|

시장보고서

상품코드

2072712

ASEAN의 지붕재 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)ASEAN Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

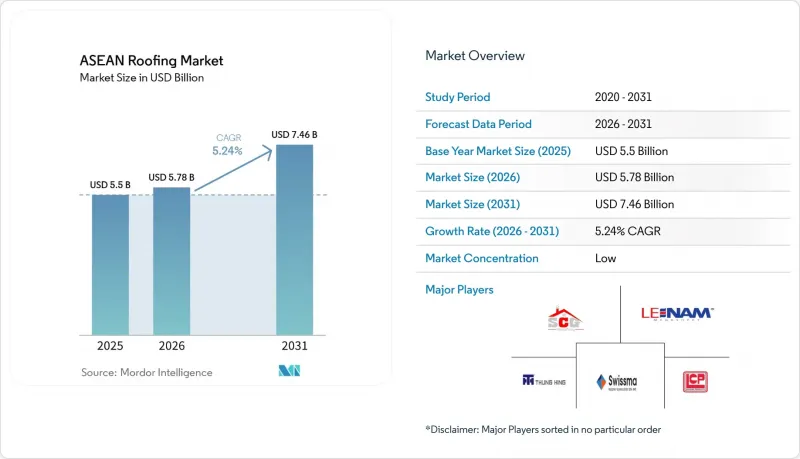

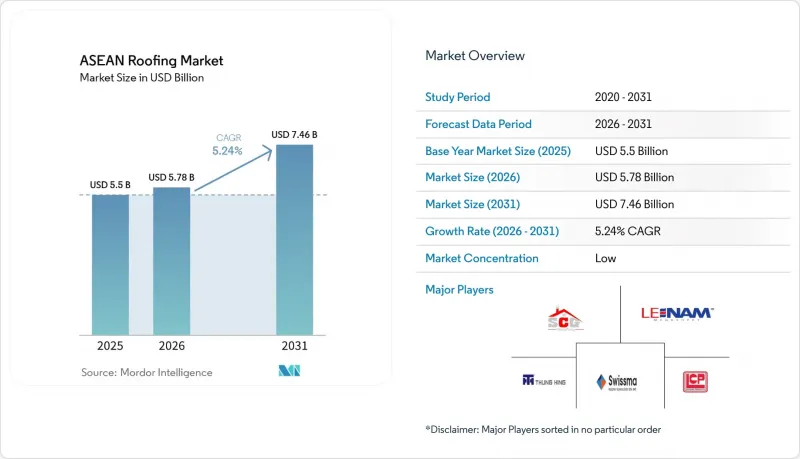

Mordor Intelligence에 의하면, ASEAN의 지붕재 시장 규모는 2025년에 55억 달러로 평가되었고, 2026년에 57억 8,000만 달러로 추정되고, 2031년까지 74억 6,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 5.24%로 성장할 전망입니다.

본 보고서는 자재 유형별(아스팔트 슁글, 점토 및 콘크리트 기와, 금속 지붕재, 역청 및 개질 아스팔트 방수 시트, 단층 방수 시트, 목재, 기타), 시공 유형별(신축, 지붕 재시공 및 교체), 용도별(주택, 상업시설, 산업 시설, 기타), 지역별(인도네시아, 베트남, 태국, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

ASEAN의 지붕재 시장 동향 및 인사이트

정부 주도의 주택·인프라 계획이 지붕재 수요를 확대

민간 건설의 진척도에 편차가 나타나는 가운데, 정부 주도의 주택 계획이 아세안 지붕재 시장에 확실한 버팀목이 되고 있습니다. 인도네시아에서는 43조 6,000억 루피아(26억 5,000만 달러)의 예산을 투입해 2025년 말까지 기준 미달 주택 200만 호를 개보수할 계획으로, 서자바, 반텐, 중부 자바 등 주택 부족이 심각한 주에서 지붕재 교체 수요를 직접적으로 견인하고 있습니다. 베트남에서는 2025년에 10만 2,600세대 이상의 사회주택이 준공되어 연간 계획을 초과 달성했습니다. 2026년 목표는 15만 8,723호로 상향 조정되었으며, 그 배경에는 공공 투자 지출 확대가 있습니다. 이러한 프로그램이 중요한 이유는 민간 주택 착공이 둔화되더라도 지붕재 수요량을 유지할 수 있을 뿐만 아니라, 제조업체와 시공업체의 수주 전망이 더욱 명확해지기 때문입니다. 또한, 대규모 주택 건설에서 인증을 받은 표준화된 자재의 사용을 촉진함으로써, 비정규 제품이나 재활용 지붕재의 비중을 점차 줄이고, 아세안(ASEAN) 지붕재 시장에서 정규적이고 개척 가능한 고객 기반을 확대하는 데에도 기여할 것입니다.

친환경 건축 및 열 성능 규제에 따른 지붕 사양의 강화

건축 외피의 성능에 관한 규제는 아세안(ASEAN) 지붕재 시장에서 제품 선택에 꾸준한 변화를 가져오고 있습니다. 국제에너지기구(IEA)가 수립한 아세안(ASEAN)의 에너지 효율이 높은 건축물에 관한 로드맵에서는 열대 기후에서 지붕이 중요한 열 경계라고 지적하고 있습니다. 이 로드맵은 냉방 수요를 줄이기 위한 실용적인 대책으로 쿨 루프, 그린 루프, 그리고 수동 환기를 강조하고 있습니다. 2026년 4월, 아세안 에너지 센터(ACE)와 유엔 환경 계획(UNEP)이 발표한 '수동 냉각 로드맵' 또한 한 걸음 더 나아가, 각국의 건축기준법에서 패시브 냉각 요건을 의무화할 것을 권장하는 한편, 반사형 지붕을 주요 대책으로 제시하고 있습니다. 녹색 인증 제도가 프로젝트 금융이나 공공 조달에서 실질적인 요건이 되면, 구매자들은 개별적인 저가 부품이 아닌, 기준을 준수한 지붕 시스템 일체를 구매하는 경향이 강해집니다. 이러한 추세는 반사형, 단열형 및 통합형 지붕 시스템을 촉진하여, 아세안(ASEAN) 지붕재 시장을 공공 및 상업 프로젝트에서의 단순한 상품 구매 단계에서 벗어나게할 것입니다.

원자재 가격 변동이 프로젝트의 수익성과 공급업체의 이익률을 압박하고 있습니다.

원자재 비용의 변동은 여전히 아세안 지붕재 시장에 있어 가장 뚜렷한 걸림돌 중 하나입니다. 아스팔트, 폴리염화비닐(PVC) 수지, 열가소성 폴리올레핀(TPO) 컴파운드 및 강철 코일은 현지 건설 일정이나 입찰 일정과 종종 맞지 않는 세계 상품 주기의 영향을 받기 쉽습니다. 경제협력개발기구(OECD)의 『2025년 철강 전망』에 따르면, 아세안(ASEAN)의 금속 지붕 제조업체들에게 매우 중요한 스트립 및 코일 구매자들에게 있어 가격 변동은 생산 능력 확충이나 수요 증가의 불균형에서 비롯될 가능성이 있습니다. 2024년과 2025년에는 이러한 가격 변동으로 인해 공급업체의 이익률이 압박을 받게 되었고, 입찰 가격을 확보하기 어려워졌기 때문에 일부 도급업체는 품질이 낮은 자재를 선택할 수밖에 없게 되었습니다. 헤지 능력, 장기 조달 계약 또는 일정 수준의 원자재 통합 체계를 갖추지 못한 제조업체는 아세안 지붕재 시장의 장기적인 프로젝트 주기에서 여전히 큰 위험에 노출되어 있습니다.

부문별 분석

2025년, 금속 지붕재는 아세안 지붕재 시장의 38%를 차지했으며, 해당 지역 전체에서 가장 큰 소재 카테고리가 되었습니다. 이러한 위상은 산업용 창고, 도시 근교의 주택, 그리고 공공 프로젝트에서 폭넓게 활용되고 있는 데 기인하며, 이러한 분야에서는 시공 속도와 평방미터당 비용이 여전히 주요 구매 기준으로 작용하고 있습니다. 또한, 이 부문은 해당 지역의 제조 및 물류 인프라 확충의 혜택도 누리고 있습니다. 스팬이 넓고 경사가 완만한 지붕에는 일반적으로 성형 금속판이 사용되며, 경우에 따라 단열 복합층과 결합되기도 하기 때문입니다. OECD의 2025년 철강 전망은 아세안(ASEAN)을 2030년까지 철강 수요가 강력하게 증가할 것으로 예상되는 몇 안 되는 지역 중 하나로 꼽고 있으며, 이는 이러한 배경을 뒷받침하고 있습니다. 아세안 지붕재 시장에서 이를 통해 금속 지붕 제조업체들은 가격 변동이 심한 상황에서도 전략적으로 중요한 자재 공급 기반을 확보할 수 있게 됩니다.

아세안 지붕재 시장에서 단층 필름은 2031년까지 연평균 성장률(CAGR) 6.4%를 나타낼 것으로 예측되며, 예측 기간 동안 가장 빠르게 성장하는 건축자재 그룹이 될 전망입니다. 이러한 수요를 주도하고 있는 것은 싱가포르, 자카르타, 호치민시의 데이터센터와 고사양 상업용 지붕으로, 이 지역에서는 이음매 파손 위험이 낮고 교체에 따른 가동 중단 기간이 짧기 때문에 열용접 시스템이 선택되고 있습니다. 태국과 베트남의 주택에서는 점토 기와와 콘크리트 기와가 여전히 문화적·건축적 중요성을 지니고 있습니다. 그러나 다층 건물에서는 더 가벼운 섬유 시멘트나 금속 재질의 건축자재로 대체해야 한다는 압박에 직면해 있습니다. 아스팔트 슁글은 태국, 말레이시아, 필리핀의 고급 주택가를 중심으로 여전히 집중적으로 채택되고 있습니다. 한편, 아스팔트계 방수 시트는 시공 업체의 기반이 확립되어 있고, 용접식 시스템에 비해 필요한 장비가 적기 때문에 평지붕을 가진 상업시설이나 산업 시설에서 계속해서 채택되고 있습니다. 목재 지붕재는 감소 추세를 보이고 있는 반면, 폴리카보네이트, uPVC, 섬유 시멘트 시트는 합리적인 가격대의 주택 리모델링 분야에서 보급이 확대되고 있습니다. 특히, 인증을 받은 단열성 및 유지보수가 용이한 제품이 정부 주도의 리노베이션 수요와 부합하는 지역에서는 이러한 경향이 두드러집니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the ASEAN roofing market size is projected to be USD 5.5 billion in 2025, USD 5.78 billion in 2026, and reach USD 7.46 billion by 2031, growing at a CAGR of 5.24% from 2026 to 2031.

This report is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, Metal Roofing, Bituminous / Modified Bitumen Membranes, Single-Ply Membranes, Wood, and Others), Construction Type (New Construction, Reroofing and Replacement), Application (Residential, Commercial, Industrial, and More), and Geography (Indonesia, Vietnam, Thailand, and More). The Market Forecasts are Provided in Terms of Value (USD).

ASEAN Roofing Market Trends and Insights

Government Housing and Infrastructure Pipelines Expanding Roofing Demand

Government-backed housing schemes are providing a reliable support base for the ASEAN roofing market as private construction moves unevenly. In Indonesia, the renovation of 2 million substandard dwellings by the end of 2025, backed by Rp 43.6 trillion (USD 2.65 billion), is directly driving roofing replacement demand in provinces with large housing deficits such as West Java, Banten, and Central Java. In Vietnam, more than 102,600 social housing units were completed in 2025, which exceeded the annual plan, and the 2026 target rises to 158,723 units, with stronger public investment disbursement behind it. These programs matter because they sustain roofing volume even when private housing starts slow, and they create clearer order visibility for manufacturers and contractors. They also encourage the use of certified, standardized materials in mass housing, gradually reducing the role of informal or recycled roofing inputs and broadening the formal, addressable base of the ASEAN roofing market.

Green-Building and Thermal-Performance Regulation Tightening Roof Specifications

Regulations around building envelope performance are steadily changing product choice in the ASEAN roofing market. The International Energy Agency (IEA) roadmap for energy-efficient buildings in ASEAN identifies roofs as the critical thermal boundary in tropical climates. It highlights cool roofs, green roofs, and passive ventilation as practical measures to reduce cooling demand. The Passive Cooling Roadmap launched by the ASEAN Centre for Energy (ACE) and the United Nations Environment Programme (UNEP) in April 2026 goes further by recommending mandatory passive cooling requirements in national building codes and identifying reflective roofs as a leading intervention. Once green certification systems become a practical requirement for project financing or public procurement, buyers tend to purchase compliant roof assemblies rather than isolated low-cost components. That dynamic supports reflective, insulated, and integrated roof systems and moves the ASEAN roofing market away from purely commodity purchasing in institutional and commercial projects.

Raw-Material Cost Volatility Compressing Project Economics and Supplier Margins

Input cost volatility is still one of the clearest brakes on the ASEAN roofing market. Bitumen, Polyvinyl Chloride (PVC) resin, Thermoplastic Polyolefin (TPO) compounds, and steel coil are exposed to global commodity cycles that often move out of step with local construction schedules and tender timelines. According to the Organisation for Economic Co-operation and Development's (OECD) 2025 Steel Outlook, fluctuations in pricing for strip and coil buyers, crucial for metal roofing manufacturers in ASEAN, may arise from capacity additions and inconsistent demand growth. In 2024 and 2025, those swings compressed supplier margins and pushed some contractors toward downgraded material choices when protecting bids became difficult. Manufacturers without hedging capacity, long-term sourcing arrangements, or some level of input integration remain more exposed during long project cycles in the ASEAN roofing market.

Other drivers and restraints analyzed in the detailed report include:

- Industrial, Logistics, and Data Centre Build Out Driving Insulated Metal Panel Demand

- Tropical Climate and Monsoon Exposure Reinforcing Premium Waterproofing Specification

- Skilled Installer Shortages Reducing Execution Quality and Slowing Specialized Roof Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal roofing accounted for 38% of the ASEAN roofing market in 2025, making it the largest material category across the region. Its position is tied to broad use in industrial warehousing, peri-urban housing, and public projects where speed of installation and cost per square meter remain central buying criteria. The category also benefits from the region's manufacturing and logistics build-out, as large-span, low-slope roofs commonly default to profiled metal sheets, sometimes paired with insulated composite layers. The OECD's 2025 steel outlook reinforces this backdrop by identifying ASEAN as one of the few regions where steel demand is expected to grow strongly through 2030. In the ASEAN roofing market, this gives metal roofing manufacturers a material supply base that remains strategically important even when prices are volatile.

Single-ply membranes are projected to grow at a 6.4% CAGR in the ASEAN roofing market through 2031, making them the fastest-growing material group in the forecast period. Their demand is being led by data centers and high-specification commercial roofs in Singapore, Jakarta, and Ho Chi Minh City, where heat-welded systems are chosen for low seam-failure risk and short replacement shutdown windows. Clay and concrete tiles still retain cultural and architectural relevance in Thai and Vietnamese housing. Still, they face pressure to be replaced by lighter fiber-cement and metal options in multi-story applications. Asphalt shingles remain more concentrated in premium residential pockets in Thailand, Malaysia, and the Philippines. At the same time, bituminous membranes continue to serve flat commercial and industrial roofs because they have a familiar installer base and lower equipment needs than welded systems. Wood roofing is declining, while polycarbonate, uPVC, and fiber-cement sheets are gaining traction in affordable housing renovation, especially where certified heat-reflective, low-maintenance products align with state-backed renovation demand.

Complete Report Scope:

- By Material Type

- Asphalt Shingles

- Clay & Concrete Tiles

- Metal Roofing

- Bituminous / Modified Bitumen Membranes

- Single-Ply Membranes (TPO, EPDM, and PVC)

- Wood

- Others

- By Construction Type

- New Construction

- Reroofing and Replacement

- By Application

- Residential

- Commercial

- Industrial

- Institutional

- Others

- By Geography

- Indonesia

- Vietnam

- Thailand

- Philippines

- Rest of ASEAN

List of Companies Covered in this Report:

- SCG Roofing

- Swissma Building Technologies

- Thung Hing

- Le Nam Megasheet

- LCP Group

- Kemudi Sempurna

- Asia Jaya Sepadu

- UGI

- PT. Insulated Panel Indonesia

- Subzero

- PT. Mandiri Mulia Makmur Abadi (MMMA)

- ROOFMAXX

- Kingspan

- Sika

- SOPREMA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Housing and Infrastructure Pipelines Expanding Roofing Demand

- 4.2.2 Green Building and Thermal Performance Rules Supporting Cool and Insulated Roofs

- 4.2.3 Industrial, Logistics, Cold Chain, and Data Center Build Out Increasing Demand for Insulated Panels and Membranes

- 4.2.4 Tropical Humidity, Monsoon Exposure, and Leakage Risk Lifting Waterproofing Intensity

- 4.2.5 Green Roofs, Siphonic Drainage, and Stormwater Features Adding Premium Content

- 4.2.6 Lower Intra-ASEAN Trade Barriers Improving Access to Premium Roofing Inputs

- 4.3 Market Restraints

- 4.3.1 Raw Material Cost Volatility in Bitumen, Resin, and Petrochemical Inputs Pressuring Margins

- 4.3.2 Skilled Installer Shortages Reducing Execution Quality and Slowing Specialized Roof Adoption

- 4.3.3 Competition from Lower Cost Substitute Materials Capping Pricing Power

- 4.3.4 Import Dependence and Uneven Regional Standards Complicating Supply Decisions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Cost Structure Analysis

- 4.8 Trend and Impacts of Roofing Replacements

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material Type

- 5.1.1 Asphalt Shingles

- 5.1.2 Clay & Concrete Tiles

- 5.1.3 Metal Roofing

- 5.1.4 Bituminous / Modified Bitumen Membranes

- 5.1.5 Single-Ply Membranes (TPO, EPDM, and PVC)

- 5.1.6 Wood

- 5.1.7 Others

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Reroofing and Replacement

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Institutional

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 Indonesia

- 5.4.2 Vietnam

- 5.4.3 Thailand

- 5.4.4 Philippines

- 5.4.5 Rest of ASEAN

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 SCG Roofing

- 6.4.2 Swissma Building Technologies

- 6.4.3 Thung Hing

- 6.4.4 Le Nam Megasheet

- 6.4.5 LCP Group

- 6.4.6 Kemudi Sempurna

- 6.4.7 Asia Jaya Sepadu

- 6.4.8 UGI

- 6.4.9 PT. Insulated Panel Indonesia

- 6.4.10 Subzero

- 6.4.11 PT. Mandiri Mulia Makmur Abadi (MMMA)

- 6.4.12 ROOFMAXX

- 6.4.13 Kingspan

- 6.4.14 Sika

- 6.4.15 SOPREMA

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment