|

시장보고서

상품코드

2066576

암호화폐 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cryptocurrency - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

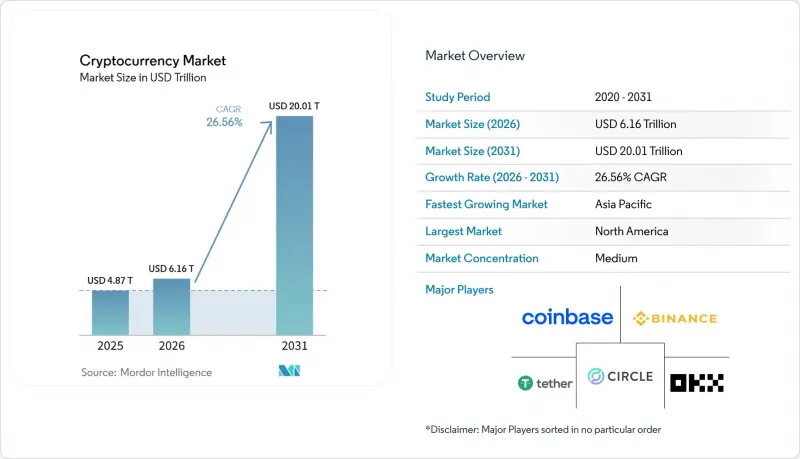

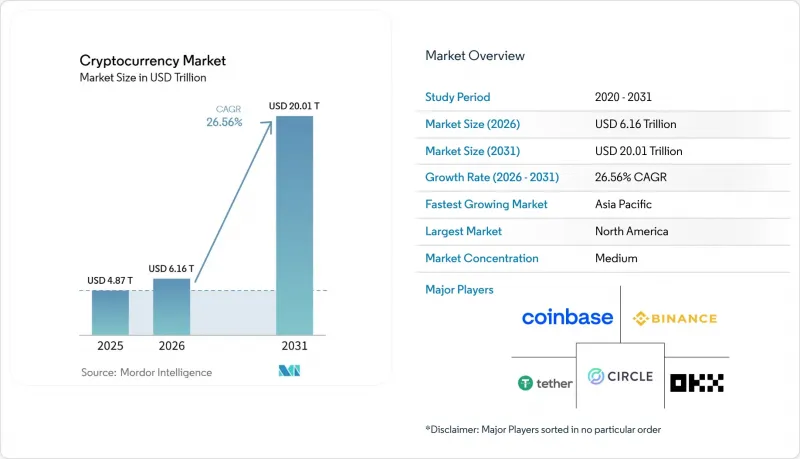

Mordor Intelligence에 의하면, 암호화폐 시장 규모는 2025년 4조 8,700억 달러로 평가되었습니다. 2026년에는 6조 1,600억 달러로 확대되어 2031년까지 20조 100억 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 26.56%로 성장할 전망입니다.

본 보고서는 거래 목적(결제·송금, 거래 및 투자 송금, 기타), 사용자 유형(개인, 기관), 암호화폐(BTC, ETH, 리플, 비트코인 캐시, 카르다노, 기타) 및 지역(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 암호화폐 시장 동향 및 인사이트

규제 대상인 현물 비트코인 ETF의 급증으로 기관 투자자의 자금 유입이 촉진되고 있습니다.

2024년 1월 미국에서 현물 비트코인 상장투자상품(ETP)이 승인됨에 따라, 투명성이 높고 규제가 잘 갖춰진 체계가 구축되었으며, 연금 기금, 기부 기금 및 자문 플랫폼을 통한 수탁 운용의 길이 열렸습니다. 이 상품 구조는 신중한 투자자 규정에 부합하고, 직접적인 수탁에 수반되는 운용상의 마찰을 줄여주었기 때문에 기관 투자자들 수요가 증가했으며, 이는 암호화폐 시장의 성장 추세를 뒷받침했습니다. 미국에서의 승인 및 규제 당국의 지속적인 관여는 다른 관할권에 대한 신호 효과를 높였으며, 규제 대상 시장에서 암호화폐 ETP 상품이나 멀티어셋 펀드 설계 등 상품 혁신의 흐름을 가속화했습니다. 수탁사의 투명한 준비금 공개와 감사받은 펀드 운영이 결합되어, 기관 투자자의 규정 준수 대응 체제가 강화되었으며, 실사 소요 시간이 단축되었습니다. 이러한 진전에 따라, 주요 투자 방침서에서 비트코인에 대한 노출도가 정상화되었으며, 시장에 참여하는 기관 투자자의 범위가 확대되었습니다.

유로존 전역에 MiCA가 도입됨에 따라, 조화로운 국경을 초월한 인프라가 구축될 것

‘암호자산 시장 규제(MiCA)’는 2024년 말 유럽연합(EU) 전역에서 완전히 시행되었으며, 각국마다 달랐던 규정을 대체하여 발행자 및 중개업체를 대상으로 한 단일 패스포트 제도가 도입되었습니다. 2025년 12월까지 100개가 넘는 암호화폐 서비스 제공업체가 MiCA의 인가를 받아 사업을 전개하게 되었으며, 이를 통해 단일 라이선스로 유럽경제지역(EEA) 전역의 고객에게 서비스를 제공할 수 있게 되어 중복되는 규정 준수 부담이 완화되었습니다. 스테이블코인 발행 및 보관 업무에 관한 통일된 규정에 따라 국경을 초월한 마찰이 완화되고 소비자 보호가 강화되었습니다. 그 결과, 이 지역의 암호화폐 시장에서 기관 투자자들의 신뢰가 높아지면서 서비스 확대가 이루어졌습니다. MiCA에 기반한 자본 및 위험 관리 요건으로 인해 시장 진입 장벽이 높아졌으며, 업무 회복력과 공시 기준을 충족하는 사업자들 간의 통합이 촉진되고 있습니다. 이는 2025년에는 규제를 준수하는 유로화 기반 스테이블코인이 보급되고, 지속적으로 진화하는 유럽 시장에서 규제 대상 결제 자산에 대한 수요가 높아지고 있음을 시사합니다.

전력망에 대한 반발과 채굴 활동의 일시 중단이 용량 확대를 제약

정책 입안자들과 송전망 운영자들은 에너지 집약적인 작업 증명(PoW) 운영으로 인한 전력 수요에 대해 우려를 표명했습니다. 이는 암호화폐 시장과 관련된 대규모 시설의 허가 절차 및 지속가능성에 관한 공시 요건에 영향을 미쳤습니다. 유럽의 규제 수립 과정에서는 금융 소비자 보호는 물론 기후 리스크 및 운용 리스크에 대한 공시가 중시되고 있으며, 이로 인해 사업 확대를 목표로 하는 기업들의 규정 준수 비용이 증가하고 있습니다. AI 워크로드로 인한 데이터센터용량 확보 경쟁이 심화되면서 전력 및 토지 이용에 따른 기회 비용이 증가했고, 이로 인해 일부 지역에서는 채굴 공급 확대가 제약을 받았습니다. 2025년 투자 결정에는 일부 컴퓨팅 인프라가 수익성이 높은 AI 용도으로 전환되는 추세가 반영되어, 시장 내 채굴 용량 확충의 여지가 줄어들었습니다. 이러한 압력은 중기적으로 효율성 향상과 입지 최적화로의 전환을 촉진하는 동시에, 독립형 재생에너지 및 에너지 시장 수요 반응(Demand Response) 참여의 정당성을 강화하고 있습니다.

부문별 분석

2025년, 거래 및 투자 이전은 암호화폐 시장 점유율의 49.52%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 31.24%로 성장할 것으로 전망됩니다. 이는 규제 대상 파생상품 및 거래소 거래로의 접근을 위한 구조적 전환을 반영한 것입니다. 규제를 준수하는 거래소로 전환함에 따라 유동성이 확대되고 거래 상대방 리스크가 감소하면서, 기관 투자자들이 시장에서 효율적으로 헤지 및 포트폴리오 재조정을 수행할 수 있는 능력이 강화되었습니다. 스테이블코인을 통한 결제는 플랫폼 간 담보 및 현금성 자산의 신속한 이동을 지속적으로 뒷받침하며, 자본 효율성과 시장의 반응성을 향상시켰습니다. 규제 대상 상품의 확대에 따라 운용 기준과 수탁 보증이 개선되어, 더 대규모의 거래와 폭넓은 참여가 촉진되었습니다. 그 결과, 암호화폐 시장에는 보다 명확한 리스크 관리 체계와 전통 금융과의 연계 지점을 갖춘, 더욱 견고한 거래 기반이 구축되었습니다.

결제·송금 분야에서는 규제 대상 발행사가 은행과의 제휴를 확대하고, 개인 및 법인의 활용 사례를 뒷받침하는 준법 체계를 확충함에 따라, 국경을 넘는 자금 이동에서 스테이블코인의 유용성이 높아져 그 혜택을 누렸습니다. ‘분산형 금융 프로토콜 플로우’ 부문에서는 리스크 관리 도구가 개선되고 있는 담보 대출, 유동성 공급, 토큰화된 담보 전략에 대해 재무 담당자와 시장 조성자들의 관심이 계속해서 집중되었습니다. 국경을 초월한 B2B 결제, 자산의 토큰화, NFT 관련 활동을 포함하는 ‘기타’ 카테고리는 2025년에 자산운용사가 온체인 펀드를 출범시키고 결제 네트워크와 함께 결제 시범 운영을 시작함에 따라 그 범위가 다양해졌습니다. 이러한 동향을 종합해 보면, 암호화폐 시장의 단기 거래량에서 결제와 거래가 가장 큰 비중을 차지하는 한편, 실용성의 조합이 더욱 광범위해지고 있음을 알 수 있습니다. 따라서 암호화폐 업계는 일상적인 자금 이동 및 전문적인 리스크 관리와 연계된 활용 사례에 맞추어 인프라와 규정 준수 체계를 구축해 나가고 있습니다.

지역별 분석

북미는 2025년에 35.38%의 점유율을 차지하며, 규제 대상 ETP, 기관용 수탁 서비스, 그리고 암호화폐 시장에 전문가들의 진입을 촉진하는 탄탄한 파생상품 시장으로부터 계속해서 혜택을 누렸습니다. 스테이블코인 및 거래소 감독과 관련된 미국의 정책 발전은 서비스 제공업체와 투자자에게 투명성을 높여주었으며, 유동성과 시장의 깊이를 뒷받침했습니다. 감사 절차를 거친 수탁 기관의 규모가 확대됨에 따라, 자산 운용사 및 기업의 재무 부서에 대한 접근성이 개선되었고, 대규모 자금 풀 시장 진입이 촉진되었습니다. 캐나다 및 국경을 넘는 송금 경로는 디지털 달러와 저비용 송금에 대한 수요 증가에 기여하며, 해당 지역 시장에서 실용성 중심의 성장을 뒷받침했습니다. 이러한 요소들이 복합적으로 작용하여, 제품의 폭, 규정 준수 및 기관 투자자들의 채택 측면에서 북미의 선도적 지위가 유지되었습니다.

아시아태평양은 결제 활용 사례, 지역별 규제 명확화, 그리고 암호화폐 시장과 관련된 결제 모델을 형성하기 위한 중앙은행의 실험을 배경으로, 2031년까지 연평균 성장률(CAGR) 29.24%를 기록하며 가장 빠르게 성장하는 지역이 될 것으로 전망됩니다. 규제 당국은 금융 허브 내에서 스테이블코인 및 중개업체를 대상으로 한 인허가 제도를 마련하고, 기관 투자자의 업무에 대한 안전 조치를 마련했습니다. 결제 플랫폼과 슈퍼앱은 소비자와 가맹점이 디지털 달러에 접근할 수 있는 기회를 확대함으로써, 송금 경로와 전자상거래 결제를 뒷받침했습니다. 여러 국가에 걸쳐 진행되는 시범 사업에서는 국경을 초월한 실시간 총액 결제 시험이 계속되고 있으며, 이는 시장과 연계된 지역 결제 시스템에서 공공 및 민간 토큰이 수행할 장기적인 역할을 보여주는 것입니다. 이러한 동향들이 맞물려 아시아태평양의 참여 확대와 인프라 투자를 뒷받침하고 있습니다.

MiCA를 중심으로 한 유럽의 체계는 27개 회원국 전체에 걸쳐 조화로운 라이선싱 환경을 구축하고, 중복되는 규정 준수 부담을 경감하는 패스포트 제도를 가능하게 했습니다. 이를 통해 해당 지역의 암호화폐 시장에서의 사업 확장 전략이 탄력을 받았습니다. 인가를 받은 CASPs는 2025년에 국경을 초월한 사업 확장을 확대했으며, 규제를 준수하는 유로화 기반 스테이블코인은 은행과의 제휴 및 결제 시범 운영을 통해 보급이 확대되었습니다. 온체인 상품의 규모가 확대되는 가운데, 감독 당국은 금융 안정과 투자자 보호를 확보하기 위해 스테이블코인 및 DeFi를 위한 위험 관리 체계를 마련하고 있습니다. 대형 자산운용사가 출시한 토큰화 펀드는 전문 투자자를 대상으로 한 판매망과 관여를 확대하며, 자본 시장과의 연계를 강화했습니다. 이러한 정책과 상품의 변화가 맞물리면서, 유럽은 시장에 더 깊이, 더 안전하게 참여하기 위한 길을 계속 걷고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the cryptocurrency market size is expected to increase from USD 4.87 trillion in 2025 to USD 6.16 trillion in 2026 and reach USD 20.01 trillion by 2031, growing at a CAGR of 26.56% over 2026-2031.

This report is Segmented by Transaction Purpose (Payments & Remittances, Trading and Investment Transfers, and More), User Type (Retail, Institutional), Cryptocurrency (BTC, ETH, Ripple, Bitcoin Cash, Cardano, Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Cryptocurrency Market Trends and Insights

Surge in Regulated Spot-Bitcoin ETFs Unlocking Institutional Capital

The approval of spot Bitcoin exchange-traded products in the United States in January 2024 created a transparent and regulated wrapper that opened fiduciary access for pensions, endowments, and advisory platforms. Institutional demand increased as the product structure aligned with prudent investor rules and reduced operational frictions associated with direct custody, which has reinforced the growth profile of the Cryptocurrency market. U.S. approval and continued supervisory engagement improved the signalling effect for other jurisdictions and accelerated product innovation pipelines, including options on crypto ETPs and multi-asset fund designs in regulated venues. The combination of transparent reserve disclosures at custodians and audited fund operations strengthened compliance readiness for institutional allocators and reduced due diligence cycle times. These developments helped normalize Bitcoin exposure within mainstream investment policy statements and broadened the addressable base of institutions participating in the market.

Euro-Wide MiCA Roll-Out Creating Harmonized Cross-Border Infrastructure

The Markets in Crypto-Assets Regulation became fully enforceable across the European Union in late 2024, replacing divergent national rules with a single passporting framework for issuers and intermediaries. By December 2025, over 100 Crypto-Asset Service Providers operated under MiCA authorization, which allowed a single license to serve clients across the European Economic Area and reduced duplicative compliance overhead. Unified rules for stablecoin issuance and custodial operations lowered cross-border frictions and improved consumer safeguards, which in turn increased institutional confidence to scale services in the region's Cryptocurrency market. Capital and risk management requirements under MiCA raised the threshold for entry and are supporting consolidation among providers that meet operational resilience and disclosure standards. Compliant euro-denominated stablecoins gained traction during 2025, signalling rising demand for regulated settlement assets in Europe's evolving market .

Energy-Grid Backlash and Miner Moratoria Constraining Capacity Expansion

Policymakers and grid operators raised concerns about power demand from energy-intensive proof-of-work operations, which influenced permitting processes and sustainability disclosure requirements tied to large installations interacting with the Cryptocurrency market. European rulemaking has emphasized climate and operational risk disclosures alongside financial consumer protection, which raises compliance costs for operators seeking expansion. Heightened competition for data centre capacity from AI workloads increased the opportunity cost of electricity and land use, which constrained supply growth for mining in several sites. Investment decisions in 2025 reflected pivot dynamics where some compute infrastructure migrated to higher-yield AI applications, reducing the headroom for mining capacity additions within the market. These pressures support a medium-run shift toward efficiency upgrades and location optimization while reinforcing the case for off-grid renewables and demand response participation in energy markets.

Other drivers and restraints analyzed in the detailed report include:

- Rapid CBDC Pilots in APAC and GCC Accelerating Settlement Infrastructure

- AI-Powered Compliance Tools Reducing Fraud-Loss Ratios

- Fragmented KYC and AML Enforcement Creating Compliance Arbitrage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Trading and Investment Transfers accounted for 49.52% of the Cryptocurrency market share in 2025 and are projected to grow at a 31.24% CAGR through 2031, reflecting a structural shift toward regulated derivatives and exchange-traded access. The transition to compliant trading venues deepened liquidity and reduced counterparty risk, which strengthened the ability of institutions to hedge and rebalance efficiently in the market. Stablecoin settlement continued to support the rapid movement of collateral and cash equivalents across platforms, improving capital efficiency and market responsiveness. As regulated products scaled, operational standards and custody assurances improved, supporting larger ticket sizes and broader participation. The result is a more durable trading foundation in the crypto market, with clearer risk controls and integration points to traditional finance.

Payments and Remittances benefited from growing stablecoin utility for cross-border flows as regulated issuers expanded banking partnerships and compliance coverage that supports retail and enterprise use cases. The Decentralized Finance Protocol Flows category continued to attract treasurers and market makers to secured lending, liquidity provisioning, and tokenized collateral strategies where risk tooling is improving. The Others category, which includes cross-border B2B settlements, asset tokenization, and NFT-related activity, diversified in 2025 as asset managers launched on-chain funds and settlement pilots with payment networks. Together, these trends point to a broader utility mix, with payments and trading carrying the largest weight in near-term volumes within the Cryptocurrency market. The Cryptocurrency industry is therefore aligning infrastructure and compliance with use cases that connect to everyday money movement and professional risk management.

Geography Analysis

North America held 35.38% in 2025 and continued to benefit from regulated ETPs, institutional custody, and deep derivatives markets that attract professional participation in the Cryptocurrency market. U.S. policy advances on stablecoin oversight and exchange oversight increased clarity for service providers and investors, which supported liquidity and market depth. The scale of audited custodians improved access for asset managers and corporate treasuries, which facilitated on-ramps for large pools of capital. Canada and cross-border remittance corridors contributed incremental demand for digital dollars and low-cost transfers, which reinforced utility-driven growth in the region's market. Together, these elements sustained North America's leadership in product breadth, compliance, and institutional adoption.

Asia-Pacific is projected to be the fastest-growing region at 29.24% CAGR through 2031 on the back of payment use cases, regional regulatory clarity, and central bank experimentation that shape settlement models relevant to the crypto market. Regulators advanced licensing regimes for stablecoins and intermediaries in financial hubs, which provided guardrails for institutional operations. Payment platforms and super-apps expanded digital dollar access for consumers and merchants, which supported remittance corridors and e-commerce payments. Multi-country pilots continued to test real-time gross settlement across borders, which informs the long-run role of public and private tokens in regional payment systems that interface with the market. These trends collectively underpin rising participation and infrastructure investment in Asia-Pacific.

Europe's framework, centred on MiCA, created a harmonized licensing environment across 27 member states and enabled passporting that reduces duplicative compliance, which supports scale-up strategies in the region's Cryptocurrency market. Authorized CASPs expanded operations across borders in 2025, and compliant euro-denominated stablecoins gained adoption through banking partnerships and payment pilots. Supervisors are advancing risk frameworks for stablecoins and DeFi to ensure financial stability and investor protection as on-chain products scale. Tokenized funds from major asset managers extended distribution and engagement among professional investors, which strengthened linkages with capital markets. Together, these policy and product shifts keep Europe on a path toward deeper, safer participation in the market.

- Coinbase Global Inc.

- Binance Holdings Ltd.

- Tether Limited (USDT)

- Circle Internet Financial LLC (USDC)

- OKX (OK Group)

- Kraken (Payward Inc.)

- KuCoin

- Huobi (HTX)

- Bybit Fintech Ltd.

- Bitfinex

- Gate.io

- Bitstamp Ltd.

- Gemini Trust Company LLC

- Upbit Exchange (Dunamu Inc.)

- Bithumb Korea Co. Ltd.

- Bitget (Singapore)

- MEXC Global

- Coincheck Inc.

- Bitso S.A. de C.V.

- Coinone

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in regulated spot-Bitcoin ETFs (2024-25)

- 4.2.2 Euro-wide MiCA roll-out unlocking cross-border crypto services

- 4.2.3 Rapid CBDC pilots in Asia-Pacific & GCC boosting settlement trials

- 4.2.4 AI-powered compliance tools lowering fraud-loss ratios

- 4.2.5 Corporate treasury adoption by NASDAQ-100 constituents

- 4.2.6 Mobile-super-apps in Africa & SEA integrating USDC rails

- 4.3 Market Restraints

- 4.3.1 Energy-grid backlash & miner moratoria in Nordics & U.S.

- 4.3.2 Fragmented KYC / AML enforcement outside MiCA scope

- 4.3.3 Stable-coin de-pegs triggering tighter reserve mandates

- 4.3.4 Blockchain-engineering talent drain to Gen-AI sector

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Environmental Impact Analysis

5 Market Size & Growth Forecasts (Value)

- 5.1 By Transaction Purpose

- 5.1.1 Payments & Remittances

- 5.1.2 Trading and Investment Transfers

- 5.1.3 Decentralized Finance (DeFi) Protocol Flows

- 5.1.4 Others (Cross-border B2B Settlements, Asset Tokenization & Settlements, NFT Purchases)

- 5.2 By User Type

- 5.2.1 Retail

- 5.2.2 Institutional

- 5.3 By Cryptocurrency

- 5.3.1 BTC

- 5.3.2 ETH

- 5.3.3 Ripple

- 5.3.4 Bitcoin Cash

- 5.3.5 Cardano

- 5.3.6 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX

- 5.4.3.7 NORDICS

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South East Asia

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market-level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Coinbase Global Inc.

- 6.4.2 Binance Holdings Ltd.

- 6.4.3 Tether Limited (USDT)

- 6.4.4 Circle Internet Financial LLC (USDC)

- 6.4.5 OKX (OK Group)

- 6.4.6 Kraken (Payward Inc.)

- 6.4.7 KuCoin

- 6.4.8 Huobi (HTX)

- 6.4.9 Bybit Fintech Ltd.

- 6.4.10 Bitfinex

- 6.4.11 Gate.io

- 6.4.12 Bitstamp Ltd.

- 6.4.13 Gemini Trust Company LLC

- 6.4.14 Upbit Exchange (Dunamu Inc.)

- 6.4.15 Bithumb Korea Co. Ltd.

- 6.4.16 Bitget (Singapore)

- 6.4.17 MEXC Global

- 6.4.18 Coincheck Inc.

- 6.4.19 Bitso S.A. de C.V.

- 6.4.20 Coinone

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment