|

시장보고서

상품코드

2072666

중동 및 아프리카의 카톤 보드 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Middle East and Africa Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

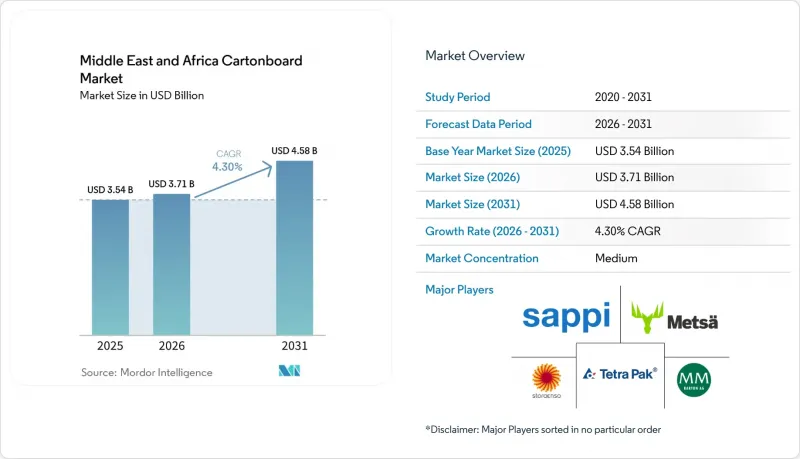

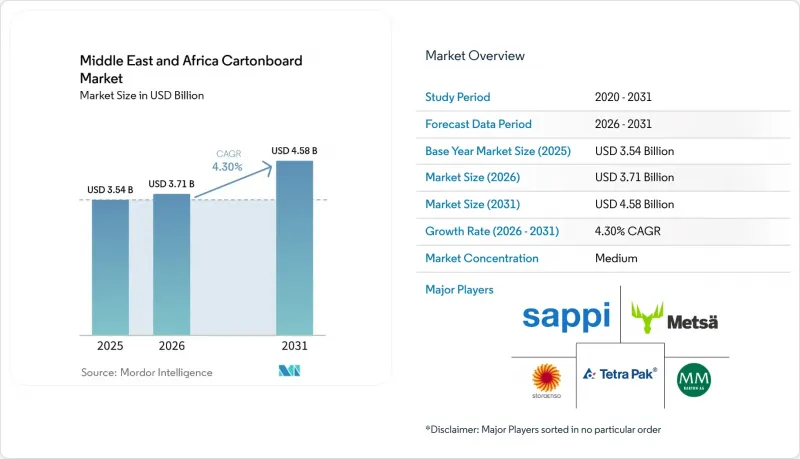

Mordor Intelligence에 의하면, 중동 및 아프리카의 카톤 보드 시장 규모는 2025년에 35억 4,000만 달러로 평가되었고, 2026년 37억 1,000만 달러로 추정되고, 2031년까지 45억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.30%를 나타낼 전망입니다.

본 보고서는 제품 등급별(고형 표백 카톤 보드, 고형 미표백 카톤 보드 등), 포장 형태별(접이식 상자, 액체 포장 등), 최종 사용자 산업별(식품, 음료 등) 및 지역별(사우디아라비아, 아랍에미리트, 튀르키예, 남아프리카공화국, 이집트, 나이지리아, 기타 중동 및 아프리카 국가)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중동 및 아프리카의 카톤 보드 시장 동향 및 분석

플라스틱 대체 및 포장 규제로 인한 호재

UAE의 2022년 장관 결정 제380호에 근거한 2단계 조치가 2026년 1월 1일부터 발효됨에 따라, 플라스틱 음료 컵 및 뚜껑, 수저, 식품 용기, 접시의 수입, 제조 및 거래가 금지되었습니다. 이 제품들은 모두 섬유계 대체재에 직접 대응하는 제품입니다. 이러한 변화로 인해 많은 외식 산업 및 테이크아웃 업종에서 카톤 보드 수요는 자발적인 지속가능성 선택이라기 보다는 규제 준수를 목적으로 한 구매로 전환되고 있습니다. 이러한 압력은 공급 기반 전체에 고르게 미치고 있는 것은 아닙니다. 왜냐하면 대규모 가공업체는 소규모 시설에 비해 추적성, 재료 조성, 생산의 일관성을 더 쉽게 입증할 수 있기 때문입니다. 이러한 차이로 인해, 긴 인증 절차를 거치지 않고도 다국적 기업의 조달 기준을 충족할 수 있는 인증을 받은 지역 가공업체의 입지가 강화되고 있습니다. 또한, 식품과 직접 접촉하는 상황에서는 보다 적절한 등급의 선정, 보다 청결한 표면, 그리고 보다 안정적인 가공 성능에 대한 요구가 높아지고 있습니다. 중동 및 아프리카의 카톤 보드 시장은 이러한 규제 변화로 인해 단기적인 수요 증가를 보이고 있습니다. 이는 몇 가지 눈에 띄는 소비자용 제품 분야에서 단순한 재료 절감 대신 포장 재설계가 진행되고 있기 때문입니다.

포장 식품 소비 증가

포장 식품 소비 증가는 여전히 이 지역에서 가장 광범위한 수요 기반을 형성하고 있습니다. 특히, 도시화의 진전, 현대적인 소매점의 확산, 그리고 바빠지는 가정생활로 인해 일상적인 구매 행동이 변화하고 있는 지역에서 이러한 현상이 두드러집니다. 가구 규모 축소와 신선식품 조리에 할애할 수 있는 시간이 줄어들면서, 1차 및 2차 포장 과정에서 카톤 보드가 사용되는 즉석 섭취가 가능하고 상온 보관이 가능하며 편의성을 중시하는 식품 형태가 인기를 얻고 있습니다. 이러한 동향이 중요한 이유는 플라스틱 규제로 인해 일부 카테고리의 브랜드 소유주들이 소재를 미세하게 조정하는 것이 아니라 포장 구조를 재설계해야 하는 상황에 직면해 있기 때문입니다. 생산자가 식품 접촉 적합성, 진열 시 외관 개선, 그리고 대규모 가공에서 신뢰할 수 있는 가공 성능을 요구할 경우, 접이식 카톤 보드 및 푸드서비스용 카톤 보드가 가장 큰 이점을 제공합니다. 튀르키예는 카톤 보드 판재의 주요 가공업체일 뿐만 아니라, GCC(걸프협력회의) 국가들로 향하는 유통 경로에서 포장 식품공급처 역할도 수행하고 있어, 가공 측면에서 유익한 측면을 제공합니다. 따라서 중동 및 아프리카의 카톤 보드 시장에서는 원자재 가격 변동과 수입품과의 경쟁이 가공업체의 수익성을 압박하고 있는 상황에서도 소비가 견조한 기조를 유지하고 있습니다.

수입 펄프 및 카톤 보드 가격 변동

중동 및 아프리카의 카톤 보드 시장은 여전히 수입 펄프, 재생 섬유 및 완제품 카톤 보드에 크게 의존하고 있으며, 이로 인해 가공업체의 이익률은 세계 가격 변동과 밀접하게 연동되어 있습니다. 유럽 및 아시아에서의 생산 능력 확대, 생산자의 환율 변동, 운송 병목 현상 등은 모두 현지 원자재 공급 기반이 제한적이기 때문에 해당 지역의 투입 비용에 즉각적으로 반영될 가능성이 있습니다. 마이어-멜른호프사는 2026년 1분기 실적 보고서에서 중동의 지정학적 긴장이 에너지, 운송, 화학제품 분야에 상당한 비용 압박을 초래하고 있다고 밝혔습니다. 또한, 이 회사의 2025년 결산 보고서에서는 중동에 위치한 두 곳의 포장 공장에서 발생할 수 있는 가동 중단 위험에 대해서도 지적된 바 있습니다. 이러한 충격이 발생하는 시기는 가격 수준과 마찬가지로 중요합니다. 왜냐하면, 카톤 보드 원가 재조정은 FMCG(일용소비재) 고객들이 포장 가격 인상을 수용하기 전에 가공업체에 먼저 영향을 미치는 경우가 많기 때문입니다. 이러한 시차로 인해 이익률이 압박받고 현금 흐름이 약화되어, 고객과의 계약이 탄탄한 대규모 가공업체에 비해 소규모 사업자는 더 큰 위험에 노출되게 됩니다. 중동 및 아프리카의 카톤 보드 시장은 이러한 상황 속에서도 성장을 이어갈 가능성이 있지만, 제품 등급, 가공업체의 규모, 수입 경로에 따라 수익의 편차가 더욱 커질 것으로 보입니다.

부문별 분석

2025년 기준으로, 접이식 카톤 보드는 시장 점유율의 38.32%를 차지했으며, 중동 및 아프리카 카톤 보드 시장에서 가장 큰 비중을 차지하고 있습니다. 이는 식품, 개인 위생 용품, 헬스케어용 카톤 보드 상자에 적합하며, 널리 인정받는 사양 기준에 부합하기 때문입니다. 이러한 강성, 인쇄 품질, 식품 접촉 적합성의 균형 덕분에, 대중 시장 및 프리미엄 소매 채널에서 진열 매력과 규정 준수를 동시에 충족해야 하는 상황에서 계속해서 핵심적인 위치를 차지하고 있습니다. 또한, 브랜드 소유주들이 위생, 원료의 순도, 일관된 가공 성능을 더욱 중요시하게 되면서, 이 등급은 버진 펄프 표면으로의 전환이라는 추세의 혜택을 받고 있습니다. 중동 및 아프리카의 카톤 보드 업계에서 이러한 점은 원자재 가격이 상승하더라도 많은 2차 포장 분야에서 접이식 카톤 보드가 상업적 표준으로 자리 잡게 되는 요인이 되고 있습니다. 유럽에서의 수입 공급은 여전히 매우 중요하며, 메차 보드사는 2026년 4월, 중동의 지정학적 긴장으로 인해 물류 비용과 특정 원자재 비용이 증가하고 있으며, 향후 몇 분기 동안 추가적인 영향이 예상된다고 밝혔습니다.

솔리드 블리치드 보드는 연평균 성장률(CAGR) 7.53%로 성장하고 있으며, 이는 제품 등급 중 가장 높은 성장률입니다. 이는 의약품 포장, 고급 화장품용 상자, 그리고 고급 푸드서비스 분야에서 밝고 청결한 느낌과 정밀한 인쇄 결과가 요구되기 때문입니다. 액체 포장용 보드는 단기 주기의 일시적 구매가 아닌, 유제품 및 주스 제조업체와의 장기적인 무균 포장 계약에 힘입어 비교적 안정적인 추세를 유지하고 있습니다. 테트라팩이 UAE의 메리하 데일리 팩토리에 투자한 것은 새로운 가공 및 충전 설비가 해당 지역의 상온 보관 가능한 유제품 및 주스용 카톤에 대한 수요를 어떻게 지속적으로 견인하고 있는지를 보여줍니다. 화이트 라이닝 칩보드 및 무표백 솔리드 보드는 여전히 비용이나 강도를 중시하는 용도로 사용되고 있지만, 현재 중동 및 아프리카의 카톤 보드 시장을 주도하고 있는 프리미엄 규격 준수 수요의 영향을 비교적 덜 받는 상황입니다. 등급 구성의 다양화는 순전히 가격에 기반한 구매에서 기능에 기반한 사양으로의 전환을 나타내며, 특히 규제 당국의 감독, 수출용 표시 기준 및 제품 안전성 요구 사항이 강화되고 있는 분야에서 두드러지게 나타납니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the middle east and africa cartonboard market size was valued at USD 3.54 billion in 2025 and is estimated to grow from USD 3.71 billion in 2026 to reach USD 4.58 billion by 2031, at a CAGR of 4.30% during the forecast period (2026-2031).

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, and More), Packaging Format (Folding Cartons, Liquid Packaging, and More), End-User Industry (Food, Beverage, and More), and Geography (Saudi Arabia, United Arab Emirates, Turkey, South Africa, Egypt, Nigeria, and Rest of Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Middle East and Africa Cartonboard Market Trends and Insights

Plastic Substitution And Packaging Regulation Tailwinds

The UAE's second phase under Ministerial Decision No. 380 of 2022 became effective on January 1, 2026, and it prohibited the import, manufacture, and trade of plastic beverage cups and lids, cutlery, food containers, and plates, all of which map directly to fiber-based alternatives. That shift turns cartonboard demand into a compliance-driven purchase rather than a voluntary sustainability option for many foodservice and take-away formats. The pressure is not falling evenly across the supply base, because larger converters can document traceability, material composition, and production consistency more easily than smaller facilities. That difference improves the position of certified regional converters that can meet multinational procurement standards without long qualification cycles. It also increases the need for better grade selection, cleaner surfaces, and more stable converting performance where direct food contact is involved. The Middle East and Africa cartonboard market receives a near-term demand lift from this regulatory shift because packaging redesign is replacing simple material reduction in several visible consumer applications.

Rising Packaged Food Consumption

Rising packaged food consumption continues to provide the broadest demand base for the region, especially where urban growth, modern retail rollout, and busier household routines are changing everyday purchase behavior. Smaller households and less time for fresh meal preparation are supporting ready-to-eat, shelf-stable, and convenience-led food formats that use cartons in primary and secondary packaging chains. This trend matters because plastic restrictions are pushing brand owners in several categories to redesign packaging structures rather than make minor material changes. Folding Boxboard and food service board benefit most where producers want food-contact acceptance, stronger shelf appearance, and dependable converting performance at scale. Turkey adds a useful processing dimension because it serves as both a large converter of cartonboard and a packaged food supplier into GCC channels. The Middle East and Africa cartonboard market therefore keeps a strong consumption floor even when input cost volatility and import competition complicate converter profitability.

Imported Pulp And Board Price Volatility

The Middle East and Africa cartonboard market remains heavily exposed to imported pulp, recycled fiber, and finished board, which keeps converter margins closely tied to global price cycles. Capacity additions in Europe and Asia, producer currency moves, and shipping bottlenecks can all reach local input costs quickly because the region has limited ability to offset them with local raw material depth. Mayr-Melnhof said in its Q1 2026 trading statement that geopolitical tensions in the Middle East were creating noticeable cost pressure on energy, transportation, and chemicals, while its 2025 results also flagged interruption risk for its 2 Middle Eastern packaging plants. The timing of these shocks matters just as much as the price level, because board cost resets often reach converters before FMCG customers accept packaging price increases. That gap compresses margins, weakens cash flow, and leaves smaller operators more exposed than scale converters with stronger customer contracts. The Middle East and Africa cartonboard market can keep growing under these conditions, but returns become more uneven across product grades, converter sizes, and import corridors.

Other drivers and restraints analyzed in the detailed report include:

- Beverage Carton Demand From Dairy And Juice

- Pharmaceutical And Healthcare Packaging Localization

- Limited Recovered Fiber And Collection Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding Boxboard held 38.32% of the market in 2025, giving it the largest role in the Middle East and Africa cartonboard market because it fits food, personal care, and healthcare cartons with a broadly accepted specification base. Its balance of stiffness, print quality, and food-contact suitability keeps it central where shelf appeal and compliance need to coexist inside mass-market and premium retail channels. The grade also benefits from the shift toward virgin-fiber surfaces, since brand owners are placing more weight on hygiene, material integrity, and consistent converting performance. In the Middle East and Africa cartonboard industry, this makes Folding Boxboard the commercial default for many secondary packs even when raw material prices move higher. Imported European supply still matters heavily, and Metsa Board said in April 2026 that geopolitical tensions in the Middle East were increasing logistics and certain raw material costs, with further effects expected in later quarters.

Solid Bleached Board is expanding at a 7.53% CAGR, the fastest among product grades, because pharmaceutical packs, premium cosmetics cartons, and higher-end foodservice applications need brightness, cleanliness, and precise print results. Liquid Packaging Board remains steadier, supported by long-term aseptic relationships with dairy and juice producers rather than short-cycle spot buying. Tetra Pak's investment at the UAE's Meliha Dairy Factory shows how new processing and filling assets continue to reinforce ambient dairy and juice carton demand in the region. White-Lined Chipboard and Solid Unbleached Board still serve cost-led and strength-led applications, but they are less exposed to the premium compliance pull that now shapes the Middle East and Africa cartonboard market. The broader grade mix shows a move away from purely price-based buying and toward function-based specification, especially where regulatory scrutiny, export presentation standards, and product safety demands are rising.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

- By Geography

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

List of Companies Covered in this Report:

- Mayr-Melnhof Karton AG

- Stora Enso Oyj

- Metsa Board Corporation

- Billerud Aktiebolag (publ)

- Holmen AB

- Sappi Limited

- Graphic Packaging International, LLC

- Tetra Pak International S.A.

- Nippon Paper Industries Co., Ltd.

- Oji Holdings Corporation

- Hotpack Holding and Investment Ltd

- Takamul Industrial Company

- United Carton Industries Company

- Arabian Packaging LLC

- Emirates Printing Press LLC

- Universal Carton Industries LLC

- Napco National

- Al Bayader International LLC

- Bony Packaging LLC

- Nampak Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Plastic Substitution and Packaging Regulation Tailwinds

- 4.3.2 Rising Packaged Food Consumption

- 4.3.3 Beverage Carton Demand From Dairy and Juice

- 4.3.4 Pharmaceutical and Healthcare Packaging Localization

- 4.3.5 Halal-Certified Food Export Expansion

- 4.3.6 Hot-Climate Preference for Shelf-Stable Cartons

- 4.4 Market Restraints

- 4.4.1 Imported Pulp and Board Price Volatility

- 4.4.2 Limited Recovered Fiber and Collection Infrastructure

- 4.4.3 Red Sea and Long-Haul Freight Disruptions

- 4.4.4 Power, Water, and Currency Stress on Converters

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

- 5.4 By Geography

- 5.4.1 Middle East

- 5.4.1.1 Saudi Arabia

- 5.4.1.2 United Arab Emirates

- 5.4.1.3 Turkey

- 5.4.1.4 Rest of Middle East

- 5.4.2 Africa

- 5.4.2.1 South Africa

- 5.4.2.2 Egypt

- 5.4.2.3 Nigeria

- 5.4.2.4 Rest of Africa

- 5.4.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Mayr-Melnhof Karton AG

- 6.4.2 Stora Enso Oyj

- 6.4.3 Metsa Board Corporation

- 6.4.4 Billerud Aktiebolag (publ)

- 6.4.5 Holmen AB

- 6.4.6 Sappi Limited

- 6.4.7 Graphic Packaging International, LLC

- 6.4.8 Tetra Pak International S.A.

- 6.4.9 Nippon Paper Industries Co., Ltd.

- 6.4.10 Oji Holdings Corporation

- 6.4.11 Hotpack Holding and Investment Ltd

- 6.4.12 Takamul Industrial Company

- 6.4.13 United Carton Industries Company

- 6.4.14 Arabian Packaging LLC

- 6.4.15 Emirates Printing Press LLC

- 6.4.16 Universal Carton Industries LLC

- 6.4.17 Napco National

- 6.4.18 Al Bayader International LLC

- 6.4.19 Bony Packaging LLC

- 6.4.20 Nampak Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment