|

시장보고서

상품코드

2066591

유럽의 소형 위성 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Small Satellite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

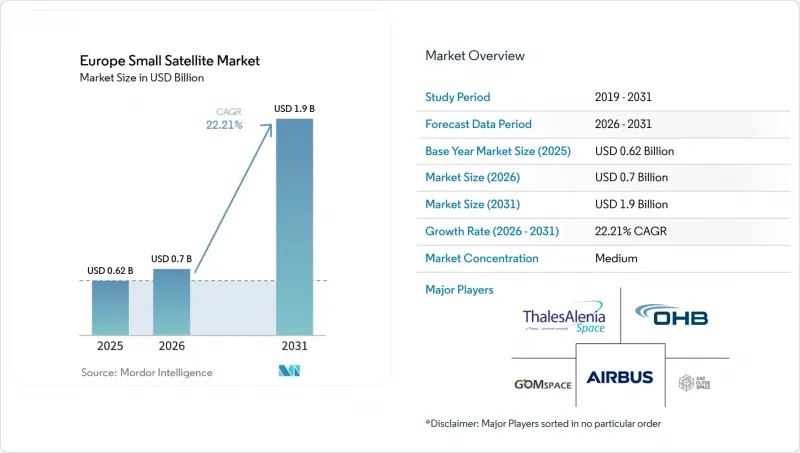

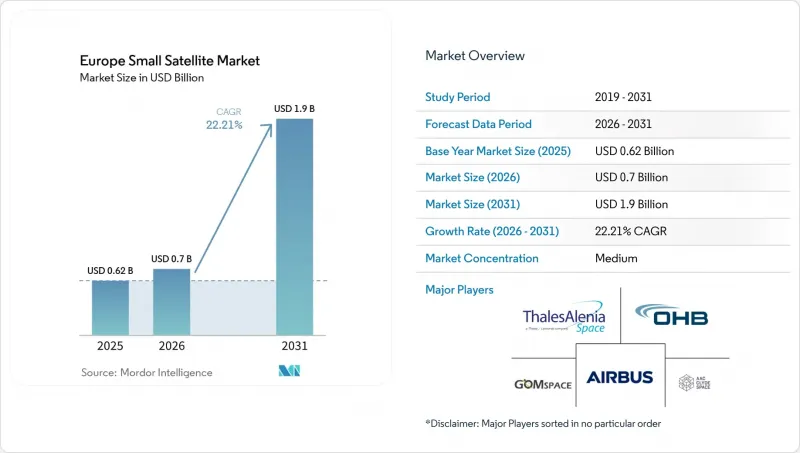

Mordor Intelligence에 의하면, 유럽의 소형 위성 시장 규모는 2025년 6억 2,000만 달러로 평가되었고, 2026년 7억 달러로 추정되고, 2031년까지 19억 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 22.21%를 나타낼 전망입니다.

본 보고서는 용도별(통신, 지구관측, 항법, 우주 관측, 기타), 궤도별(LEO, MEO, GEO), 최종 사용자별(상업, 정부·민간, 군사), 위성 질량별(펨토 위성, 피코 위성, 나노 위성 등) 및 지역별(영국, 프랑스, 독일 등)로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

유럽의 소형 위성 시장 동향 및 인사이트

유럽에서 지구관측 위성군 프로그램의 급증

정부가 지원하는 지구관측 위성 군은 유럽의 소형 위성 시장에서 가장 뚜렷한 구조적 수요 촉진요인으로 작용하고 있습니다. 이탈리아의 IRIDE 프로그램은 6개의 위성 군집에 걸쳐 총 68기의 위성을 대상으로 하고 있으며, 2026년 3월까지 이미 16기의 Eaglet II 위성이 궤도에 투입되었으며, 2027년까지 완전한 배치를 목표로 하고 있습니다. 그리스도 국가 소형 위성 프로그램에 1억 3,000만 유로(1억 5,133만 달러)를 지원하기로 결정했습니다. 이 자금은 산불 감지, 해상 감시, 농업 모니터링에 중점을 둔 13기의 위성에 투입될 예정입니다. 이러한 프로그램들은 단순히 수주를 창출하는 데 그치지 않고, 이후의 상업 임무를 위한 기술 인증 주기를 단축하며, 유럽 소형 위성 시장에 진출하는 사업자들의 실행 위험을 줄이는 역할도 하고 있습니다. 유럽우주국(ESA)의 ‘FutureEO Scout’ 시리즈에는 현재 HydroGNSS 외에도 새로 승인된 Hibidis 및 SOVA-S 임무가 포함되어 있으며, 이는 소형 저비용 플랫폼이 단순한 대안 차원을 넘어 표준적인 과학적 선택지로 자리 잡고 있음을 보여줍니다.

유럽의 신생 우주 스타트업으로의 벤처 캐피털 유입 확대

2025년에는 민간 자본의 유입이 다시 증가하면서 유럽의 소형 위성 시장에 폭넓은 자금 기반을 마련해 주었습니다. ESPI의 『Space Venture 2025』 보고서에 따르면, 2025년 유럽의 우주 벤처 기업들은 14억 유로(16억 2,000만 달러)의 민간 투자를 유치했으며, 벤처 캐피털의 투자액은 전년 대비 13% 증가한 12억 유로(13억 9,000만 달러)에 달했습니다. 자금 조달 현황을 살펴보면, 독일이 1위를 차지했고, 핀란드, 프랑스, 불가리아, 영국이 그 뒤를 이었습니다. 이는 자본 형성이 단일 국가 클러스터를 넘어 확산되고 있음을 뒷받침합니다. 동시에, 2024년과 2025년 모두에서 보안 및 방위 관련 기업이 유럽의 우주 투자 총액의 30%를 차지하고 있어, 상업 및 방위 분야의 자금 조달 경로가 점점 더 융합되고 있음을 보여줍니다. 2025년의 자금 조달 상황은 여전히 불균형한 상태가 지속되고 있습니다. 이는 2025년 자금 조달 라운드 상위 5건이 6억 2,900만 유로(7억 3,220만 달러)를 차지했기 때문이며, 이로 인해 소규모 플랫폼 개발 기업과 데이터 기업들은 어려운 상황에 처하게 되어, 2차 기업들 간의 통합이 진행될 가능성이 높아지고 있습니다.

전용 마이크로 로켓공급 부족과 비용 상승

유럽 소형 위성 시장에서 가장 시급한 구조적 제약은 운용 가능한 자국산 마이크로 발사 수단이 없습니다는 점입니다. 2026년 초 현재, 유럽산 소형 발사체 중 상업적 궤도 진입에 성공한 사례는 없으며, Isar Aerospace의 ‘Spectrum’ 로켓은 2026년 5월 궤도 적격성 시험을 목표로 하고 있었으나, Orbex는 2026년 2월에 사업을 중단했습니다. 이에 대해 ESA는 2025년 7월, ‘European Launcher Challenge’ 참가 기업으로 5개사를 예비 선정했으며, 각 기업에는 최대 1억 6,900만 유로(1억 9,673만 달러) 규모의 계약이 부여될 예정입니다. 현지에서의 발사 빈도가 개선될 때까지는 사업자들이 여전히 미국의 공동 발사에 대한 일정 의존도, 환율 리스크, 그리고 유럽의 신규 발사 시스템에 대한 비행 실적이 부족하여 보험사로부터의 신뢰가 제한적이라는 과제에 직면하게 될 것입니다. 기아나 우주 센터에 위치한 CNES의 ELM-Diamant 복합 시설은 2026년 이후 물리적 발사 기반을 강화할 예정이지만, 인프라만으로는 단기적으로 발사 빈도 문제를 해결할 수 없습니다.

부문별 분석

2025년 유럽 소형 위성 시장에서 지구관측이 38.32%를 차지했습니다. 이는 코페르니쿠스 관련 임무의 긴 조달 주기, IRIDE의 전개, 그리고 각국의 관측 의무화 정책에 힘입은 결과입니다. 이러한 점유율은 현재 수요를 상회하는 수준을 반영하고 있는데, 이는 많은 유럽 정부들이 현재 관측 위성을 단순한 선택적 프로그램 자산이 아닌 핵심 공공 인프라로 간주하고 있기 때문입니다. 그리스의 국가 소형 위성 프로그램은 이러한 변화를 명확히 보여주고 있으며, ESA가 관리하는 체계 하에서 열·광학·레이더 모니터링용 위성 13기를 계획하고 있습니다. 또한 에어버스는 2026년 1월 ‘Pleiades Neo Next’ 프로그램을 발표하며 이 부문의 고해상도 분야를 강화했습니다. 이 프로그램에서는 2028년 초에 첫 발사가 예정되어 있으며, 20cm급의 원본 해상도 이미지를 제공할 계획입니다.

통신은 가장 빠르게 성장하고 있는 분야이며, 이 분야의 유럽 소형 위성 시장 규모는 2031년까지 연평균 성장률(CAGR) 23.17%로 확대될 것으로 전망됩니다. IRIS2는 272기의 저궤도(LEO) 위성이 통신 계층을 제공하며, 매우 많은 기관으로부터의 미수주 물량을 보유하고 있어 여전히 주요 축으로 자리 잡고 있습니다. 동시에, ‘GOVSATCOM’은 이미 운영 단계에 접어들었으며, 회원국 전반에 걸친 실용적이고 안전한 연결의 활용 사례를 입증하고 있습니다. 여기에서는 임무 구성에 따라 동일한 노드가 암호화 통신, 해상 감시, IoT 백홀 또는 센서 중계를 지원할 수 있으므로, 듀얼 유스(군민 겸용) 능력이 더욱 두드러지게 나타납니다. 항법 및 우주 관측은 절대적인 규모로 볼 때 여전히 미미한 수준이지만, ESA의 ‘Celeste’ 콘스텔레이션은 LEO(저궤도) 기반의 위치 정보 검증이 유럽 소형 위성 산업에서 정책적 중요성을 더해가고 있음을 보여주고 있습니다. 기술 실증 및 IoT 임무를 포함하는 ‘기타’ 부문은 기업 차원에서는 여전히 분산된 상태이지만, 기기에서 위성으로의 통신에 관한 규제와 서비스 모델이 성숙해짐에 따라 의미 있는 수요 기반을 구축해 나가고 있습니다.

저궤도(LEO)는 2025년에 75.15%의 점유율을 차지한 것으로 평가되었으며, 지구관측, IoT 및 보안 통신 분야에서 재방문 간격, 지연 시간, 발사 비용에 대한 요건을 충족하기 위해 유럽 소형 위성 시장에서 여전히 명확한 운영의 핵심을 이루고 있습니다. 이탈리아의 IRIDE 프로그램은 이 궤도가 현재 공공 조달에 얼마나 깊이 뿌리내리고 있는지를 보여주고 있으며, 2026년 3월까지 이미 16기의 Eaglet II 위성이 궤도에 투입되었고, 6개의 위성군에 걸쳐 총 68기의 위성을 배치하는 계획이 진행되고 있습니다. LEO를 상업적으로 매력적으로 만드는 이러한 높은 밀도가, 동시에 운영상의 부담도 가중시키고 있습니다. 현재 충돌 회피나 우주 쓰레기에의 노출이 위성의 수명 예측과 보험료율에 영향을 미치고 있기 때문입니다. GEO는 기존의 방송 및 고정형 광대역 서비스에 있어 여전히 중요하지만, 유럽의 소형 위성 분야에서 추가적인 성장이 기대되는 분야는 아닙니다.

중궤도(MEO)는 가장 빠르게 성장하고 있는 궤도로, 이 궤도층에서 유럽 소형 위성 시장 규모는 2031년까지 연평균 성장률(CAGR) 23.81%로 확대될 것으로 전망됩니다. 주요 수요 요인으로는 18기의 MEO 위성으로 구성된 IRIS2의 하이브리드 아키텍처, 갈릴레오 2세대 개발의 지속, 그리고 ESA가 추진하는 하이브리드 신호 전송 실증 프로젝트 ‘셀레스테’를 들 수 있습니다. 비 GSO 시스템에 관한 조정 절차도 여기서 중요합니다. 규제상 리드타임이 2-5년 걸리기 때문에 조기에 신청을 하여 주파수 조정을 신속하게 진행할 수 있는 사업자가 점점 더 유리해지기 때문입니다. 또한 유럽에서는 유럽방위청(EDA)의 LEO2VLEO 이니셔티브와 2026년 3월에 체결된 VLEO-DEF 계약을 통해 더 낮은 주파수 대역에서의 운용 시험이 진행되고 있으며, 이를 통해 예측 기간 내에 상업적으로 의미 있는 궤도 등급이 추가될 가능성이 있습니다. 그렇긴 하지만, 2031년까지의 유럽 소형 위성 시장에서 LEO와 MEO의 조합이 여전히 주요 성장 경로가 될 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the europe small satellite market size is projected to expand from USD 0.62 billion in 2025 and USD 0.70 billion in 2026 to USD 1.90 billion by 2031, registering a 22.21% CAGR between 2026 and 2031.

This report is Segmented by Application (Communication, Earth Observation, Navigation, Space Observation, and Others), Orbit (LEO, MEO, and GEO), End-User (Commercial, Government and Civil, and Military), Satellite Mass (Femtosatellites, Picosatellites, Nanosatellites, and More), and Geography (United Kingdom, France, Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Small Satellite Market Trends and Insights

Surge in European Earth-observation Constellation Programs

Government-backed Earth observation constellations have become the clearest structural demand driver in the Europe small satellite market. Italy's IRIDE program covers 68 satellites across 6 constellations, and 16 Eaglet II satellites were already in orbit by March 2026, with full deployment targeted by 2027. Greece also committed EUR 130 million (USD 151.33 million) to its National Small Satellite Program, which will fund 13 satellites focused on wildfire detection, maritime awareness, and agricultural monitoring. These programs do more than create orders; they shorten technology qualification cycles for later commercial missions and lower perceived execution risk for operators entering the Europe small satellite market. European Space Agency's (ESA's) FutureEO Scout line now includes HydroGNSS and newly approved Hibidis and SOVA-S missions, demonstrating that compact, lower-cost platforms are becoming a standard scientific option rather than a fallback.

Growing Venture-capital Inflows into Europe NewSpace Start-ups

Private capital inflows strengthened again in 2025, providing the Europe small satellite market with a broader financing base. European space ventures attracted EUR 1.4 billion (USD 1.62 billion) in private investment in 2025, while venture capital rose 13% year over year to EUR 1.2 billion (USD 1.39 billion) according to ESPI's Space Venture 2025 report. Germany led that funding map, followed by Finland, France, Bulgaria, and the UK, which confirms that capital formation is spreading beyond a single national cluster. At the same time, security- and defense-oriented companies accounted for 30% of total European space investment in both 2024 and 2025, indicating that commercial and defense funding channels are increasingly converging. The funding picture remains uneven because the 5 largest rounds in 2025 accounted for EUR 629 million (USD 732.20 million), keeping smaller platform developers and data firms under pressure and raising the likelihood of consolidation across the second tier.

Limited Availability and Rising Costs of Dedicated Micro-launch Vehicles

The most immediate structural constraint on the Europe small satellite market is the absence of an operational indigenous micro-launch option. No European micro-launcher had achieved commercial orbital delivery by early 2026, while Isar Aerospace's Spectrum vehicle was targeting orbital qualification in May 2026, and Orbex ceased operations in February 2026. ESA responded in July 2025 by preselecting 5 companies for the European Launcher Challenge, with each eligible for contracts of up to EUR 169 million (USD 196.73 million). Until local cadence improves, operators still face scheduling dependency on US rideshares, currency exposure, and limited insurer confidence because flight heritage remains thin for new European launch systems. CNES's ELM-Diamant complex at the Guiana Space Centre improves the physical launch base from 2026 onward, but infrastructure alone does not solve cadence in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Europe Defence Fund Backing Small-satellite ISR Assets

- Europe Green Deal Climate-monitoring Targets Boosting Demand

- Satellite insurance premiums rising for less than 50 kg class

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Earth observation accounted for 38.32% of the Europe small satellite market in 2025, supported by the long procurement cycle for Copernicus-linked missions, the IRIDE deployment, and national sensing mandates. That position reflects more than current demand because many European governments now treat observation satellites as core public infrastructure rather than optional program assets. Greece's National Small Satellite Program clearly shows that shift, with 13 satellites planned for thermal, optical, and radar monitoring under an ESA-managed framework. Airbus also strengthened the high-resolution end of this segment in January 2026, when it announced the Pleiades Neo Next program, with the first launch planned for early 2028 and 20 cm-class native-resolution imagery.

Communication is the fastest-growing application, and the Europe small satellite market size for this segment is projected to expand at a 23.17% CAGR through 2031. IRIS2 remains the main anchor because its 272 LEO satellites provide the communication layer with a very large institutional backlog. At the same time, GOVSATCOM has already moved into operations and demonstrates a practical, secure connectivity use case across member states, where dual-use capability becomes more visible because the same node can support encrypted communications, maritime awareness, IoT backhaul, or sensor relay depending on the mission stack. Navigation and space observation remain smaller in absolute terms, but ESA's Celeste constellation shows that LEO-based positioning validation is gaining policy importance within the European small satellite industry. The others category, which includes technology demonstrations and IoT missions, remains fragmented at the company level but is still building a meaningful pool of demand as device-to-satellite rules and service models mature.

Low Earth Orbit (LEO) held a 75.15% share in 2025 and remains the clear operational center of the Europe small satellite market because it meets the revisit, latency, and launch-cost needs of Earth observation, IoT, and secure communications. Italy's IRIDE program shows how deeply this orbit is now embedded in public procurement, with 16 Eaglet II satellites already in orbit by March 2026 and a path to 68 satellites across 6 constellations. The same density that makes LEO commercially attractive is also raising its operating burden, since conjunction avoidance and debris exposure are now affecting lifetime assumptions and insurance pricing. GEO still matters for legacy broadcast and fixed broadband services, but it is not where incremental growth is occurring in the European small-satellite class.

Medium Earth Orbit (MEO) is the fastest-growing orbit, and the Europe small satellite market size for this layer is projected to rise at a 23.81% CAGR through 2031. The main demand logic comes from IRIS2's hybrid architecture with 18 MEO satellites, continued Galileo second-generation development, and ESA's Celeste demonstration work on hybrid signal delivery. Coordination procedures for non-GSO systems also matter here because regulatory lead times of 2 to 5 years increasingly favor operators that filed early and can move faster through spectrum coordination. Europe is also testing lower operating bands through the European Defence Agency's LEO2VLEO effort and the VLEO-DEF contract signed in March 2026, which may add a commercially relevant orbit class within the forecast window. Even so, LEO and MEO together remain the main growth path for the Europe small satellite market through 2031.

List of Companies Covered in this Report:

- Airbus SE

- Innovative Solutions In Space B.V.

- ICEYE Oy

- AAC Clyde Space AB

- OHB SE

- Surrey Satellite Technology Ltd.

- Thales Alenia Space

- EnduroSat AD

- SatRev S.A.

- Planet Labs PBC

- HEMERIA

- GomSpace A/S

- UAB Kongsberg NanoAvionics (Kongsberg Gruppen ASA)

- Exotrail

- Berlin Space Technologies GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Europe Defence Fund backing small-satellite ISR assets

- 4.2.2 Surge in European Earth-observation constellation programs

- 4.2.3 Europe Green Deal climate-monitoring targets boosting demand

- 4.2.4 Growing venture-capital inflows into Europe NewSpace start-ups

- 4.2.5 Institutional demand for in-orbit servicing and debris removal

- 4.2.6 Tightened launch-window availability spurring rideshare-optimization tools

- 4.3 Market Restraints

- 4.3.1 Limited availability and rising costs of dedicated micro-launch vehicles

- 4.3.2 Spectrum-allocation bottlenecks at ITU and CEPT

- 4.3.3 Satellite insurance premiums rising for less than 50 kg class

- 4.3.4 Export-control regime divergence within Europe

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 By Orbit

- 5.2.1 Low Earth Orbit (LEO)

- 5.2.2 Medium Earth Orbit (MEO)

- 5.2.3 Geostationary Orbit (GEO)

- 5.3 By End-User

- 5.3.1 Commercial

- 5.3.2 Government and Civil

- 5.3.3 Military

- 5.4 By Satellite Mass

- 5.4.1 Femtosatellites

- 5.4.2 Picosatellites

- 5.4.3 Nanosatellites

- 5.4.4 Microsatellites

- 5.4.5 Minisatellites

- 5.5 By Geography

- 5.5.1 United Kingdom

- 5.5.2 France

- 5.5.3 Germany

- 5.5.4 Russia

- 5.5.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Airbus SE

- 6.4.2 Innovative Solutions In Space B.V.

- 6.4.3 ICEYE Oy

- 6.4.4 AAC Clyde Space AB

- 6.4.5 OHB SE

- 6.4.6 Surrey Satellite Technology Ltd.

- 6.4.7 Thales Alenia Space

- 6.4.8 EnduroSat AD

- 6.4.9 SatRev S.A.

- 6.4.10 Planet Labs PBC

- 6.4.11 HEMERIA

- 6.4.12 GomSpace A/S

- 6.4.13 UAB Kongsberg NanoAvionics (Kongsberg Gruppen ASA)

- 6.4.14 Exotrail

- 6.4.15 Berlin Space Technologies GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment