deployments, increases compliance costs, and creates uncertainty. This challenge is particularly pronounced for new entrants aiming for timely market access.

Other drivers and restraints analyzed in the detailed report include:

- Multi-sector demand for Earth-observation analytics

- National-security shift to proliferated LEO fleets

- Space-debris mitigation costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Earth observation expanded with a 24.71% CAGR forecast for 2026-2031, overtaking communication's dominance despite communication holding 45.25% of the small satellite market share in 2025. Planet Labs and ICEYE add high-resolution and SAR data that agriculture and insurance customers absorb in real time. The small satellite market size for Earth-observation services is propelled by analytics platforms that monetize alerts rather than raw pixels. Communication still relies on massive fleets like Starlink, but growth slows as North American consumer uptake plateaus. Analytic providers tailor products to defense, maritime, and disaster-response users, capturing higher margins.

Meanwhile, navigation payloads test LEO signals to protect against jamming. Scientific space-observation missions, though vital, remain niche due to limited funding. The application mix shows a split between high-volume consumer broadband and high-value data services, each shaping satellite design differently.

LEO accounted for 42.75% of the small satellite market size in 2025, driven by internet constellations that value low latency. MEO is projected to grow at a 24.83% CAGR because positioning, navigation, and timing missions balance coverage and survivability without requiring thousands of craft. Defense contracts such as ESS place protected communication relays in MEO to sidestep GEO latency while avoiding LEO drag. GEO operators retrofit electric propulsion and flexible payloads, yet still lose share as customers demand latency under 100 ms. Regulatory fights over scarce GEO slots push emerging nations toward LEO alternatives. Hybrid fleets mixing MEO relays with LEO user links emerge as a compromise, spreading investment risk across orbits.

Geography Analysis

North America led with a 53.77% share in 2025 due to Starlink's deployment pace and the Pentagon's spending on proliferated architecture. The Andromeda contract spreads orders across 14 companies, encouraging supply-chain diversity and competition. Rocket Lab's USD 1.85 billion backlog underlines how vertical integration secures margins despite price pressure. Canada's Telesat prepares a 298-satellite network serving polar regions, broadening continental service coverage.

Asia-Pacific is forecasted to grow at a 24.63% CAGR as China's Guowang constellation and India's NewSpace India Limited scale local manufacturing. Chang Guang Satellite Technology sells high-resolution data across Southeast Asia and Africa at aggressive prices. India expands PSLV output, letting regional startups bypass foreign launch queues. Japan leverages precision manufacturing to supply electric-propulsion components, while Australia's streamlined licensing draws ground-station investors.

Europe holds a stable 15-18% share, constrained by fragmented procurement and slower spectrum coordination. OneWeb completed its 634-satellite fleet and targets enterprise connectivity. ESA's three-satellite CO2M program supports the EU Carbon Border Adjustment Mechanism, tying Earth-observation demand to climate policy. Middle East wealth funds back domestic platforms through Western joint ventures. South America sees steady growth as Brazil's BNDES finances indigenous manufacturing, while Satellogic's Uruguay plant ships 35-kg buses for agriculture analytics.

- Space Exploration Technologies Corp.

- Airbus SE

- Lockheed Martin Corporartion

- GomSpace Group AB

- ICEYE Oy

- AAC Clyde Space AB

- OHB SE

- Surrey Satellite Technology Ltd.

- Thales Alenia Space

- L3Harris Technologies, Inc.

- Sierra Space Corporation

- Planet Labs PBC

- Northrop Grumman Corporation

- Kongsberg NanoAvionics UAB (Kongsberg Gruppen ASA)

- Blue Canyon Technologies, LLC (RTX Corporation)

- NSIL Corporation Limited

- Chang Guang Satellite Technology Co. Ltd.

- German Orbital Systems GmbH

- Satellogic Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Reusable-launch cost collapse

- 4.2.2 LEO broadband mega-constellations boom

- 4.2.3 Multi-sector demand for Earth-observation analytics

- 4.2.4 National-security shift to proliferated LEO fleets

- 4.2.5 Climate-compliance monitoring mandates

- 4.2.6 Export-credit support for domestic constellations

- 4.3 Market Restraints

- 4.3.1 Spectrum-licensing bottlenecks

- 4.3.2 Space-debris mitigation costs

- 4.3.3 Single-source supply of rad-hard components

- 4.3.4 Increased VLEO drag during solar maximum

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 By Orbit

- 5.2.1 Low Earth Orbit (LEO)

- 5.2.2 Medium Earth Orbit (MEO)

- 5.2.3 Geostationary Orbit (GEO)

- 5.3 By End-User

- 5.3.1 Commercial

- 5.3.2 Government and Civil

- 5.3.3 Military

- 5.4 By Satellite Mass

- 5.4.1 Femtosatellites

- 5.4.2 Picosatellites

- 5.4.3 Nanosatellites

- 5.4.4 Microsatellites

- 5.4.5 Minisatellites

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Space Exploration Technologies Corp.

- 6.4.2 Airbus SE

- 6.4.3 Lockheed Martin Corporartion

- 6.4.4 GomSpace Group AB

- 6.4.5 ICEYE Oy

- 6.4.6 AAC Clyde Space AB

- 6.4.7 OHB SE

- 6.4.8 Surrey Satellite Technology Ltd.

- 6.4.9 Thales Alenia Space

- 6.4.10 L3Harris Technologies, Inc.

- 6.4.11 Sierra Space Corporation

- 6.4.12 Planet Labs PBC

- 6.4.13 Northrop Grumman Corporation

- 6.4.14 Kongsberg NanoAvionics UAB (Kongsberg Gruppen ASA)

- 6.4.15 Blue Canyon Technologies, LLC (RTX Corporation)

- 6.4.16 NSIL Corporation Limited

- 6.4.17 Chang Guang Satellite Technology Co. Ltd.

- 6.4.18 German Orbital Systems GmbH

- 6.4.19 Satellogic Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment