|

시장보고서

상품코드

2072671

표백 침엽수 크라프트 펄프 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Bleached Softwood Kraft Pulp - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

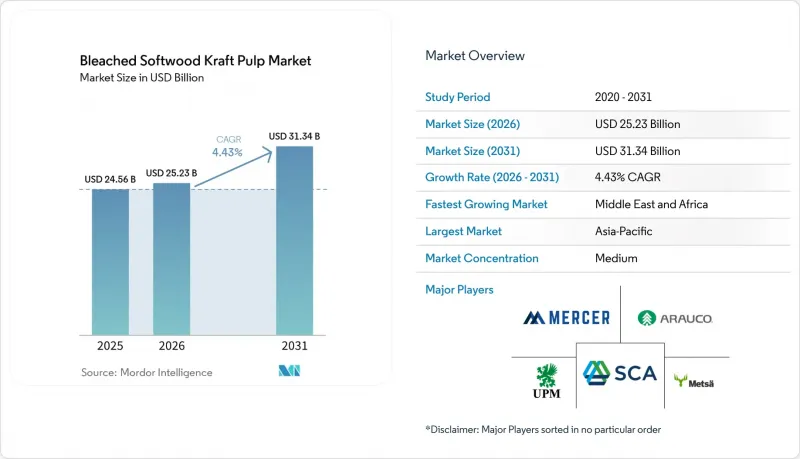

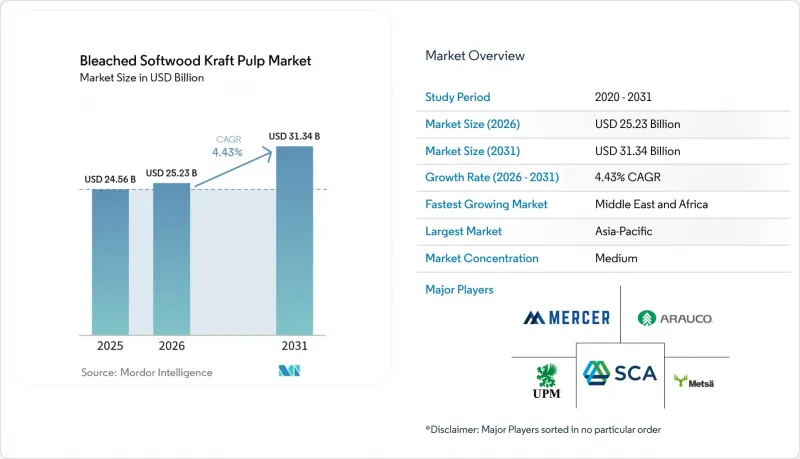

Mordor Intelligence에 의하면, 표백 침엽수 크라프트 펄프 시장 규모는 2025년 245억 6,000만 달러로 평가되었고, 2026년에는 252억 3,000만 달러로 추정되고, 2031년까지 313억 4,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 4.43%로 성장할 전망입니다.

본 보고서는 용도별(티슈, 플러프, 인쇄 및 필기용지, 특수지, 포장지), 등급별(북부 표백 연목 크라프트지(NBSK), 남부 표백 연목 크라프트지(SBSK) 등), 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 표백 침엽수 크래프트 펄프 시장 동향 및 인사이트

강도가 요구되는 용도에서 장섬유가 수행하는 대체할 수 없는 역할

표백 침엽수 크래프트 펄프 시장은 강도 성능을 타협할 수 없는 용도에서 여전히 장섬유에 의존하고 있습니다. 2.5-4.5mm 크기의 침엽수 크래프트 펄프 섬유는 인장 강도, 파열 강도 및 인열 강도에 따라 등급이 결정되며, 제지 제조업체에 필요한 결합 네트워크와 시트 연속성을 제공합니다. 비렐루드(Birelud)사의 카를스보르그(Karlsborg) NBSK 사양은 이 등급이 FDA 및 EU의 식품 접촉 요건을 충족하는 동시에, 까다로운 펄프 배합 설계에서 기대되는 강도 프로파일도 실현하고 있음을 보여줍니다. SCA사의 오스트란드 공장은 티슈, 포장용지, 특수용지용 NBSK를 공급하고 있으며, 이 회사는 이미 연간 100만 톤을 넘는 생산 능력을 바탕으로 추가 증산을 계획하고 있습니다. 이러한 제품 요건과 공급에 대한 확고한 노력이 맞물리면서, 구매자가 활엽수 펄프의 배합 비율을 높여 비용 최적화를 도모하려 해도 표백 침엽수 크라프트 펄프(BSKP) 시장 수요는 탄탄한 수준을 유지하고 있습니다.

보강층이 필요한 컨테이너 보드의 성장

표백 침엽수 크래프트 펄프 시장은 컨테이너 보드의 라이너 및 미디엄에 사용되는 보강 섬유에 의해서도 뒷받침되고 있습니다. AF&PA의 보고에 따르면, 2026년 1분기 컨테이너 보드 총 생산량은 2025년 1분기 대비 8% 감소했으나, 2026년 1분기 말 재고는 2025년 4분기 말 대비 여전히 3% 감소한 상태이며, 이는 생산 능력 감축 이후 가동 균형이 타이트해지고 있음을 시사합니다. 스마핏 웨스트록사는 2026년 4월 실적 설명회에서 2026년 1분기에는 거의 모든 섬유 등급에서 거의 매진 상태에 이르렀으며, 원가 상승에 대응하기 위해 추가적인 가격 인상을 단행했다고 밝혔습니다. 컨테이너 보드 제조 과정에서 모든 공정에 표백 침엽수 펄프가 사용되는 것은 아니지만, 에지 크러시 및 파열 강도 기준이 엄격한 프리미엄 보강층의 경우 여전히 침엽수 섬유에 의존하고 있습니다. 3월부터 2026년 2분기까지 상자 수요가 회복되고, 라이너보드 공급이 계속해서 제한되는 가운데, 표백 침엽수 크라프트 펄프(BSKP) 시장은 최저 비용의 원료가 아닌, 신뢰할 수 있는 보강 품질을 추구하는 제지 업체들로부터 지지를 얻고 있습니다.

활엽수계 대체재에 대한 구조적인 비용 부담

표백 침엽수 크라프트 펄프 시장은 표백 활엽수 크라프트 펄프에 비해 뚜렷한 비용 문제를 겪고 있습니다. 침엽수 펄프 생산에는 더 고가의 섬유 원료, 더 긴 섬유 전처리 과정, 그리고 장섬유의 무결성을 유지하기 위한 공정 조건이 필요하기 때문에 비용 구조는 유칼립투스 기반의 활엽수 펄프 공급에 비해 구조적으로 높은 수준을 유지하고 있습니다. 메차 그룹은 2025년도 연간 결산에서 유럽 및 중국의 침엽수 시장용 펄프 수요가 여전히 부진하며, 활엽수 펄프로의 부분적인 대체로 인해 최종 제품에서의 NBSK 사용량이 감소하고 있다고 밝혔습니다. 머서 인터내셔널의 'One Goal One Hundred' 프로그램은 2026년 1분기까지 목표액 1억 달러 중 4,100만 달러의 비용 절감을 달성했습니다. 이는 가격 회복이 문제를 해결할 것이라고 가정하는 것이 아니라, 각 생산 업체들이 내부 비용 절감에 얼마나 주력하고 있는지를 보여주는 것입니다. 이러한 조치가 취해지고 있음에도 불구하고, 예측 기간 동안 표백 침엽수 크라프트 펄프(BSKP) 시장이 조림 활엽수와의 핵심 목재 비용 격차를 메우기 어려울 것으로 보이며, 그로 인해 성능이 낮은 등급에서는 대체 압력이 계속될 것으로 보입니다.

부문별 분석

2025년 기준으로 티슈는 표백 침엽수 크라프트 펄프 시장 규모의 37.13%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 5.87%로 확대될 것으로 전망됩니다. 이러한 요인들이 복합적으로 작용하여, 티슈는 표백 침엽수 크라프트 펄프 업계에서 가장 규모가 크고 가장 빠르게 성장하고 있는 용도가 되었습니다. 이 부문은 성숙한 경제권에서의 안정적인 프리미엄화 추세와 동남아시아 및 남아시아에서의 1인당 보급률 가속화라는 두 가지 병행되는 수요 흐름의 혜택을 받고 있습니다. TAPPI Paper360에 따르면, 선진국 시장에서 자체 브랜드 티슈의 판매량이 전체의 40%에 육박할 가능성이 있으며, 이는 매년 티슈 제조기 2대 분량의 생산 능력에 해당하는 수요를 창출하게 될 것입니다. 성능 요건도 중요한 요소입니다. 왜냐하면 다층 티슈의 외층은 활엽수가 많이 포함된 펄프로는 달성하기 어려운 부드러움, 두께, 습윤 강도라는 목표를 충족시키기 위해 여전히 장섬유의 밀도에 의존하고 있기 때문입니다.

플라프 펄프는 성인용 요실금 용품, 유아용 기저귀, 여성용 위생용품 수요와 밀접한 관련이 있기 때문에 전략적 관점에서 볼 때 여전히 두 번째로 중요한 용도로 남아 있습니다. Stora Enso사의 2025년 자본 시장용 자료에서는 플라프 펄프를 '방어력이 있는 부문'이라고 규정하며, Skutskar 공장의 재편을 플라프 펄프 생산량 증가와 직접적으로 연결하고 있습니다. 이는 생산자들이 보다 지속 가능한 수요 분야로 적극적으로 전환하고 있음을 보여줍니다. 포장 분야의 이용 사례는 여전히 생산량 측면에서 중요한 위치를 차지하고 있지만, BSKP는 주로 다층 라이너 보드의 보강재로 사용되며 원료 배합 전체를 결정짓는 요소는 아니기 때문에 그 이용 사례는 보다 선택적인 양상을 띠고 있습니다. 캠포어의 제품 자료에서는 티슈, 포장, 필터용 등급의 보강 강도와 정제 용이성이 강조되고 있으며, 이는 제지 제조업체가 원료 비용 최소화보다 신뢰성 높은 가동성과 강도를 필요로 하는 상황에서 이 등급이 그 가치를 유지하고 있는 이유를 설명해 줍니다. 인쇄 및 필기용지 수요는 계속해서 감소하고 있는 반면, 특수지는 백색도나 성형성에 민감한 용도에서 여전히 중요한 역할을 하고 있습니다. 따라서 표백 침엽수 크래프트 펄프(BSKP) 시장의 용도 구성은 기존의 제지용에서 위생용품, 특수지 및 고성능 포장재로 점차 전환되고 있습니다.

지역별 분석

2025년, 아시아태평양은 표백 침엽수 크래프트 펄프 시장의 38.76%를 차지했으며, 최대의 지역 수요 거점이 되었습니다. 중국은 해상 운송을 통한 NBSK 거래에서 최대 수입국이자 한계 가격을 결정하는 구매자이므로, 여전히 중요한 요인으로 작용하고 있습니다. 이 지역의 티슈 부문은 고급 다층 티슈 생산에 수입 BSKP를 계속해서 활용하고 있는 반면, 판지 및 위생용품은 지역 전체에서 보다 광범위한 수요 기반을 형성하고 있습니다. 인도 및 인도네시아에서는 소득 증가와 현대적인 소매 형태의 보급에 따라 1인당 종이 소비량이 증가하고 있으며, 그 중요성이 커지고 있습니다. 일본에서는 고광택 티슈 및 특수 등급 종이에 대한 수요가 성숙기에 접어들었음에도 여전히 견조한 양상을 보이고 있으며, 이는 해당 지역 내 고품질 수입 수요를 유지하는 데 기여하고 있습니다. 또한, 아시아태평양은 대규모 국내 침엽수 자원 기반이 부족하여 지속적으로 수입에 의존하는 상태가 이어지고 있으며, 이 지역의 표백 침엽수 크래프트 펄프(BSKP) 시장은 운송 비용, 무역 흐름 및 수출국 생산자의 가동률에 대해 매우 민감한 상태를 유지하고 있습니다.

북미와 유럽은 표백 침엽수 크라프트 펄프 시장의 주요 생산 거점으로, 캐나다가 전 세계 NBSK 생산량의 대부분을 공급하고 있으며, 스웨덴과 핀란드가 두 번째 주요 생산 거점을 형성하고 있습니다. 유럽의 표백 침엽수 크래프트 펄프 소비량은 2025년에 2024년 대비 10% 감소했습니다. 이는 티슈 수요가 비교적 견조한 추세를 보인 반면, 인쇄용지와 필기용지에서는 활엽수로의 대체 압력이 높아진 것을 반영한 것입니다. EUDR(유럽 목재 규정)에 따라 유럽으로 제품을 판매하는 수출업체에는 규정 준수 및 추적성 관련 비용이 추가로 발생하고 있으며, UPM사는 모든 요건을 충족하기 위해 이행 기간 동안 규정 준수 조치를 추진하고 있다고 밝혔습니다. 또한, 브리티시컬럼비아주에서는 생산 능력이 감소하고 있는 반면, 캐나다 동부에는 전략적 투자가 유입되고 있어 북미 내 지역별 분포도 변화하고 있습니다. 캐나다 인프라 은행에 따르면, J.D. 어빙사가 세인트존에서 추진 중인 '프로젝트 넥스트젠'은 6억 6,000만 달러의 대출을 통해 추진되는 15억 달러 규모의 현대화 프로젝트로, 생산량을 70% 이상 늘리는 동시에 톤당 온실가스 배출량을 절반으로 줄이는 것을 목표로 하고 있습니다.

표백 침엽수 크래프트 펄프 시장에서 중동 및 아프리카은 2026-2031년 연평균 성장률(CAGR) 6.31%를 기록할 전망이며, 지역별로는 가장 빠른 성장세를 보일 것으로 전망됩니다. 수요는 도시화, 식품 및 소비재 포장 수요의 확대, 그리고 현지 섬유 공급량이 적은 국가들의 티슈 생산 능력 확대에 힘입어 증가하고 있습니다. 사우디아라비아의 '비전 2030' 프로그램은 하류 포장 분야에 대한 투자를 촉진하고 있는 반면, 이집트와 나이지리아에서는 확대되는 도시 중산층에 의해 티슈 수요가 형성되고 있습니다. 사하라 이남 아프리카는 소비 기반이 매우 낮은 수준에서 시작되었기 때문에 현지 펄프 산업의 규모가 그리 크지 않더라도 이 지역에는 장기적인 성장 여지가 있습니다. 남미는 BSKP 수요 거점이라기보다는 생산 및 물류 지역으로서의 중요성이 여전히 높지만, 브라질과 아르헨티나에서의 포장 수요 증가에 힘입어 여전히 증가분공급량을 흡수하고 있습니다. 브라질에서 아라우코사의 펄프 수출을 위한 광범위한 인프라 구축은 활엽수 펄프를 중심으로 진행되고 있지만, 그럼에도 불구하고 지역 전체의 물류 환경을 개선함으로써 남미 수출망 전반에 걸친 표백 침엽수 크라프트 펄프(BSKP) 시장의 무역 효율성을 간접적으로 뒷받침하는 결과로 이어집니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 전망 및 시나리오 분석

AJY 26.07.03According to Mordor Intelligence, the bleached softwood kraft pulp market size is expected to increase from USD 24.56 billion in 2025 to USD 25.23 billion in 2026 and reach USD 31.34 billion by 2031, growing at a CAGR of 4.43% over 2026-2031.

This report is Segmented by Application (Tissue, Fluff, Printing and Writing, Specialty Paper, and Packaging), Grade (Northern Bleached Softwood Kraft (NBSK), Southern Bleached Softwood Kraft (SBSK), and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Bleached Softwood Kraft Pulp Market Trends and Insights

Irreplaceable Role Of Long Fiber In Strength Applications

The bleached softwood kraft pulp market continues to depend on long fiber where strength performance cannot be compromised. Softwood kraft pulp fibers at 2.5-4.5 millimeters give paper makers the bonding network and sheet continuity needed in grades that rely on tensile, burst, and tear properties. Billerud's Karlsborg NBSK specification shows that the grade meets FDA and EU food contact requirements while also delivering the strength profile expected in demanding furnish designs. SCA's Ostrand mill is supplying NBSK into tissue, packaging paper, and specialty paper, and the company is still planning capacity growth from a base already above 1 million tonnes per year. That combination of product requirements and supply commitment means the bleached softwood kraft pulp (BSKP) market keeps a resilient demand floor even when buyers try to optimize costs with more hardwood content.

Growth In Containerboard Requiring Reinforcement Layers

The bleached softwood kraft pulp market is also supported by the use of reinforcement fibers in containerboard liner and medium. AF&PA reported that total containerboard production in Q1 2026 fell 8% from Q1 2025, yet inventories at the end of Q1 2026 were still 3% lower than at the end of Q4 2025, which points to tighter operating balance after capacity reductions. Smurfit Westrock stated in its April 2026 earnings call that it had reached near sold-out status for nearly every fiber grade in Q1 2026 and had launched another round of price increases to address higher costs. Containerboard does not use bleached softwood pulp everywhere, but premium reinforcement layers still depend on softwood fiber where edge crush and burst targets are strict. As box demand improves from March through Q2 2026 and available linerboard supply remains disciplined, the bleached softwood kraft pulp (BSKP) market gains support from mills that need dependable reinforcement quality rather than the lowest-cost furnish.

Structurally Higher Cost Vs Hardwood Alternatives

The bleached softwood kraft pulp market faces a clear cost challenge against bleached hardwood kraft pulp. Softwood pulp production requires more expensive fiber input, longer fiber preparation, and process conditions that preserve long-fiber integrity, so the cost base remains structurally above eucalyptus-based hardwood supply. Metsa Group stated in its full-year 2025 results that softwood market pulp demand remained muted in Europe and China and that partial replacement with hardwood pulp was reducing NBSK volumes in end products. Mercer International's One Goal One Hundred program had reached USD 41 million in savings through Q1 2026 against a USD 100 million target, which shows how strongly producers are focused on internal cost reduction rather than assuming price recovery will solve the issue. Even with that response, the bleached softwood kraft pulp (BSKP) market is unlikely to close the core wood cost gap with plantation hardwood during the forecast period, so substitution pressure will continue in lower-performance grades.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce-Induced Packaging Stress Requirements

- Limited Substitution Possibility In High-Performance Grades

- Limited Fiber Availability Due To Long Growth Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tissue accounted for 37.13% share of the bleached softwood kraft pulp market size in 2025, and it is also projected to expand at a 5.87% CAGR through 2031. That combination makes tissue the largest and fastest-growing application in the bleached softwood kraft pulp industry. The segment benefits from two parallel demand streams, stable premiumization in mature economies and faster per-capita adoption in Southeast Asia and South Asia. TAPPI Paper360 said private-label tissue could approach 40% of volume in developed markets, which is equal to the demand created by two tissue machine capacities each year. The performance requirement also matters, because multi-ply tissue outer plies still depend on long-fiber density to meet softness, caliper, and wet strength targets that hardwood-heavy furnishes struggle to achieve.

Fluff pulp remains the second most important application from a strategic standpoint because it is tied to adult incontinence, baby diaper, and feminine hygiene demand. Stora Enso's 2025 capital markets material described fluff pulp as a defensible segment and linked its Skutskar restructuring directly to higher fluff output, which shows that producers are actively shifting toward more durable demand pockets. Packaging stays volume significant, but the use case is more selective because BSKP mainly reinforces multi-ply linerboard rather than setting the full furnish mix. Canfor's product material highlights reinforcement strength and ease of refining for tissue, packaging, and filter grades, which explains why the grade retains value where paper makers need dependable runnability and strength rather than the lowest possible furnish cost. Printing and writing paper continues to decline, while specialty paper keeps a premium role for brightness and formation-sensitive uses, so the application mix in the bleached softwood kraft pulp (BSKP) market is gradually shifting toward hygiene, specialty, and performance packaging rather than legacy paper grades.

Complete Report Scope:

- By Application

- Tissue

- Fluff

- Printing and Writing

- Specialty Paper

- Packaging

- By Grade

- Northern Bleached Softwood Kraft (NBSK)

- Southern Bleached Softwood Kraft (SBSK)

- Other Grades

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Nordics

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Indonesia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Africa

- North America

Geography Analysis

Asia-Pacific held 38.76% of the bleached softwood kraft pulp market share in 2025, making it the largest regional demand center. China remains the key factor because it is the largest importer and the marginal price-setting buyer in the seaborne NBSK trade. The region's tissue sector continues to draw imported BSKP into premium multi-ply tissue production, while paperboard and hygiene products create a broader demand base across the region. India and Indonesia are moving up in importance as rising incomes and modern retail formats increase per-capita paper consumption. Japan remains a mature but demanding outlet for high-brightness tissue and specialty grades, which helps preserve premium import demand in the region. Asia-Pacific also stays permanently import dependent because it lacks a large domestic boreal softwood resource base, so the bleached softwood kraft pulp (BSKP) market in the region remains highly sensitive to shipping costs, trade flows, and producer operating rates in exporting countries.

North America and Europe form the main production center of the bleached softwood kraft pulp market, with Canada supplying a major share of global NBSK output and Sweden and Finland forming the second major producer bloc. Europe's consumption of bleached softwood kraft pulp fell by 10% in 2025 from 2024, reflecting hardwood substitution pressure in printing and writing papers even as tissue demand remained more resilient. The EUDR is adding compliance and traceability costs for exporters selling into Europe, and UPM said it was carrying out compliance work during the transition period to meet the full requirements. Production geography inside North America is also shifting because British Columbia has been losing capacity while eastern Canada is receiving strategic investment. Canada Infrastructure Bank said J.D. Irving's Project NextGen in Saint John is a USD 1.5 billion modernization supported by a USD 660 million loan and is intended to lift production by more than 70% while cutting greenhouse gas emissions per tonne by half.

The Middle East and Africa is projected to record the fastest regional growth at a 6.31% CAGR from 2026 to 2031 in the bleached softwood kraft pulp market. Demand is being supported by urbanization, broader food and consumer goods packaging needs, and tissue capacity growth in countries with little local fiber supply. Saudi Arabia's Vision 2030 program is encouraging downstream packaging investment, while Egypt and Nigeria are building tissue demand from a growing urban middle class. Sub-Saharan Africa starts from a very low consumption base, which gives the region a long runway for growth even without a large local pulp industry. South America remains more important as a production and logistics region than as a demand center for BSKP, but growing packaging demand in Brazil and Argentina is still absorbing incremental volumes. Arauco's broader infrastructure buildout for pulp exports in Brazil is centered on hardwood pulp, yet it still improves regional logistics that can indirectly support trade efficiency for the bleached softwood kraft pulp (BSKP) market across the South American export chain.

- Metsa Group

- UPM-Kymmene Corporation

- Celulosa Arauco y Constitucion S.A.

- Svenska Cellulosa Aktiebolaget SCA (publ)

- Mercer International Inc.

- Global Cellulose Fibers

- West Fraser Timber Co.

- Canfor Corporation

- Stora Enso Oyj

- J.D. Irving, Limited

- Billerud AB

- Smurfit Westrock Company

- Domtar Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

- 3.1 Market Snapshot

- 3.2 Demand Anchors and End-Use Mix

- 3.3 Pricing Outlook and Margin Trends

- 3.4 Strategic Implications

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.1.1 Supply-Side Dynamics

- 4.1.2 Geographic Concentration (Canada, Nordics, USA)

- 4.1.3 Long Forestry Rotation Cycles

- 4.1.4 Limited Plantation Expansion Potential

- 4.1.5 Supply Elasticity Constraints

- 4.1.6 Exposure to Supply Shocks: Wildfires, Pests, and Geopolitical Disruptions

- 4.1.7 Impact of Logging Policies and Environmental Restrictions

- 4.2 Production and Capacity Analysis

- 4.2.1 Installed Capacity by Region

- 4.2.2 Capacity Utilization Trends

- 4.2.3 Aging Asset Base vs Modernization

- 4.2.4 Limited Greenfield Capacity Additions

- 4.2.5 Downtime and Curtailments

- 4.2.6 Integration with Sawmill Industry (Chip Dependency)

- 4.3 Raw Material and Fiber Economics

- 4.3.1 Softwood Species (Pine, Spruce, Fir)

- 4.3.2 Wood Cost Structure (Higher vs Hardwood)

- 4.3.3 Dependency on Sawmill Residues (Chips Supply)

- 4.3.4 Regional Fiber Cost Competitiveness

- 4.3.5 Forestry Sustainability and Certification

- 4.4 Trade Flow and Market Linkages

- 4.4.1 Export-Oriented Supply Structure

- 4.4.2 Key Trade Routes (Canada/Nordics ? China/Europe)

- 4.4.3 China as Marginal Buyer and Price Influencer

- 4.4.4 Trade Disruptions and Geopolitical Exposure

- 4.5 Pricing Analysis

- 4.5.1 Benchmark Grade: NBSK Pricing

- 4.5.2 Historical Price Cycles

- 4.5.3 Structural Premium vs Hardwood Pulp

- 4.5.4 Key Price Drivers: Supply Tightness, Reinforcement Demand, and Energy and Logistics Costs

- 4.5.5 Forward Price Outlook

- 4.6 Cost Structure and Cost Curve

- 4.6.1 Cost Breakdown (Wood, Energy, Chemicals, Labor)

- 4.6.2 Global Cost Curve Positioning

- 4.6.3 Energy Cost Sensitivity

- 4.7 Market Dynamics

- 4.7.1 Market Drivers

- 4.7.1.1 Irreplaceable Role of Long Fiber in Strength Applications

- 4.7.1.2 Growth in Containerboard Requiring Reinforcement Layers

- 4.7.1.3 E-commerce-Induced Packaging Stress Requirements (Higher Strength)

- 4.7.1.4 Limited Substitution Possibility in High-Performance Grades

- 4.7.1.5 Expansion of Industrial Paper (Sack Kraft, Heavy-Duty Bags)

- 4.7.1.6 Improved Quality Standards in Packaging & Hygiene Products

- 4.7.2 Market Restraints

- 4.7.2.1 Structurally Higher Cost vs Hardwood Alternatives

- 4.7.2.2 Limited Fiber Availability Due to Long Growth Cycles

- 4.7.2.3 Dependence on Sawmill Output for Wood Chip Supply

- 4.7.2.4 Exposure to Forestry Disruptions (Fires, Pests, Climate Impact)

- 4.7.1 Market Drivers

- 4.8 Technology and Process Landscape

- 4.8.1 Kraft Pulping (Softwood Processing)

- 4.8.2 Fiber Strength Optimization

- 4.8.3 Bleaching Technologies (ECF)

- 4.8.4 Energy Recovery Systems

- 4.8.5 Automation and Digital Mills

- 4.9 ESG and Sustainability Analysis

- 4.9.1 Forestry Management Practices

- 4.9.2 Carbon Footprint

- 4.9.3 Biodiversity Considerations

- 4.9.4 Water and Emissions

- 4.9.5 Certification Landscape

5 MARKET SIZE AND GROWTH FORECAST

- 5.1 By Application

- 5.1.1 Tissue

- 5.1.2 Fluff

- 5.1.3 Printing and Writing

- 5.1.4 Specialty Paper

- 5.1.5 Packaging

- 5.2 By Grade

- 5.2.1 Northern Bleached Softwood Kraft (NBSK)

- 5.2.2 Southern Bleached Softwood Kraft (SBSK)

- 5.2.3 Other Grades

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Russia

- 5.3.3.5 Nordics

- 5.3.3.6 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Indonesia

- 5.3.4.5 Rest of Asia-Pacific

- 5.3.5 Middle East and Africa

- 5.3.5.1 Middle East

- 5.3.5.2 Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Metsa Group

- 6.4.2 UPM-Kymmene Corporation

- 6.4.3 Celulosa Arauco y Constitucion S.A.

- 6.4.4 Svenska Cellulosa Aktiebolaget SCA (publ)

- 6.4.5 Mercer International Inc.

- 6.4.6 Global Cellulose Fibers

- 6.4.7 West Fraser Timber Co.

- 6.4.8 Canfor Corporation

- 6.4.9 Stora Enso Oyj

- 6.4.10 J.D. Irving, Limited

- 6.4.11 Billerud AB

- 6.4.12 Smurfit Westrock Company

- 6.4.13 Domtar Corporation

7 FUTURE OUTLOOK AND SCENARIO ANALYSIS

- 7.1 Strategic Outlook and Future Dynamics

- 7.2 Supply Constraints vs Demand Growth

- 7.3 Sustainability of Price Premium

- 7.4 Investment Outlook

- 7.5 Risk Assessment

- 7.6 Future Role in Global Fiber Mix