|

시장보고서

상품코드

2066438

중국의 공장 자동화 및 산업 제어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China Factory Automation And Industrial Controls - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

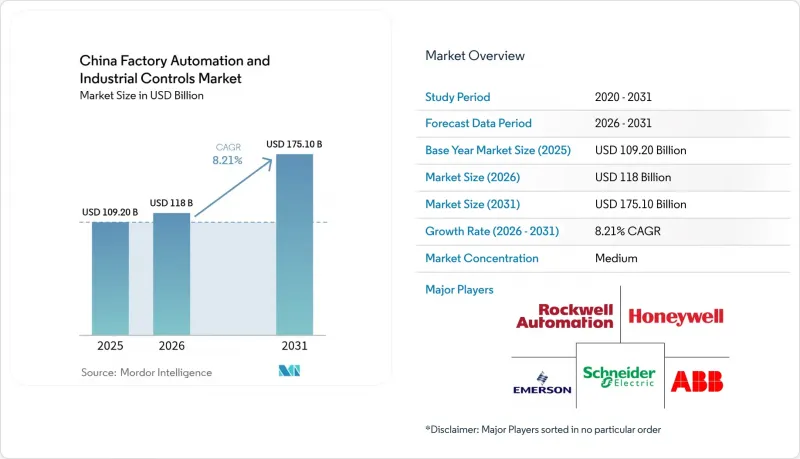

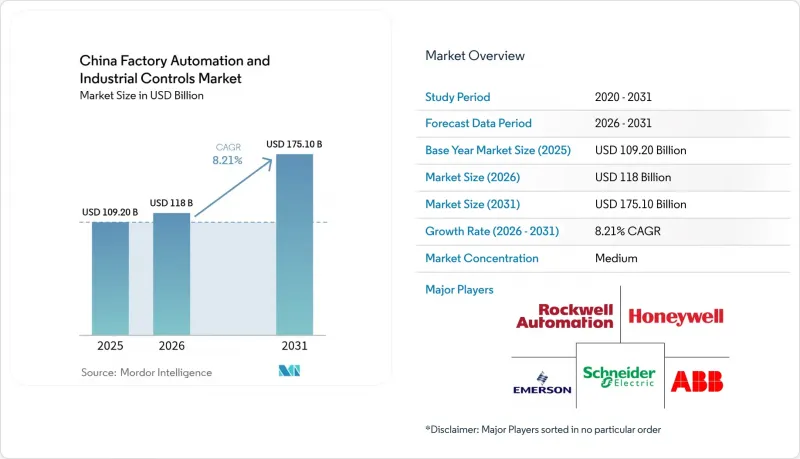

Mordor Intelligence에 의하면, 중국의 공장 자동화 및 산업 제어 시장 규모는 2025년에 1,092억 달러로 평가되었습니다. 2026년에 1,180억 달러에 달하고, 2031년까지 1,751억 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 8.21%로 성장할 전망입니다.

본 보고서는 구성 요소(하드웨어, 소프트웨어 등), 제어 시스템의 유형(분산 제어 시스템(DCS), 프로그래머블 로직 컨트롤러(PLC) 등), 최종 사용자 산업(자동차·EV, 일렉트로믹스 및 반도체 등), 자동화 솔루션의 유형(디스크리트 자동화 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국의 공장 자동화 및 산업 제어 시장 동향 및 인사이트

‘중국 제조 2025’에 따른 스마트 제조로의 전환을 위한 정부의 인센티브

중국 정부는 세계 최대 규모의 산업 정책 프로그램 중 하나를 추진하고 있으며, 1조 위안 규모의 정부 계열 벤처 펀드와 2025년까지 핵심 자동화 부품의 70%를 국산화하도록 의무화하는 공업정보화부(MIIT)의 지침을 결합했습니다. 중소기업을 대상으로 한 자동화 개보수 사업에는 97억 달러 상당의 주정부 차원의 보조금이 배정되어 있어, 자원이 제한적인 공장이라도 협동 로봇이나 엣지 컴퓨팅 허브를 도입할 수 있게 되었습니다. 조달 우대 조치, 세금 환급, 신속한 승인 절차가 어우러져 현지화된 공급망, 더욱 경쟁력 있는 가격 책정, 그리고 신속한 기술 도입이라는 선순환을 만들어내고 있습니다. 자동화 공급업체는 확실한 수요의 혜택을 누리는 한편, 제조업체는 높은 처리량, 안정적인 품질, 낮은 에너지 소비를 실현하는 상호 연결된 생산 라인을 통해 더 빠른 투자 회수(ROI)를 달성할 수 있습니다. 또한, 이 일련의 정책에는 데이터 주권 요건도 포함되어 있어, 기밀성이 높은 현장 데이터를 중국 국경 내에 보관하는 국내 IIoT 플랫폼의 보급을 촉진하고 있습니다.

전기자동차(EV) 및 배터리 기가팩토리를 통한 유연한 생산에 대한 수요 증가

전기자동차(EV) OEM 제조업체와 배터리 제조업체들은 전례 없는 속도로 생산 규모를 확대하고 있으며, 모듈식이며 AI를 활용한 자동화에 대한 수요가 급증하고 있습니다. CATL, BYD, Gotion은 2024년, 연중무휴 24시간 리튬 이온 배터리 생산을 뒷받침하면서 99.5%의 품질 검사 정확도를 달성하기 위해 2만 대 이상의 로봇을 도입했습니다. XPeng이 138억 달러를 투자하는 휴머노이드 로봇 프로젝트는 단일 시설 내에서 여러 차종을 생산할 수 있는 유연한 생산 라인의 필요성을 부각시키고 있습니다. 테슬라의 상하이 기가팩토리는 연간 75만 대라는 생산 기준을 세웠지만, 중국의 경쟁사들은 디지털 트윈과 PLC 및 로봇을 연동한 아키텍처를 통해 이 수준을 재현하고자 하고 있습니다. 이러한 노력은 국내 공급업체가 제조하는 모션 컨트롤러, 드라이브, 머신 비전 시스템에 대한 장기적인 수주를 공고히 하고, 중국의 공장 자동화 및 산업 제어 시장을 한층 더 활성화시키고 있습니다.

레거시 OT 시스템의 사이버 보안 취약점

‘INCONTROLLER’ 악성코드 사건은 인터넷 연결을 염두에 두고 설계되지 않았던 수십년전의 PLC 및 SCADA 노드에 심각한 취약점이 존재함을 드러냈습니다. 공장이 분석을 위해 IIoT 클라우드에 연결됨에 따라, 이러한 취약점은 랜섬웨어, 지적 재산권 도용, 그리고 잠재적인 안전 사고를 초래하는 요인이 되고 있습니다. 운영 담당자는 현재 생산 네트워크에 제로 트러스트 아키텍처, 로컬 데이터센터, 지속적인 패치 적용 절차를 다층적으로 도입해야 하며, 이로 인해 자본 지출(CAPEX)과 프로젝트 기간이 늘어나고 있습니다. 지정학적 긴장이 고조됨에 따라 외국산 펌웨어 및 칩셋에 대한 감시가 강화되고 있어, 성능이 동등하더라도 구매자들은 신뢰할 수 있는 국내 공급업체를 선택하고 있습니다. 이러한 당면한 설비 투자 부담으로 인해, 본래라면 견조했을 중국의 공장 자동화 및 산업 제어 시장의 연평균 성장률(CAGR)이 소폭 억제되고 있습니다.

부문별 분석

하드웨어 부문은 로봇 및 서보 드라이브 도입 대수가 사상 최고치를 기록한 데 힘입어 2025년 매출의 59.98%를 차지했으나, 공장들이 AI를 활용한 최적화를 추구하는 가운데 소프트웨어 부문은 연평균 성장률(CAGR) 12.54%로 성장할 전망입니다. 국내 로봇 제조업체들은 현지 시장 점유율을 2015년 17.5%에서 2024년에는 32%로 끌어올리며, 적재 중량, 재현성, 평균 고장 간격(MTBF) 등의 지표에서 급속한 추격을 보였습니다.

서비스 부문은 현재 시장 점유율이 가장 낮은 분야임에도 불구하고, 시스템 통합, 운영자 역량 강화, 라이프사이클 지원에 대한 안정적인 수요를 확보하고 있어 연금형 현금 흐름을 형성하고 있습니다. 도입이 확대됨에 따라 제조업체들은 기계 설치에서 데이터 기반의 성능 향상으로 초점을 전환하고 있으며, 고정자산 수익률을 높이는 MES, APS, 디지털 트윈에 예산을 배정하고 있습니다. 그 결과, 선순환이 만들어집니다. 첨단 소프트웨어는 기존 기계에서 더 높은 처리량을 이끌어내고, 추가 투자를 촉진하며, 중국의 공장 자동화 및 산업 제어 시장에서 성장세를 지속시킬 것입니다.

프로그래머블 로직 컨트롤러(PLC)는 2025년에 32.24%라는 압도적인 시장 점유율을 차지했으며, 2031년까지 연평균 성장률(CAGR) 11.62%를 기록할 전망으로, 이산 제조 및 공정 플랜트 양쪽 모두에서 그 핵심적인 역할을 확고히 하고 있습니다. Inovance Technology나 STEP Electric과 같은 국내 기업들은 현지 지원과 경쟁력 있는 가격 정책, 그리고 중국 기준에 맞추어 조정된 펌웨어를 결합함으로써 유럽과 미국의 대형 기업들이 가진 선두 위치를 꾸준히 좁혀가고 있습니다.

중소기업들이 단일 용도의 작업 스테이션을 자동화함에 따라 소형 PLC 시장은 5.6%의 성장률을 기록하고 있지만, 석유화학 및 전력 분야의 미션 크리티컬 용도에서는 중대형 모델 부문에서 여전히 다국적 기업들이 우위를 점하고 있습니다. 연속 생산 산업에서는 상호 보완적인 SCADA 및 DCS 계층이 활발히 도입되고 있는 반면, HMI 패널은 새로운 로봇 셀이 도입될 때마다 그 규모가 확대되고 있습니다. 모션 컨트롤러에 대한 수요는 로봇 공학의 급속한 성장을 반영하고 있으며, 중국의 공장 자동화 산업의 모든 분야에서 성장을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the china factory automation and industrial controls market size is projected to be USD 109.20 billion in 2025, USD 118 billion in 2026, and reach USD 175.10 billion by 2031, growing at a CAGR of 8.21% from 2026 to 2031.

This report is Segmented by Component (Hardware, Software, and More), Control System Type (Distributed Control Systems (DCS), Programmable Logic Controllers (PLC), and More), End-User Industry (Automotive and EV, Electronics and Semiconductor, and More), Automation Solution (Discrete Automation, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Factory Automation And Industrial Controls Market Trends and Insights

Government Incentives for Made-in-China 2025 Smart Manufacturing Upgrades

Beijing orchestrates one of the world's largest industrial-policy programs, coupling a CNY 1 trillion state-backed venture fund with MIIT guidelines that require 70% domestic content in core automation parts by 2025. Provincial subsidies worth USD 9.7 billion are earmarked for SME automation retrofits, allowing even resource-constrained factories to deploy collaborative robots and edge-computing hubs. Together, procurement preferences, tax rebates, and fast-track approvals create a self-reinforcing cycle of localized supply chains, more competitive pricing, and quick technology adoption. Automation vendors benefit from guaranteed demand, while manufacturers gain faster ROI from interconnected production lines that deliver higher throughput, consistent quality, and lower energy consumption. The policy suite also embeds data-sovereignty requirements, driving uptake of domestic IIoT platforms that keep sensitive shop-floor data within China's borders.

Accelerated Demand for Flexible Manufacturing from EV and Battery Gigafactories

Electric-vehicle OEMs and cell makers are scaling production at unprecedented speed, driving a surge in demand for modular, AI-driven automation. CATL, BYD, and Gotion deployed more than 20,000 robots in 2024 to support 24/7 lithium-ion cell output while achieving 99.5% quality-inspection accuracy. XPeng's USD 13.8 billion humanoid-robotics initiative underscores the need for agile lines capable of multivehicle production in a single facility. Tesla's Shanghai Gigafactory has set a 750,000-unit annual benchmark that Chinese rivals aim to replicate through digital twins and synchronized PLC-robot architectures. These programs anchor long-term orders for motion controllers, drives, and machine-vision systems made by domestic suppliers, further lifting the China Factory Automation and Industrial Controls Market.

Cyber-Security Vulnerabilities in Legacy OT Systems

The INCONTROLLER malware episode exposed gaping holes in decades-old PLCs and SCADA nodes that were never designed for Internet connectivity. As factories connect to IIoT clouds for analytics, these soft spots invite ransomware, intellectual-property theft, and potential safety incidents. Operators must now layer zero-trust architectures, local data centers, and continuous patching routines onto production networks, inflating capex and project timelines. Heightened geopolitical tensions intensify scrutiny of foreign firmware and chipsets, nudging buyers toward trusted domestic vendors even when performance is on par. The immediate capex burden slightly tempers the otherwise robust CAGR of the China Factory Automation and Industrial Controls Market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Industrial Internet-of-Things (IIoT) Platforms

- Edge-AI-Based Predictive Maintenance Reducing Unplanned Downtime

- Fragmented Industrial Communication Standards Hindering Interoperability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware contributed 59.98% of 2025 revenue, anchored by record robot and servo-drive installations, yet software is poised to grow at a 12.54% CAGR as factories chase AI-enabled optimization. Domestic robot vendors lifted their local share from 17.5% in 2015 to 32% in 2024, signaling rapid catch-up on payload, repeatability, and mean-time-between-failure metrics.

Services, though currently the smallest slice, secure consistent demand for systems integration, operator upskilling, and lifecycle support, forming annuity-style cash flows. As adoption deepens, manufacturers shift focus from mechanical installation to data-driven performance gains, rerouting budgets toward MES, APS, and digital twins that amplify return on fixed assets. The result is a virtuous cycle: advanced software squeezes extra throughput from existing machines, encouraging further investment and sustaining momentum in the China Factory Automation and Industrial Controls Market.

Programmable Logic Controllers held a commanding 32.24% share in 2025 and are on track to log an 11.62% CAGR to 2031, affirming their centrality in both discrete and process plants. Domestic firms such as Inovance Technology and STEP Electric steadily erode Western incumbents' leads by bundling local support with competitive pricing and firmware tuned for Chinese standards.

Small PLCs post 5.6% growth as SMEs automate single-purpose stations, while mid-to-large models still favor multinationals for mission-critical applications in petrochemicals and power. Complementary SCADA and DCS layers flourish in continuous industries, whereas HMI panels expand with each new robot cell. Motion-controller demand mirrors the robotics surge, underpinning growth across all nodes of the china factory automation industry.

List of Companies Covered in this Report:

- ABB Ltd.

- Siemens AG

- Schneider Electric SE

- Rockwell Automation, Inc.

- Mitsubishi Electric Corporation

- Omron Corporation

- Yokogawa Electric Corporation

- Honeywell International Inc.

- Emerson Electric Company

- Bosch Rexroth AG

- Fanuc Corporation

- Yaskawa Electric Corporation

- Delta Electronics, Inc.

- Advantech Co., Ltd.

- Panasonic Holdings Corporation

- Beckhoff Automation GmbH and Co. KG

- Keyence Corporation

- Fuji Electric Co., Ltd.

- Nidec Corporation

- Inovance Technology Co., Ltd.

- Shanghai STEP Electric Corporation

- Hollysys Automation Technologies Ltd.

- Zhejiang Supcon Technology Co., Ltd.

- Zhejiang Chint Electrics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of Industrial Internet-of-Things (IIoT) platforms

- 4.2.2 Government incentives for "Made-in-China 2025" smart-manufacturing upgrades

- 4.2.3 Accelerated demand for flexible manufacturing from EV and battery gigafactories

- 4.2.4 Edge-AI based predictive-maintenance reducing unplanned downtime

- 4.2.5 On-premise 5G private networks enabling ultra-reliable low-latency control

- 4.2.6 Rising labor-cost inflation driving robotic substitution in SMEs

- 4.3 Market Restraints

- 4.3.1 Cyber-security vulnerabilities in legacy OT systems

- 4.3.2 Fragmented industrial communication standards hindering interoperability

- 4.3.3 Shortage of domain-skilled automation engineers

- 4.3.4 Capital-expenditure freezes in export-oriented factories amid geo-economic risk

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Control System Type

- 5.2.1 Distributed Control Systems (DCS)

- 5.2.2 Programmable Logic Controllers (PLC)

- 5.2.3 Supervisory Control and Data Acquisition (SCADA)

- 5.2.4 Human-Machine Interface (HMI)

- 5.2.5 Motion Controllers and Drives

- 5.3 By End-User Industry

- 5.3.1 Automotive and EV

- 5.3.2 Electronics and Semiconductor

- 5.3.3 Food and Beverage

- 5.3.4 Chemicals and Petrochemicals

- 5.3.5 Metals and Mining

- 5.3.6 Other End-User Industries

- 5.4 By Automation Solution

- 5.4.1 Discrete Automation

- 5.4.2 Process Automation

- 5.4.3 Hybrid Automation

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Siemens AG

- 6.4.3 Schneider Electric SE

- 6.4.4 Rockwell Automation, Inc.

- 6.4.5 Mitsubishi Electric Corporation

- 6.4.6 Omron Corporation

- 6.4.7 Yokogawa Electric Corporation

- 6.4.8 Honeywell International Inc.

- 6.4.9 Emerson Electric Company

- 6.4.10 Bosch Rexroth AG

- 6.4.11 Fanuc Corporation

- 6.4.12 Yaskawa Electric Corporation

- 6.4.13 Delta Electronics, Inc.

- 6.4.14 Advantech Co., Ltd.

- 6.4.15 Panasonic Holdings Corporation

- 6.4.16 Beckhoff Automation GmbH and Co. KG

- 6.4.17 Keyence Corporation

- 6.4.18 Fuji Electric Co., Ltd.

- 6.4.19 Nidec Corporation

- 6.4.20 Inovance Technology Co., Ltd.

- 6.4.21 Shanghai STEP Electric Corporation

- 6.4.22 Hollysys Automation Technologies Ltd.

- 6.4.23 Zhejiang Supcon Technology Co., Ltd.

- 6.4.24 Zhejiang Chint Electrics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment