|

시장보고서

상품코드

2072714

미국의 3PL 창고 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States 3PL Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

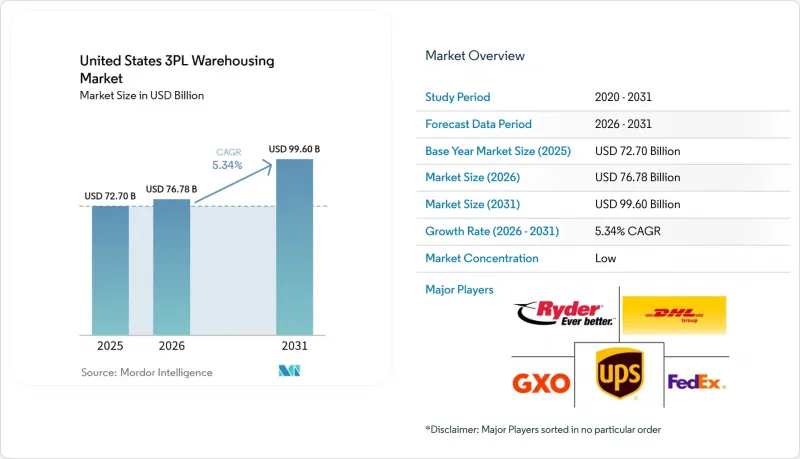

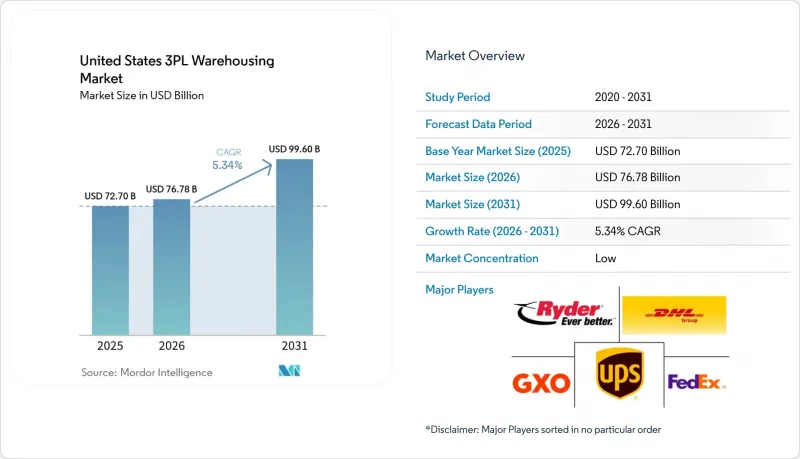

Mordor Intelligence에 의하면, 미국의 3PL 창고 시장 규모는 2025년에 727억 달러로 평가되었고, 2026년 767억 8,000만 달러로 추정되고, 2031년까지 996억 달러에 이를 것으로 예측되며, 2026-2031년 예측 기간 CAGR은 5.34%를 나타낼 전망입니다.

미국의 3PL 창고 시장이 확대되고 있는 배경에는 화주들이 고정자산인 창고를 관세 변동이나 조달 경로 변경, 나아가 더욱 신속한 주문 처리(fulfillment)에 대한 기대에 대응할 수 있는 변동비형 계약으로 전환하고 있기 때문입니다. 본 보고서는 서비스 유형별(보관, 물류, 부가가치 서비스), 창고 유형별(일반 공유형, 전용 계약형, 보세창고), 온도 관리별(비온도 관리, 온도 관리), 기술 도입 현황별(수동, 반자동, 완전 자동), 그리고 최종 사용자별(제조업, 소비재 등)로 분류되어 있습니다. 시장 전망은 금액 기준으로 제시되어 있습니다.

미국의 3PL 창고 시장 동향 및 인사이트

팬데믹 이후 전자상거래 물류 붐의 현황

제3자 물류 서비스는 이제 일상적인 운영 모델로 자리 잡았으며, 브랜드의 84%가 적어도 일부 주문에 대해 제3자 물류 업체를 이용하고 있고, 44.0%는 2026년까지 물류 센터 수를 늘릴 계획입니다. 팬데믹 기간 동안 나타났던 보관 수요의 급증은 다소 진정세를 보였지만, 옴니채널 대응, 브랜드 포장, 키트 구성, 반품 처리 등 모든 분야에서 창고 내 작업 공정이 늘어나면서 주문이 복잡해짐에 따라 수요는 여전히 견조한 추세를 보이고 있습니다. 이러한 변화로 인해, 단일 대형 물류 센터뿐만 아니라 여러 거점을 관리할 수 있는 3PL 사업자가 유리한 입장에 있습니다. 또한, 섹션 321의 데미니스(미량) 면제 폐지로 인해, 크로스보더 전자상거래 사업자들은 미국 내에 추가적인 물류 거점을 구축해야 하는 상황에 직면해 있습니다. 75% 이상의 브랜드가 2026년에 최소 한 개의 새로운 판매 채널을 추가할 계획이며, 이는 모든 채널에서 재고 배치 및 주문 조정에 대한 요구가 더욱 높아질 것임을 의미합니다. 그 결과, 미국의 3PL 창고 시장에서는 단순한 기본 보관 업무보다 서비스 집약형 업무를 통해 얻는 수익이 증가하고 있습니다.

미국 공급망의 니어쇼어링과 리쇼어링

니어쇼어링은 두 가지 연쇄적인 단계를 통해 창고 수요를 증가시키고 있습니다. 우선, 화물은 국경에서 환적과 보세 창고 용량이 필요하며, 그 후 내륙의 완충 재고 및 지역 배송 공간으로 이동합니다. 쿠네 앤 나겔(Kune & Nagel)사의 엘파소 보세창고는 개장 후 1년 만에 수용 한도에 도달했으며, 이에 따라 이 회사는 2025년 11월, 인접한 새로운 부지를 활용해 창고 규모를 60% 확장할 것이라고 발표했습니다. 이 사례는 내륙 지역의 창고 네트워크가 완전히 정비되기 전에 국경 지역 시장이 얼마나 긴박한 상황인지 보여줍니다. 제조업체가 북미에 생산 거점을 구축하기로 결정하면, 공급 차질이나 운임 변동으로부터 대비하기 위해 보다 안정적인 창고 체계도 필요해집니다. 이로 인해 남서부 및 중서부 일부 회랑 지역에 위치한 전용·보세·고준수 시설이 유리한 입지를 확보하게 됩니다. 따라서 미국의 3PL 창고 시장은 무역 경로의 변화뿐만 아니라, 이러한 조달 결정에 따른 장기적인 사업 주기로부터도 혜택을 받고 있습니다.

심각한 인력 부족과 임금 인플레이션

전국 물류 거점 전반에 걸쳐 구인 건수가 여전히 높은 수준을 유지하고 있어, 인력은 창고의 생산 능력에 대한 직접적인 제약 요인으로 남아 있습니다. 최신 JOLTS(구인 및 이직 통계) 발표에 따르면, 2026년 3월 운송, 창고, 유틸리티 분야의 구인 건수는 80만 건을 넘어섰습니다. 2026년 초까지 운송·창고 업계의 보수 수준이 계속 상승함에 따라, 임금 인상이 이 문제를 더욱 심각하게 만들고 있습니다. 높은 이직률은 이 문제의 해결을 더욱 어렵게 만들고 있습니다. 사업자는 생산성을 안정적으로 유지하는 대신, 직원들의 연수나 재교육에 많은 시간을 할애할 수밖에 없기 때문입니다. 자동화를 통해 일부 부담은 완화되겠지만, 보다 고도화된 기술 시스템을 운영·지원할 수 있는 근로자에 대한 수요도 높아질 것입니다. 따라서 인력은 미국 3PL 창고 운영 시장에서 단기적으로 가장 뚜렷한 제약 요인 중 하나로 남아 있습니다.

부문별 분석

2025년, 보관 서비스는 미국 3PL 창고 운영 시장의 46.81%를 차지했으며, 팔레트 및 재고 수용 능력이 여전히 이 시장의 기반을 형성하고 있는 것으로 나타났습니다. 이러한 높은 시장 점유율이 꾸준히 유지되고 있는 이유는 많은 화주들이 관세 변경, 리드타임 변동, 조달 경로 재편으로 인한 위험을 완화하기 위해 국내 완충 재고를 더 많이 보유하고 있기 때문입니다. 또한, 다중 채널 재고 풀을 운영하는 소매업체나 제조업체에게 있어 유통 및 재고 관리 역시 여전히 중요한 역할을 하고 있습니다. 그렇긴 하지만, 성장 추세는 단순한 보관 계약보다는 노동 집약적인 서비스 쪽으로 이동하고 있습니다. 부가가치 서비스 및 키팅, 라벨링, 재포장, 반품 처리 등을 포함한 기타 서비스는 2031년까지 연평균 성장률(CAGR) 8.18%로 확대될 것으로 전망됩니다.

이러한 급속한 성장은 풀필먼트 파트너에게 동일한 창고 공간 내에서 더 많은 공정을 맡아 주기를 바라는 고객층 증가를 반영하고 있습니다. ShipBob의 보고서에 따르면, 각 브랜드는 판매 채널의 수와 주문 처리의 복잡성을 늘리고 있으며, 이로 인해 총 보관 수요 증가세가 둔화되고 있음에도 불구하고 고객사당 수익은 증가하고 있습니다. 이에 따라 가격 협상 방식도 변화하고 있습니다. 계약 내용은 단순한 보관 요금에서 작업 횟수, 취급 규칙, 서비스 보증에 연동된 요금 체계로 점차 전환되고 있기 때문입니다. 켄코(Kenco)와 그레이오렌지(GreyOrange) 간의 5년에 걸친 제휴는 중견 물류 사업자가 오케스트레이션 소프트웨어와 로봇 기술을 활용하여 풀필먼트 센터 전반에 걸쳐 이러한 고부가가치 업무를 확대하고 있는 실제 사례를 보여줍니다. 미국의 3PL 창고 업계에서 이러한 서비스 구성의 변화는 노동 관리를 철저히 하면서도 업무 흐름의 자동화를 동시에 실현할 수 있는 운영사의 이익률을 뒷받침하고 있습니다.

2025년, 미국의 3PL 창고 운영 시장에서 일반적인 공유형 또는 다중 고객형 창고가 49.32%의 점유율을 차지했습니다. 이는 2024년에 나타난 재고 변동을 겪었음에도 불구하고, 유연성이 여전히 높은 가치를 지니고 있음을 입증하고 있습니다. 많은 화주들은 전용 시설에 자본을 묶어두지 않고도 공간을 확대하거나 축소할 수 있기 때문에 계속해서 공유형 창고를 선호하고 있습니다. 이러한 형태는 지역적 서비스 범위가 필요한 경우나, 아직 단일 운영 모델에 특화된 시설을 원하지 않는 임차인에게도 적합합니다. 한편, 전용 계약 창고는 2031년까지 연평균 7.35%의 성장률이 예상되며, 이는 다른 어떤 창고 형태보다 빠른 속도입니다. 이러한 급속한 성장은 주로 대형 제조업체나 규제 대상 화주와 같은 다양한 고객층을 반영한 것으로, 이들은 보다 안정적인 공급망 체계를 구축하는 시점에 확실한 운송 능력을 확보하고자 합니다.

이 두 가지 형태의 분화는 시장이 두 가지 유형의 리스크 관리를 동시에 충족하고 있음을 보여줍니다. 공유 공간은 처리량이 변동할 때 고객이 유연성을 유지하는 데 도움이 되는 반면, 전용 공간은 수요가 더 예측 가능해질 때 용량 부족이나 가격 급등으로부터 고객을 보호합니다. 또한, 수입업체들이 관세 납부를 유예하거나 수입품 관련 정책의 불확실성을 관리할 방법을 모색함에 따라 보세창고의 중요성도 커지고 있습니다. 2025년 초에 문을 연 오하이오주 콜럼버스 근교에 위치한 DSV의 120만 제곱피트 규모의 멀티클라이언트 시설은 설계가 적절하다면 단일 자산으로도 고사양 산업 사용자 및 전자상거래 입주자 모두에게 서비스를 제공할 수 있음을 보여줍니다. 미국의 3PL 창고 운영 시장에서 창고 유형의 선택은 각 화주가 어느 정도의 유연성, 규정 준수 및 비용 가시성을 필요로 하는지에 점점 더 좌우되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.07.03According to Mordor Intelligence, the united states 3PL warehousing market size was valued at USD 72.70 billion in 2025 and estimated to grow from USD 76.78 billion in 2026 to reach USD 99.60 billion by 2031, at a CAGR of 5.34% during the forecast period 2026-2031.

The United States 3PL warehousing market is expanding because shippers are moving fixed warehouse assets into variable-cost contracts that can absorb tariff swings, changing sourcing routes, and faster fulfillment expectations. This report is Segmented by Service Type (Storage, Distribution, Value-Added Services), by Warehouse Type (General Shared, Dedicated Contract, Bonded), by Temperature Control (Non-Temperature Controlled, Temperature Controlled), by Technology Adoption (Manual, Semi-Automated, Fully Automated), and by End User (Manufacturing, Consumer Goods, and More). The Market Forecasts are Provided in Terms of Value.

United States 3PL Warehousing Market Trends and Insights

E-Commerce Fulfillment Boom Post-Pandemic Baseline

Third-party fulfillment is now embedded in everyday operating models, with 84% of brands using a third-party fulfillment company for at least some orders, and 44.0% planning to increase their number of fulfillment centers in 2026. The storage surge seen during the pandemic period has matured, but order complexity has kept demand firm because omnichannel compliance, branded packaging, kitting, and returns work all require more warehouse touches. That shift favors 3PL operators that can manage multiple sites rather than only a single large distribution center. The removal of the Section 321 de minimis exemption is also pushing cross-border e-commerce sellers to establish more domestic fulfillment footprints in the United States. More than 75% of brands plan to add at least 1 new sales channel in 2026, which means inventory placement and order orchestration become more demanding across every channel. As a result, the United States 3PL warehousing market is gaining more revenue from service intensity than from basic storage alone.

Nearshoring and Reshoring of the United States Supply Chains

Nearshoring is increasing warehouse demand in 2 linked steps, with freight first needing border transload and bonded capacity, and then moving into inland buffer stock and regional distribution space. Kuehne+Nagel's El Paso bonded warehouse reached full capacity within 1 year of opening, which led the company to announce a 60% expansion through a new adjacent site in November 2025. That example shows how border markets are tightening before inland warehouse networks have fully adjusted. Once manufacturers commit to North American production footprints, they also need more stable warehouse arrangements to protect against supply interruptions and rate volatility. This favors dedicated, bonded, and high-compliance facilities in the Southwest and selected Midwest corridors. The United States 3PL warehousing market is therefore benefiting not only from trade rerouting, but also from the longer operating cycles that follow those sourcing decisions.

Acute Labor Shortages and Wage Inflation

Labor remains a direct limit on warehouse output because open positions are still elevated across the national logistics base. The latest JOLTS release showed more than 800,000 job openings in transportation, warehousing, and utilities in March 2026. Wage growth is compounding the issue, since transportation and warehousing compensation continued to rise through early 2026. High turnover makes the problem harder to solve because operators spend more time training and retraining staff instead of stabilizing productivity. Automation can ease some of the pressure, but it also increases the need for workers who can operate and support more technical systems. For that reason, labor remains one of the clearest near-term limits on the United States 3PL warehousing market.

Other drivers and restraints analyzed in the detailed report include:

- Cold-Chain Expansion for Food and Pharma

- Warehouse Automation and Robotics Cost Advantages

- Urban-Core Land Scarcity and Zoning Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Storage accounted for 46.81% of the United States 3PL warehousing market in 2025, indicating that pallet and inventory capacity still form the basis of this market. That large share has remained resilient because many shippers are holding more domestic buffer stock to reduce exposure to tariff changes, lead-time volatility, and sourcing realignment. Distribution and inventory management also remain important for retailers and manufacturers running multi-channel inventory pools. Even so, the growth pattern has moved toward more labor-intensive services rather than pure storage contracts. Value-added services and others, including kitting, labeling, repackaging, and returns handling, are projected to expand at an 8.18% CAGR through 2031.

This faster growth reflects a customer mix that wants fulfillment partners to absorb more process steps inside the same warehouse footprint. ShipBob reported that brands are increasing channel counts and fulfillment complexity, which supports higher revenue per client even as total storage demand grows more slowly. That changes pricing discussions, because contracts move away from a narrow storage rate and toward charges tied to touches, handling rules, and service commitments. Kenco's 5-year partnership with GreyOrange shows how mid-tier operators are using orchestration software and robotics to scale those higher-value activities across fulfillment centers. In the United States 3PL warehousing industry, this service mix shift supports margins for operators that can pair labor discipline with workflow automation.

General shared or multi-client warehousing held 49.32% of United States 3PL warehousing market share in 2025, which confirms that flexibility still carries strong value after the inventory swings seen in 2024. Many shippers continue to prefer shared capacity because it allows them to scale space up or down without tying capital to dedicated buildings. This format also suits tenants that need regional coverage but do not yet want a site built around a single operating model. At the same time, dedicated contract warehousing is projected to grow at 7.35% through 2031, which is faster than any other warehouse format. That faster growth reflects a different customer set, mainly larger manufacturers and regulated shippers that want assured capacity once they commit to a more stable supply chain footprint.

The split between these 2 formats shows that the market is serving 2 kinds of risk management at once. Shared space helps customers stay flexible during volume swings, while dedicated space protects them against capacity shortages and price spikes once demand becomes more predictable. Bonded warehousing has also gained relevance as importers look for ways to defer duties and manage policy uncertainty around inbound goods. DSV's 1.2 million-square-foot multi-client facility near Columbus, Ohio, which opened in early 2025, shows how a single asset can serve both high-spec industrial users and e-commerce tenants when the design is right. In the United States 3PL warehousing market, warehouse type selection increasingly depends on how much flexibility, compliance, and cost visibility each shipper needs.

Complete Report Scope:

- By Service Type

- Storage

- Distribution and Inventory Management

- Value-Added Services and Others (Kitting, Labeling)

- By Warehouse Type

- General Shared / Multi-client Warehousing

- Dedicated Contract Warehousing

- Bonded Warehousing

- By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- By Technology Adoption

- Manual

- Semi-automated

- Fully Automated

- By End User Industry

- Manufacturing

- Consumer Goods

- Food and Beverage

- Retail and E-commerce

- Healthcare and Pharma

- Other End-user Industries

- By Region

- Northeast

- Southeast

- Midwest

- Southwest

- West

List of Companies Covered in this Report:

- DHL Group

- GXO Logistics

- Ryder System, Inc.

- United Parcel Service of America, Inc. (UPS)

- FedEx

- XPO, Inc.

- Kuehne+Nagel

- DSV A/S (Including DB Schenker)

- GEODIS

- CMA CGM Group (Including CEVA Logistics)

- Penske Corporation

- Lineage, Inc.

- Americold

- NFI Industries

- Kenco Group

- CJ Logistics

- Saddle Creek Logistics Services

- OHL

- Buske Logistics

- Burris Logistics

- Weber Logistics

- Radial

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Commerce Fulfilment Boom (Post-Pandemic Baseline)

- 4.2.2 Nearshoring and Reshoring of the United States Supply Chains

- 4.2.3 Cold-Chain Expansion for Food and Pharma

- 4.2.4 Warehouse Automation and Robotics Cost Advantages

- 4.2.5 Institutional REIT Investment Expanding Capacity

- 4.2.6 State-Level Logistics Tax Incentives (SE and Midwest)

- 4.3 Market Restraints

- 4.3.1 Acute Labor Shortages and Wage Inflation

- 4.3.2 Urban-Core Land Scarcity and Zoning Hurdles

- 4.3.3 Rising Interest-Rate Driven Cap-Ex Squeeze

- 4.3.4 ESG Compliance Costs for Temperature-Controlled Sites

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Technology Innovations Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Rivalry Among Competitors

- 4.8 Evolution of Cold-Chain Warehousing Requirements

- 4.9 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Storage

- 5.1.2 Distribution and Inventory Management

- 5.1.3 Value-Added Services and Others (Kitting, Labeling)

- 5.2 By Warehouse Type

- 5.2.1 General Shared / Multi-client Warehousing

- 5.2.2 Dedicated Contract Warehousing

- 5.2.3 Bonded Warehousing

- 5.3 By Temperature Control

- 5.3.1 Non-Temperature Controlled

- 5.3.2 Temperature Controlled

- 5.4 By Technology Adoption

- 5.4.1 Manual

- 5.4.2 Semi-automated

- 5.4.3 Fully Automated

- 5.5 By End User Industry

- 5.5.1 Manufacturing

- 5.5.2 Consumer Goods

- 5.5.3 Food and Beverage

- 5.5.4 Retail and E-commerce

- 5.5.5 Healthcare and Pharma

- 5.5.6 Other End-user Industries

- 5.6 By Region

- 5.6.1 Northeast

- 5.6.2 Southeast

- 5.6.3 Midwest

- 5.6.4 Southwest

- 5.6.5 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 GXO Logistics

- 6.4.3 Ryder System, Inc.

- 6.4.4 United Parcel Service of America, Inc. (UPS)

- 6.4.5 FedEx

- 6.4.6 XPO, Inc.

- 6.4.7 Kuehne+Nagel

- 6.4.8 DSV A/S (Including DB Schenker)

- 6.4.9 GEODIS

- 6.4.10 CMA CGM Group (Including CEVA Logistics)

- 6.4.11 Penske Corporation

- 6.4.12 Lineage, Inc.

- 6.4.13 Americold

- 6.4.14 NFI Industries

- 6.4.15 Kenco Group

- 6.4.16 CJ Logistics

- 6.4.17 Saddle Creek Logistics Services

- 6.4.18 OHL

- 6.4.19 Buske Logistics

- 6.4.20 Burris Logistics

- 6.4.21 Weber Logistics

- 6.4.22 Radial

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment