|

시장보고서

상품코드

2072703

중동 및 북아프리카의 지붕재 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Middle East and North Africa Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

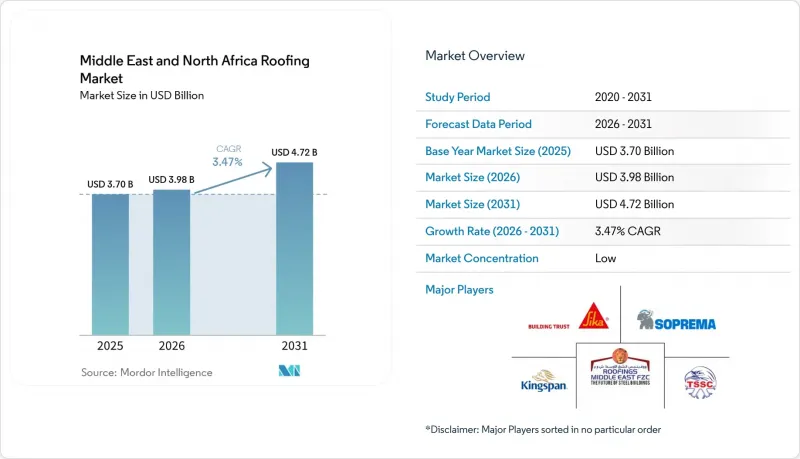

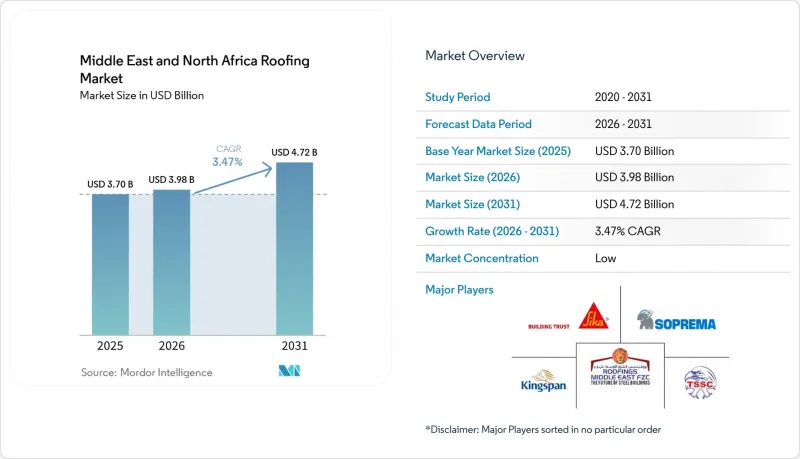

Mordor Intelligence에 의하면, 중동 및 북아프리카의 지붕재 시장 규모는 2025년 37억 달러로 평가되었고, 2026년 39억 8,000만 달러로 추정되고, 2031년까지 47억 2,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 3.47%를 나타낼 전망입니다.

본 보고서는 자재별(아스팔트 슁글, 점토 및 콘크리트 기와, 금속 지붕 등), 건축 형태별(신축, 지붕 재시공 및 교체), 용도별(주택, 상업시설, 산업 시설, 공공시설, 기타) 및 지역별(사우디아라비아, 아랍에미리트, 이집트 등)으로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중동 및 북아프리카의 지붕재 시장 동향 및 인사이트

사우디아라비아의 초대형 프로젝트, 주택 건설 확대 및 관광 주도형 지붕재 수요

사우디아라비아는 주택 건설 확대와 대규모 관광 프로젝트가 동시에 진행되고 있는 만큼, 중동 및 북아프리카의 지붕재 시장에서 여전히 가장 뚜렷한 수요 동력으로 자리 잡고 있습니다. 주택 건설 프로그램이 지붕재에 대한 기본적인 수요를 끌어올리고 있는 반면, 관광 및 복합 애플리케이션 개발은 단열성, 방음성 및 태양광 발전 통합과 관련된 요건이 더 엄격한 고성능 시스템으로의 전환을 촉진하고 있습니다. 이러한 상황의 변화에 따라 지붕재 패키지의 가치 구성이 변화하고 있으며, 현재는 기본적인 범용 자재가 아닌 사양 주도형 시스템을 필요로 하는 프로젝트가 증가하고 있습니다. 프로젝트 승인 기준, 보증에 대한 기대치 및 시스템 인증 요건을 충족하는 공급업체는 단순히 생산량만으로 경쟁하는 공급업체보다 유리한 입장에 있습니다. 그 결과, 중동 및 북아프리카의 지붕재 시장은 대규모 판매와 첨단 기술력이라는 두 가지 이점을 모두 누리고 있습니다.

의무화된 에너지 규제로 인해 지붕 단열재 및 반사성 지붕재의 사용이 확대되고 있습니다.

중동 및 북아프리카의 지붕재 시장에서 에너지 규제는 현재 직접적인 사양 결정 요인으로 작용하고 있습니다. 이는 규제 준수가 건축 허가 및 설계 승인 절차에 포함되어 있기 때문입니다. 두바이 시 당국은 신축 평지붕 및 경사가 완만한 지붕에 대해 태양 반사율 지수(SRI)의 최저치를 78로 정하고 있으며, 아부다비와 카타르에서도 이와 유사한 건축 성능 기준이 도입되어 있습니다. 사우디아라비아에서는 사우디 건축기준법에 따라 지붕 구조의 열관류율에 제한이 설정되어 있으며, 발표된 조사 결과에 따르면 단열재를 채택함으로써 해당 국가의 모든 기후대에서 건물의 에너지 소비량을 줄일 수 있는 것으로 나타났습니다. 실제로, 반사성 마감재만을 사용하는 방식은 코팅재의 성능과 단열성을 모두 갖추고, 장기적인 에너지 규제를 준수할 수 있는 지붕 구조에 시장 점유율을 점차 빼앗기고 있습니다. 이로 인해 프로젝트당 평균 자재비가 상승하고 있으며, 중동 및 북아프리카의 지붕재 시장 전반에서 부가가치가 높은 제품 구성이 촉진되고 있습니다.

철강, 아스팔트, 폴리머 및 수입과 연동되는 원자재 비용의 변동

원자재 비용의 변동은 중동 및 북아프리카의 지붕재 시장에서 여전히 이익률 확대에 있어 가장 뚜렷한 제약 요인 중 하나로 남아 있습니다. 2025년 『Buildings』에 게재된 연구에 따르면, 카타르의 건설 가격 조정 메커니즘은 신뢰할 수 있는 현지 가격 지표가 부족하거나 지연될 경우, 시공사를 충분히 보호하지 못하고 있는 것으로 밝혀졌습니다. 금속 지붕재 공급업체는 설령 현지 가격이 단기간 동안 하락하더라도, 세계 철강 가격, 운임 및 수입 패리티의 변동 영향을 계속 받게 될 것입니다. 북아프리카에서는 수입 원자재가 환율 변동이나 상품 가격 변동의 영향을 받을 가능성이 있기 때문에 이러한 위험이 더욱 두드러집니다. 이러한 비용의 불안정성은 사양 업그레이드 제안을 어렵게 만들며, 중동 및 북아프리카 지붕재 시장 전체에서 프로젝트가 고부가가치 제품으로 전환되는 속도를 늦출 가능성이 있습니다.

부문별 분석

2025년, 역청 및 개질 아스팔트계 방수 시트는 총 수요의 33.5%를 차지했으며, 중동 및 북아프리카의 지붕재 시장에서 가장 큰 재료 그룹이 되었습니다. 이러한 우위는 입증된 내열성, 시공업체들 사이에서 널리 인정받고 있는 점, 그리고 사우디아라비아와 이집트 등 여러 국가에서 현지화된 공급망에 의해 여전히 뒷받침되고 있습니다. 또한, 이러한 방수 시트는 주거용 및 일반적인 상업용 분야에서도 널리 보급되어 있으며, 이러한 분야에서는 구매자들이 여전히 초기 비용과 확립된 시공 방법을 중요하게 여기고 있습니다. 이러한 장점에도 불구하고, 프로젝트 발주처가 더욱 강력한 방수 성능, 높은 반사율, 보증 지원을 요구함에 따라 자재 구성은 점차 고부가가치 시스템으로 전환되고 있습니다. 이러한 변화로 인해 총 톤수 증가세는 완만한 수준에 그치고 있지만, 중동 및 북아프리카의 지붕재 업계에서 부가가치 성장이 촉진되고 있습니다.

열가소성 폴리올레핀(TPO), 에틸렌·프로파일렌·디엔 단량체(EPDM), 폴리염화비닐(PVC)을 포함한 단층 필름은 2031년까지 연평균 성장률(CAGR)이 5.8%로, 가장 빠르게 성장이 전망되는 소재 부문입니다. 그 매력은 옥상 태양광 발전과의 호환성, 사용 중인 건물에서의 보다 친환경적인 시공, 그리고 해안 지역 상업 프로젝트의 쿨루프 규정 준수에 있습니다. 두바이 전력·수도청(DEWA)의 보고서에 따르면, 2025년까지 두바이의 8,430개 건물에 총 725메가와트의 옥상 태양광 발전 설비가 연결될 예정이며, 이는 설치 시스템과의 호환성을 갖추고 보증 요건을 충족하는 지붕 구조에 대한 수요가 높음을 입증하고 있습니다. 금속 지붕은 산업 시설에서도 중요한 역할을 하고 있습니다. 한편, 북아프리카와 중동 일부 지역에서는 점토 기와와 콘크리트 기와가 여전히 중요한 위치를 차지하고 있어, 지붕재 시장은 단일 소재가 주도하는 형태가 아니라 다양한 소재가 혼재하는 상태가 지속될 전망입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 동향과 분석

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the middle east and north africa roofing market size is projected to expand from USD 3.70 billion in 2025 and USD 3.98 billion in 2026 to USD 4.72 billion by 2031, registering a CAGR of 3.47% between 2026 to 2031.

This report is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, Metal Roofing, and More), by Construction Type (New Construction and Reroofing and Replacement), by Application (Residential, Commercial, Industrial, Institutional, and Others), and by Geography (Saudi Arabia, United Arab Emirates, Egypt, and More). The Market Forecasts are Provided in Terms of Value (USD).

Middle East and North Africa Roofing Market Trends and Insights

Saudi Giga-Projects, Housing Expansion, and Tourism-Led Roof Demand

Saudi Arabia remains the clearest demand engine for the Middle East and North Africa roofing market, as housing expansion and large destination projects are advancing simultaneously. Housing programs are increasing baseline roof demand, while tourism and mixed-use developments are pushing projects toward higher-performing systems with stronger thermal, acoustic, and solar integration requirements. This mix is changing the value profile of the roof package, as more projects now require specification-led systems rather than basic commodity materials. Suppliers that meet project approval standards, warranty expectations, and system certification requirements are in a stronger position than those that compete only on output volume. As a result, the Middle East and North Africa roofing market is benefiting from both high volume and richer technical content.

Mandatory Energy Codes Increasing Roof Insulation and Reflective Roof Adoption

Energy regulation is now a direct specification force in the Middle East and North Africa roofing market because compliance is built into permit and design approval processes. Dubai Municipality requires a minimum Solar Reflectance Index (SRI) of 78 for flat and low-sloped roofs in new construction, and comparable building performance systems are active in Abu Dhabi and Qatar. In Saudi Arabia, the Saudi Building Code sets limits on roof assembly thermal transmittance, and published research shows that insulation can reduce building energy use across the country's climate zones. The practical effect is that reflective finishes alone are losing ground to roof assemblies that combine membrane performance with insulation and longer-term energy compliance. This is raising the average material bill per project and supporting a higher-value product mix across the roofing market in the Middle East and North Africa.

Volatile Steel, Bitumen, Polymer, and Import-Linked Input Costs

Input cost volatility remains one of the clearest limits on margin expansion in the Middle East and North Africa roofing market. A 2025 study in Buildings found that construction price adjustment mechanisms in Qatar do not fully protect contractors when reliable local pricing benchmarks are weak or delayed. Metal roofing suppliers also remain exposed to movements in global steel pricing, freight, and import parity, even when local prices soften for short periods. The risk is more pronounced in North Africa because imported raw materials can be affected by currency fluctuations and commodity price movements. This cost instability makes specification upgrades harder to sell and can delay the conversion of projects into higher-value products across the Middle East and North Africa roofing market.

Other drivers and restraints analyzed in the detailed report include:

- Industrial, Logistics, and Warehouse Build-Out Supporting Insulated Metal Roof Panels

- Waterproofing Upgrade Cycle for Flat Roofs in Hot-Climate Commercial Assets

- Price-Led Specification Behavior Slowing Premium Membrane Conversion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bituminous / modified bitumen membranes accounted for 33.5% of total demand in 2025, making them the largest material group in the Middle East and North Africa roofing market. Their lead still rests on proven heat resistance, wide contractor familiarity, and localized supply chains in countries such as Saudi Arabia and Egypt. These membranes are also well established across residential and standard commercial applications, where buyers still put strong weight on initial cost and known installation practices. Even with this lead, the material mix is gradually shifting toward higher-value systems as project owners request stronger waterproofing, greater reflectivity, and warranty support. That shift is boosting value growth in the Middle East and North Africa roofing industry, even as total tonnage rises at a more moderate pace.

Single-ply membranes, including thermoplastic polyolefin (TPO), ethylene propylene diene monomer (EPDM), and polyvinyl chloride (PVC), are the fastest-growing material category at a 5.8% CAGR through 2031. Their appeal lies in rooftop solar compatibility, cleaner installation on occupied buildings, and compliance with cool-roof rules in Gulf commercial projects. Dubai Electricity and Water Authority reported that 725 megawatts of rooftop solar had been connected across 8,430 buildings in Dubai by 2025, underscoring demand for roof assemblies compatible with mounting systems and meeting warranty requirements. Metal roofing also plays an important role in industrial facilities. At the same time, clay and concrete tiles remain relevant in parts of North Africa and the Middle East, and the roofing market will remain mixed rather than single-material-led.

Complete Report Scope:

- By Material Type

- Asphalt Shingles

- Clay and Concrete Tiles

- Metal Roofing

- Bituminous / Modified Bitumen Membranes

- Single-Ply Membranes (TPO, EPDM, and PVC)

- Wood

- Other Roofing Materials

- By Construction Type

- New Construction

- Reroofing and Replacement

- By Application

- Residential

- Commercial

- Industrial

- Institutional

- Other Applications

- By Geography

- Saudi Arabia

- United Arab Emirates

- Egypt

- Morocco

- Qatar

- Rest of the Middle East and North Africa

List of Companies Covered in this Report:

- Sika

- Soprema

- Kingspan

- TSSC Group

- Roofings Middle East

- Emirates Industrial Panel

- Litco Industries

- Compass Waterproofing

- SECC Insulation

- Target Engineering Specialized Works

- Maghreb Steel

- Pyramids Steel

- Al-Majd International for Bituminous Insulation

- SAHARA Insulation Factory

- Saudi Insulation Factory

- BMI Group

- Saint-Gobain

- GAF

- Owens Corning

- Arabian Tiles Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Saudi Giga-Projects, Housing Expansion, and Tourism-Led Roof Demand

- 4.2.2 Mandatory Energy Codes Increasing Roof Insulation and Reflective Roof Adoption

- 4.2.3 Industrial, Logistics, and Warehouse Build-Out Supporting Insulated Metal Roof Panels

- 4.2.4 Waterproofing Upgrade Cycle for Flat Roofs in Hot-Climate Commercial Assets

- 4.2.5 Solar-Ready Rooftop Specifications Increasing Demand for PV-Compatible Roofing Systems

- 4.2.6 Extreme Rain and Flood Resilience Retrofits Accelerating Waterproofing-Led Reroofing

- 4.3 Market Restraints

- 4.3.1 Volatile Steel, Bitumen, Polymer, and Import-Linked Input Costs

- 4.3.2 Shortage of Certified Installers for Advanced Roof Systems

- 4.3.3 Summer Heat and Hot-Work Restrictions Narrowing Installation Windows

- 4.3.4 Price-Led Specification Behavior Slowing Premium Membrane Conversion

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Cost Structure Analysis

- 4.8 Trend and Impacts of Roofing on Replacements

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Material Type

- 5.1.1 Asphalt Shingles

- 5.1.2 Clay and Concrete Tiles

- 5.1.3 Metal Roofing

- 5.1.4 Bituminous / Modified Bitumen Membranes

- 5.1.5 Single-Ply Membranes (TPO, EPDM, and PVC)

- 5.1.6 Wood

- 5.1.7 Other Roofing Materials

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Reroofing and Replacement

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Institutional

- 5.3.5 Other Applications

- 5.4 By Geography

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Egypt

- 5.4.4 Morocco

- 5.4.5 Qatar

- 5.4.6 Rest of the Middle East and North Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Sika

- 6.4.2 Soprema

- 6.4.3 Kingspan

- 6.4.4 TSSC Group

- 6.4.5 Roofings Middle East

- 6.4.6 Emirates Industrial Panel

- 6.4.7 Litco Industries

- 6.4.8 Compass Waterproofing

- 6.4.9 SECC Insulation

- 6.4.10 Target Engineering Specialized Works

- 6.4.11 Maghreb Steel

- 6.4.12 Pyramids Steel

- 6.4.13 Al-Majd International for Bituminous Insulation

- 6.4.14 SAHARA Insulation Factory

- 6.4.15 Saudi Insulation Factory

- 6.4.16 BMI Group

- 6.4.17 Saint-Gobain

- 6.4.18 GAF

- 6.4.19 Owens Corning

- 6.4.20 Arabian Tiles Company

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment