|

시장보고서

상품코드

2066672

북미의 자동차용 접착제 및 실란트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Automotive Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

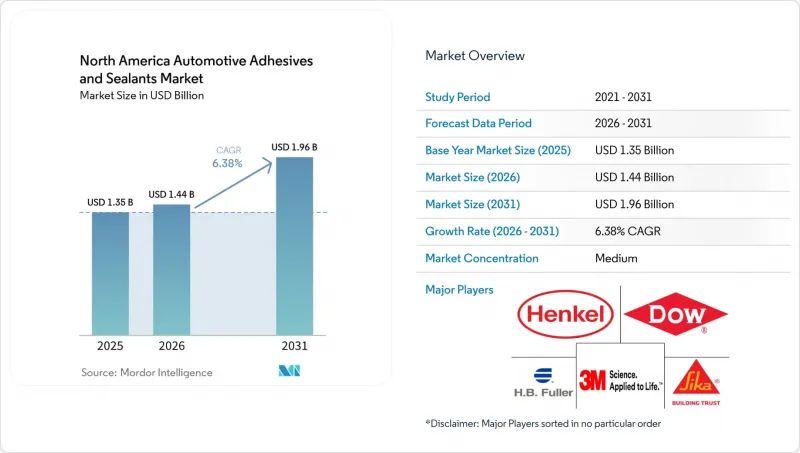

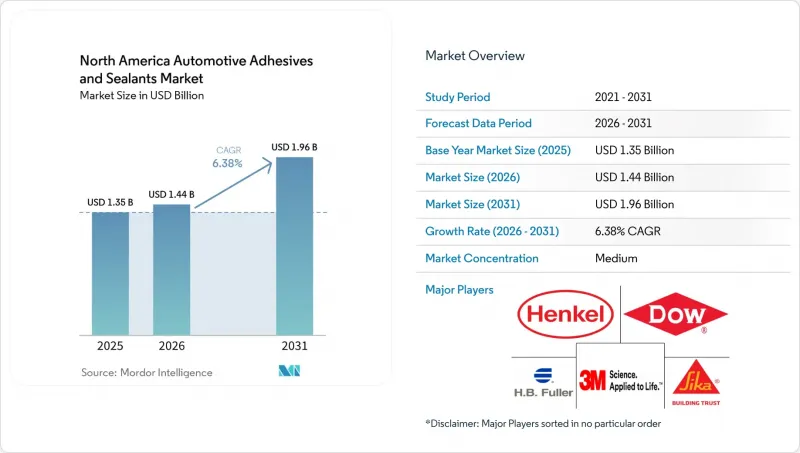

Mordor Intelligence에 의하면, 북미의 자동차용 접착제 및 실란트 시장 규모는 2025년 13억 5,000만 달러로 평가되었습니다. 2026년에는 14억 4,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 6.38%로 성장을 지속하여, 2031년에는 19억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 수지(폴리우레탄, 아크릴, 시아노아크릴레이트, 에폭시, 실리콘, VAE/EVA, 기타 수지), 기술(반응형, 핫멜트, 실란트, 용제형, UV 경화형, 수성) 및 지역(미국, 캐나다, 멕시코)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미의 자동차용 접착제 및 실란트 시장 동향 및 인사이트

전기자동차(EV) 특유의 접착 요구 사항의 급증

기가팩토리에 대한 투자를 통해 접착제의 사양이 재정의되고 있습니다. 파나소닉 에너지의 캔자스 공장에서는 열전도율이 2 W/m*K를 초과하는 에폭시 수지가 요구되는 반면, 폭스바겐의 온타리오 공장에서는 3,000회의 열 사이클 후에도 80%의 접착 강도를 유지하는 실리콘계 열 인터페이스 재료가 승인되었습니다. 미시간주에 위치한 테슬라와 LG의 합작 기업에서는 10초 이내에 타크 프리 상태가 되는 UV 경화형 화학 물질을 사용하는 디스펜싱 로봇을 도입하여, 유전 성능을 저하시키지 않으면서 사이클 타임을 단축하는 자동화 대응 제품을 실현하고 있습니다. 1억 달러 상당의 연방 정부 보조금이 고체 배터리 밀봉 관련 연구 개발을 지원하고 있으며, 이는 UL 94 V-0 난연성 기준을 충족하는 난연성 접착제에 대한 수요를 견인하고 있습니다.

USMCA 전 지역에서 경량화 의무화

USMCA의 현지 조달률 규제로 인해, 강철에서 용접이 불가능한 알루미늄 및 탄소섬유 복합재료로의 전환이 가속화되고 있습니다. 멕시코산 차량의 적합률은 2025년 7월까지 76.1%에 달했으며, 2년 동안 8퍼센트포인트 상승했습니다. 포드의 ‘F-150 Lightning’과 GM의 ‘Silverado EV’에서는 알루미늄 압출 성형품을 강철 서브프레임에 접착하기 위해 내충격성 에폭시 수지가 채택되었으며, 이에 따른 표면 처리용 프라이머로 인해 접착제 시스템의 비용이 8-12% 증가했습니다.

석유계 수지 원자재 가격의 변동

BASF와 Wanhua의 예상치 못한 가동 중단으로 인해 2026년 3월 TDI 현물 가격은 8.13% 상승했습니다. 한편, 주요 원료인 아닐린은 가스 가격 급등과 해상 운임 상승으로 인해 2024년 4분기에 18% 상승했습니다. 2025년에는 중국 생산자들이 탄소 집약도 목표를 달성하기 위해 생산량을 줄이면서 아크릴 모노머 공급이 12% 부족해졌고, 이로 인해 북미의 컴파운드 제조업체들의 이익률이 압박을 받았습니다. 혼합 제조업체는 분기별 조정 조항을 적용했으나, 연간 계약에 묶여 있던 1차 공급업체는 2025년 중 4,000만-6,000만 달러의 이익 감소를 겪게 되었습니다.

부문별 분석

폴리우레탄은 구조용 접착, NVH(소음·진동·거칠기) 저감, 이음매 밀봉 분야에서 뛰어난 적용성을 바탕으로, 2025년 북미의 자동차용 접착제 및 실란트 시장 수요 중 25.35%를 차지했습니다. 그러나 내장재 제조업체들이 저온 활성화에 우선순위를 두고 있는 만큼, VAE/EVA 수지는 2031년까지 연평균 성장률(CAGR) 6.45%를 기록하며 성장할 것으로 전망됩니다. 이를 통해 오븐의 에너지 소비를 30% 절감하고, 재활용 활동을 지원할 수 있게 됩니다. 에폭시 수지는 25 MPa를 초과하는 인장 강도가 필요한 충돌 안전상 중요한 접합부에서 여전히 필수적이지만, 한편 실리콘 수지는 -40°C에서 +150°C에 이르는 온도 범위에서 안정성을 발휘하기 때문에 배터리 열 관리 용도로의 사용이 증가하고 있습니다. 시아노아크릴레이트를 함유한 아크릴계 수지는 60초 미만의 고정 장치 없이도 경화되는 시간을 특징으로 하며, 센서 브래킷 등 틈새 시장의 신속 조립 용도에서 주목받고 있습니다. 또한, 폴리이미드 등의 ‘기타 수지’는 열 차단 용도에서 높은 이익률을 실현하고 있습니다.

VAE/EVA의 성장은 재활용 소재의 함유율을 높이기 위한 각 OEM 업체들의 노력과 맥을 같이하고 있습니다. 한편, 헨켈사의 바이오 비율 60%인 폴리우레탄은 5 MPa 이하의 랩 전단 강도를 저하시키지 않으면서도 폴리우레탄이 지속가능성 목표를 달성할 수 있음을 입증하고 있습니다. 에폭시 수지 공급업체들은 이종 재료의 접합부에서 발생하는 열팽창률 차이를 해결하기 위해 강화 등급의 개발을 추진하고 있습니다. 또한, 실리콘 수지 배합 제조업체들은 고전압 배터리 설계 요건을 충족하기 위해 절연 내력을 20 kV/mm 이상으로 높이기 위한 노력을 기울이고 있습니다. 시아노아크릴레이트 수지 개발 업체는 빛이 닿지 않는 부위를 위해 UV 경화와 습기 경화를 결합한 기술을 도입하여, ADAS 모듈의 자동 생산 라인에서의 적용 범위를 확대되고 있습니다. 전반적으로, 수지 선정은 기계적 성능과 에너지 소비 절감, 그리고 사용 후 재활용성 향상 간의 균형을 갖춘 화학 조성으로 전환되고 있으며, 이는 북미의 자동차용 접착제 및 실란트 시장에서 진행 중인 변화를 반영하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the north america automotive adhesives and sealants market size is expected to grow from USD 1.35 billion in 2025 to USD 1.44 billion in 2026 and is forecast to reach USD 1.96 billion by 2031 at 6.38% CAGR over 2026-2031.

This report is Segmented by Resin (Polyurethane, Acrylic, Cyanoacrylate, Epoxy, Silicone, VAE/EVA, and Other Resins), Technology (Reactive, Hot-Melt, Sealants, Solvent-Borne, UV-Cured, and Water-Borne), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Automotive Adhesives And Sealants Market Trends and Insights

Surging EV-Specific Bonding Requirements

Gigafactory investments are redefining adhesive specifications. Panasonic Energy's Kansas plant requires epoxies with thermal conductivity exceeding 2 W/m*K, while Volkswagen's Ontario facility has approved silicone thermal interface materials that retain 80% bond strength after 3,000 thermal cycles. Dispensing robots at the Tesla-LG joint venture in Michigan utilize UV-cured chemistries that achieve a tack-free state in under 10 seconds, enabling automation-compatible products that reduce cycle times without compromising dielectric performance. Federal grants worth USD 100 million are supporting R&D into solid-state cell encapsulation, driving demand for flame-retardant adhesives that meet UL 94 V-0 flammability standards.

Lightweighting Mandates Across USMCA

USMCA content rules are accelerating the transition from steel to aluminum and carbon-fiber composites, which cannot be welded. Compliance rates for Mexican-origin vehicles reached 76.1% by July 2025, an increase of 8 percentage points over two years. Ford's F-150 Lightning and GM's Silverado EV rely on crash-resistant epoxies to bond aluminum extrusions to steel subframes, with associated surface-preparation primers now contributing an 8-12% increase in adhesive system costs.

Raw-Material Volatility for Petro-Resins

Unplanned outages at BASF and Wanhua caused TDI spot prices to rise by 8.13% in March 2026, while aniline, a key feedstock, increased by 18% in Q4 2024 due to gas price spikes and higher ocean freight costs. Acrylic monomer supply tightened by 12% in 2025 as Chinese producers reduced output to meet carbon-intensity targets, squeezing margins for North American compounders. While formulators implemented quarterly adjustment clauses, Tier-1 suppliers bound by annual contracts faced USD 40-60 million in margin erosion during 2025.

Other drivers and restraints analyzed in the detailed report include:

- OEM Shift to Mixed-Material Body-in-White

- Rapid Growth of Battery Gigafactories

- Limited High-Temperature Recyclability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane accounted for 25.35% of the 2025 demand in the North America automotive adhesives and sealants market due to its adaptability in structural bonding, NVH damping, and seam sealing. However, VAE/EVA resins are anticipated to grow at a 6.45% CAGR through 2031, as interior-trim manufacturers prioritize low-temperature activation, which reduces oven energy consumption by 30% and supports recycling efforts. Epoxy remains critical for crash-critical joints requiring tensile strength above 25 MPa, while silicone usage is increasing in battery thermal-management applications due to its stability across a temperature range of -40 °C to +150 °C. Acrylics, including cyanoacrylates, are gaining traction in niche rapid-assembly applications, such as sensor brackets, due to their sub-60-second fixture-free curing times. Additionally, "other resins," such as polyimides, command premium margins in thermal-barrier applications.

The growth of VAE/EVA aligns with OEM commitments to increase recycled content, while Henkel's 60% bio-based polyurethane demonstrates how polyurethanes can meet sustainability goals without compromising lap-shear strength below 5 MPa. Epoxy suppliers are developing toughened grades to address differential expansion in mixed-material joints, and silicone formulators are enhancing dielectric strength beyond 20 kV/mm to meet the requirements of high-voltage battery designs. Cyanoacrylate developers are integrating UV and moisture curing for shadowed areas, expanding their use in automated ADAS module production lines. Overall, resin selection is shifting toward chemistries that balance mechanical performance with reduced energy consumption and improved end-of-life recyclability, reflecting the ongoing transition in the North America automotive adhesives and sealants market.

List of Companies Covered in this Report:

- 3M

- Arkema

- Ashland

- Avery Dennison Corp.

- Dow

- DuPont

- Dymax

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International

- ITW Performance Polymers

- Jowat SE

- MasterBond

- Matrix Adhesives Group

- PARKER HANNIFIN CORP

- Permabond LLC

- Sika AG

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging EV-specific bonding requirements

- 4.2.2 Lightweighting mandates across USMCA

- 4.2.3 OEM shift to mixed-material body-in-white

- 4.2.4 Rapid growth of battery gigafactories

- 4.2.5 Tier-1 adoption of smart curing lines

- 4.2.6 IRA-driven reshoring of supply chains

- 4.3 Market Restraints

- 4.3.1 Raw-material volatility for petro-resins

- 4.3.2 Limited high-temperature recyclability

- 4.3.3 OSHA scrutiny on isocyanate exposure

- 4.3.4 Scale-up risk for bio-based chemistries

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin

- 5.1.1 Polyurethane

- 5.1.2 Acrylic

- 5.1.3 Cyanoacrylate

- 5.1.4 Epoxy

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 By Technology

- 5.2.1 Reactive

- 5.2.2 Hot-melt

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 UV-cured

- 5.2.6 Water-borne

- 5.3 By Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 Avery Dennison Corp.

- 6.4.5 Dow

- 6.4.6 DuPont

- 6.4.7 Dymax

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Huntsman International

- 6.4.11 ITW Performance Polymers

- 6.4.12 Jowat SE

- 6.4.13 MasterBond

- 6.4.14 Matrix Adhesives Group

- 6.4.15 PARKER HANNIFIN CORP

- 6.4.16 Permabond LLC

- 6.4.17 Sika AG

- 6.4.18 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment