|

시장보고서

상품코드

2072544

아시아태평양의 특수 비료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific Specialty Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

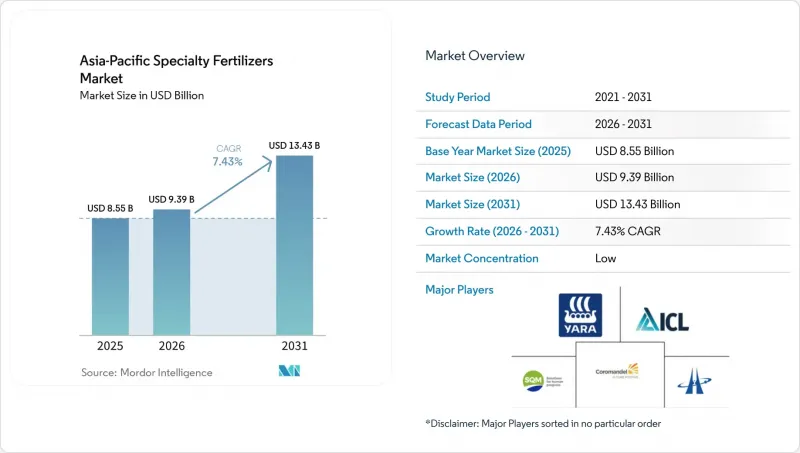

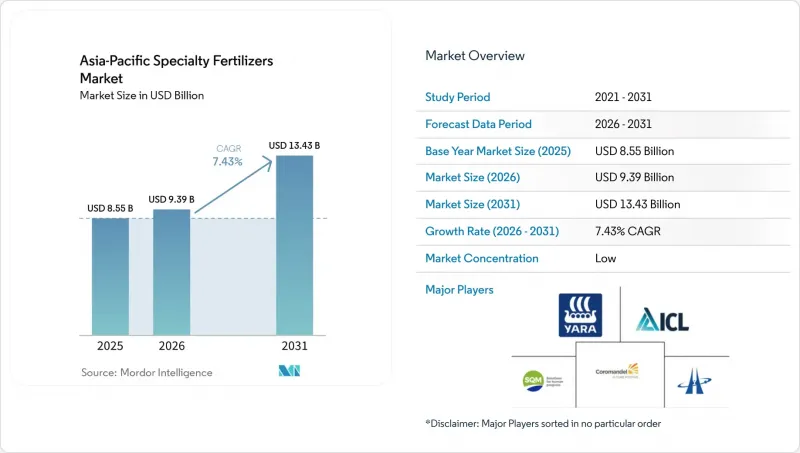

Mordor Intelligence에 의하면, 아시아태평양의 특수 비료 시장 규모는 2025년에 85억 5,000만 달러로 평가되었습니다. 2026년 93억 9,000만 달러에서 2031년까지 134억 3,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 7.43%를 나타낼 전망입니다.

본 보고서는 특수 비료의 유형(CRF, 액체 비료, SRF, 수용성 비료), 시용 방법(비료 관개, 엽면 시비, 토양 시비), 작물 유형(밭작물, 원예작물, 잔디 및 관상용 작물), 그리고 국가(호주, 방글라데시, 중국, 인도, 인도네시아, 일본 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(미터톤) 단위로 제시되어 있습니다.

아시아태평양의 특수 비료 시장 동향 및 인사이트

정밀 시비 도입

정밀 시비 방식의 도입은 자동 관개 시스템과 원활하게 연동되는 수용성 및 액상 제제에 대한 수요를 창출하며, 아시아태평양의 특수 비료 시장을 재편하고 있습니다. 중국 국가발전개혁위원회는 2024년에 물·비료 통합 프로젝트에 28억 달러를 배정했고, 2027년까지 500만 헥타르 규모의 새로운 비료 공급 인프라를 구축하는 것을 목표로 하고 있습니다. 이러한 정책적 지원은 이 기술이 살포 시비에 비해 비료 소비량을 20-30% 줄이면서도 작물 수확량을 15-25% 늘릴 수 있다는 것이 입증된 능력을 반영한 것입니다. 이러한 경제적 이점은 특히 고부가가치 작물에서 두드러지며, 비료 및 관개 시스템을 통해 중요한 생육 단계에 필요한 미량 영양소의 혼합물을 정확하게 공급함으로써 식물의 영양 공급과 자원 활용을 모두 최적화할 수 있습니다.

정부의 양분 효율화 장려책

아시아태평양의 선진 시장에서 시행되는 정부 인센티브 프로그램은 직접 보조금이나 세제 혜택 등을 통해 방출 조절 비료 및 고효율 비료에 대한 인위적인 수요 프리미엄을 창출하고 있습니다. 2024년에 2,500억 엔(16억 8,000만 달러)을 투입해 시작된 일본의 ‘K 프로그램’에서는 특수 비료를 주요 농산물로 지정하고, 비용의 50%를 보조하는 대상으로 삼고 있습니다. 이러한 정책 개입으로 인해, 기존에 방출 조절 비료의 보급을 제한하던 가격 프리미엄이 사실상 해소되면서, 시장의 펀더멘털을 넘어서는 수요 패턴의 구조적 변화가 초래되고 있습니다.

제품 구매 시 발생하는 고액의 초기 비용

특수 비료는 기존 NPK 비료에 비해 200-400%의 가격 프리미엄이 붙어 있어, 특히 아시아태평양 농업 생산자의 80%를 차지하며 금융 지원이나 위험 관리 도구에 대한 접근성이 제한된 소규모 농가에게 있어 도입에 큰 장벽이 되고 있습니다. 서방형 요소의 가격은 보통 1톤당 800-1,200달러인 반면, 기존 요소는 300-400달러이므로 농가에서는 비료 구입을 위해 2-3배의 운영 자금을 투입해야 합니다. 이러한 비용 차이는 상품 가격이 투입 비용 상승을 흡수할 수 있는 여지가 제한적인 쌀이나 밀 생산자들에게 특히 큰 과제로 대두되고 있으며, 농업적 효과가 입증되었음에도 불구하고 도입에 있어 구조적인 장벽이 되고 있습니다.

부문별 분석

아시아태평양의 특수 비료 시장에서 액체 비료는 시장 점유율의 54.0%(2025년 기준)를 차지하고 있으며, 이 지역의 집약형 농업 지역에서 급속히 확대되고 있는 정밀 시비 시스템과의 원활한 호환성이 그 원동력이 되고 있습니다. 이 부문의 선도적 지위는 작물 수확량을 최적화하기 위해 정확한 영양분 계량과 균일한 살포가 필수적인 자동 시비 시스템에서 액상 제제가 지닌 근본적인 장점을 반영하고 있습니다.

방출 조절 비료는 환경 규제와 탄소 크레딧 제도가 영양소 손실 및 온실가스 배출을 줄이는 기술을 점점 더 중시함에 따라, 2026년부터 2031년까지 연평균 성장률(CAGR) 7.8%를 기록하며 가장 빠르게 성장하는 부문으로 자리매김하고 있습니다. 방출 조절 비료 중에서도 폴리머 코팅 부문은 미세 플라스틱 규제라는 새로운 과제에 직면해 있으며, 환경에 대한 우려를 해소하면서도 방출 특성을 유지할 수 있는 팜 스테아린, 키토산, 전분계 폴리머 등의 생분해성 코팅 소재를 위한 혁신이 추진되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 개 보고서의 내용

제3장 주요 요약 및 주요 조사 결과

제4장 주요 업계 동향

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 비료 업계 CEO가 직면하는 중요 전략적 과제

KTHAccording to Mordor Intelligence, the asia-Pacific specialty fertilizer market size was valued at USD 8.55 billion in 2025 and estimated to grow from USD 9.39 billion in 2026 to reach USD 13.43 billion by 2031, at a CAGR of 7.43% during the forecast period (2026-2031).

This report is Segmented by Specialty Type (CRF, Liquid Fertilizer, SRF, and Water Soluble), by Application Mode (Fertigation, Foliar, Soil), by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental), and by Country (Australia, Bangladesh, China, India, Indonesia, Japan, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Asia-Pacific Specialty Fertilizers Market Trends and Insights

Precision Fertigation Adoption

Precision fertigation adoption is reshaping the Asia-Pacific specialty fertilizer landscape by creating demand for water-soluble and liquid formulations that integrate seamlessly with automated irrigation systems. China's National Development and Reform Commission allocated USD 2.8 billion in 2024 for water-fertilizer integration projects, targeting 5 million hectares of new fertigation infrastructure by 2027. This policy push reflects the technology's proven ability to reduce fertilizer consumption by 20-30% while increasing crop yields by 15-25% compared to broadcast applications. The economic advantage becomes particularly compelling for high-value crops where fertigation systems can deliver targeted micronutrient blends during critical growth stages, optimizing both plant nutrition and resource utilization.

Government Nutrient-Efficiency Incentives

Government incentive programs across developed Asia-Pacific markets are creating artificial demand premiums for controlled-release and enhanced-efficiency fertilizers through direct subsidies and tax relief mechanisms. Japan's K Program, launched in 2024 with JPY 250 billion (USD 1.68 billion) in funding, designates specialty fertilizers as critical agricultural products eligible for 50% cost-sharing support. This policy intervention effectively eliminates the price premium that historically limited controlled-release fertilizer adoption, creating a structural shift in demand patterns that extends beyond market fundamentals.

High Upfront Product Cost

The 200-400% price premium of specialty fertilizers over conventional NPK creates significant adoption barriers, particularly among smallholder farmers who represent 80% of Asia-Pacific agricultural producers and operate with limited access to credit and risk management tools. Controlled-release urea typically costs USD 800-1,200 per tonne compared to USD 300-400 for conventional urea, requiring farmers to invest 2-3 times more working capital for fertilizer purchases. This cost differential becomes particularly challenging for rice and wheat producers, where commodity prices provide limited margin to absorb input cost increases, creating a structural barrier to adoption that persists despite proven agronomic benefits.

Other drivers and restraints analyzed in the detailed report include:

- Shift to High-Value Horticulture

- Soil Micronutrient Depletion

- Polymer and Potash Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid fertilizers dominate the Asia-Pacific specialty fertilizer market share, accounting for 54.0% in 2025, driven by their seamless compatibility with precision fertigation systems that are expanding rapidly across the region's intensive agricultural areas. The segment's leadership position reflects the fundamental advantage of liquid formulations in automated application systems where precise nutrient metering and uniform distribution are critical for optimizing crop performance.

Controlled-release fertilizers represent the fastest-growing segment, with a 7.8% CAGR through 2026 to 2031, as environmental regulations and carbon credit programs increasingly favor technologies that reduce nutrient losses and greenhouse gas emissions. The polymer-coated segment within controlled-release fertilizers faces emerging challenges from microplastic regulations, driving innovation toward biodegradable coating materials, including palm stearin, chitosan, and starch-based polymers that maintain release characteristics while addressing environmental concerns

Complete Report Scope:

- Speciality Type

- CRF

- Polymer Coated

- Polymer-Sulfur Coated

- Others

- Liquid Fertilizer

- SRF

- Water Soluble

- CRF

- Application Mode

- Fertigation

- Foliar

- Soil

- Crop Type

- Field Crops

- Horticultural Crops

- Turf & Ornamental

- Country

- Australia

- Bangladesh

- China

- India

- Indonesia

- Japan

- Pakistan

- Philippines

- Thailand

- Vietnam

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- Yara International ASA

- ICL Group Ltd

- Sociedad Quimica y Minera de Chile SA

- Coromandel International Ltd.

- Huaqiang Chemical Group Stock Co., Ltd.

- Haifa Chemicals Ltd

- Compo Expert GmbH (Grupa Azoty S.A.)

- Kingenta Ecological Engineering Group Co. Ltd

- Nutrien Ltd

- Koch Industries Inc

- Hebei Sanyuan Jiuqi Fertilizer Co. Ltd

- Shandong Luxi Chemical Co. Ltd

- Hubei Xinyangfeng Fertilizer Co. Ltd

- Zhongchuang Xingyuan Chemical Technology Co. Ltd

- Zouping Hongyun Biotechnology Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Precision fertigation adoption

- 4.6.2 Government nutrient-efficiency incentives

- 4.6.3 Shift to high-value horticulture

- 4.6.4 Soil micronutrient depletion

- 4.6.5 E-commerce access to niche inputs

- 4.6.6 Carbon-credit backed N?O-reduction demand

- 4.7 Market Restraints

- 4.7.1 High upfront product cost

- 4.7.2 Polymer and potash price volatility

- 4.7.3 Emerging microplastic-coating bans

- 4.7.4 Cold-chain gaps for liquid products

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Speciality Type

- 5.1.1 CRF

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 SRF

- 5.1.4 Water Soluble

- 5.1.1 CRF

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

- 5.4 Country

- 5.4.1 Australia

- 5.4.2 Bangladesh

- 5.4.3 China

- 5.4.4 India

- 5.4.5 Indonesia

- 5.4.6 Japan

- 5.4.7 Pakistan

- 5.4.8 Philippines

- 5.4.9 Thailand

- 5.4.10 Vietnam

- 5.4.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Yara International ASA

- 6.4.2 ICL Group Ltd

- 6.4.3 Sociedad Quimica y Minera de Chile SA

- 6.4.4 Coromandel International Ltd.

- 6.4.5 Huaqiang Chemical Group Stock Co., Ltd.

- 6.4.6 Haifa Chemicals Ltd

- 6.4.7 Compo Expert GmbH (Grupa Azoty S.A.)

- 6.4.8 Kingenta Ecological Engineering Group Co. Ltd

- 6.4.9 Nutrien Ltd

- 6.4.10 Koch Industries Inc

- 6.4.11 Hebei Sanyuan Jiuqi Fertilizer Co. Ltd

- 6.4.12 Shandong Luxi Chemical Co. Ltd

- 6.4.13 Hubei Xinyangfeng Fertilizer Co. Ltd

- 6.4.14 Zhongchuang Xingyuan Chemical Technology Co. Ltd

- 6.4.15 Zouping Hongyun Biotechnology Co. Ltd