|

시장보고서

상품코드

2072704

HR 혁신 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)HR Transformation Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

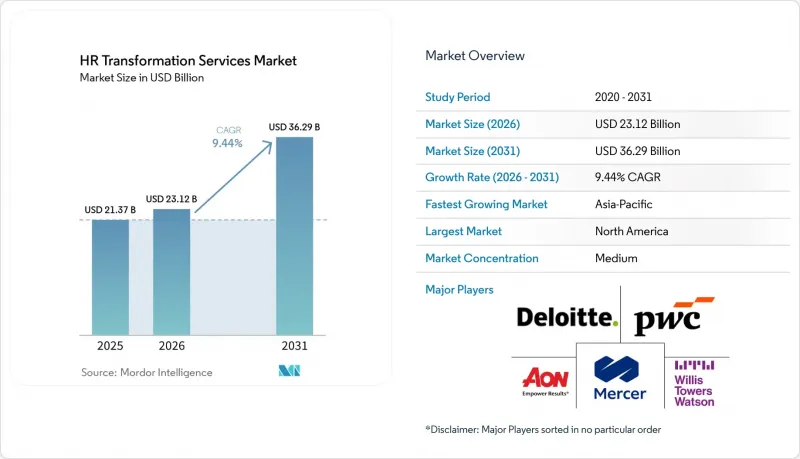

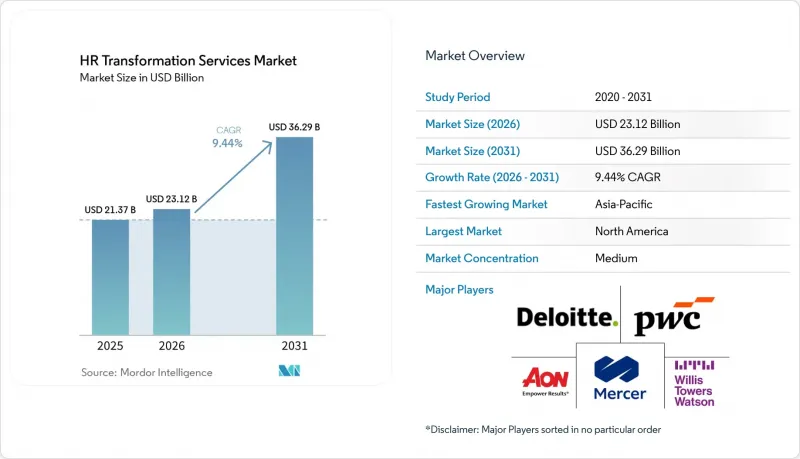

Mordor Intelligence에 의하면, HR 혁신 서비스 시장 규모는 2025년 213억 7,000만 달러로 평가되었고, 2026년에는 231억 2,000만 달러로 추정되고, 2031년까지 362억 9,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 9.44%로 성장할 전망입니다.

본 보고서는 서비스 유형별(HR 운영 모델 및 조직 설계 등), 기업 규모별(대기업, 중소기업), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학 등), 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류되어 있으며, 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 HR 혁신 서비스 시장 동향 및 인사이트

엔드투엔드 인사 운영 모델 재설계에 대한 기업 수요 증가

엔드투엔드 재설계는 HR 혁신 서비스 시장의 지출 계획에서 최우선 과제로 자리 잡고 있습니다. 이는 기업 측이 새로운 도구만으로는 성과를 바꿀 수 없다는 점을 인식하게 되었기 때문입니다. 많은 조직에서는 속도, 분석, AI를 활용한 의사결정보다 관리, 승인 및 관리상의 일관성을 중시하여 구축된 인사 체제를 여전히 유지하고 있습니다. 이러한 상황에 따라 고객들은 개별 프로젝트가 아닌, 단일 범위 내에서 프로세스 소유권, 서비스 제공 계층, 워크플로우 자동화, 의사결정 권한 및 관리자용 셀프 서비스를 포괄하는 프로그램으로 눈을 돌리고 있습니다. 최근 동향을 살펴보면, AI 기능이 HR 스택 전반에 점차 통합되고 있으며, 그 가치는 조직 내 워크플로우 구성 및 거버넌스에 좌우되기 때문에 재설계 작업의 시급성이 더욱 커지고 있습니다. 2026년에는 HR 워크플로우에 전용 AI 에이전트가 도입됨에 따라, 이와 유사한 방향성이 대두되었습니다. 이로 인해, 자동화를 대규모로 안정적으로 운영하기 전에 기업이 승인 로직, 에스컬레이션 규칙 및 역할 정의를 재검토할 필요성이 더욱 커지고 있습니다. 그 결과, HR 혁신 서비스 시장에서는 개별적인 기술 업데이트 작업보다 아키텍처 전체에 대한 재설계에 대한 수요가 높아지고 있습니다.

클라우드 기반 HR 혁신 로드맵의 도입 확대

많은 조직이 클라우드 기반 HCM을 급여 계산, 인재 관리, 입사 절차, 근무 일정 관리 및 인력 계획의 기반으로 삼게 되면서, 클라우드 도입은 계속해서 HR 혁신 서비스 시장을 뒷받침하고 있습니다. 도입 초기 단계에서는 기존의 HR 프로세스를 그대로 따르는 표준적인 구성에 의존하는 경우가 많았기 때문에 최적화, 통합, 거버넌스 업무를 위해 다시 공급업체에 의뢰하는 고객사가 증가하고 있습니다. 한 대형 클라우드 HCM 플랫폼은 13,000개 고객사에 걸쳐 1억 4,000만 명 이상의 사용자에게 서비스를 제공하고 있으며, 2026년 상반기에는 825건의 신규 시스템 가동이 완료되었습니다. 이는 여전히 지속적인 재설계 및 도입 서비스가 필요한 대규모 도입 기반이 존재함을 보여줍니다. 또한, 최근 플랫폼 출시를 통해 제품군 전반에 걸친 AI 통합, 워크플로우의 표준화, 기술 거버넌스가 강화되면서 서비스 제공 범위가 초기 플랫폼 도입 당시를 훨씬 뛰어넘어 확대되고 있습니다. 자율형 엔터프라이즈 기능으로의 광범위한 전환에 따라, 급여 계산, 채용, 온보딩, 인력 계획과 같은 인사 워크플로는 내장형 어시스턴트와 더욱 긴밀하게 연동되게 되었지만, 여전히 설정 및 변경과 관련된 지원이 필요합니다. 이 '클라우드 도입 → 최적화' 순환 구조는 성숙한 지역과 고성장 지역 모두에서 인사 혁신 서비스 시장을 향한 지속적인 수요 파이프라인을 창출하고 있습니다.

기존 인사 조직에서 발생하는 막대한 변경 관리 부담

HR 혁신 서비스 시장은 여전히 기존 HR 팀의 저항에 직면해 있습니다. 그 이유는 많은 프로그램이 역할, 승인 경로, 서비스 경계 및 책임 모델을 동시에 변경하기 때문입니다. 따라서 경영진이 디지털 도구나 AI를 활용한 업무 프로세스의 필요성에 동의하고 있더라도, 변화는 어려워집니다. 2026년 디지털화 관련 조사에 따르면, 시간적 제약과 도입의 복잡성이 여전히 기업들에게 큰 장벽으로 작용하고 있는 것으로 나타났으며, 이는 HR 재설계 프로그램의 진행을 지연시키는 실행상의 부담과 밀접한 관련이 있습니다. 다국적 기업의 경우, 정책의 일원화, 급여 계산의 일관성 확보, 직원 데이터 거버넌스를 관할 구역을 넘나들며 조율하여 진행해야 하기 때문에 이 문제가 더욱 심각해지는 경우가 많습니다. 2026년에 시행된, 여러 클라우드 HCM 모듈을 활용해 유럽과 미국 전역의 인사 환경을 현대화한 프로젝트는 운영 및 도입에 따른 부담이 얼마나 광범위하게 미칠 수 있는지를 보여줍니다. 따라서 전략적 필요성이 이미 명확한 경우라 하더라도, 인사 혁신 서비스 시장에서는 판매 주기가 길어지고 납기일이 지연될 가능성이 있습니다.

부문별 분석

2025년, HR 프로세스 혁신 및 재설계는 HR 혁신 서비스 시장의 28.37%를 차지했으며, 워크플로우 재설계가 여전히 기업의 구매 결정에서 핵심적인 위치를 차지하고 있음을 여실히 보여주고 있습니다. 이러한 주도적인 지위는 명확한 지출 순서를 반영하고 있습니다. 많은 고객사는 자동화나 고급 분석에 더 많은 투자를 하기 전에, 프로세스 논리, 서비스 계층 및 업무 인계 절차를 수정하고자 하기 때문입니다. 기존 워크플로우에 클라우드 기반 HCM을 도입한 조직의 경우, 대개 얻을 수 있는 이점이 제한적이기 때문에 HR 혁신 서비스 시장 내에서는 워크플로우 재설계에 이어 두 번째로 많은 예산이 배정되고 있습니다. 또한, 많은 기업이 이전의 전환 프로그램에 이어 플랫폼 통합, 연동 개선, 설정 최적화를 추진하고 있는 만큼, HR 기술 혁신 서비스도 중요한 역할을 하고 있습니다.

'인력 분석 및 HR 데이터 전환'은 2031년까지 연평균 성장률(CAGR) 11.62%로 확대될 것으로 예측되며, HR 혁신 서비스 시장에서 가장 빠르게 성장하는 서비스 부문이 될 전망입니다. 이 분야의 성장은 단계적으로 진행되고 있습니다. 클라이언트는 먼저 데이터 소스를 통합하고, 다음으로 거버넌스를 개선한 뒤, 실용적인 계획 모델을 구축하고, 마지막으로 이러한 인사이트를 관리자의 워크플로우에 반영해야 하기 때문입니다. 최근 동향에 따르면, 인력 계획을 비즈니스 및 재무적 요구 사항과 더욱 긴밀하게 연계함으로써 이러한 추세를 뒷받침하고 있으며, 그 결과 기술, 데이터, 운영 설계를 아우를 수 있는 서비스 제공업체에 대한 수요가 증가하고 있습니다. '인사 공유 서비스 및 아웃소싱의 혁신'은 대부분의 경우 초기 재설계 프로그램을 거친 후, 공유 서비스 센터를 통해 서비스 제공을 표준화한 대기업을 대상으로 계속해서 제공되고 있습니다. '인사 운영 모델 및 조직 설계'의 현재 지출 규모는 여전히 작지만, 기업의 구매 담당자들이 AI를 활용한 인사 업무 프로세스를 확대하기 전에 보다 견고한 청사진을 요구하게 됨에 따라 그 중요성이 커지고 있습니다. 따라서 인사 혁신 서비스 업계는 일회성 플랫폼 도입에만 의존하는 것이 아니라, 기반이 되는 재설계와 데이터 중심의 현대화를 결합한 방향으로 전환하고 있습니다.

지역별 분석

2025년, 북미는 HR 혁신 서비스 시장 점유율의 38.29%를 차지했으며, 지역별로는 가장 큰 기여도를 보였습니다. 이 지역은 대기업 구매처가 고도로 집중되어 있고, 성숙한 컨설팅 및 IT 서비스 체계가 갖춰져 있으며, 기업의 HR 기능 전반에 걸쳐 클라우드 HCM이 광범위하게 도입되어 있다는 장점을 갖추고 있습니다. 미국은 여전히 수요의 핵심을 차지하고 있는데, 이는 대기업들이 AI 도입을 HR 워크플로우, 데이터 모델, 거버넌스의 실질적인 재설계와 연계하려고 하기 때문입니다. 캐나다는 다국적 기업의 프로그램과의 지역적 협력을 통해 수요를 확대하고 있는 반면, 멕시코는 북미의 각 사업 지역에서 니어쇼어 서비스 제공과 정책 조정이 일반화됨에 따라 그 중요성이 커지고 있습니다. 이러한 요인들로 인해 북미의 HR 혁신 서비스 시장은 초기 재설계 프로젝트부터 그 이후의 최적화 작업에 이르기까지 계속해서 호황을 누리고 있습니다.

유럽에서는 다국적 기업 전반에 걸쳐 규정 준수 의무와 프로세스 표준화에 대한 수요가 여전히 높기 때문에 인사 혁신 서비스에 대한 안정적인 수요가 지속되고 있습니다. 또한, 이 지역은 기존의 인사 체계와 복잡한 도입 환경으로 인해 큰 부담을 안고 있으며, 독일 DIHK가 2026년에 실시한 조사에 따르면, 시간적 제약과 도입의 복잡성이 여전히 비즈니스 디지털화의 주요 장벽으로 작용하고 있는 것으로 나타났습니다. 이러한 과제로 인해, 단순한 기술 도입뿐만 아니라 재설계, 거버넌스 및 변경 관리를 종합적으로 제공할 수 있는 공급자에 대한 수요가 증가하고 있습니다. 남미에서는 여전히 규모가 작은 편이지만, 브라질 및 기타 다국적 기업의 사업 거점에서는 기업의 디지털 전환 및 현지 노동 규정 준수 요건과 관련된 업무가 서서히 증가하기 시작하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 14.26%로 확대될 것으로 예측되며, HR 혁신 서비스 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 인도는 주요 견인 역할을 하고 있으며, 노동력의 정규화, 디지털 공공 인프라, 세계 역량 센터의 확대를 통해 공유 서비스의 재설계, 급여 계산의 표준화, 그리고 분석 지원에 대한 수요가 발생하고 있습니다. 컨퍼런스 보드는 2026년 보고서에서 아시아태평양의 CEO들이 성장, 리스크 및 운영 모델을 재검토하고 있으며, 이에 따라 인사 혁신이 단순한 운영상의 과제를 넘어 보다 광범위한 비즈니스 과제로 자리매김했다고 지적했습니다. 일본, 중국, 한국 및 아세안 시장에서도 기업들이 노동력 모델의 현대화를 추진하고 국경을 초월한 협력을 강화해 나가는 가운데, 수년에 걸친 프로젝트 파이프라인이 구축되고 있습니다. 중동은 사우디아라비아와 아랍에미리트(UAE)의 국가 차원 노동력 개발 프로그램을 통해 성장을 이어가고 있는 반면, 아프리카는 남아프리카공화국과 나이지리아 등 시장에서 노동력의 정규화와 기술 부문의 성장에 힘입어 여전히 초기 단계의 기회를 제공합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the HR transformation services market size is expected to increase from USD 21.37 billion in 2025 to USD 23.12 billion in 2026 and reach USD 36.29 billion by 2031, growing at a CAGR of 9.44% over 2026-2031.

This report is Segmented by Service Type (HR Operating Model and Organizational Design, and More), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa), The Market Forecasts are Provided in Terms of Value (USD).

Global HR Transformation Services Market Trends and Insights

Growing Enterprise Demand for End-To-End HR Operating Model Redesign

End-to-end redesign has moved to the front of spending plans in the HR transformation services market because enterprises now see that new tools alone do not change outcomes. Many organizations still maintain HR structures built for control, approvals, and administrative consistency rather than for speed, analytics, and AI-supported decision-making. That is pushing clients toward programs that cover process ownership, service delivery layers, workflow automation, decision rights, and manager self-service within a single scope rather than in isolated projects. Recent product developments show that AI capabilities are being embedded across the HR stack, making redesign work more urgent because value depends on how workflows are configured and governed within the organization. A similar direction emerged in 2026 with the introduction of specialized AI agents into HR workflows, which further raises the need for enterprises to rethink approval logic, escalation rules, and role definitions before automation can work reliably at scale. As a result, the HR transformation services market is seeing stronger demand for full architecture redesign than for isolated technology refresh work.

Rising Adoption of Cloud-Based HR Transformation Roadmaps

Cloud adoption continues to support the HR transformation services market, as many organizations now treat cloud HCM as the foundation for payroll, talent, onboarding, scheduling, and workforce planning. The first wave of deployments often relied on standard configurations that mirrored older HR processes, so a growing number of clients are returning to providers for optimization, integration, and governance work. More than 140 million users across 13,000 customers were served by a major cloud HCM platform, with 825 new go-lives completed in the first half of 2026, indicating a large installed base that still requires ongoing redesign and adoption services. Recent platform releases also strengthened suite-wide AI integration, unified workflows, and skills governance, extending the service tail well beyond initial platform deployment. A broader move toward autonomous enterprise capabilities further connected HR workflows such as payroll, recruiting, onboarding, and workforce planning with embedded assistants that still require configuration and change support. This cloud-then-optimize cycle is creating a durable pipeline for the HR transformation services market in both mature and high-growth regions.

High Change-Management Burden Across Legacy HR Organizations

The HR transformation services market still faces resistance from legacy HR teams because many programs change roles, approval paths, service boundaries, and accountability models simultaneously. That makes transformation difficult even when leadership agrees with the need for digital tools and AI-enabled workflows. A 2026 digitalization survey found that time constraints and implementation complexity remained major barriers for enterprises, which aligns closely with the execution burden that slows HR redesign programs. The issue is often greater in multinational organizations because policy harmonization, payroll alignment, and employee data governance must move in step across jurisdictions. A 2026 engagement that modernized an HR landscape across Europe and the United States using multiple cloud HCM modules illustrates how broad the operating and adoption burden can become. Because of this, the HR transformation services market can see long sales cycles and extended delivery timelines even when the strategic need is already clear.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Data-Driven Workforce Planning And HR Analytics

- Increased Pressure to Improve Employee Experience and Workforce Agility

- Difficulty Quantifying Near-Term ROI from Transformation Programs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

HR Process Transformation and Reengineering accounted for 28.37% of the HR transformation services market in 2025, underscoring that workflow redesign remains central to enterprise buying decisions. This leadership reflects a clear spending sequence, as many clients want to fix process logic, service layers, and handoffs before investing more deeply in automation and advanced analytics. Organizations that move cloud HCM onto older workflows often see only limited gains, so redesign work continues to attract the largest budgets inside the HR transformation services market. HR Technology Transformation Services also plays a major role, as many enterprises are now consolidating platforms, improving integrations, and refining configurations following earlier migration programs.

Workforce Analytics and HR Data Transformation is projected to expand at an 11.62% CAGR through 2031, making it the fastest-growing service category in the HR transformation services market. Growth here is building in phases because clients first need to unify data sources, then improve governance, then create usable planning models, and then embed those insights into manager workflows. Recent product developments support this pattern by linking workforce planning more closely with business and financial needs, which increases the need for providers that can bridge technology, data, and operating design. HR Shared Services and Outsourcing Transformation continues to serve large organizations that are standardizing delivery through shared services centers, often after an initial redesign program. HR Operating Model and Organizational Design remains smaller by current spend, but it is gaining weight as enterprise buyers look for a stronger blueprint before they scale AI-enabled HR workflows. The HR transformation services industry is therefore shifting toward a mix of foundational redesign and data-centered modernization rather than relying solely on one-time platform implementation.

Complete Report Scope:

- By Service Type

- HR Operating Model and Organizational Design

- HR Process Transformation and Reengineering

- HR Technology Transformation Services

- HR Shared Services and Outsourcing Transformation

- Workforce Analytics and HR Data Transformation

- By Enterprise Size

- Large Enterprises

- Small And Medium Enterprises

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Information Technology and Telecom

- Retail and E-commerce

- Industrial Manufacturing

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 38.29% of the HR transformation services market share in 2025, making it the largest regional contributor. The region benefits from a high concentration of large enterprise buyers, mature consulting and IT services capacity, and wide adoption of cloud HCM across corporate HR functions. The United States remains the core demand engine because large employers are trying to align AI ambitions with practical redesign of HR workflows, data models, and governance. Canada adds volume through regional alignment with multinational programs, while Mexico is gaining relevance as nearshore delivery and policy coordination across North American operating zones become more common. These factors keep the HR transformation services market active in North America across both initial redesign mandates and follow-on optimization work.

Europe continues to generate steady demand for HR transformation services as compliance obligations and process standardization needs remain high across multinational employers. The region also carries a significant burden from older HR structures and complex implementation environments, and Germany's 2026 DIHK survey showed that time constraints and implementation complexity were still major barriers to business digitalization. That friction supports demand for providers that can combine redesign, governance, and change management rather than technology deployment alone. South America is still smaller in scale, but Brazil and other multinational operating hubs are starting to generate incremental work tied to enterprise digitalization and local labor compliance requirements.

Asia-Pacific is projected to expand at a 14.26% CAGR through 2031, making it the fastest-growing region in the HR transformation services market. India is a major driver because workforce formalization, digital public infrastructure, and growth in global capability centers are creating demand for shared services redesign, payroll standardization, and analytics support. The Conference Board reported in 2026 that CEOs across Asia-Pacific were reassessing growth, risk, and operating models, which elevated HR transformation from an operational issue to a broader business agenda. Japan, China, South Korea, and ASEAN markets are also building multi-year pipelines as companies modernize workforce models and seek better cross-border coordination. The Middle East is growing through national workforce development programs in Saudi Arabia and the UAE, while Africa remains an earlier-stage opportunity, led by formalization and technology-sector growth in markets such as South Africa and Nigeria.

- Aon plc

- Automatic Data Processing, Inc.

- Buck Global, LLC

- Capgemini SE

- Deloitte Touche Tohmatsu Limited

- International Business Machines Corporation

- KPMG International Limited

- Mercer LLC

- SD Worx

- NGA Human Resources

- NTT DATA Group Corporation

- Strada

- Oracle Corporation

- PricewaterhouseCoopers International Limited

- Genpact

- SAP SE

- Tata Consultancy Services Limited

- Wipro Limited

- Willis Towers Watson Public Limited Company

- Zalaris ASA

- HCL Technologies Limited

- Alight, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Enterprise Demand For End-To-End HR Operating Model Redesign

- 4.2.2 Rising Adoption Of Cloud-Based HR Transformation Roadmaps

- 4.2.3 Need To Standardize Global HR Policies Across Distributed Workforces

- 4.2.4 Increased Pressure To Improve Employee Experience And Workforce Agility

- 4.2.5 Expansion Of Data-Driven Workforce Planning And HR Analytics

- 4.2.6 Accelerating Compliance Needs For Multi-Country Labor And Privacy Regulations

- 4.3 Market Restraints

- 4.3.1 High Change-Management Burden Across Legacy HR Organizations

- 4.3.2 Difficulty Quantifying Near-Term ROI From Transformation Programs

- 4.3.3 Talent Shortage In HR Process Redesign And Change Advisory Skills

- 4.3.4 Fragmented Legacy HR Systems And Data Migration Complexity

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat Of New Entrants

- 4.8.2 Bargaining Power Of Suppliers

- 4.8.3 Bargaining Power Of Buyers

- 4.8.4 Threat Of Substitutes

- 4.8.5 Intensity of Comptetive Rivalary

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 HR Operating Model and Organizational Design

- 5.1.2 HR Process Transformation and Reengineering

- 5.1.3 HR Technology Transformation Services

- 5.1.4 HR Shared Services and Outsourcing Transformation

- 5.1.5 Workforce Analytics and HR Data Transformation

- 5.2 By Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small And Medium Enterprises

- 5.3 By End-user Industry

- 5.3.1 BFSI

- 5.3.2 Healthcare and Life Sciences

- 5.3.3 Information Technology and Telecom

- 5.3.4 Retail and E-commerce

- 5.3.5 Industrial Manufacturing

- 5.3.6 Government and Public Sector

- 5.3.7 Other End-user Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Netherlands

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Aon plc

- 6.4.2 Automatic Data Processing, Inc.

- 6.4.3 Buck Global, LLC

- 6.4.4 Capgemini SE

- 6.4.5 Deloitte Touche Tohmatsu Limited

- 6.4.6 International Business Machines Corporation

- 6.4.7 KPMG International Limited

- 6.4.8 Mercer LLC

- 6.4.9 SD Worx

- 6.4.10 NGA Human Resources

- 6.4.11 NTT DATA Group Corporation

- 6.4.12 Strada

- 6.4.13 Oracle Corporation

- 6.4.14 PricewaterhouseCoopers International Limited

- 6.4.15 Genpact

- 6.4.16 SAP SE

- 6.4.17 Tata Consultancy Services Limited

- 6.4.18 Wipro Limited

- 6.4.19 Willis Towers Watson Public Limited Company

- 6.4.20 Zalaris ASA

- 6.4.21 HCL Technologies Limited

- 6.4.22 Alight, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment