|

시장보고서

상품코드

2072660

인도의 디스크리트 GPU 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Discrete GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

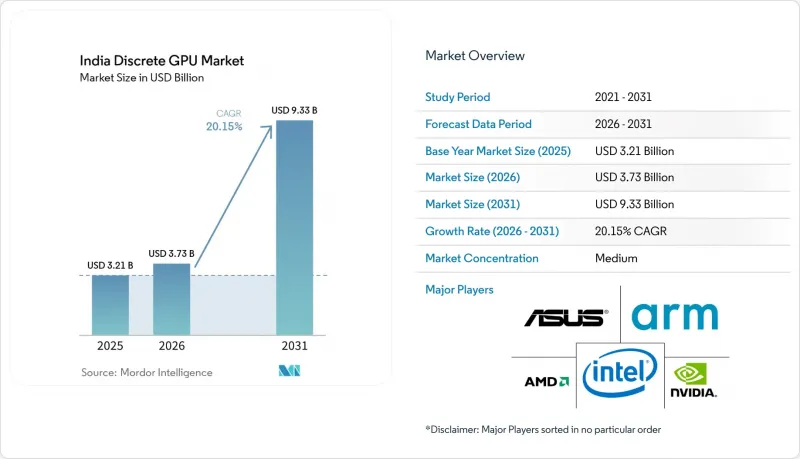

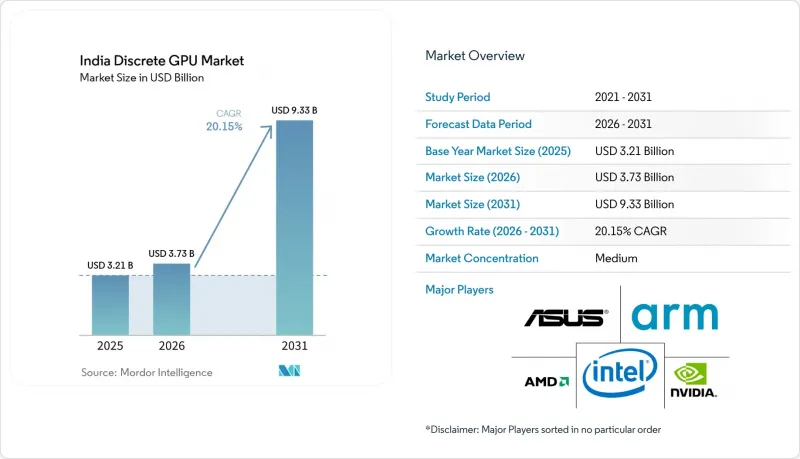

Mordor Intelligence에 의하면, 인도의 디스크리트 GPU 시장 규모는 2025년 32억 1,000만 달러로 평가되었고, 2026년에는 37억 3,000만 달러로 추정되고, 2031년까지 93억 3,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 20.15%로 성장할 전망입니다.

본 보고서는 디바이스 용도별(모바일 디바이스 및 태블릿, PC 및 워크스테이션, 서버 및 데이터센터용 가속기, 게임기 등), 메모리 유형별(GDDR 기반 GPU 및 HBM 기반 GPU), 성능 등급별(저가형 GPU, 메인스트림 GPU, 고성능 소비자용 GPU, 데이터센터/AI 가속기용 GPU)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도의 디스크리트 GPU 시장 동향 및 분석

GPU 가속이 필요한 AI 워크로드 증가

인도의 하이퍼스케일 사업자들은 파일럿 클러스터에서 멀티 기가와트 규모의 캠퍼스로 전환하고 있으며, 각 캠퍼스에는 80-150kW를 소비하는 AI 랙이 줄지어 서 있습니다. 마이크로소프트는 175억 달러를, 구글은 150억 달러를 각각 새로운 리저널 존에 배정했으며, 두 곳 모두 고밀도 GPU 패브릭을 중심으로 최적화되어 있습니다. 정부의 조달도 더 이상 주변적인 존재가 아닙니다. 'IndiaAI Mission'만으로도 3만 8,000대의 GPU를 발주했으며, 2027년까지 6만 3,000대를 목표로 하고 있어 이미 압박받고 있는 공급망에 추가적인 압박이 가해지고 있습니다. 각 사업자들은 현물 시장의 높은 가격을 피하기 위해 수년에 걸친 할당량을 확보하고 있으며, 사실상 수요를 앞당기고 있습니다. 그 결과, AI 워크로드가 기존의 가상화를 능가하는 구조적 변화가 일어나고 있으며, 이것이 인도 디스크리트 GPU 시장의 장기적인 성장 기반이 되고 있습니다.

Z세대와 밀레니얼 세대 사이에서 급성장하는 PC 게임 문화

2025년 1분기 노트북 출하량은 전년 동기 대비 8.1% 증가했으며, 게이밍 노트북이 일반용 모델을 앞질렀습니다. 각 커스텀 PC 제조업체들은 YouTube와 JioCinema를 통해 수백만 명에게 중계되는 e스포츠 대회의 호조에 힘입어, 지난 5년간 세 자릿수의 성장률을 기록했습니다. 퀄컴의 'Snapdragon 8 Elite'에는 클럭 주파수 1.1GHz의 3코어 Adreno GPU가 탑재되어, 언리얼 엔진 5의 나나이트(Nanite) 에셋을 실시간으로 처리할 수 있는 최초의 모바일용 칩이 되었습니다. 모바일과 데스크톱의 경험이 융합됨에 따라, 전용 그래픽 카드의 목표 시장은 PC에서 휴대용 기기로 확대되고 있습니다. 클라우드 게임 서비스는 하드웨어 수요를 잠식하는 것이 아니라 공존하고 있습니다. 이는 경쟁하는 기업들이 지연 시간에 민감한 게임에서는 여전히 로컬 렌더링을 선호하기 때문입니다.

지속적인 수입 관세가 BOM 비용을 상승시키고 있습니다.

HS 코드 85439000에 해당하는 그래픽 카드에는 7.5%의 관세, 10%의 사회복세, 18%의 IGST가 부과되어, 소매 가격은 입고 원가보다 15-20% 비쌉니다. 2026년 초까지 1달러당 82루피에서 85루피로 환율이 변동함에 따라, 청구액에 3-4%가 추가로 가산될 것입니다. 각 하이퍼스케일러 기업들은 OEM 업체와의 직접 거래를 통해 이러한 영향을 완화하고 있지만, 소규모 시스템 빌더에게는 그러한 협상력이 없습니다. 현지 조립이 확대되기 전까지는 관세 관련 불확실성으로 인해 일반 소비자들이 구매를 계속 주저하게 될 것이며, 이는 인도 디스크리트 GPU 시장의 연평균 성장률(CAGR)을 끌어내리는 요인이 될 것입니다.

부문별 분석

2025년, 서버 및 데이터센터용 가속기는 인도 디스크리트 GPU 시장 점유율의 38.62%를 차지했으며, 이 부문은 2031년까지 연평균 성장률(CAGR) 20.45%로 성장할 전망입니다. Yotta사가 Nvidia의 Blackwell Ultra 모듈 2만 736개를 20억 달러에 발주한 사례는 하이퍼스케일러들이 전용 AI 칩을 선호하는 경향을 여실히 보여주고 있습니다. e스포츠와 컨텐츠 제작이 활성화됨에 따라, PC 및 워크스테이션과 관련된 인도의 디스크리트 GPU 시장 규모는 견조한 추세를 보이고 있지만, 럭스케일 도입과 비교하면 성장세가 둔화되고 있습니다. 모바일 기기는 Snapdragon 8 Elite의 Adreno와 같은 통합 GPU를 활용하고 있어 카테고리 간의 경계를 모호하게 만들고 있지만, 매출에서 차지하는 비중은 미미합니다. 자동차용 ADAS와 엣지 로보틱스는 틈새 도입 분야로 부상하며 수요가 확대되는 새로운 수직 시장을 창출하고 있지만, 향후 10년 동안 데이터센터의 규모를 넘어설 일은 없을 것입니다.

전략적 계산은 명확합니다. H100급 보드 1장을 도입하는 것만으로도, 소비자용 GPU 12장 분량이 필요한 상황을 해소할 수 있어 랙 공간과 전력을 절약할 수 있습니다. 그 결과, 기업의 예산이 AI 가속기로 이동하고 있으며, 판매 대수가 중급 제품에 쏠리더라도 수익의 이동은 가속화되고 있습니다. 인도의 디스크리트 GPU 업계는 계속해서 애호가 커뮤니티를 육성하고 있지만, 공급업체들의 로드맵은 하이퍼스케일 분야의 수주가 주도하게 될 것입니다. TCS가 AMD MI455X 클러스터에서 보여주고 있듯이, 완전한 AI 패브릭을 공동 설계하는 통합 업체들은 턴키 성능의 수준을 높여가며 기존의 OEM 구성을 대체하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the india discrete GPU market size is expected to increase from USD 3.21 billion in 2025 to USD 3.73 billion in 2026 and reach USD 9.33 billion by 2031, growing at a CAGR of 20.15% over 2026-2031.

This report is Segmented by Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles, and More), Memory Type (GDDR-Based GPUs, and HBM-Based GPUs), Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and Data Center/AI Accelerator GPUs). The Market Forecasts are Provided in Terms of Value (USD).

India Discrete GPU Market Trends and Insights

Rising AI Workloads Demanding GPU Acceleration

India's hyperscale operators have moved from pilot clusters to multi-gigawatt campuses, each lined with AI racks that swallow 80-150 kilowatts. Microsoft earmarked USD 17.5 billion, and Google pledged USD 15 billion for new regional zones, both optimized around dense GPU fabrics. Government procurement is no longer peripheral; the IndiaAI Mission alone has ordered 38,000 GPUs and targets 63,000 units by 2027, tightening an already strained supply chain. Operators now lock in multi-year allocations to avoid spot-market premiums, effectively pulling forward demand. The upshot is a structural shift where AI workloads overshadow traditional virtualization, anchoring long-run growth for the India discrete GPU market.

Booming PC-Gaming Culture Among Gen-Z and Millennials

Notebook shipments climbed 8.1% year over year in Q1 2025 as gaming laptops outpaced mainstream models. Custom PC builders report triple-digit expansion over five years, driven by esports tournaments that stream to millions on YouTube and JioCinema. Qualcomm's Snapdragon 8 Elite added a three-core Adreno GPU clocked at 1.1 GHz, the first mobile silicon to handle Unreal Engine 5 Nanite assets in real time.This convergence between mobile and desktop experiences expands the addressable base for discrete graphics beyond PCs into handheld devices. Cloud gaming services coexist rather than cannibalize hardware demand because competitive players still prefer local rendering for latency-sensitive titles.

Persistent Import Tariffs Inflating BOM Costs

Graphics boards under HS 85439000 attract 7.5% customs duty, 10% social-welfare cess, and 18% IGST, pushing retail tags 15-20% above landed cost. Currency drift from INR 82 to INR 85 per USD by early 2026 adds another 3-4% to invoices. Hyperscalers mitigate the hit with direct OEM deals, but small system builders lack that leverage. Until local assembly scales, tariff uncertainty will keep mainstream buyers on the fence, shaving points off the India discrete GPU market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Government Initiatives Such as Make-in-India Boosting Local GPU Manufacturing

- Proliferation of OTT Video Creation Tools Needing Real-Time Rendering

- Power Infrastructure Deficits Limiting High-End GPU Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Servers and datacenter accelerators represented 38.62% of India discrete GPU market share in 2025, and the segment is poised for a 20.45% CAGR through 2031. Yotta's USD 2 billion order for 20,736 Nvidia Blackwell Ultra modules exemplifies hyperscaler preference for purpose-built AI silicon. The India discrete GPU market size tied to PCs and workstations remains robust as esports and content creation flourish, yet growth tails off compared with rack-scale deployments. Mobile devices leverage integrated GPUs like Snapdragon 8 Elite's Adreno, blurring category lines but contributing modest revenue slices. Automotive ADAS and edge robotics emerge as niche adopters, introducing new verticals that broaden demand but will not outrun datacenter volume this decade.

The strategic calculus is clear: deploying one H100-class board offsets the need for a dozen consumer GPUs, saving rack space and power. Consequently, enterprise budgets are tilting toward AI accelerators, accelerating the revenue shift even if unit volumes skew to mid-tier parts. The India discrete GPU industry continues to cultivate enthusiast communities, but hyperscale orders will dominate supplier roadmaps. Integrators that co-design full AI fabrics, as TCS does with AMD MI455X clusters, are raising the bar for turnkey performance and displacing traditional OEM configurations.

Complete Report Scope:

- By Device Application

- Mobile Devices and Tablets

- PCs and Workstations

- Servers and Datacenter Accelerators

- Gaming Consoles and Handhelds

- Automotive / ADAS

- Other Embedded and Edge Devices

- By Memory Type

- GDDR-based GPUs

- HBM-based GPUs

- By Performance Tier

- Low-Cost GPUs (less than 100 USD)

- Mainstream GPUs (100 USD to 400 USD)

- High-Performance Consumer GPUs (400 USD to 1,200 USD)

- Data Center / AI Accelerator GPUs (greater than 1,200 USD)

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Qualcomm Technologies Inc.

- Samsung Electronics Co., Ltd.

- Apple Inc.

- Imagination Technologies Limited

- Arm Ltd.

- MediaTek Inc.

- Huawei Technologies Co., Ltd. (HiSilicon)

- ASUS Tek Computer Inc.

- GIGABYTE Technology Co., Ltd.

- Micro-Star International Co., Ltd. (MSI)

- Colorful Technology Company Limited

- EVGA Corporation

- Sapphire Technology Limited

- Palit Microsystems Ltd.

- Galax Technology Limited

- Leadtek Research Inc.

- Zotac Technology Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming PC-gaming culture among Gen-Z and millennials

- 4.2.2 Rising AI workloads demanding GPU acceleration in Indian data centers

- 4.2.3 Government initiatives such as Make-in-India boosting local GPU manufacturing

- 4.2.4 Proliferation of OTT video creation tools needing real-time rendering

- 4.2.5 Under-reported: Web3 start-ups building on-chain graphics engines

- 4.2.6 Under-reported: Adoption of GPU-powered on-device medical imaging in semi-urban hospitals

- 4.3 Market Restraints

- 4.3.1 Persistent import tariffs inflating BOM costs

- 4.3.2 Power infrastructure deficits limiting high-end GPU deployment

- 4.3.3 Under-reported: Scarcity of PCIe Gen 5 supply chain nodes in India

- 4.3.4 Under-reported: Fragmented after-sales service network for workstation-grade GPUs

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Application

- 5.1.1 Mobile Devices and Tablets

- 5.1.2 PCs and Workstations

- 5.1.3 Servers and Datacenter Accelerators

- 5.1.4 Gaming Consoles and Handhelds

- 5.1.5 Automotive / ADAS

- 5.1.6 Other Embedded and Edge Devices

- 5.2 By Memory Type

- 5.2.1 GDDR-based GPUs

- 5.2.2 HBM-based GPUs

- 5.3 By Performance Tier

- 5.3.1 Low-Cost GPUs (less than 100 USD)

- 5.3.2 Mainstream GPUs (100 USD to 400 USD)

- 5.3.3 High-Performance Consumer GPUs (400 USD to 1,200 USD)

- 5.3.4 Data Center / AI Accelerator GPUs (greater than 1,200 USD)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies Inc.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 Apple Inc.

- 6.4.7 Imagination Technologies Limited

- 6.4.8 Arm Ltd.

- 6.4.9 MediaTek Inc.

- 6.4.10 Huawei Technologies Co., Ltd. (HiSilicon)

- 6.4.11 ASUS Tek Computer Inc.

- 6.4.12 GIGABYTE Technology Co., Ltd.

- 6.4.13 Micro-Star International Co., Ltd. (MSI)

- 6.4.14 Colorful Technology Company Limited

- 6.4.15 EVGA Corporation

- 6.4.16 Sapphire Technology Limited

- 6.4.17 Palit Microsystems Ltd.

- 6.4.18 Galax Technology Limited

- 6.4.19 Leadtek Research Inc.

- 6.4.20 Zotac Technology Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment