|

시장보고서

상품코드

2066630

북미의 물류 자동화 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)North America Logistics Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

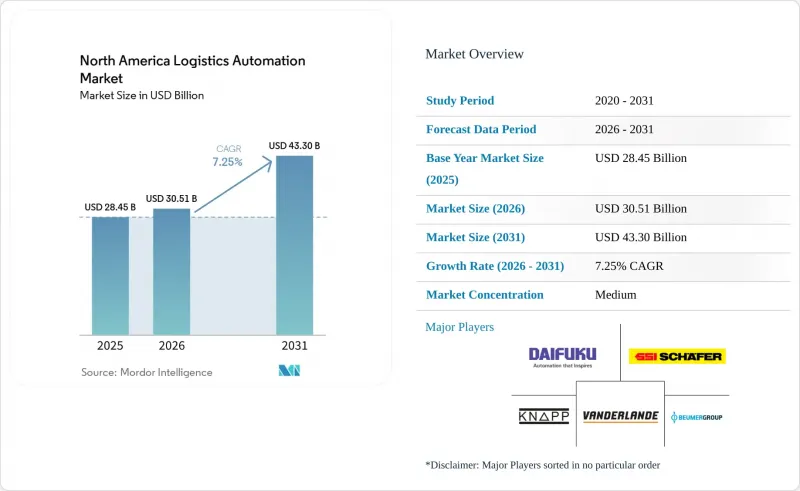

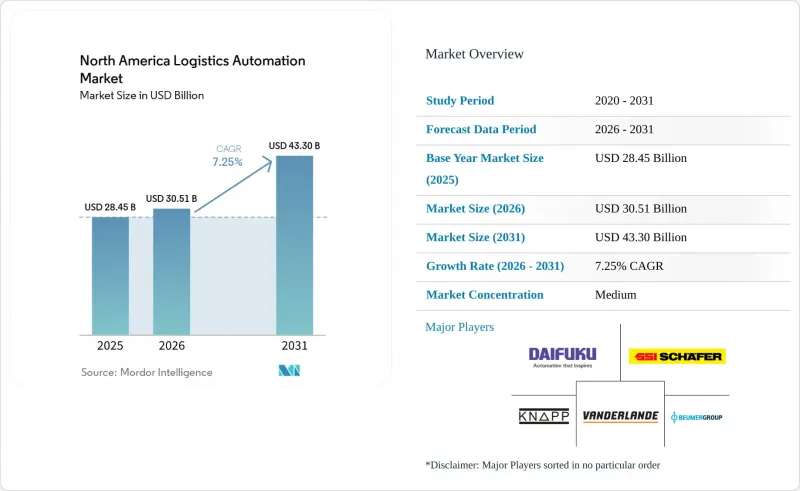

Mordor Intelligence에 의하면, 북미 물류 자동화 시장 규모는 2025년 284억 5,000만 달러에서 2026년에는 305억 1,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 7.25%로 성장을 지속하여, 2031년에는 433억 달러에 이를 것으로 예측됩니다.

본 보고서는 기능별(창고 자동화 및 운송 자동화), 자동화 수준별(완전 자동화 시스템 및 반자동화 시스템), 구성 요소별(하드웨어, 소프트웨어, 서비스), 최종 사용 산업별(전자상거래 및 소포, 식품 및 음료, 식료품 소매, 의류 및 패션 등), 그리고 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미 물류 자동화 시장 동향과 인사이트

전자상거래의 주문 처리 밀도와 당일 배송 서비스 수준

북미 물류 자동화 시장에서 당일 배송은 프리미엄 서비스에서 핵심적인 업무 요건으로 자리 잡고 있습니다. 아마존은 2026년 중반까지의 연초 대비 기간 동안 당일 또는 익일 배송 건수가 10억 건을 돌파했으며, 2026년 4월에는 미국의 중규모 도시권에 18곳의 당일 배송 시설을 신설했습니다. 이로 인해 자동화에 대한 수요가 교외 및 교외 외곽(엑서반) 지역으로 더욱 확대되었습니다. 이러한 변화로 인해 사업자들은 1제곱미터당 처리 단위 수를 늘릴 수밖에 없게 되었으며, 고속 분류, 소형 ASRS, 그리고 ‘상품에서 사람으로(Goods-to-Person)’ 방식의 워크플로우 도입이 더욱 중요해지고 있습니다. 또한, 이로 인해 투자 대상이 초대형 풀필먼트 센터에서 경쟁력을 유지하기 위해 여전히 고밀도 자동화가 필요한 소규모 마이크로 허브로 전환되고 있습니다. 북미 물류 자동화 시장에서는 현재 서비스 수준에 대한 압박이 커지면서, 인건비나 보관 밀도와 마찬가지로 시설 설계에 영향을 미치고 있습니다. 그 결과, 본격적인 그린필드 건설을 기다리지 않고 수요지 근처에 도입할 수 있는 모듈식 시스템으로의 전환이 가속화되고 있습니다.

창고 업계의 인력 부족과 임금 상승

노동력 부족은 북미 물류 자동화 시장에서 여전히 가장 강력한 경제적 촉진요인 중 하나입니다. 이는 사업자들이 단기적인 경기 순환이 아니라 구조적인 문제에 대응하고 있기 때문입니다. 미국 창고·보관 업계의 평균 시급은 2025년 1월 25.02달러에서 상승하여, 2026년 1월에는 26.58달러, 2026년 2월에는 26.68달러에 달했으며, 창고 네트워크 전체에서 임금 상승 압력이 계속해서 높은 수준을 유지했습니다. 민간 기업 종업원의 인건비는 2026년 3월까지의 12개월 동안 3.4% 상승했습니다. 이는 실질적인 임금 인상 폭이 제한적이었음에도 불구하고, 인건비 부담이 여전히 컸음을 보여줍니다. 2025년 ILR Review의 조사에 따르면, 창고에 로봇을 도입하면 중상 사고는 40% 감소하는 반면, 경상 사고는 77% 증가하는 것으로 나타났습니다. 이를 통해 인간과 로봇이 공존하는 작업장에서 인체공학에 기반한 설계의 중요성이 다시 한번 강조되었습니다. 그 결과, 조달의 우선순위는 단순히 로봇 대수를 늘리는 것뿐만 아니라, ‘상품에서 사람으로(Goods-to-Person)’ 방식의 스테이션 도입과 더 우수한 워크플로우 설계로 전환되고 있습니다. 북미 물류 자동화 시장에서는 사람과 기계를 연계하는 소프트웨어가 노동 생산성 향상을 위한 가장 확실한 방안으로 점점 더 주목받고 있습니다.

고정형 자동화에 따른 막대한 초기 투자

고정형 자동화는 여전히 북미 물류 자동화 시장에서 실질적인 제약 요인으로 작용하고 있습니다. 이는 대규모 컨베이어 네트워크, 통합형 분류 시스템, 그리고 엔드투엔드 ASRS 시스템에는 여전히 수년 단위의 설비 투자가 필요하기 때문입니다. 이러한 압박은 대형 소매업체나 대형 유통업체만큼 재무적 유연성을 갖추지 못한 중견 3PL 기업이나 지역 유통업체에서 가장 크게 느껴지고 있습니다. 또한, 철강 관련 장비 가격의 급등으로 인해 투자 회수 기간이 길어지고, 턴키 프로젝트에 대한 신중한 태도가 강해지면서 투자 결정이 더욱 어려워지고 있습니다. 다만, 세제 측면에서는 일정한 구제 조치가 마련되어 있습니다. IRS(미국 국세청)의 지침에 따르면, 2026년에 가동을 시작하는 적격 설비에 대한 섹션 179 공제 한도액이 256만 달러에 달했기 때문입니다. 이와 같은 세제 체계에 따라 적격 자산에 대한 100% 특별 상각도 허용되고 있으며, 이를 통해 대상 자동화 자산의 첫해 실질 비용이 절감됩니다. 이러한 지원이 있음에도 불구하고, 북미 물류 자동화 시장의 많은 구매자들은 프로젝트 위험이 높은 상황에서는 여전히 단계적인 도입이나 유연한 비즈니스 모델을 선호하는 경향이 있습니다.

부문별 분석

2025년, 창고 자동화는 매출의 61.34%를 차지했으며, 운영자가 시설 내 피킹, 보관, 분류 및 컨베이어를 많이 활용하는 작업 흐름에 주력한 덕분에 북미 물류 자동화 시장의 중심적인 위치를 차지했습니다. 2025년에 창고 자동화가 북미 물류 자동화 시장 점유율의 61.34%를 차지한 것은 통제된 실내 환경에서 투자 수익률(ROI)을 역사상 가장 쉽게 확보할 수 있었기 때문입니다. '상품에서 사람으로(Goods-to-Person)' 방식의 ASRS, AMR 차량군 및 창고 운영 소프트웨어는 처리 능력, 노동 생산성 및 주문 정확도를 직접 향상시키기 때문에 계속해서 이 부문을 주도하고 있습니다. Medline사는 2026년 5월, 콜로라도주 오로라에 위치한 물류 센터에 24번째 AutoStore를 도입하고, 지역 수요에 대응하기 위해 로봇 96대와 빈 3만 8,000개를 추가함으로써 이러한 추세를 더욱 확대했습니다. 북미 물류 자동화 시장에서는 대규모 사업자들이 전국적으로 자동화를 표준화하는 첫 단계로서 실내 이송이 계속해서 중요하게 여겨지고 있습니다.

물류 자동화는 비교적 소규모 기반에서 시작되었지만, 2031년까지 연평균 성장률(CAGR)이 7.94%로 가장 빠르게 성장하고 있는 분야이며, 이러한 성장은 SAE 레벨 4 화물 운송 노선의 조기 상용화를 반영하고 있습니다. Gatik사는 2026년 1월, 미국 기업 최초로 대규모 완전 무인 상업 배송을 완료했으며, 텍사스주, 아칸소주, 애리조나주에 위치한 포춘 50대 소매업체를 대상으로 6만 건의 무인 배송 주문을 사고 없이 처리했습니다. 또한, Aurora Innovation사와 McLane사도 2026년 5월, 텍사스주 댈러스와 휴스턴 간 무인 운송을 시작하고, 미국 선벨트 지역 전체로 확대할 계획을 발표했습니다.

2025년에는 반자동화 시스템이 매출의 55.90%를 차지했는데, 이는 북미 물류 자동화 시장에서 가동 중인 창고의 대부분이 채택하고 있는 실용적인 구조를 반영한 것입니다. 반자동화 시스템이 매출의 55.90%를 차지한 이유는 기존 시설(브라운필드)의 상당수가 여전히 창고 관리 시스템(WMS)를 통한 인력 작업과, 상품에서 사람으로의 피킹, 팔레트 이동, 팔레타이징과 같은 반복 작업에 특화된 로봇을 결합하여 운영하고 있기 때문입니다. 이 모델을 통해 사업자는 완전한 시스템 전환에 따른 비용이나 운영 위험을 감수하지 않고도 처리 능력을 향상시킬 수 있습니다. 2025년, 스테이플스 캐나다는 밴쿠버의 물류 센터에 Locus Robotics사의 AMR 50대를 도입하여 불과 4일 만에 완전한 운영 통합을 달성함으로써, 이러한 접근 방식의 매력을 입증했습니다. 북미 물류 자동화 업계에서 이러한 하이브리드 구조는 처리량이 변동하거나 계절적 수요 급증이 발생하거나, 기존 레이아웃을 재설계하기 어려운 시설의 경우 여전히 표준적인 선택지로 자리 잡고 있습니다.

완전 자동화 시스템은 2031년까지 연평균 성장률(CAGR)이 8.13%로, 더욱 빠르게 성장하고 있습니다. 이는 그린필드 프로젝트나 대규모 네트워크 개편에서 무인 또는 거의 무인 워크플로우를 전제로 한 설계가 이루어지게 되었기 때문입니다. 센서 비용의 하락, 인식 소프트웨어의 고도화, 그리고 로봇의 지속적인 가동에 대한 신뢰도 상승이 이러한 추세를 뒷받침하고 있습니다. Locus Robotics사는 MODEX 2026에서 이동형 로봇, 통합형 피킹 암, AI를 활용한 지각 기능을 결합한 완전 자율형 풀필먼트 시스템 ‘Locus Array’를 발표했으며, 북미 DHL 공급망에서는 이미 초기 도입이 진행되고 있습니다. 그 후, Locus사는 2026년 5월에 Nexera Robotics사를 인수하고 NeuraGrasp 기술을 도입함으로써 시스템의 SKU 지원 범위를 확대했습니다. 이처럼 북미 물류 자동화 시장에서는 이동형 로봇과 로봇에 의한 조작이 공통의 오케스트레이션 계층 위에서 점점 더 긴밀하게 연동되어 작동함에 따라, 부분적 자동화와 완전한 자율화 사이의 격차가 점차 좁혀지고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the north america logistics automation market size is expected to grow from USD 28.45 billion in 2025 to USD 30.51 billion in 2026 and is forecast to reach USD 43.30 billion by 2031 at 7.25% CAGR over 2026-2031.

This report is Segmented by Function (Warehouse Automation and Transportation Automation), Automation Level (Fully-Automated Systems and Semi-Automated Systems), Component (Hardware, Software, and Services), End-User Industry (E-Commerce and Parcel, Food and Beverage, Grocery Retail, Apparel and Fashion, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America Logistics Automation Market Trends and Insights

E-Commerce Fulfillment Density and Same-Day Service Levels

Same-day delivery has moved from a premium service into a core operating requirement across the North America logistics automation market. Amazon exceeded 1 billion same-day or overnight deliveries in the year-to-date period through mid-2026 and added 18 same-day facilities in mid-sized US metro areas in April 2026, which pushed automation demand deeper into suburban and exurban nodes. That shift forces operators to process more units per square meter, which strengthens the case for high-speed sortation, compact ASRS, and goods-to-person workflows. It also redirects investment away from only very large fulfillment centers and toward smaller micro-hubs that still need dense automation to stay competitive. In the North America logistics automation market, service-level pressure is now shaping facility design as much as labor cost or storage density. The result is a faster move toward modular systems that can be deployed close to demand without waiting for full-scale greenfield construction.

Warehouse Labor Scarcity and Wage Inflation

Labor scarcity remains one of the strongest economic drivers in the North America logistics automation market because operators are responding to a structural problem rather than a short-term cycle. Average hourly earnings in US warehousing and storage reached USD 26.58 in January 2026 and USD 26.68 in February 2026, up from USD 25.02 in January 2025, which kept wage pressure elevated across warehouse networks. Compensation costs for private industry workers rose 3.4% in the 12 months to March 2026, which shows that payroll pressure remained firm even as real gains stayed limited. A 2025 ILR Review study found that warehouse robotics was associated with a 40% reduction in severe injuries and a 77% rise in non-severe injuries, which reinforced the need for better ergonomic design at human-robot workstations. This has shifted procurement priorities toward goods-to-person stations and better workflow design rather than only toward higher robot counts. In the North America logistics automation market, software that coordinates people and machines is increasingly viewed as the clearest path to labor-productivity gains.

High Upfront Capital Outlays for Fixed Automation

Fixed automation remains a real constraint on the North America logistics automation market because large conveyor networks, integrated sortation, and end-to-end ASRS systems still require multiyear capital commitments. This pressure is strongest among mid-market 3PLs and regional distributors that do not have the same balance sheet flexibility as large retailers or large distributors. Steel-related equipment inflation has also made investment decisions harder by extending payback periods and increasing caution around turnkey projects. Operators do have some relief through tax policy, as the Section 179 deduction ceiling for qualifying equipment placed in service in 2026 reached USD 2,560,000 under IRS guidance. The same tax framework also supports 100% bonus depreciation for qualifying property, which lowers the effective first-year cost of eligible automation assets. Even with that support, many buyers in the North America logistics automation market still prefer phased deployments or flexible commercial models when project risk remains high.

Other drivers and restraints analyzed in the detailed report include:

- AMR and AI Orchestration Adoption Across Fulfillment Centers

- Nearshoring-Led Network Redesign in Mexico and The United States

- Legacy-System Integration and Brownfield Retrofit Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Warehouse automation held 61.34% of revenue in 2025, which placed it at the center of the North America logistics automation market as operators focused on picking, storage, sortation, and conveyor-intensive flows inside the facility. Warehouse automation accounted for 61.34% of the North America logistics automation market share in 2025 because the return on investment has historically been easiest to capture inside controlled indoor environments. Goods-to-person ASRS, AMR fleets, and warehouse execution software continue to define this segment because they directly improve throughput, labor productivity, and order accuracy. Medline expanded that pattern in May 2026 when it deployed its 24th AutoStore installation at its Aurora, Colorado distribution center, adding 96 robots and 38,000 bins to support regional demand. The North America logistics automation market continues to treat indoor handling as the first place where high-volume operators standardize automation across a national footprint.

Transportation automation started from a smaller base, but it is the fastest-growing function at a 7.94% CAGR through 2031, and that growth reflects the early commercialization of SAE Level 4 freight lanes. Gatik became the first US company to complete fully driverless commercial deliveries at scale in January 2026, recording 60,000 driverless orders for Fortune 50 retailers in Texas, Arkansas, and Arizona without incident. Aurora Innovation and McLane also announced in May 2026 that they would begin driverless hauls in Texas between Dallas and Houston, with plans to expand across the US Sun Belt.

Semi-automated systems held 55.90% of revenue in 2025, which reflected the practical structure of most active warehouses in the North America logistics automation market. Semi-automated systems carried 55.90% of revenue because most brownfield sites still combine WMS-directed human labor with targeted robotics for repetitive tasks such as goods-to-person picking, pallet movement, or palletizing. This model helps operators improve throughput without taking on the cost and operational risk of a full cutover. Staples Canada showed the appeal of this approach in 2025 when it deployed 50 Locus Robotics AMRs in a Vancouver fulfillment center and reached full operational integration within 4 days. In the North America logistics automation industry, this hybrid structure remains the default for facilities with variable volumes, seasonal spikes, and existing layouts that are not easy to redesign.

Fully-automated systems are growing faster, with an 8.13% CAGR through 2031, because greenfield projects and major network refreshes are now being designed for unattended or near-unattended workflows. Falling sensor costs, better perception software, and stronger confidence in continuous robotic operation are supporting that move. Locus Robotics launched Locus Array at MODEX 2026 as a fully autonomous fulfillment system that combines mobile robotics, an integrated picking arm, and AI-powered perception, with early deployments already underway at DHL Supply Chain in North America. Locus then acquired Nexera Robotics in May 2026 to add NeuraGrasp technology and widen the system's SKU-handling range. The North America logistics automation market is therefore narrowing the gap between partial automation and full autonomy as mobile robotics and robotic manipulation increasingly run on a shared orchestration layer.

List of Companies Covered in this Report:

- Daifuku Co., Ltd.

- SSI SCHAEFER AG

- KNAPP AG

- Vanderlande Industries B.V.

- BEUMER Group GmbH & Co. KG

- Dematic Corp.

- Mecalux, S.A.

- Swisslog Holding AG

- TGW Logistics Group GmbH

- WITRON Logistik + Informatik GmbH

- Kardex Holding AG

- AutoStore Holdings Ltd.

- Exotec SAS

- Geekplus Technology Co., Ltd.

- Hai Robotics Co., Ltd.

- GreyOrange Pte. Ltd.

- Locus Robotics Corp.

- Cimcorp Oy

- System Logistics S.p.A.

- Bastian Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Fulfillment Density and Same-day Service Levels

- 4.2.2 Warehouse Labor Scarcity and Wage Inflation

- 4.2.3 AMR and AI Orchestration Adoption Across Fulfillment Centers

- 4.2.4 Nearshoring-led Network Redesign in Mexico and the United States

- 4.2.5 Ergonomic-risk Mitigation in High-throughput Fulfillment Sites

- 4.2.6 Tax Incentives for Domestic and Cross-border Automation Investments

- 4.3 Market Restraints

- 4.3.1 High Upfront Capital Outlays for Fixed Automation

- 4.3.2 Legacy-system Integration and Brownfield Retrofit Complexity

- 4.3.3 Steel Tariff Volatility and Longer Automation Payback

- 4.3.4 Robot-cell Safety and Cybersecurity Compliance Burden

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Function

- 5.1.1 Warehouse Automation

- 5.1.1.1 Component

- 5.1.1.1.1 Hardware

- 5.1.1.1.1.1 Mobile Robots

- 5.1.1.1.1.2 Automated Storage and Retrieval Systems

- 5.1.1.1.1.3 Automated Sorting Systems

- 5.1.1.1.1.4 Conveyor Systems

- 5.1.1.1.1.5 Automatic Identification and Data Collection (AIDC)

- 5.1.1.1.1.6 Order Picking

- 5.1.1.1.2 Software

- 5.1.1.1.3 Services

- 5.1.1.1.1 Hardware

- 5.1.1.1 Component

- 5.1.2 Transportation Automation

- 5.1.2.1 Component

- 5.1.2.1.1 Hardware

- 5.1.2.1.2 Software

- 5.1.2.1.3 Services

- 5.1.2.1 Component

- 5.1.1 Warehouse Automation

- 5.2 By Automation Level

- 5.2.1 Fully-Automated Systems

- 5.2.2 Semi-Automated Systems

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.4 By End-User Industry

- 5.4.1 E-commerce and Parcel

- 5.4.2 Food and Beverage

- 5.4.3 Grocery Retail

- 5.4.4 Apparel and Fashion

- 5.4.5 Manufacturing

- 5.4.6 Other End-User Industries

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Daifuku Co., Ltd.

- 6.4.2 SSI SCHAEFER AG

- 6.4.3 KNAPP AG

- 6.4.4 Vanderlande Industries B.V.

- 6.4.5 BEUMER Group GmbH & Co. KG

- 6.4.6 Dematic Corp.

- 6.4.7 Mecalux, S.A.

- 6.4.8 Swisslog Holding AG

- 6.4.9 TGW Logistics Group GmbH

- 6.4.10 WITRON Logistik + Informatik GmbH

- 6.4.11 Kardex Holding AG

- 6.4.12 AutoStore Holdings Ltd.

- 6.4.13 Exotec SAS

- 6.4.14 Geekplus Technology Co., Ltd.

- 6.4.15 Hai Robotics Co., Ltd.

- 6.4.16 GreyOrange Pte. Ltd.

- 6.4.17 Locus Robotics Corp.

- 6.4.18 Cimcorp Oy

- 6.4.19 System Logistics S.p.A.

- 6.4.20 Bastian Solutions

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment