|

시장보고서

상품코드

2072686

무표백 크라프트 펄프 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Unbleached Kraft Pulp - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

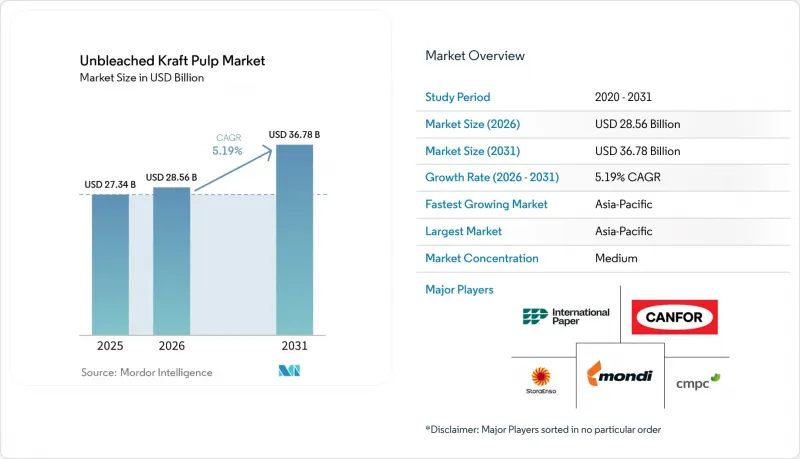

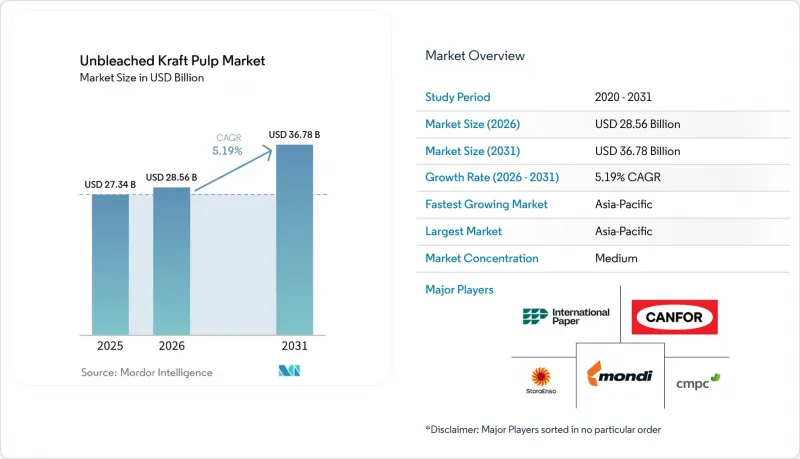

Mordor Intelligence에 의하면, 무표백 크라프트 펄프 시장 규모는 2025년 273억 4,000만 달러로 평가되었고, 2026년에는 285억 6,000만 달러로 추정되고, 2026-2031년 CAGR 5.19%로 성장을 지속할 전망이며, 2031년에는 367억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 등급별(침엽수, 활엽수, 혼합 섬유), 용도별(골판지 원지, 크라프트지, 특수지 등), 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 무표백 크라프트 펄프 시장 동향 및 인사이트

전자상거래에 힘입어 확대되는 골판지 포장 수요

전자상거래 물류는 여전히 무표백 크라프트 펄프 시장에 있어 가장 명확한 단기 수요 지표로 남아 있습니다. 이는 출하되는 각 단위마다 매장 내 보충 방식보다 더 많은 골판지 상자로 보호해야 하기 때문입니다. 무표백 크라프트 펄프(UKP) 시장은 미국 컨테이너보드 업계의 견조한 가동 상황의 혜택을 지속적으로 누리고 있으며, 해당 업계 전반에 걸쳐 생산 능력이 축소된 이후에도 각 제지 공장은 가동률을 높은 수준으로 유지해 왔습니다. AF&PA의 보고에 따르면, 2025년 컨테이너 보드의 가동률은 91.9%를 유지했습니다. 이는 설비 용량이 5.1% 감소했음에도 불구하고 달성된 것으로, 최종 수요가 구조적인 생산 능력 감축분을 상쇄했음을 보여줍니다. 해당 조사에 따르면, 2025년에는 컨테이너 보드가 미국의 종이 및 판지 총 생산 능력의 50% 이상을 차지할 것으로 나타나, 포장 시스템에서 그 핵심적인 역할이 재확인되었습니다. 이는 특히 제지 공장이 크라프트 라이너보드나 골판지 원지 제조에 신뢰할 수 있는 원료를 필요로 하는 경우, 버진 고강도 섬유의 안정적인 판로를 뒷받침하는 것입니다. 그 결과, UKP 시장은 골판지 포장 수요와 계속해서 밀접하게 연동되고 있으며, 전자상거래로 인한 출하량 증가가 소비량을 견고하게 뒷받침하고 있습니다.

지속 가능한 미표백 포장재로 전환

표백되지 않은 크라프트 펄프 시장 역시 재활용이 용이하고, 점점 더 엄격해지는 지속가능성 규제로 인해 사양 결정이 간편한 포장 형태로의 전환에 힘입어 혜택을 보고 있습니다. 2025년 2월에 발효된 규정(EU) 2025/40은 2030년까지 EU 시장에 출시되는 모든 포장이 재활용 가능해야 한다는 목표를 제시하고 있으며, 이 규정은 2026년 8월부터 적용됩니다. 이러한 추세는 단일 소재 및 섬유 기반 포장 구조를 촉진하고 있으며, 운송 및 고하중 용도에서 코팅 및 표백 처리되지 않은 종이에 대한 수요를 높이고 있습니다. 독일에서는 2025년 포장용지 생산량이 1,250만 톤에 달했고, 전체 제지 생산량의 67%를 차지했으며, 2024년 대비 1.8% 증가하는 등 뚜렷한 수요 증가 조짐이 나타났습니다. 또한, 무표백 크라프트 펄프(UKP) 시장은 포장 사양에 적합한 섬유 옵션을 평가할 때 조달 팀이 공정 화학 물질 및 배출 프로파일을 더욱 중시하게 된 점에서도 혜택을 보고 있습니다. 이에 따라, 가혹한 사용 조건에서도 기계적 성능을 저하시키지 않으면서 더 강력한 환경적 입지를 확보하고자 하는 프로젝트에서 미표백 등급이 우위를 점하고 있습니다.

재생 섬유(OCC 기반 생산) 부문에서의 치열한 경쟁

무표백 크라프트 펄프 시장은 최대 강도보다 원가 관리가 더 중요시되는 골판지 용도 분야에서 재생 섬유로부터 가장 직접적인 경쟁 압박을 받고 있습니다. 대형 포장 그룹은 버진 펄프와 재생 펄프를 결합한 시스템을 지속적으로 구축하고 있으며, 이로 인해 독립계 시장 펄프 판매업체가 확보할 수 있는 시장 점유율이 줄어들고 있습니다. 스마핏 웨스트록사는 전 사업장에서 연간 1,300만 톤의 재생 섬유를 소비하고 있다고 보고하고 있으며, 이를 통해 주요 생산업체들이 혼합 섬유 전략을 어느 정도 규모로 전개하고 있는지 엿볼 수 있습니다. 인터내셔널 페이퍼(International Paper)도 2026년 4월 NORPAC 인수를 합의했으며, 골판지 및 재생 경량 골판지의 생산 능력을 확대함으로써 시스템의 유연성을 높이고 있습니다. 이는 영국 시장(UKP)에 있어 중요한 의미를 지닙니다. 왜냐하면 통합형 재생 펄프 생산 능력이 증가할 때마다, 가격에 민감한 등급의 원료에서 버진 브라운 파이버에 대한 상업적 수요가 감소할 가능성이 있기 때문입니다. 이러한 억제 효과는 북미와 유럽에서 가장 두드러지는데, 이는 해당 지역에 성숙한 회수 시스템과 통합형 포장 그룹이 존재하며, 경제 상황에 따라 원료 구성을 유연하게 변경할 수 있는 능력이 뛰어나기 때문입니다.

부문별 분석

2025년, 등급별 세계 수요의 57.23%를 침엽수가 차지했으며, 라이너보드 및 고강도 용지 용도에 이르는 무표백 크라프트 펄프 시장의 중심적인 위치를 유지했습니다. 이 부문의 경쟁력은 스프루스, 소나무, 전나무 원료가 지닌 장섬유의 장점을 반영한 것으로, 이는 까다로운 포장 용도에서 인장 강도와 파열 강도를 확보하는 데 여전히 필수적입니다. 또한, 유럽과 북미의 바이어들은 여전히 인증을 받은 조달을 중요하게 여기고 있으며, FSC 및 PEFC 체계가 침엽수 펄프 조달 기준을 형성하고 있습니다. 인증과 강도 성능이 고객의 사양에서 시너지 효과를 발휘하기 때문에 이는 무표백 크라프트 펄프(UKP) 시장의 등급 안정성을 뒷받침하고 있습니다. 칠레의 미표백 라디에이터 소나무 펄프 생산량은 2022년 50만 3,000톤에서 2024년에는 32만 6,200톤으로 감소했습니다. 이는 공급업체의 엄격한 제품 포트폴리오 관리가 수출 경로에서 침엽수 공급량을 부족하게 만들 가능성도 있음을 시사합니다. 이러한 공급 조정을 통해, 제지 공장이 강도 기준을 타협할 수 없는 용도에서 침엽수 원료의 핵심적인 역할이 더욱 강화되었습니다.

활엽수는 연평균 성장률(CAGR) 5.73%로 확대될 것으로 예측되며, 2031년까지의 부문별 무표백 크라프트 펄프(UKP) 시장 규모에서 가장 빠르게 성장할 등급이 될 전망입니다. 이러한 성장은 아시아 제지 공장에서 유칼립투스계 원료의 사용 확대에 힘입은 것입니다. 해당 지역에서는 섬유의 최대 강도보다 비용 대비 성능의 균형이 더 중요하게 여겨지는 경우가 많기 때문입니다. 브라질은 2025년에 국내 펄프 생산량이 2,940만 톤에 달했고, 수출량이 2024년 대비 11.6% 증가한 2,070만 톤으로 상승함에 따라, 계속해서 주요한 구조적 촉진요인으로 작용하고 있습니다. 또한, 동남아시아와 인도의 제지 공장에서는 투입 비용과 판지의 성능을 최적화하기 위해 활엽수와 침엽수를 혼합하고 있기 때문에 무표백 크라프트 펄프 업계에서도 혼합 섬유 등급의 상업적 가치가 높아지고 있습니다. 이로 인해 등급 간 경쟁이 치열해지고 있지만, 무표백 크라프트 펄프 시장에서 강도가 중요한 사양의 경우 여전히 침엽수가 기준으로 여겨지고 있다는 사실에는 변함이 없습니다.

지역별 분석

아시아태평양은 2025년 무표백 크라프트 펄프 시장 점유율의 39.45%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 5.92%로 확대될 것으로 전망됩니다. 이로써 해당 지역은 가장 규모가 크고 가장 빠르게 성장하는 지역 부문으로서의 위상을 유지하게 될 것입니다. 중국은 세계 최대의 판지 생산국이며, 품질에 민감한 골판지 포장재 생산을 위해 계속해서 버진 펄프 등급을 필요로 하고 있기 때문에 여전히 이 지역의 주요 수요 거점으로 남아 있습니다. 인도는 조직화된 소매업의 확대, 의약품 포장 수출, 그리고 전자상거래 주문 처리 활동 증가에 힘입어, 이 지역 내에서 수요가 가장 빠르게 증가하는 국가가 되었습니다. 일본과 한국은 특히 산업용 및 전자 관련 포장 분야에서 기술적으로 고도의 특수 용지 용도를 통해 무표백 크라프트 펄프 시장을 지속적으로 뒷받침하고 있습니다. UPM은 2026년 1분기 CEO 프레젠테이션에서 유럽과 북미 시장 상황이 약세를 보이고 있음에도 불구하고 아시아의 특수지 시장은 안정세를 유지하고 있다고 밝혔습니다.

2025년과 2026년, 유럽의 무표백 크라프트 펄프 시장에서는 규제 주도형 수요 동향이 더욱 두드러지게 나타났습니다. 규정(EU) 2025/40 및 2026년 8월의 적용 개시 시기에 따라, 포장재 구매자들은 재활용 가능한 섬유 기반 제품으로의 전환을 앞당길 수밖에 없게 되었습니다. 독일의 포장용지 생산량은 2025년에 1,250만 톤에 달하고, 국내 종이 생산량의 67%를 차지했습니다. 이는 해당 국가에서 포장용지가 종이 수요를 얼마나 깊이 좌우하게 되었는지를 보여줍니다. 비렐루드사는 고급 포장 자재 사업에 주력하는 일환으로, 2026년 1분기 스칼브라카 공장에서의 작업을 포함하여 시스템 전반의 생산 능력 향상을 지속적으로 추진했습니다. 몬디사 역시 루조무베로크의 바이오매스 발전 프로젝트를 통해 장기적인 인프라 구축을 추진하고 있으며, 이를 통해 통합 공장의 에너지 자급률이 75%에서 90%로 상승할 것으로 예측됩니다.

북미는 대규모 통합형 컨테이너보드 생산 거점과 포장 자산에 대한 지속적인 투자를 바탕으로, 무표백 크라프트 펄프 시장의 주요 소비 및 생산 거점으로서의 위상을 유지해 왔습니다. 2025년 미국의 포장 용지 생산량은 1.7% 증가한 반면, 컨테이너보드 가동률은 91.9%를 유지하여, 수요가 생산 능력의 감소에 잘 적응하고 있음을 보여주었습니다. 남미는 계속해서 주로 무표백 크라프트 펄프 시장공급 지역으로서의 역할을 수행하고 있으며, 아라우코사의 스크리우 프로젝트는 2025년 4분기까지 물리적 진척률이 42.6%에 달했고, 2027년 하반기 가동 개시를 향해 예정대로 진행되고 있습니다. CMPC의 나투레자 프로젝트 역시 향후 주요 생산 능력 확충 사업으로 자리매김하고 있으며, 연간 최대 250만 톤의 생산 계획에 더해 전용 수출 터미널 전략을 통해 2030년까지 세계 무역 흐름에 영향을 미칠 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 전략적 전망 및 향후 동향

AJY 26.07.03According to Mordor Intelligence, the unbleached kraft pulp market size is expected to grow from USD 27.34 billion in 2025 to USD 28.56 billion in 2026 and is forecast to reach USD 36.78 billion by 2031 at 5.19% CAGR over 2026-2031.

This report is Segmented by Grade (Softwood, Hardwood, and Mixed Fiber), Application (Containerboard, Kraft Paper, Specialty Paper, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Unbleached Kraft Pulp Market Trends and Insights

Growth In Corrugated Packaging Demand Driven By E-Commerce

E-commerce logistics remained the clearest near-term demand signal for the unbleached kraft pulp market because each shipped unit typically requires more corrugated protection than store-based replenishment formats. The unbleached kraft pulp (UKP) market continued to benefit from strong operating conditions in U.S. containerboard, where mills kept utilization high even after capacity reductions across the sector. AF&PA reported that containerboard operating rates held at 91.9% in 2025, even as installed capacity declined by 5.1%, which showed that end demand absorbed the structural footprint cuts. The same survey showed that containerboard represented more than 50% of total U.S. paper and paperboard capacity in 2025, reinforcing its central role in the packaging system. This supports a stable outlet for virgin strength fiber, especially where mills need dependable furnish for kraft linerboard and corrugating medium. As a result, the UKP market continues to track corrugated packaging demand closely, with e-commerce shipment growth providing a durable floor for consumption.

Shift Toward Sustainable, Unbleached Packaging Materials

The unbleached kraft pulp market is also benefiting from the shift toward packaging formats that are easier to recycle and simpler to specify under tightening sustainability rules. Regulation (EU) 2025/40 entered into force in February 2025 and sets a path under which all packaging placed on the EU market must be recyclable by 2030, with the regulation applying from August 2026. This direction favors mono-material and fiber-based packaging structures, which has increased the appeal of uncoated and unbleached paper formats in transport and heavy-duty uses. Germany provided a clear demand signal in 2025, when packaging paper output reached 12.5 million tonnes and represented 67% of total paper production, up 1.8% from 2024. The unbleached kraft pulp (UKP) market also benefits from procurement teams placing more weight on process chemistry and discharge profiles when evaluating fiber options for packaging specifications. That gives unbleached grades an advantage in programs that seek stronger environmental positioning without giving up mechanical performance in demanding applications.

Strong Competition From Recycled Fiber (OCC-Based Production)

The unbleached kraft pulp market faces its most direct competitive pressure from recycled fiber in containerboard applications where cost discipline matters more than peak strength. Large packaging groups continue to build systems that combine virgin and recycled furnish, which reduces the addressable share available to independent market pulp sellers. Smurfit Westrock reported annual recycled fiber consumption of 13 million tonnes across its operating footprint, showing the scale at which major producers are managing mixed fiber strategies. International Paper also agreed in April 2026 to acquire NORPAC, adding containerboard and recycled lightweight containerboard capability that improves system flexibility. This matters for the UKP market because each increase in integrated recycled capacity can reduce merchant demand for virgin brown fiber in cost-sensitive grades. The restraint is strongest in North America and Europe, where mature collection systems and integrated packaging groups have greater ability to shift furnish according to economics.

Other drivers and restraints analyzed in the detailed report include:

- Plastic Substitution In Retail And Transport Packaging

- Growth In Heavy-Duty Packaging

- Limited Use In High-Quality Applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Softwood held 57.23% of global demand by grade in 2025, which kept it at the center of the unbleached kraft pulp market across linerboard and heavy-duty paper uses. The segment's lead reflects the long-fiber advantage of spruce, pine, and fir furnish, which remains essential for tensile and burst strength in demanding packaging applications. Buyers in Europe and North America also continue to place weight on certified sourcing, with FSC and PEFC frameworks shaping procurement eligibility for softwood supply. This supports grade stability in the unbleached kraft pulp (UKP) market because certification and strength performance work together in customer specifications. Chile's production of unbleached radiata pine pulp reached 326,200 tonnes in 2024, down from 503,000 tonnes in 2022, which showed that portfolio discipline among suppliers can also tighten softwood availability in export channels. That supply adjustment reinforced the premium role of softwood furnish in applications where mills cannot compromise on strength benchmarks.

Hardwood is projected to expand at a 5.73% CAGR, which makes it the fastest-growing grade in the unbleached kraft pulp (UKP) market size by segment through 2031. Growth is being supported by wider use of eucalyptus-based furnish in Asian mills, where cost-performance balance often matters more than peak fiber strength. Brazil remained the key structural enabler because national pulp production reached 29.4 million tonnes in 2025 and exports climbed to 20.7 million tonnes, up 11.6% from 2024. Mixed fiber grades are also gaining commercial value in the unbleached kraft pulp industry because mills in Southeast Asia and India are blending hardwood and softwood to optimize input cost and board performance. This keeps grade competition active, but it does not change the fact that softwood remains the reference point for strength-critical specifications in the unbleached kraft pulp market.

Complete Report Scope:

- By Grade

- Softwood Unbleached Kraft Pulp

- Hardwood Unbleached Kraft Pulp

- Mixed Fiber Unbleached Kraft Pulp

- By Application

- Containerboard

- Kraft Paper

- Specialty Paper

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Nordics

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Indonesia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Africa

- North America

Geography Analysis

Asia-Pacific held 39.45% of the unbleached kraft pulp market share in 2025 and is projected to expand at a 5.92% CAGR through 2031, which keeps it as both the largest and fastest-growing regional segment. China remains the main regional demand center because it is the world's largest paperboard producer and continues to require virgin fiber grades for quality-sensitive corrugated packaging output. India is the strongest demand-growth vector within the region, supported by organized retail expansion, pharmaceutical packaging exports, and rising e-commerce fulfillment activity. Japan and South Korea continue to support the unbleached kraft pulp market through technically demanding specialty paper uses, especially in industrial and electronics-linked packaging chains. UPM stated in its Q1 2026 CEO presentation that specialty paper markets in Asia remained stable, even as conditions were softer in Europe and North America.

Europe showed a more regulation-led demand profile in the unbleached kraft pulp market during 2025 and 2026. Regulation (EU) 2025/40 and its August 2026 application timeline pushed packaging buyers to move earlier on recyclable fiber-based formats. Germany's packaging paper production reached 12.5 million tonnes in 2025 and accounted for 67% of national paper output, which showed how deeply packaging has come to dominate paper demand in the country. Billerud continued to upgrade capabilities across its system, including work at Skarblacka in Q1 2026, as part of its focus on premium packaging materials. Mondi also advanced long-term infrastructure through its biomass power project in Ruzomberok, which is expected to raise energy self-sufficiency at the integrated mill from 75% to 90%.

North America remained a major consumption and production hub for the unbleached kraft pulp market, supported by its large integrated containerboard base and continued investment in packaging assets. Packaging paper production in the United States grew 1.7% in 2025, while containerboard operating rates remained at 91.9%, which showed that demand adjusted well to lower capacity. South America continued to function mainly as a supply region for the unbleached kraft pulp market, with Arauco's Sucuriu project reaching 42.6% physical progress by Q4 2025 and remaining on schedule for start-up in the second half of 2027. CMPC's Natureza project also remained a major future capacity addition, with planned output of up to 2.5 million tonnes per year and a dedicated export terminal strategy that will influence global trade flows through 2030.

- International Paper Company

- Stora Enso Oyj

- Mondi plc

- Suzano S.A.

- CMPC Celulosa S.A.

- Canfor Pulp Products Inc.

- Billerud Aktiebolag (publ)

- UPM-Kymmene Corporation

- Oji Holdings Corporation

- Nippon Paper Industries Co., Ltd.

- Georgia-Pacific LLC

- Packaging Corporation of America

- Domtar Corporation

- Mercer International Inc.

- Celulosa Arauco y Constitucion S.A.

- Sappi Limited

- Svenska Cellulosa Aktiebolaget SCA (publ)

- Metsa Board Corporation

- Klabin S.A.

- Smurfit Westrock plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Structure and Integration Dynamics

- 4.2.1 Integrated vs Market Pulp Structure

- 4.2.2 Role of Containerboard Producers (Backward Integration)

- 4.2.3 Regional Production Clusters

- 4.2.4 Degree of Market Fragmentation

- 4.3 Raw Material and Fiber Economics

- 4.3.1 Fiber Mix: Softwood dominant and Mixed hardwood integration

- 4.3.2 Lower Chemical Processing vs Bleached Pulp

- 4.3.3 Wood Cost Structure and Availability

- 4.3.4 Yield Efficiency

- 4.3.5 Recycling Integration in Fiber Mix

- 4.3.6 Sustainability Advantage

- 4.4 Production and Capacity Analysis

- 4.4.1 Global Installed Capacity

- 4.4.2 Integration with Containerboard Mills

- 4.4.3 Capacity Utilization Trends

- 4.4.4 Capacity Additions and Mill Conversions

- 4.4.5 Brownfield vs Greenfield Investments

- 4.5 Trade Flow and Supply Chain

- 4.5.1 Domestic Consumption vs Export Share

- 4.5.2 Key Exporting Regions

- 4.5.3 Key Import Markets

- 4.5.4 Logistics and Freight Impact

- 4.5.5 Regional Self-Sufficiency Trends

- 4.5.6 Supply Chain Disruptions

- 4.6 Pricing Analysis

- 4.7 Cost Structure and Competitiveness

- 4.7.1 Cost Breakdown: Wood, energy, chemicals

- 4.7.2 Cost Advantage vs Bleached Pulp

- 4.7.3 Impact of Recycling Integration

- 4.7.4 Regional Cost Competitiveness

- 4.7.5 Margin Analysis

- 4.8 Market Dynamics

- 4.8.1 Market Drivers

- 4.8.1.1 Growth in Corrugated Packaging Demand Driven by E-commerce

- 4.8.1.2 Shift Toward Sustainable, Unbleached Packaging Materials

- 4.8.1.3 Plastic Substitution in Retail and Transport Packaging

- 4.8.1.4 Growth in Heavy-Duty Packaging

- 4.8.1.5 Lower Chemical Processing Enhancing Environmental Acceptance

- 4.8.1.6 Integration Strategies by Packaging Companies

- 4.8.2 Market Restraints

- 4.8.2.1 Strong Competition from Recycled Fiber (OCC-based production)

- 4.8.2.2 Limited Use in High-Quality Applications

- 4.8.2.3 Raw Material Cost Volatility (wood supply impact)

- 4.8.2.4 Environmental Pressure on Forestry and Land Use

- 4.8.1 Market Drivers

- 4.9 Technology and Process Landscape

- 4.9.1 Kraft Pulping Process (Unbleached Focus)

- 4.9.2 Chemical Recovery Systems

- 4.9.3 Energy Efficiency Improvements

- 4.9.4 Fiber Strength Optimization

- 4.9.5 Automation and Digitalization

- 4.10 ESG and Sustainability Analysis

- 4.10.1 Reduced Chemical Usage vs Bleached Pulp

- 4.10.2 Carbon Footprint Comparison

- 4.10.3 Forestry Sustainability

- 4.10.4 Recycling Integration

- 4.10.5 Regulatory Landscape

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Grade

- 5.1.1 Softwood Unbleached Kraft Pulp

- 5.1.2 Hardwood Unbleached Kraft Pulp

- 5.1.3 Mixed Fiber Unbleached Kraft Pulp

- 5.2 By Application

- 5.2.1 Containerboard

- 5.2.2 Kraft Paper

- 5.2.3 Specialty Paper

- 5.2.4 Other Applications

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Russia

- 5.3.3.5 Nordics

- 5.3.3.6 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Indonesia

- 5.3.4.5 Rest of Asia-Pacific

- 5.3.5 Middle East and Africa

- 5.3.5.1 Middle East

- 5.3.5.2 Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 International Paper Company

- 6.4.2 Stora Enso Oyj

- 6.4.3 Mondi plc

- 6.4.4 Suzano S.A.

- 6.4.5 CMPC Celulosa S.A.

- 6.4.6 Canfor Pulp Products Inc.

- 6.4.7 Billerud Aktiebolag (publ)

- 6.4.8 UPM-Kymmene Corporation

- 6.4.9 Oji Holdings Corporation

- 6.4.10 Nippon Paper Industries Co., Ltd.

- 6.4.11 Georgia-Pacific LLC

- 6.4.12 Packaging Corporation of America

- 6.4.13 Domtar Corporation

- 6.4.14 Mercer International Inc.

- 6.4.15 Celulosa Arauco y Constitucion S.A.

- 6.4.16 Sappi Limited

- 6.4.17 Svenska Cellulosa Aktiebolaget SCA (publ)

- 6.4.18 Metsa Board Corporation

- 6.4.19 Klabin S.A.

- 6.4.20 Smurfit Westrock plc

7 STRATEGIC OUTLOOK AND FUTURE DYNAMICS

- 7.1 Packaging-Led Demand Outlook

- 7.2 Competition vs Recycled Fiber

- 7.3 Risk Assessment

- 7.4 Future Role in Fiber Mix