|

시장보고서

상품코드

2072451

치과 교정 용품 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Orthodontic Supplies - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

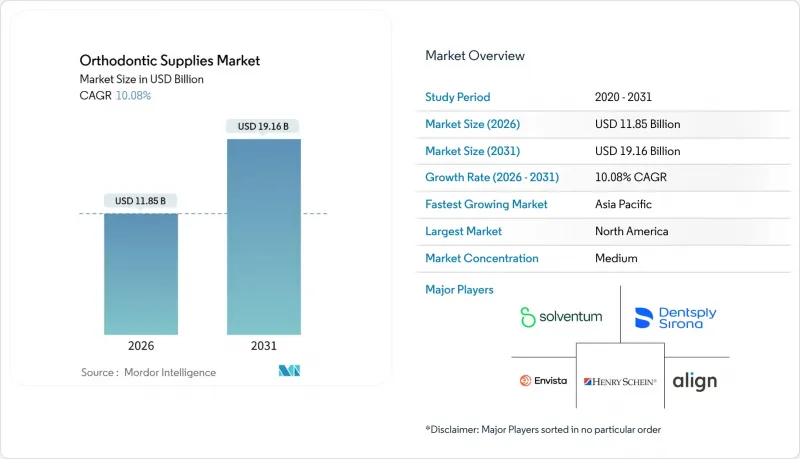

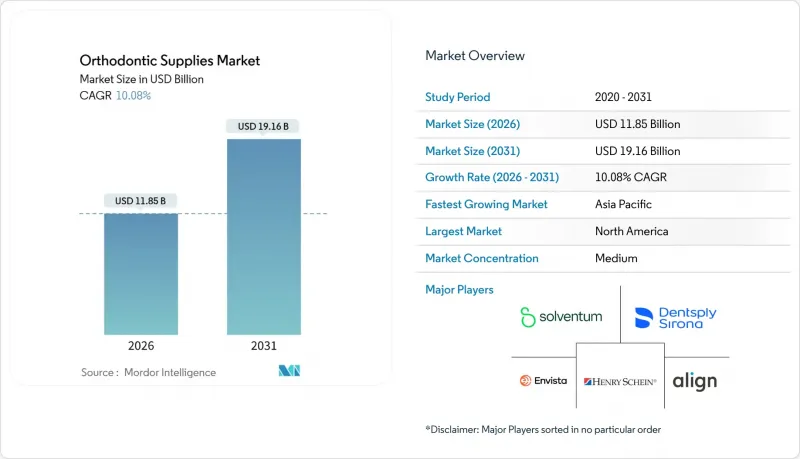

Mordor Intelligence에 의하면, 치과 교정 용품 시장 규모는 2026년에 118억 5,000만 달러로 추정되고 예측 기간(2026-2031년)에서 CAGR 10.08%로 성장을 지속하여, 2031년에는 191억 6,000만 달러에 이를 전망입니다.

본 보고서는 제품 유형(브래킷, 아치와이어, 밴드 및 구강측 튜브, 리가처, 앵커 장치, 투명 교정기, 리테이너, 접착제, 기타), 소재(금속, 세라믹 등), 환자층(소아 등), 최종 사용자(병원, 치과 등), 지역(북미 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 치과 교정 용품 시장 동향 및 인사이트

부정교합 유병률 증가

WHO의 자료에 따르면, 부정교합은 “'침묵의 공중보건 부담' 로 규정되어 있지만, 치료 접근의 장벽으로 인해 치료 이용률은 제한되고 있습니다. 인도 및 인도네시아 치과의사협회는 현재 진단부터 치료 시작까지의 기간을 단축하기 위한 인식 제고 활동을 전개하고 있으며, 잠재적인 수요를 실제 치료 시작으로 이어가고 있습니다. 대중 시장을 겨냥한 저가형 금속 브라켓과 부유층을 위한 프리미엄 세라믹 옵션 등 다층적인 제품 포트폴리오를 갖춘 공급업체가 그로 인해 발생하는 수요를 포착하고 있습니다. 7-9세 아동을 대상으로 한 조기 개입 지침에 따라 치료 대상 연령대가 확대되면서, 환자 1인당 평생 치료비가 증가하고 있습니다. 인구 단위의 선별 검사를 의무화하고 있는 관할 구역은 없기 때문에 수요 창출 측면에서는 여전히 민간 부문의 노력이 중심이 되고 있습니다.

클리어 얼라이너 분야의 기술적 발전

혁신의 초점은 소재에서 소프트웨어로 옮겨가고 있습니다. 2025년에 승인된 Align Technology의 AI CAD/C 도구(CADe)는 엑스레이 영상상의 랜드마크를 자동으로 표시하여 치료 계획 수립 시간을 40% 단축합니다. 셀프 리게이션 브라켓은 마찰을 줄여 내원 횟수를 감소시킴으로써, 진료 의자의 가동률을 극대화하고자 하는 DSO(치과 진료소 운영 조직)의 요구에 부합합니다. 규제 당국은 투명 교정기의 적응증을 복잡한 소아 치열 확장까지 확대함으로써, 한때 확고한 입지를 차지했던 브라켓 치료 시장 점유율을 빼앗고 있습니다. 통합된 디지털 워크플로우를 갖추지 못한 공급업체는 교정 치과의사들이 업무 부담을 줄여주는 플랫폼을 도입함에 따라, 상품화로 인한 가격 경쟁에 직면하게 될 것입니다.

높은 치료비와 제한된 보험 적용 범위

미국의 일반적인 치과 보험 플랜에서는 교정 치료에 대한 보장 한도가 2,000달러 정도로 설정되어 있어, 나머지 3,000-5,000달러는 가구가 본인 부담해야 합니다. 미국 교정치과의사협회(AAO)는 인플레이션으로 인해 가계 예산이 압박받는 가운데, 할부 결제 계획의 연체율이 상승하고 있다고 지적했습니다. 인도나 브라질에서는 치료비가 몇 달 치 수입에 달하기 때문에 치료를 받을 수 있는 사람은 도시 지역의 엘리트 계층으로 한정되어 있습니다. DTC(소비자 직접 판매) 방식의 교정기 브랜드는 클리닉 가격보다 최대 50% 저렴하지만, 감독 체계의 미비에 대한 규제 당국의 단속으로 인해 그 경쟁력이 약화될 가능성이 있습니다.

부문별 분석

2025년, 브라켓은 치과 교정 용품 시장의 33.52%를 차지하며, 얼라이너로는 여전히 해결해야 할 과제가 있는 격렬한 생체역학적 이동이 필요한 증례에서 선호되었습니다. 한편, 성인들이 심미성을 중시하고, 진료석에서 3D 프린팅을 통해 주문형 트레이 제작이 가능해짐에 따라, 투명 교정기는 연평균 성장률(CAGR) 14.25%로 성장하고 있습니다. 아치 와이어와 리가처는 여전히 대량으로 소비되는 소모품이지만, 합금의 배합이 표준화됨에 따라 가격 압박에 직면하고 있습니다. 리테이너는 적극적인 치료가 끝난 후에도 안정적인 지속적인 수입을 가져다주며, 새로운 열가소성 수지 재질의 리테이너는 착용감을 향상시키고 있습니다. 2024년에는 접착제 박리로 인한 리콜이 발생함에 따라, 치과 병원들은 신뢰할 수 있는 품질 보증 데이터를 보유한 공급업체를 우선적으로 선택했습니다.

디지털 생태계 덕분에 수익은 얼라이너 납품과 연계된 소프트웨어 구독 모델로 전환되고 있습니다. 스캐너, AI 기반 치료 계획, 원격 모니터링을 통합한 치과 병원은 공급업체의 플랫폼에 얽매이게 되어, 다른 플랫폼으로 전환하는 데 드는 비용이 높아지고 있습니다. 일시적 고정 장치(TAD)와 같은 특수 장치는 판매량이 적음에도 불구하고, 복잡한 증례를 해결하기 위해 높은 이익률을 유지하고 있습니다. 초기 예방 장치부터 장기적인 유지 장치에 이르기까지 치료의 전 과정을 아우르는 공급업체는 교차 판매를 통해 시장 점유율을 지킬 수 있는 입장에 있습니다.

스테인리스 스틸은 내구성과 합리적인 가격 덕분에 2025년 교정용 의료기기 시장 규모의 44.63%를 차지했습니다. 세라믹 브라켓은 변색에 강하고 치아 색상에 맞추어 제작되는 장치인 만큼, 환자들이 상대적으로 높은 비용을 지불하는 경향이 있어 연평균 성장률(CAGR) 13.51%로 시장이 확대되고 있습니다. 니켈-티타늄 제 초탄성 와이어는 여전히 필수적이지만, 전 세계 생산량의 60-70%가 중국에 집중되어 있어 공급망의 위험 요인으로 작용하고 있습니다. 클리어 얼라이너 시장에서는 힘의 전달과 착용감을 최적화한 독자적으로 개발한 필름을 사용한 폴리머 블렌드가 주류를 이루고 있습니다. 유럽에서 개발된 생체 흡수성 복합재료는 장치 제거를 위한 내원 횟수를 줄여주며, 지속가능성 측면에서도 높은 평가를 받고 있습니다.

아시아공급업체들은 첨단 세라믹 및 폴리머 분야에 막대한 투자를 하고 있으며, 유럽 및 미국의 기존 기업들과의 기술 격차를 좁혀가고 있습니다. 그렇긴 하지만, FDA나 CE 인증을 취득하는 데 있어서는 확립된 규제 대응 체계를 갖추고 ISO 13485 인증을 획득한 공장을 보유한 기업이 여전히 유리합니다.

지역별 분석

2025년, 북미는 전 세계 매출의 36.44%를 차지했습니다. 높은 보험 가입률이 교정 치료비의 일부를 상쇄하고 있어, DSO(치과 서비스 조직)에 의한 업계 재편이 가속화되고 있습니다. 각 벤더사는 서비스 수준, 수량 할인, 대규모 진료 네트워크에 맞춘 통합 디지털 플랫폼을 무기로 경쟁을 펼치고 있습니다. 유럽 시장은 성숙해 있지만 안정적이며, 독일, 프랑스, 영국에서는 지속가능성 목표에 부합하도록 생체 흡수성 소재 개발이 진행되고 있습니다. 의료기기 규제를 준수하는 것은 운영 비용을 증가시키는 한편, 제품의 안전성을 확보하기 위해 자금력이 있는 공급업체에 유리하게 작용합니다.

아시아태평양은 성장의 원동력이며, 2031년까지의 연평균 성장률(CAGR)은 13.01%로 예측됩니다. 중국에서는 2·3선 도시의 의료 투자와, 투명 교정기 보급을 뒷받침하는 가처분 소득 증가가 호재로 작용하고 있습니다. 인도의 도시 지역 클리닉에서는 얼라이너가 적극적으로 도입되고 있지만, 농촌 지역에서는 여전히 경제적 격차가 존재하고 있습니다. 일본과 한국은 성숙한 디지털 치과 생태계를 자랑하며, AI를 활용한 치료 계획 수립과 원격 모니터링이 일상적으로 이루어지고 있습니다. 호주는 규제 체계를 FDA 기준에 부합하도록 조정하여, 태평양을 가로지르는 플랫폼 이전을 간소화하고 있습니다. 이 공급업체는 인프라의 제약을 극복하는 클라우드 기반 치료 계획과 현지 제조 및 유통 파트너를 결합함으로써 성공을 거두고 있습니다.

중동 및 아프리카은 여전히 발전 단계에 있습니다. 수요는 걸프협력회의(GCC) 회원국, 즉 아랍에미리트와 사우디아라비아에 집중되어 있으며, 의료 관광과 외국인 거주자들의 존재가 프리미엄 의료 서비스 수요를 뒷받침하고 있습니다. 남아프리카는 사하라 이남 아프리카에서의 도입을 주도하고 있지만, 소득 격차가 시장 전체의 추가 성장을 저해하고 있습니다. 라틴아메리카에서는 거시경제의 변동에 따라 달라지는 주기적인 수요가 나타납니다. 브라질과 아르헨티나에서는 상당한 판매량을 기록하고 있지만, 환율 변동에 대응하기 위해서는 지역에 맞춘 가격 전략이 필요합니다. 각 공급업체는 유연한 결제 옵션과 모듈식 제품 구성을 통해 지역별 특유의 위험을 완화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.03According to Mordor Intelligence, the orthodontic supplies market size is estimated at USD 11.85 billion in 2026, and is expected to reach USD 19.16 billion by 2031, at a CAGR of 10.08% during the forecast period (2026-2031).

This report is Segmented by Product Type (Brackets, Archwires, Bands & Buccal Tubes, Ligatures, Anchorage Appliances, Clear Aligners, Retainers, Adhesives, Others), Material (Metal, Ceramic, and More), Patient Group (Children, and More), End-User (Hospitals, Dental Clinics, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Orthodontic Supplies Market Trends and Insights

Growing Prevalence of Malocclusions

WHO data frame malocclusion as a silent public-health burden, yet access barriers limit treatment uptake. Dental associations in India and Indonesia now run education drives that shorten diagnosis-to-treatment timelines, translating latent need into active case starts. Vendors with tiered portfolios-low-cost metal brackets for mass markets and premium ceramic options for affluent consumers-capture the resulting volume. Early intervention guidelines for children aged 7-9 extend therapeutic windows, raising lifetime spend per patient. No jurisdiction mandates population-level screening, so private-sector efforts remain central to demand creation.

Technological Advances in Clear Aligners

Innovation has shifted from materials to software. Align Technology's AI CADe tool, cleared in 2025, auto-plots radiographic landmarks and cuts planning time 40%. Self-ligating brackets reduce friction and trim appointment frequency, resonating with DSOs that maximize chair utilization. Regulatory bodies have opened clear-aligner indications to complex pediatric expansion, displacing brackets in a former stronghold. Vendors lacking integrated digital workflows face commodity pricing as orthodontists adopt platforms that save labor.

High Treatment Cost and Limited Insurance Cover

Typical U.S. dental plans cap orthodontic benefits near USD 2,000, leaving households to finance the remaining USD 3,000-5,000. The American Association of Orthodontists noted rising default rates on payment plans as inflation erodes budgets. In India and Brazil, therapy can equal several months of income, restricting uptake to urban elites. DTC aligner brands undercut clinic prices by up to 50%, yet regulator crackdowns on supervision gaps may reduce their edge.

Other drivers and restraints analyzed in the detailed report include:

- AI-Powered Chair-Side Customization

- Expansion of Dental Service Organizations

- Regulatory Scrutiny of Direct-to-Consumer Aligners

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Brackets retained 33.52% of orthodontic supplies market in 2025, favored for severe biomechanical movements that aligners still find challenging. Clear aligners, however, are growing at a 14.25% CAGR as adults prioritize aesthetics and chair-side 3D printing supports on-demand trays. Archwires and ligatures remain high-volume consumables but face price pressure as alloy recipes standardize. Retainers produce steady annuity revenue after active treatment, and newer thermoplastic versions improve comfort. Adhesive bond failures triggered 2024 recalls, prompting clinics to favor suppliers with robust quality-assurance data.

Digital ecosystems tilt revenue toward software subscriptions bundled with aligner deliveries. Practices that integrate scanners, AI-planning, and remote monitoring become locked into vendor platforms, raising switching costs. Specialty appliances such as temporary anchorage devices maintain high margins despite lower volume because they solve complex cases. Suppliers covering the full treatment continuum-from early interceptive devices to long-term retention-are positioned to cross-sell and defend share.

Stainless steel held 44.63% of orthodontic supplies market size in 2025 because of durability and affordability. Ceramic brackets advance at a 13.51% CAGR as patients pay premiums for tooth-colored fixtures that resist staining. Nickel-titanium superelastic wires remain indispensable, yet 60-70% of global production is concentrated in China, driving supply-chain risk. Polymer blends dominate clear aligners, with proprietary films tuned for force delivery and comfort. Bio-resorbable composites developed in Europe eliminate removal appointments and enhance sustainability credentials.

Asian suppliers invest heavily in advanced ceramics and polymers, narrowing technology gaps with Western incumbents. Nonetheless, navigating FDA and CE clearances still favors companies with established regulatory infrastructure and ISO 13485-certified plants.

Complete Report Scope:

- By Product Type

- Brackets

- Archwires

- Bands & Buccal Tubes

- Ligatures

- Anchorage Appliances

- Clear Aligners

- Retainers

- Adhesives

- Others

- By Material

- Metal

- Ceramic

- Nickel-Titanium

- Stainless Steel

- Polymer/Plastics

- Bio-resorbable Materials

- By Patient Group (Age)

- Children (<=12 yrs)

- Teenagers (13-19 yrs)

- Adults (20-40 yrs)

- Older Adults (>40 yrs)

- By End-User

- Hospitals

- Dental Clinics

- Orthodontic & Dentofacial Orthopedic Clinics

- Academic & Research Institutes

- Direct-to-Consumer / At-home

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America produced 36.44% of global revenue in 2025. High insurance penetration offsets a portion of orthodontic costs, and DSOs accelerate consolidation. Vendors compete on service-level performance, volume rebates, and integrated digital platforms tailored to large practice networks. Europe is mature but stable, with Germany, France, and the United Kingdom advancing bio-resorbable materials in line with sustainability goals. Medical Device Regulation compliance raises operating cost yet ensures product safety, favoring well-capitalized suppliers.

Asia-Pacific is the growth engine, forecast at a 13.01% CAGR through 2031. China benefits from healthcare investment in Tier-2 and Tier-3 cities and rising disposable income that supports clear-aligner uptake. India's urban clinics adopt aligners aggressively, although rural affordability gaps persist. Japan and South Korea showcase mature digital dentistry ecosystems, where AI planning and remote monitoring are routine. Australia aligns regulatory frameworks with FDA norms, simplifying trans-Pacific platform transfers. Suppliers succeed by pairing local manufacturing or distribution partners with cloud-based treatment planning that bypasses infrastructure constraints.

The Middle East and Africa remain nascent. Demand concentrates in Gulf Cooperation Council states-United Arab Emirates and Saudi Arabia-where medical tourism and expatriate populations support premium care. South Africa leads sub-Saharan adoption, yet income disparity restrains wider market growth. Latin America shows cyclical demand driven by macroeconomic volatility; Brazil and Argentina deliver sizable volumes but require localized pricing strategies to navigate currency swings. Vendors mitigate regional risks through flexible payment options and modular product configurations.

- Align Technology

- American Orthodontics

- Angelalign Technology

- DB Orthodontics

- Dentaurum

- Dentsply Sirona

- Envista Holdings

- Forestadent

- G&H Orthodontics

- Geniova

- Great Lakes Dental Technologies

- Henry Schein Orthodontics

- Modern Orthodontics

- Rocky Mountain Orthodontics

- SCHEU-DENTAL

- Shenzhen Smartee Denti-Technology

- Solventum

- Straumann Group

- TP Orthodontics

- Ultradent Products

- Zhejiang Protect Orthodontic Appliance

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Prevalence of Malocclusions

- 4.2.2 Rising Disposable Income & Demand for Aesthetics

- 4.2.3 Technological Advances in Clear Aligners/Self-Ligating Braces

- 4.2.4 Expansion Of Dental Service Organizations

- 4.2.5 AI-Powered Digital Chair-Side Customization

- 4.2.6 Eco-Friendly Bio-Resorbable Materials

- 4.3 Market Restraints

- 4.3.1 High Treatment Cost & Limited Insurance Cover

- 4.3.2 Product Recalls & Adverse Effects

- 4.3.3 Supply-Chain Reliance on Niche Alloy Suppliers

- 4.3.4 Regulatory Scrutiny of Direct-To-Consumer Aligners

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Brackets

- 5.1.2 Archwires

- 5.1.3 Bands & Buccal Tubes

- 5.1.4 Ligatures

- 5.1.5 Anchorage Appliances

- 5.1.6 Clear Aligners

- 5.1.7 Retainers

- 5.1.8 Adhesives

- 5.1.9 Others

- 5.2 By Material

- 5.2.1 Metal

- 5.2.2 Ceramic

- 5.2.3 Nickel-Titanium

- 5.2.4 Stainless Steel

- 5.2.5 Polymer/Plastics

- 5.2.6 Bio-resorbable Materials

- 5.3 By Patient Group (Age)

- 5.3.1 Children (<=12 yrs)

- 5.3.2 Teenagers (13-19 yrs)

- 5.3.3 Adults (20-40 yrs)

- 5.3.4 Older Adults (>40 yrs)

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Dental Clinics

- 5.4.3 Orthodontic & Dentofacial Orthopedic Clinics

- 5.4.4 Academic & Research Institutes

- 5.4.5 Direct-to-Consumer / At-home

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Align Technology

- 6.3.2 American Orthodontics

- 6.3.3 Angelalign Technology

- 6.3.4 DB Orthodontics

- 6.3.5 Dentaurum

- 6.3.6 Dentsply Sirona

- 6.3.7 Envista Holdings

- 6.3.8 Forestadent

- 6.3.9 G&H Orthodontics

- 6.3.10 Geniova

- 6.3.11 Great Lakes Dental Technologies

- 6.3.12 Henry Schein Orthodontics

- 6.3.13 Modern Orthodontics

- 6.3.14 Rocky Mountain Orthodontics

- 6.3.15 SCHEU-DENTAL

- 6.3.16 Shenzhen Smartee Denti-Technology

- 6.3.17 Solventum

- 6.3.18 Straumann Group

- 6.3.19 TP Orthodontics

- 6.3.20 Ultradent Products

- 6.3.21 Zhejiang Protect Orthodontic Appliance

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment