|

시장보고서

상품코드

2072835

독일의 방위 물류 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Germany Defense Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

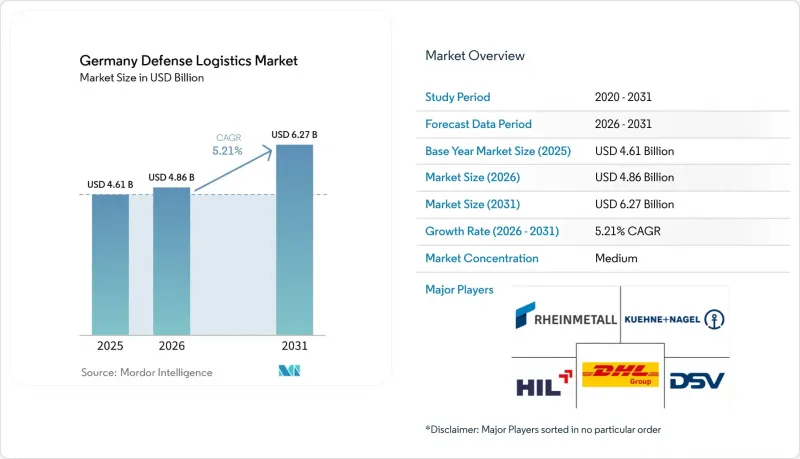

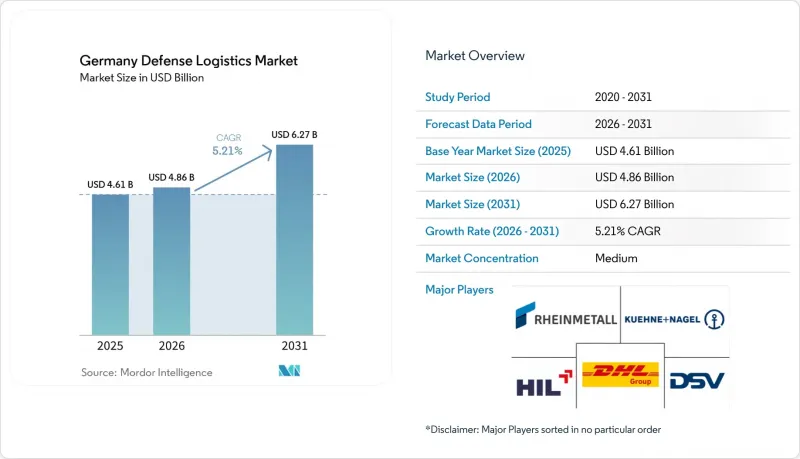

Mordor Intelligence에 의하면, 독일 방위 물류 시장 규모는 2025년 46억 1,000만 달러, 2026년 48억 6,000만 달러에서 2031년까지 62억 7,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 5.21%를 나타낼 전망입니다.

본 보고서는 서비스 유형별(무기, 부대 이동, 기술 지원 및 유지보수, 의료 지원·보건 서비스 등), 물류 기능별(수송, 창고·유통 등), 최종 사용자별(육군, 해군, 공군 등), 지역별(노르트라인-베스트팔렌주, 바이에른주, 바덴-뷔르템베르크주 등)로 분류되어 있습니다. 예측치는 금액(달러)으로 표시되어 있습니다.

독일 방위 물류 시장 동향과 인사이트

독일 연방군(Bundeswehr)의 1,000억 유로(1,160억 달러) 규모의 "존더펠모겐(Sondervermogen)"이 멀티모달 물류의 현대화를 가속화하고 있습니다.

독일의 국방 예산 구조는 현재 일반 예산과 특별 기금 두 가지 경로를 통해 운영되고 있으며, 이로 인해 독일 국방 물류 시장의 물류 수요 규모와 가시성이 크게 높아지고 있습니다. "존더펠모겐" 기금에서 지원되는 255억 유로(296억 달러)를 포함해, 2026년 국방 예산 총액 1,082억 유로(1,254억 달러)는 물류 계획이 더 이상 제한적인 갱신 주기가 아니라 지속적인 군사 준비 태세와 연계되어 있음을 보여주는 가장 명확한 징후입니다. 가장 강력한 신호 중 하나는 종합적인 기본협정에 따라 2,000대 이상의 RMMV HX 군용 수송 차량이 발주되었다는 점입니다. 이를 통해 연료, 탄약 및 공병 장비의 자체 수송 능력이 비약적으로 향상될 것입니다. 차량 구성이 중요한 이유는 중량급 기종이 단순한 국내 일상 수송뿐만 아니라 사전 배치 및 부대의 지속적인 지원을 뒷받침하는 역할을 수행하기 때문입니다. 2026년 1월부터 시행되는 연방 의회의 ““계획·조달 가속화법”또한, 방위 계약에서 기존에 존재하던 병목 현상을 해소함으로써 물류 인프라, 차량 지원 및 관련 서비스의 신속한 이행을 뒷받침합니다. 그 결과, 독일의 방위 물류 시장에서는 조달 물량을 수송 태세, 정비소 활동 및 정비 지원과 직접 연계하는 계약 건수가 더욱 견조하게 증가하고 있습니다.

나토(NATO)의 억지 요건에 따라 라인강 회랑을 따라 신속 전개용 비축 물자 확보를 추진

동맹의 계획 수립 과정에서 독일의 철도, 도로, 항만 및 집결지 인프라에 대한 의존도가 높아짐에 따라, 나토(NATO)의 물류 분야에서 독일의 역할은 더욱 핵심적인 위치를 차지하고 있습니다. ““OPLAN DEU”는 위기 발동 후 6개월 이내에 최대 80만 명의 동맹군 병력과 20만 대의 차량을 이동시키기 위한 거점으로 독일을 지정하고 있으며, 이에 따라 독일 방위 물류 시장에서 비축, 수송대 지원 및 수송 조정에 대한 기초적인 수요가 증가하고 있습니다. 이러한 수요는 국유 운송 능력에만 국한되는 것은 아닙니다. 왜냐하면 서비스 제공업체와 군사 계획 담당자 간의 추가적인 협력이 없다면, 민간 계약만으로는 이 정도 수요 급증을 감당할 수 없기 때문입니다. 라인메탈사가 2025년 2월에 체결한 부대 재배치 지원에 관한 기본 협정은 수송대 서비스, 숙박, 급식, 급유, 폐기물 관리와 같은 광범위한 물류 업무가 점점 더 대규모 계약으로 통합되고 있음을 보여줍니다. 이러한 변화로 인해, 단순한 화물 운송업체로서 경쟁하는 것이 아니라 현장 지원과 이동 서비스를 통합적으로 관리할 수 있는 사업자가 유리한 입장에 서게 됩니다. 따라서 독일의 국방 물류 시장은 군사 수송량 증가뿐만 아니라, 운영상의 책임이 통합된 물류 계약으로의 광범위한 전환을 통해서도 혜택을 보고 있습니다.

'푸마' 보병전투차의 개량 주기 지연으로 인해 창고 용량이 부족해짐

'푸마' 현대화 주기는 정비 공간과 예비 부품 처리 능력이 장기간 묶여 있는 상태이기 때문에 독일 방위 물류 시장에서 운영상의 유연성을 제한하고 있습니다. 297량의 푸마 차량을 S1 규격으로 업그레이드하는 작업은 2029년 완료를 목표로 하고 있으며, 다른 지상 시스템에도 지원이 필요함에도 불구하고 주요 정비 공장 및 작업장의 자원은 계속해서 이 작업에 배정된 상태입니다. 업그레이드 범위에는 미사일 통합, 센서 개량, 디지털 무선 장비 도입이 포함되어 있으며, 각 단계마다 시험 및 검수 작업이 추가됨에 따라 일반적인 처리 시간이 연장되고 있습니다. 2025년 12월에 체결된 푸마 200량 추가 도입에 관한 합의 역시, 가장 유능한 정비 팀이 이 플랫폼에 집중해야 하는 기간을 더욱 연장하게 될 것입니다. 이로 인해 독일 방위 물류 시장의 육군 부문 전반에서 차량 증강과 차량 지원이 동시에 증가함에 따라, 작업 순서 조정이라는 문제가 발생하고 있습니다. 민간 도급업체는 그러한 압박 중 일부를 흡수할 수는 있지만, 현재 거점 규모의 제약으로 인해 핵심 네트워크 외부로 이전할 수 있는 잉여 업무의 양에는 한계가 있습니다.

부문별 분석

2025년, 무기 부문은 매출의 41.07%를 차지하며 독일 방위 물류 시장에서 가장 큰 서비스 부문이 되었습니다. 이 부문은 엄격한 군사 규정 하에서 탄약 취급, 무기 관련 보관, 특수 운송, 조달 조정 및 문서 관리를 포괄하고 있기 때문에 여전히 핵심적인 수요원으로 자리 잡고 있습니다. 2026년 1월 딜 디펜스(Deal Defense)사와 BAAINBw가 체결한 IRIS-T 계약은 이러한 추세를 뒷받침하는 사례입니다. 미사일 생산 확대는 안전한 창고 보관, 체계적인 취급, 엄격하게 관리되는 공급망에 대한 수요를 직접적으로 증가시키기 때문입니다.

기술 지원 및 유지보수는 가장 빠르게 성장하고 있는 서비스 분야로, 이 부문은 2026년부터 2031년까지 연평균 성장률(CAGR) 8.05%로 확대될 것으로 전망됩니다. 이러한 성장은 차량 및 항공기 보유 대수 증가, 유지관리 주기의 장기화, 그리고 육상 및 항공 시스템 전반에 걸쳐 외부 위탁형 및 실적 연동형 지원 모델이 꾸준히 보급된 데 기인합니다. 롤스로이스 파워 시스템즈가 2026년 3월에 체결한 푸마 차량용 MTU 파워팩 약 200기 계약은 추진 시스템 관련 지원이 애프터마켓 사업에서 점점 더 큰 비중을 차지하고 있음을 보여줍니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액, 2026-2031년)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the germany defense logistics market size is projected to expand from USD 4.61 billion in 2025 and USD 4.86 billion in 2026 to USD 6.27 billion by 2031, registering a CAGR of 5.21% between 2026 to 2031.

This report is Segmented by Service Type (Armament, Troop Movement, Technical Support and Maintenance, Medical Aid & Health Services, and More), by Logistics Function (Transportation, Warehousing, and Distribution, and More), by End User (Army, Navy, Air Force, and More), and by Region (North Rhine-Westphalia, Bavaria, Baden-Wurttemberg, and More). The Forecasts are Provided in Terms of Value (USD).

Germany Defense Logistics Market Trends and Insights

Bundeswehr's EUR 100 Billion (USD 116.0 billion) Sondervermogen Accelerates Multi-Modal Logistics Modernization.

Germany's defense budget structure now works through both the regular budget and the special fund, which has materially increased the scale and visibility of logistics demand in Germany's defense logistics market. The combined 2026 defense budget of EUR 108.2 billion (USD 125.4 billion), including EUR 25.5 billion (USD 29.6 billion) from the Sondervermogen fund, is the clearest sign that logistics planning is now tied to sustained military readiness rather than limited replacement cycles. One of the strongest signals came from the call-off for more than 2,000 RMMV HX military transport vehicles under the broader framework agreement, which sharply lifts Germany's organic movement capacity for fuel, ammunition, and engineering equipment. The vehicle mix matters because the heavier variants support pre-positioning and force sustainment rather than just routine domestic movement. The Bundestag's accelerated planning and procurement law, effective from January 2026, also reduces earlier bottlenecks in defense contracting, thereby supporting faster execution of logistics infrastructure, fleet support, and related services. As a result, the Germany defense logistics market is seeing a stronger pipeline of contracts that link procurement volumes directly to transport readiness, depot activity, and maintenance support.

NATO Deterrence Requirements Drive Rapid-Deployment Stockpiles Along the Rhine Corridor

Germany's role inside NATO logistics has become more central as alliance planning increasingly depends on the country's rail, road, port, and staging infrastructure. OPLAN DEU identifies Germany as the hub for moving up to 800,000 allied troops and 200,000 vehicles within 6 months of crisis activation, thereby lifting baseline demand for stockpiling, convoy support, and transit coordination in the German defense logistics market. This demand is not limited to state-owned capacity because commercial contracts alone cannot absorb a surge of that scale without added integration across service providers and military planners. Rheinmetall's February 2025 framework agreement for force redeployment support shows how broader logistics tasks, such as convoy services, housing, catering, refueling, and waste management, are increasingly being bundled into larger contracts. That shift favors operators that can manage field support and movement services together rather than compete only as freight carriers. The Germany defense logistics market therefore benefits not only from higher military traffic volumes, but also from a wider transfer of operational responsibilities into integrated logistics contracts.

Slower Puma IFV Retrofit Cycle Ties Up Warehouse Capacity

The Puma modernization cycle is constraining operational flexibility in the Germany defense logistics market because maintenance space and spare parts handling capacity remain tied up for long periods. The S1-standard upgrade of 297 Puma vehicles has a completion target of 2029, ensuring key depot and workshop resources remain committed while other land systems also require support. The upgrade scope includes missile integration, improved sensors, and digital radio equipment, and each layer adds testing and acceptance work that extends normal throughput times. The December 2025 agreement for 200 additional Puma vehicles also lengthens the period during which the most capable maintenance cells remain heavily focused on this platform. This creates a sequencing problem because fleet expansion and fleet support are rising simultaneously across the Army portion of the Germany defense logistics market. Commercial contractors can absorb part of that pressure, but current footprints limit how much overflow work can move out of the core network.

Other drivers and restraints analyzed in the detailed report include:

- Digital-Twin Roll-Out for Military Depots Cuts Inventory Lead-Times

- Civil-Military Logistics Integration with DB Cargo Unlocks Rail Capacity

- Tight MoD Cyber-Security Rules Delay Third-Party Cloud Onboarding

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Armament accounted for 41.07% of revenue in 2025, making it the largest service segment in the German defense logistics market. This segment remains the core demand center because it covers munitions handling, weapons-related storage, specialized transport, procurement coordination, and documentation under strict military compliance rules. The January 2026 IRIS-T contracts signed by Diehl Defense and BAAINBw reinforce this pattern because missile production growth directly increases the need for secure warehousing, controlled handling, and tightly managed supply chains.

Technical support and maintenance is the fastest-growing service area, and the segment is projected to expand at 8.05% CAGR from 2026 to 2031. Growth comes from larger fleets, longer sustainment cycles, and the steady spread of outsourced or performance-linked support models across land and air systems. Rolls-Royce Power Systems' March 2026 contract for around 200 MTU Powerpacks for Puma vehicles shows how propulsion support is becoming a larger part of the aftermarket workload.

Complete Report Scope:

- By Service Type

- Armament

- Military Troops Movement Support

- Technical Support & Maintenance

- Medical Aid & Health Services

- Fire-fighting Protection

- Other Services

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing & Distribution

- Value-added Services (Labelling, Kitting, Consulting)

- Transportation

- By End User

- Army

- Navy

- Air Force

- Others

- By Region

- North Rhine-Westphalia

- Bavaria (Bayern)

- Baden-Wurttemberg

- Rest of States

List of Companies Covered in this Report:

- Rheinmetall AG

- HIL Heeresinstandsetzungslogistik GmbH

- DHL Group

- Kuehne+Nagel

- DSV (incl. DB Schenker)

- Airbus Defence and Space

- MBDA Deutschland GmbH

- KNDS Deutschland (formerly Krauss-Maffei Wegmann)

- Diehl Defence

- Hensoldt

- Leonardo Germany GmbH

- BAE Systems Deutschland

- MTU Aero Engines

- Lufthansa Technik Defense

- CEVA Logistics (CMA CGM)

- Hellmann Worldwide Logistics

- Rohlig Logistics

- GEODIS Germany

- DACHSER Defence & Aerospace Logistics

- Elbit Systems Deutschland

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview & Role of Logistics in Modern Warfare

- 4.2 Defense Spending Trends

- 4.3 Market Drivers

- 4.3.1 Bundeswehr's EUR 100 Billion Sondervermogen Accelerates Multi-Modal Logistics Modernization

- 4.3.2 NATO Deterrence Requirements Drive Rapid-Deployment Stockpiles Along The Rhine Corridor

- 4.3.3 Digital-Twin Roll-Out for Military Depots Cuts Inventory Lead-Times by More than 15 %

- 4.3.4 Civil-Military Logistics Integration with DB Cargo Unlocks Rail Capacity

- 4.3.5 Hydrogen-Powered Tactical Vehicle Pilots Demand New Fuel-Chain Services

- 4.3.6 EU Military Mobility Funding Boosts Cross-Border Corridor Upgrades

- 4.4 Market Restraints

- 4.4.1 Slower Puma IFV Retrofit Cycle Ties Up Warehouse Capacity

- 4.4.2 Tight Mod Cyber-Security Rules Delay Third-Party Cloud Onboarding

- 4.4.3 Skilled Logistics Personnel Shortage in Bundeswehr Civilian Corps

- 4.4.4 Environmental Approval Delays for New Ammunition Storage Sites

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Defense Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Service Type

- 5.1.1 Armament

- 5.1.2 Military Troops Movement Support

- 5.1.3 Technical Support & Maintenance

- 5.1.4 Medical Aid & Health Services

- 5.1.5 Fire-fighting Protection

- 5.1.6 Other Services

- 5.2 By Logistics Function

- 5.2.1 Transportation

- 5.2.1.1 Road

- 5.2.1.2 Air

- 5.2.1.3 Sea and Inland Waterways

- 5.2.1.4 Rail

- 5.2.2 Warehousing & Distribution

- 5.2.3 Value-added Services (Labelling, Kitting, Consulting)

- 5.2.1 Transportation

- 5.3 By End User

- 5.3.1 Army

- 5.3.2 Navy

- 5.3.3 Air Force

- 5.3.4 Others

- 5.4 By Region

- 5.4.1 North Rhine-Westphalia

- 5.4.2 Bavaria (Bayern)

- 5.4.3 Baden-Wurttemberg

- 5.4.4 Rest of States

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Rheinmetall AG

- 6.4.2 HIL Heeresinstandsetzungslogistik GmbH

- 6.4.3 DHL Group

- 6.4.4 Kuehne+Nagel

- 6.4.5 DSV (incl. DB Schenker)

- 6.4.6 Airbus Defence and Space

- 6.4.7 MBDA Deutschland GmbH

- 6.4.8 KNDS Deutschland (formerly Krauss-Maffei Wegmann)

- 6.4.9 Diehl Defence

- 6.4.10 Hensoldt

- 6.4.11 Leonardo Germany GmbH

- 6.4.12 BAE Systems Deutschland

- 6.4.13 MTU Aero Engines

- 6.4.14 Lufthansa Technik Defense

- 6.4.15 CEVA Logistics (CMA CGM)

- 6.4.16 Hellmann Worldwide Logistics

- 6.4.17 Rohlig Logistics

- 6.4.18 GEODIS Germany

- 6.4.19 DACHSER Defence & Aerospace Logistics

- 6.4.20 Elbit Systems Deutschland

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment