|

시장보고서

상품코드

2072493

지붕용 화학제품 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Roofing Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

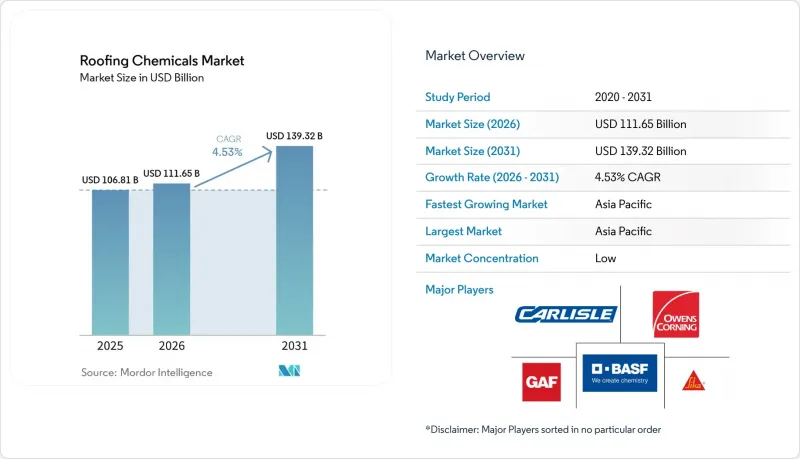

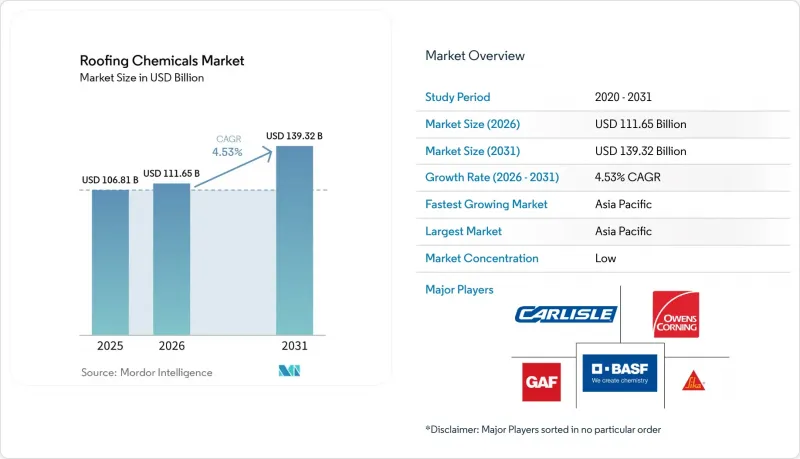

Mordor Intelligence에 의하면, 지붕용 화학제품 시장 규모는 2025년 1,068억 1,000만 달러로 평가되었습니다. 2026년에는 1,116억 5,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 4.53%로 성장을 지속하여, 2031년에는 1,393억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품별(아스팔트계, 아크릴 수지, 에폭시 수지, 엘라스토머, 스티렌, 기타 제품 유형), 최종 사용자 산업별(주택, 상업, 기타 최종 사용자 산업), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 지붕용 화학제품 시장 동향 및 인사이트

건설 및 인프라 부문의 확대

대규모 경기 부양책과 도시화 프로젝트를 배경으로, 전 세계 건설 지출은 증가 추세를 보이고 있습니다. 미국에서는 “'인프라 투자 및 고용법' 이에 따라 일반 도로 및 시도로 공사에 1,260억 달러가 투입되었으며, 이는 전년 대비 16% 증가한 수치입니다. 이러한 추세는 교량, 교통 허브, 정비 거점에서의 보호용 지붕 코팅 수요에도 영향을 미치고 있습니다. 시멘트, 목재, 인건비 상승으로 인해 도급업체의 이익률은 계속해서 압박을 받고 있으며, 내구성이 뛰어나면서도 가격 경쟁력이 있는 아스팔트계 방수 시트의 매력이 높아지고 있습니다. 수주 잔고는 견조한 추세를 보이고 있지만, 인력 부족으로 인해 시공업체들은 현장에서의 노동 시간을 줄일 수 있는 미리 혼합된 스프레이 도포식 시스템으로의 전환을 추진하고 있습니다.

노후화된 건축물과 지붕 재시공 공사

현재 북미와 유럽에서는 신축 수요를 웃도는 규모로, 부득이하게 지붕을 교체해야 하는 수요가 발생하고 있습니다. 1980년대 후반 호황기에 건설된 상업시설들이 내구 연한의 막바지에 접어들면서, 고성능 화학 물질을 활용한 개보수를 중심으로 한 예측 가능한 개보수 공사 수요가 발생하고 있습니다. 미국의 지붕 공사 서비스 부문은 2023년에 275억 달러의 매출을 기록했습니다. 이는 소유주가 유지보수 주기를 연장하고 점점 더 높아지는 에너지 효율 목표를 충족하는 고성능 방수 시트를 선택한 데 힘입은 결과입니다. 안정적인 지붕 재시공 주기가 예상에 따라, 지붕용 화학제품 시장은 신축 공사의 경기 변동에 따른 침체의 영향을 덜 받게 되었습니다.

원유 가격의 변동

아스팔트 계열 제품 라인은 원자재 비용의 변동성으로 인해 지속적인 이익률 압박에 직면해 있습니다. 조사에 따르면, 원유 가격이 1% 상승하면 3개월의 시차를 두고 아스팔트 가격이 0.58% 상승하는 것으로 나타났습니다. 2024년, 아스팔트 슁글 및 코팅 재료 제조업의 생산자물가지수는 2.19% 하락한 293.79를 기록했으며, 이는 최근 원유 가격의 안정세를 반영한 것입니다. 그렇긴 하지만, 이러한 변동성이 지속되는 것은 여전히 중요한 전략적 과제로 남아 있습니다. 각 제조업체는 성능 기준을 유지하면서 석유 의존도를 낮추는 것을 목표로 한 하이브리드 배합 개발을 통해 이 과제에 대응하고 있습니다. 이러한 변동성은 가격에 민감한 시장 부문에 큰 영향을 미치는 한편, 보다 안정적인 투입 비용을 실현하는 바이오 대체재에 대한 기회를 창출하고 있습니다.

부문별 분석

2025년, 아스팔트계 방수 시트는 시공업체들이 다루기 쉽다는 점과 초기 비용의 경제성이 높다는 점을 강점으로 삼아 31.58%의 시장 점유율을 유지하며 시장을 선도했습니다. SBS 개질 시트 등의 고분자 강화형 제품은 저온 유연성과 내피로성이 향상되어, 고성능 대체재의 등장에도 불구하고 그 존재 가치를 확고히 하고 있습니다. 그러나 지붕용 화학제품 시장이 저VOC, 쿨루프, 속경화 등의 요건으로 전환됨에 따라 폴리우레탄, 실리콘, 아크릴계 코팅 시장은 연평균 성장률(CAGR) 5.44%로 확대되고 있습니다. 다우사의 바이오 제품 ‘"NORDEL REN EPDM" 이는 기존의 성능을 유지하면서 재생 가능한 원료로의 전환을 실현하고 있습니다.

연구개발(R&D)의 초점은 아스팔트의 인성과 폴리머의 반사율 및 탄성을 융합한 하이브리드 시스템에 맞추어져 있습니다. 수성 폴리우레탄 분산액은 현재 20 MPa를 초과하는 인장 강도와 50 g/L 미만의 VOC 수준을 달성하고 있어, 지자체 보수 프로그램의 사양 채택을 위한 입지가 확고히 자리 잡았습니다. 개질 아크릴계 제품은 쿨루프의 틈새 시장을 휩쓸고 있는 반면, 실리콘계 탑코트는 경사가 완만한 지붕 구조에서 물 고임에 대한 내성 면에서 우위를 점하고 있습니다. 이처럼 잇따르는 혁신으로 인해 지붕용 화학제품 시장의 경쟁이 치열해지고 있으며, 배합에 유연성을 갖춘 공급업체에게는 미개척 시장 기회가 열리고 있습니다.

지역별 분석

아시아태평양은 2025년에 전 세계 매출의 44.02%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 5.04%를 나타낼 것으로 전망되어, 지붕용 화학제품 시장에서 가장 규모가 크고 가장 빠르게 성장하는 지역으로 자리매김하고 있습니다. 중국의 부동산 및 인프라 확충 추진에 힘입어 SBS 개질 아스팔트가 계속해서 주류를 이루고 있습니다. 한편, 인도에서는 교통 회랑 및 산업단지 건설 계획이 추진되고 있어, 고분자 강화형·반사성 코팅의 도입이 가속화되고 있습니다. 시카사가 최근 중국과 싱가포르에서 진행한 공장 투자는 모르타르 및 지붕 시스템의 현지 생산을 위한 공급업체의 노력을 여실히 보여주고 있습니다.

북미는 여전히 지붕 교체 수요가 시장을 주도하는 지역입니다. “"제목 24" 이와 같은 도시 조례에 따라, 지붕용 화학제품 시장은 고반사율·저VOC 제품으로 전환되고 있습니다. 또한, 2024년에 310억 달러에 달한 폭풍우 피해 보상금 지급은 내충격성 화학물질의 필요성이 시급하다는 점을 여실히 보여주고 있습니다. 이 지역의 지붕용 화학제품 시장 규모는 인프라 관련 법안에 따라 자금을 지원받은 학교, 공항, 연방 시설 등의 공공 부문에서 진행되는 개보수 공사에 힘입어 더욱 확대되고 있습니다.

유럽에서는 지속가능성을 위한 노력이 추진되고 있습니다. ““REACH”규제 의무와 순환형 경제 목표에 따라, 배합 제조업체들은 유해한 용제를 배제하고 재활용 경로를 도입하고 있습니다. 생고뱅(Saint-Gobain)사가 아스팔트 슁글 재활용 기술을 인수한 것은 지붕용 화학약품 시장에서 폐쇄형 순환(closed-loop) 개념이 주류로 자리 잡아가고 있음을 보여줍니다. 시장 성장은 에너지 순수지급이 발생하는 개보수 공사에 보조금 프로그램이 적용되는 독일, 프랑스, 북유럽 국가들에 집중되어 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the roofing chemicals market size is expected to grow from USD 106.81 billion in 2025 to USD 111.65 billion in 2026 and is forecast to reach USD 139.32 billion by 2031 at 4.53% CAGR over 2026-2031.

This report is Segmented by Product (Bituminous, Acrylic Resin, Epoxy Resin, Elastomers, Styrene, Other Product Types), End-User Industry (Residential, Commercial, Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Roofing Chemicals Market Trends and Insights

Expansion of Construction and Infrastructure Sector

Global construction outlays are climbing on the back of large-scale stimulus and urbanization projects. In the United States, the Infrastructure Investment and Jobs Act is driving USD 126 billion in public highway and street work, a 16% year-on-year uplift that spills over into demand for protective roofing coatings on bridges, transit hubs and maintenance depots. Elevated cement, lumber and labor costs continue to squeeze contractor margins, amplifying the appeal of durable yet price-competitive bituminous membranes. Project backlogs remain healthy, but workforce shortages are prompting applicators to shift toward pre-formulated, spray-applied systems that reduce on-site labor hours.

Aging Building Stock and Roof Replacement Projects

Non-discretionary re-roofing now outweighs new-build demand in North America and Europe. Commercial facilities erected during the late-1980s boom are reaching end-of-service life, creating a predictable stream of retrofit work anchored in premium chemical upgrades. The U.S. roofing services sector generated USD 27.5 billion in 2023, buoyed by owners opting for high-performance membranes that extend service intervals and meet rising energy-efficiency targets. Stable replacement-cycle visibility shields the roofing chemicals market from cyclical dips in new construction.

Crude-Oil Price Volatility

Bituminous product lines face sustained margin pressures due to instability in raw material costs. Studies indicate that a 1% increase in crude oil prices results in a 0.58% rise in asphalt prices, with a lag of three months. In 2024, the Producer Price Index for Asphalt Shingle and Coating Materials Manufacturing decreased by 2.19% to 293.79, reflecting the recent moderation in crude oil prices. Nevertheless, the persistent volatility remains a critical strategic concern. Manufacturers are addressing this challenge by developing hybrid formulations aimed at reducing petroleum dependency while preserving performance standards. This volatility significantly impacts price-sensitive market segments and creates opportunities for bio-based alternatives that offer more stable input costs.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Energy-Efficient and Cool Roofs

- Increasing Climate Resilience and Waterproofing Needs

- Stringent VOC/REACH Caps on Bitumen

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bituminous membranes retained a 31.58% leadership position in 2025 on the strength of contractor familiarity and attractive upfront economics. Polymer-enhanced variants such as SBS-modified sheets are improving cold-flex and fatigue resistance, ensuring relevance despite the advance of high-performing alternatives. Yet polyurethane, silicone and acrylic coatings are expanding at a 5.44% CAGR as the roofing chemicals market shifts toward low-VOC, cool-roof and rapid-cure requirements. Dow's bio-based NORDEL REN EPDM illustrates the pivot to renewable feedstocks while matching legacy performance.

R&D focus is trained on hybrid systems that marry the toughness of bitumen with the reflectance or elasticity of polymers. Waterborne polyurethane dispersions now offer tensile strengths above 20 MPa with VOC levels below 50 g/L, positioning them for specification in municipal retrofit programs. Modified acrylics dominate the cool-roof niche, while silicone topcoats win on ponding-water resistance in low-slope assemblies. This cascade of innovation keeps the roofing chemicals market competitive and opens white-space opportunities for suppliers with formulation agility.

Complete Report Scope:

- By Product

- Bituminous

- Acrylic Resin

- Epoxy Resin

- Elastomers

- Styrene

- Other Product Types (Polyurethane, Silicone, etc.)

- By End-user Industry

- Residential

- Commercial

- Other End-user Industries (Industrial and Infrastructure)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Geography Analysis

Asia-Pacific accounted for 44.02% of global revenue in 2025 and is projected to record a 5.04% CAGR to 2031, making it both the largest and fastest-advancing arena for the roofing chemicals market. China's real-estate and infrastructure push keeps SBS-modified bitumen at the forefront, while India's pipeline of transport corridors and industrial parks accelerates adoption of polymer-enhanced, reflective coatings. Sika's recent plant investments in China and Singapore demonstrate supplier commitment to localized production of mortars and roof systems.

North America remains a replacement-driven arena. Title 24 and similar city codes are steering the roofing chemicals market toward high-reflectance, low-VOC products, while USD 31 billion in 2024 storm-damage payouts underscore the urgency for impact-resistant chemistries. The region's roofing chemicals market size is further supported by public-sector retrofits of schools, airports and federal facilities funded under infrastructure legislation.

Europe advances on a sustainability mandate. REACH obligations and circular-economy targets are prompting formulators to remove hazardous solvents and embrace recycling pathways. Saint-Gobain's acquisition of asphalt-shingle recycling technology signals mainstream acceptance of closed-loop concepts within the roofing chemicals market. Market growth concentrates in Germany, France and the Nordics, where subsidy programs reward energy-positive refurbishment.

- Akzo Nobel N.V.

- BASF

- Carlisle Companies Inc.

- Dow

- Eastman Chemical Company

- GAF Materials LLC

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- HOLCIM

- Johns Manville

- Kemper System

- Owens Corning

- PPG Industries, Inc.

- RPM International Inc.

- Saint-Gobain

- Sika AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Construction and Infrastructure Sector

- 4.2.2 Aging Building Stock and Roof Replacement Projects

- 4.2.3 Growing Demand for Energy-Efficient and Cool Roofs

- 4.2.4 Increasing Climate Resilience and Waterproofing Needs

- 4.2.5 Insurance-Led Push for Class-A Fire-rated Chemistries

- 4.3 Market Restraints

- 4.3.1 Crude-oil Price Volatility

- 4.3.2 Stringent VOC/REACH Caps on Bitumen

- 4.3.3 Skilled-Labour Shortage for Spray-Applied Systems

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Bituminous

- 5.1.2 Acrylic Resin

- 5.1.3 Epoxy Resin

- 5.1.4 Elastomers

- 5.1.5 Styrene

- 5.1.6 Other Product Types (Polyurethane, Silicone, etc.)

- 5.2 By End-user Industry

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Other End-user Industries (Industrial and Infrastructure)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 BASF

- 6.4.3 Carlisle Companies Inc.

- 6.4.4 Dow

- 6.4.5 Eastman Chemical Company

- 6.4.6 GAF Materials LLC

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 HOLCIM

- 6.4.10 Johns Manville

- 6.4.11 Kemper System

- 6.4.12 Owens Corning

- 6.4.13 PPG Industries, Inc.

- 6.4.14 RPM International Inc.

- 6.4.15 Saint-Gobain

- 6.4.16 Sika AG

7 Market Opportunities and Future Outlook

- 7.1 Development of Bio-based Roofing Chemicals

- 7.2 White-space and Unmet-need Assessment