|

시장보고서

상품코드

2072591

피부 독성 시험 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Dermal Toxicity Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

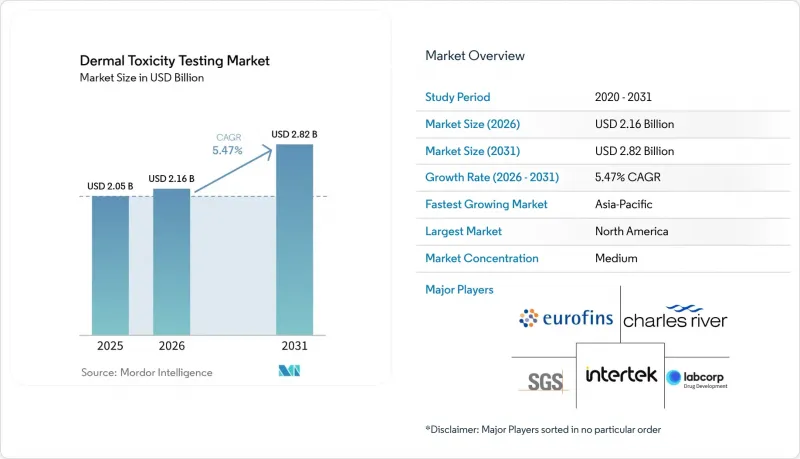

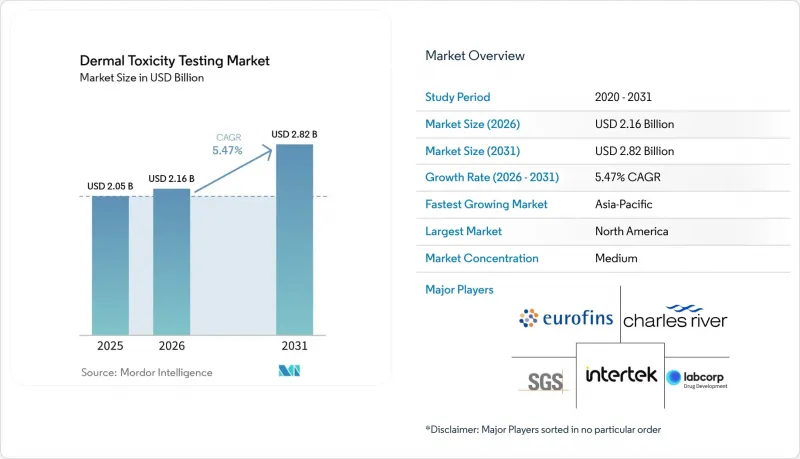

Mordor Intelligence에 의하면, 피부 독성 시험 시장 규모는 2025년에 20억 5,000만 달러로 평가되었습니다. 2026년에 21억 6,000만 달러에 달하고, 2031년까지 28억 2,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 5.47%로 성장할 전망입니다.

본 보고서는 시험 유형(in vitro, in silico, ex vivo, in vivo), 독성 평가 지표(피부 자극, 부식성, 감작성, 흡수성, 광독성), 최종 사용자(화장품, 제약, 화학, CRO, 학술 기관), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 피부 독성 시험 시장 동향 및 인사이트

화장품에 대한 동물 실험 규제에 따른 금지

여러 관할 구역에서 동물 실험 금지가 법제화됨에 따라, 경피 독성 시험 시장에 유리한 구조적 수요 변화가 발생했습니다. 유럽연합(EU)이 10년 전에 도입한 판매 제한 조치에 발맞추어, 2024년까지 미국 내 12개 주에서 종합적인 금지 조치를 시행했습니다. 2023년 12월 캐나다에서 제정된 법률에 따라, 이러한 움직임은 북미 전역으로 확산되었습니다. 현재 규제의 초점은 화학 물질과 의약품 분야로도 확대되고 있습니다. 미국 환경보호청(EPA)은 2024년 말까지 경피적 평가 지표와 관련된 140개의 대체 방법을 승인했으며, FDA의 2025년 로드맵에서는 임상시험용 의약품 신청(IND) 시 비동물 시험법(NAM)의 채택이 공식적으로 권장되고 있습니다. 일본은 2024년에 비동물 실험 프로토콜에 관한 지침을 발표하며, 아시아태평양과 보조를 맞췄습니다. 이러한 움직임들이 맞물리면서, NAM 데이터를 보유하지 않은 기업의 경우 규정 준수 리스크가 높아지고 있으며, 시험 예산은 검증된 in vitro 및 in silico 서비스로 전환되고 있습니다.

FDA 및 OECD의 체외(in vitro) 및 컴퓨터 시뮬레이션(in silico) 분석법 승인 가속화

FDA는 2025년 4월에 발표한 ““전임상 안전성 시험에서의 동물 실험 감축을 위한 로드맵”에서 ‘오르간 온 칩(Organ-on-Chip)’, AI 기반 모델링 및 가상 환자 시뮬레이션을 권장하며, 이를 조기에 도입한 기업에 대해서는 심사 절차를 간소화해 주고 있습니다. OECD는 2024년에 시험 지침 497호 및 496호의 개정을 신속히 추진하여, 오믹스 기반의 측정값 및 데이터 공유 체계를 통합했습니다. 캐나다는 2024년 9월, CEPA(캐나다 환경보호법)에 따라 2035년까지 NAMs로의 완전한 전환을 목표로 하는 보완적 전략안을 발표했습니다. 승인 절차가 신속해짐에 따라, 오랫동안 병목 현상을 일으켜 온 규제상의 불확실성이 해소됨에 따라, 피부 독성 시험 시장에서 확고한 입지를 다지고 있는 플랫폼 제공업체들에게 연구 개발의 투자 대비 효과가 더욱 높아질 것입니다.

일부 체외분석(In-Vitro Assays)법과 인간의 예후 간의 예측적 상관관계는 제한적

분석 결과가 임상 관찰 결과와 차이가 나는 경우, 특히 선천면역과 후천면역이 관여하는 피부 감작과 같은 복잡한 평가 지표에 대해서는 규제 당국이 여전히 신중한 입장을 고수하고 있습니다. 인간의 예측 패치 테스트 데이터셋에는 변동성이 관찰되며, 현재의 RHE 모델로는 이를 재현하기 어렵습니다. OECD는 가이드라인 승인에 앞서 여러 연구소가 참여하는 링 테스트를 의무화하고 있으며, 이로 인해 상품화까지의 기간이 길어지고 있습니다. 소규모 개발 기업 입장에서는 이러한 연구에 필요한 자금을 조달하는 데 있어 장벽이 매우 높습니다. 오믹스 수준의 분석과 3D 조직을 통합함으로써, 더 상세한 메커니즘의 규명이 기대되지만, 표준 프로토콜의 조화는 아직 진행 중입니다.

부문별 분석

2025년, 체외(in vitro) RHE 시스템은 OECD TG 439 및 TG 431의 승인을 바탕으로 피부 독성 시험 시장 점유율에서 49.19%로 가장 높은 비중을 차지했습니다. 혈관화 구조물의 검증 파이프라인이 완성됨에 따라, RHE 플랫폼을 활용한 피부 독성 시험 시장 규모는 꾸준히 확대될 것으로 전망됩니다. 인실리코 분석은 수백만 건의 화학 정보학 기록을 통합한 AI 라이브러리의 지원에 힘입어, 2031년까지 연평균 성장률(CAGR) 5.62%라는 가장 높은 성장률을 기록하고 있습니다.

RHE의 성숙도는 재현성이 있는 장벽 기능 지표와 GLP 실험실로의 전환 용이성에 부분적으로 기인합니다. iPS 세포 유래 각질세포의 확보와 같은 반복적인 개선을 통해 기증자 간 편차 위험이 줄어들고, 무제한의 세포 은행이 확보됩니다. 신속한 인실리코 스크리닝과 확인을 위한 RHE 시험을 결합한 하이브리드 전략은 개발 주기를 단축하고 시약 비용을 절감합니다. 이는 세계 포트폴리오를 확장하려는 기업들에게 매력적인 제안입니다. 그러나 3D 바이오 프린팅 피부는 여전히 처리량 측면에서 병목 현상에 직면해 있어, 생리학적 관련성이 높음에도 불구하고 단기적인 시장 점유율 확대에는 한계가 있습니다.

OECD의 체외 피부 모델(MUG-hOSEC) 승인은 면역 기능을 갖춘 분석법의 틈새 시장 내 채택을 확고히 하고 있습니다. 피하 지방층을 분석에 포함시킴으로써 대사 정확도가 향상되며, 더 단순한 조직에서는 감지할 수 없는 계면활성제에 의한 지질 이상이 밝혀집니다. 한편, 케미인포매틱스 알고리즘은 실증 데이터가 부족한 시장에 새롭게 진입하는 자외선 차단제에 대해 예측 독성학의 가능성을 열어주고 있습니다. 이 두 가지 흐름, 즉 생물학적 정교화와 디지털 시뮬레이션을 통해 피부 독성 시험 시장은 ‘습식 실험실’과 ‘건식 실험실’ 중 하나를 선택해야 하는 상황이 아니라, 통합된 시험 생태계로서의 입지를 확립해 가고 있습니다.

지역별 분석

2025년 북미 시장 점유율 42.68%는 성숙한 CRO(위탁 연구 기관) 환경, FDA의 적극적인 태도, 그리고 풍부한 벤처 캐피털을 반영했습니다. 또한, 이 지역에는 바이오 프린팅 관련 스타트업이 가장 밀집해 있어, 선진적인 조직 모델의 지속적인 개발 파이프라인을 뒷받침하고 있습니다. 미국의 기술 허브에서는 AI 인재를 활용해 독성 평가 알고리즘을 정교화하고 있는 반면, 캐나다의 2023년 화장품 규제로 인해 북미(NAM) 수요는 더욱 견고해지고 있습니다.

유럽에서는 “'호라이즌' 보조금을 기반으로 한 산학협력 컨소시엄을 통해 꾸준한 성장을 이어가고 있습니다. 프랑스는 조직공학공급망 대부분을 뒷받침하고 있으며, EPISKIN사의 리옹 시설에서는 SkinEthic RHE 키트가 전 세계로 수출되고 있습니다. 피부 독성 시험 시장은 EU의 상호 승인 제도의 혜택을 받고 있어, 회원국 간에 시험 결과를 상호 활용할 수 있게 됨에 따라 중복 시험에 드는 비용이 절감되고 있습니다.

아시아태평양에서는 규제 당국이 대체 시험 기준의 통일을 추진하는 가운데, 2031년까지의 연평균 성장률(CAGR)이 6.20%로 가장 높은 성장세를 보이고 있습니다. 중국에서는 2025년 2월 규정에 따라 비동물 데이터를 활용한 성분 등록 절차가 간소화되는 한편, 2025년 5월의 종합적인 안전 규정 및 7월의 시행 일정에 따라 국내 시험소들은 역량 강화를 요구받고 있습니다. 일본에서는 OECD 시험법(TG)의 개정에 발맞추어, 2025년 말에 발효된 화학물질 관리법 개정에 대해 일반인의 의견을 수렴하고 있습니다. 능력 면에서의 제약은 여전히 지속되고 있으며, 세포 배양 독성학자 양성 프로그램이 수요를 따라가지 못하고 있어, 유럽 및 미국의 CRO와의 합작 사업에 진출할 여지가 생기고 있습니다. 그렇긴 하지만, RHE 키트의 현지 생산이 증가하고 있어 수입 의존도가 완화되고, 아시아 전역의 경피 독성 시험 시장 기반이 더욱 공고해질 전망입니다.

남미와 중동 및 아프리카은 여전히 발전 단계에 있습니다. 브라질은 ANVISA가 OECD TG 439를 준수함으로써 지역 차원의 도입을 추진하고 있으나, 규제 간의 불일치가 통일된 도입을 저해하고 있습니다. 걸프협력회의(GCC) 회원국들은 관심을 보이고 있으며, 특히 고급 화장품 수입에 대해 “"동물 실험을 실시하지 않았다" 이러한 인증이 요구되는 지역에서는 그 경향이 두드러집니다. 기술 이전 파트너십과 이동식 시험 장비는 인프라 격차를 해소하고 수익의 점진적인 증가를 촉진할 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.03According to Mordor Intelligence, the dermal toxicity testing market size is projected to be USD 2.05 billion in 2025, USD 2.16 billion in 2026, and reach USD 2.82 billion by 2031, growing at a CAGR of 5.47% from 2026 to 2031.

This report is Segmented by Test Type (In-Vitro, In-Silico, Ex-Vivo, In-Vivo), Toxicity Endpoint (Skin Irritation, Corrosion, Sensitization, Absorption, Phototoxicity), End User (Cosmetics, Pharmaceutical, Chemical, Cros, Academic), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Dermal Toxicity Testing Market Trends and Insights

Regulatory Bans on Animal Testing in Cosmetics

Multiple jurisdictions codified animal-testing prohibitions, creating a structural demand shift favoring the dermal toxicity testing market. Twelve U.S. states enforced comprehensive bans by 2024, echoing the European Union's decade-old marketing restriction. Canada's December 2023 law extended the momentum across North America. Regulatory focus now spans chemicals and pharmaceuticals; the U.S. EPA had cleared 140 alternative methods for dermal endpoints by late 2024, and the FDA's 2025 roadmap formally encourages NAMs within Investigational New Drug filings. Japan issued guidance on non-animal protocols in 2024, confirming Asia-Pacific alignment. Collectively, these actions elevate compliance risk for companies lacking NAM data and redirect testing budgets toward validated in-vitro and in silico services.

Accelerated FDA & OECD Acceptance of In-Vitro & In-Silico Assays

The FDA's April 2025 "Roadmap to Reducing Animal Testing in Preclinical Safety Studies" endorses organ-on-chip, AI-based modeling, and virtual-patient simulations, granting early-adopter firms a streamlined review pathway. OECD fast-tracked updates to Test Guidelines 497 and 496 in 2024, integrating omics-based readouts and data-sharing frameworks. Canada released a complementary draft strategy under CEPA in September 2024, targeting full transition to NAMs by 2035. Faster acceptance removes a historic bottleneck-regulatory uncertainty-and magnifies return on R&D for platform providers entrenched in the dermal toxicity testing market.

Limited Predictive Correlation of Some In-Vitro Assays with Human Outcomes

Regulators remain cautious when assay outputs diverge from clinical observations, especially for complex endpoints like dermal sensitization that involve innate and adaptive immunity. Human predictive patch-test datasets reveal variability that current RHE models struggle to reproduce. OECD requires multi-laboratory ring trials prior to guideline approval, prolonging commercialization timelines. Smaller developers face steep funding hurdles to finance these studies. Integrating omics-level analytics with 3-D tissues promises richer mechanistic insight, yet standard protocols are still being harmonized.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Bioprinted 3-D Human Skin Models

- AI-Enabled High-Content Imaging for Irritation Screens

- High Capital Cost of 3-D Tissue Culture Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In-vitro RHE systems held the largest 49.19% slice of the dermal toxicity testing market share in 2025, anchored by OECD TG 439 and TG 431 acceptance. The dermal toxicity testing market size for RHE platforms is projected to advance steadily as validation pipelines for vascularized constructs finalize. In-silico assays record the fastest 5.62% CAGR through 2031, fueled by AI libraries ingesting millions of cheminformatics records.

RHE maturity partly stems from its replicable barrier-function metrics and ease of transfer into GLP labs. Iterative improvements-such as iPSC-derived keratinocyte sourcing-reduce donor-variability risks and secure unlimited cell banks. Hybrid strategies that pair quick in-silico screens with confirmatory RHE tests compress development cycles and trim reagent costs, an attractive proposition for firms scaling global portfolios. Yet, 3-D bioprinted skin still faces throughput bottlenecks, limiting its near-term share expansion despite superior physiological relevance.

OECD endorsement of ex-vivo skin (MUG-hOSEC) solidifies niche adoption for immuno-competent assays. Incorporation of hypodermal adipose layers elevates metabolic fidelity, revealing surfactant-induced lipid disturbances undetectable in simpler tissues. Chem-informatics algorithms, in parallel, unlock predictive toxicology for new-to-market UV filters where empirical data are scarce. This dual trajectory-biological sophistication and digital simulation-positions the dermal toxicity testing market as an integrated testing ecosystem rather than a binary choice between wet and dry labs.

Complete Report Scope:

- By Test Type

- In-vitro (2-D & 3-D reconstructed human epidermis)

- In-silico / Computational

- Ex-vivo Human Skin

- In-vivo Animal

- By Toxicity Endpoint

- Skin Irritation

- Skin Corrosion

- Dermal Sensitization

- Percutaneous Absorption

- Phototoxicity & Photo-allergy

- By End User

- Cosmetics & Personal-Care Companies

- Pharmaceutical & Biotech Firms

- Chemical & Agro-chemical Manufacturers

- CROs & Independent Toxicology Labs

- Academic & Government Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America's 42.68% 2025 share reflects a mature CRO landscape, proactive FDA stances, and ample venture capital. The region also hosts the densest cluster of bioprinting start-ups, feeding a continuous pipeline of advanced tissue formats. U.S. tech hubs leverage AI talent to refine toxicity algorithms, while Canada's 2023 cosmetics ban further entrenches NAM demand.

Europe sustains robust growth through collaborative industry-academic consortia under Horizon grants. France anchors much of the tissue-engineering supply chain, with EPISKIN's Lyon facility exporting SkinEthic RHE kits worldwide. The dermal toxicity testing market benefits from the EU's mutual recognition regime, enabling test portability across member states and lowering duplicate-testing expenditures.

Asia-Pacific posts the fastest 6.20% CAGR through 2031 as regulators converge on alternative-testing norms. China's February 2025 provisions streamline ingredient registration via non-animal data, while its May 2025 comprehensive safety rules and July implementation timetables spur domestic labs to upgrade their capabilities. Japan solicits public feedback on Chemical Substances Control Law updates due by late-2025, aligning with OECD TG revisions. Capacity constraints persist; training programs for cell-culture toxicologists lag demand, creating openings for Western CRO joint ventures. Nonetheless, rising local manufacturing of RHE kits is set to moderate import dependency and deepen the dermal toxicity testing market footprint across Asia.

South America and the Middle East & Africa remain nascent. Brazil pushes regional adoption through ANVISA alignment with OECD TG 439, but fragmented regulations impede uniform adoption. Gulf Cooperation Council countries display interest, especially where luxury-cosmetic imports require cruelty-free certification. Technology transfer partnerships and mobile testing units could bridge infrastructure gaps and drive incremental revenues.

- Eurofins

- SGS

- Charles River

- LabCorp

- Intertek Group

- In-Vitro International

- MatTek Corporation

- IIVS -Institute for In-Vitro Sciences

- SenzaGen AB

- XCellR8 Ltd

- MB Research Laboratories

- BioReliance (Merck KGaA)

- Cyprotex (Evotec)

- WuXi App Tec

- Pacific BioLabs

- CellSystems Biotechnologie

- Epithelix Sarl

- SkinEthic (L'Oreal)

- CELLnTec Advanced Cell Systems

- Phenion

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Bans on Animal Testing in Cosmetics

- 4.2.2 Accelerated FDA & OECD Acceptance of In-Vitro & In-Silico Assays

- 4.2.3 Growth of Bioprinted 3-D Human Skin Models

- 4.2.4 AI-Enabled High-Content Imaging for Irritation Screens

- 4.2.5 Rising Dermatological Drug Pipeline Needs Early Dermal Safety

- 4.2.6 ESG-Driven Demand for Cruelty-Free Product Claims

- 4.3 Market Restraints

- 4.3.1 Limited Predictive Correlation of Some In-Vitro Assays with Human Outcomes

- 4.3.2 High Capital Cost of 3-D Tissue Culture Platforms

- 4.3.3 Scarcity of Skilled Cell-Culture Toxicologists in Emerging Markets

- 4.3.4 Absence of Harmonized Global Regulatory Guidelines

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Test Type

- 5.1.1 In-vitro (2-D & 3-D reconstructed human epidermis)

- 5.1.2 In-silico / Computational

- 5.1.3 Ex-vivo Human Skin

- 5.1.4 In-vivo Animal

- 5.2 By Toxicity Endpoint

- 5.2.1 Skin Irritation

- 5.2.2 Skin Corrosion

- 5.2.3 Dermal Sensitization

- 5.2.4 Percutaneous Absorption

- 5.2.5 Phototoxicity & Photo-allergy

- 5.3 By End User

- 5.3.1 Cosmetics & Personal-Care Companies

- 5.3.2 Pharmaceutical & Biotech Firms

- 5.3.3 Chemical & Agro-chemical Manufacturers

- 5.3.4 CROs & Independent Toxicology Labs

- 5.3.5 Academic & Government Research Institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Eurofins Scientific

- 6.3.2 SGS SA

- 6.3.3 Charles River Laboratories

- 6.3.4 Labcorp Drug Development (Covance)

- 6.3.5 Intertek Group

- 6.3.6 In-Vitro International

- 6.3.7 MatTek Corporation

- 6.3.8 IIVS -Institute for In-Vitro Sciences

- 6.3.9 SenzaGen AB

- 6.3.10 XCellR8 Ltd

- 6.3.11 MB Research Laboratories

- 6.3.12 BioReliance (Merck KGaA)

- 6.3.13 Cyprotex (Evotec)

- 6.3.14 WuXi AppTec

- 6.3.15 Pacific BioLabs

- 6.3.16 CellSystems Biotechnologie

- 6.3.17 Epithelix Sarl

- 6.3.18 SkinEthic (L'Oreal)

- 6.3.19 CELLnTec Advanced Cell Systems

- 6.3.20 Phenion

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment