|

시장보고서

상품코드

2072895

프랑스의 방위 물류 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)France Defense Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

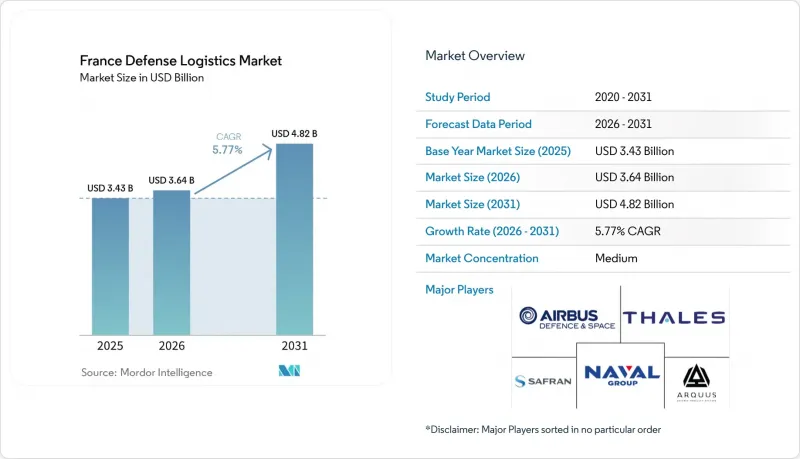

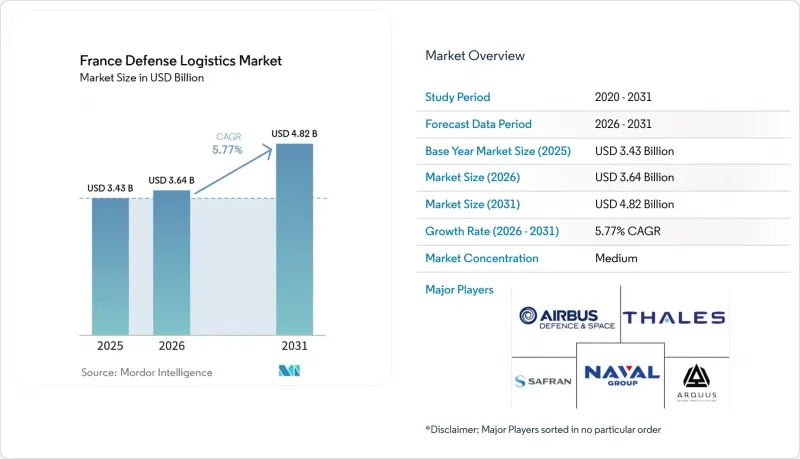

Mordor Intelligence에 의하면, 프랑스 방위 물류 시장 규모는 2025년 34억 3,000만 달러에서 2026년에는 36억 4,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 5.77%로 성장을 지속하여, 2031년에는 48억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 서비스 유형(무기, 군 부대 이동 지원, 기술 지원 및 유지보수 등), 물류 기능별(수송, 창고·유통 등), 최종 사용자별(육군, 공군 등), 지역별(일드프랑스, 오베르뉴-론-알프, 프로방스-알프-코트다쥐르, 옥시타니 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

프랑스 방위 물류 시장 동향과 인사이트

전략 항공·해상 수송 함대의 현대화

프랑스가 전략 수송 및 지원 함대의 현대화를 추진하는 가운데, 프랑스 방위 물류 시장의 서비스 규모가 확대되고 있습니다. 프랑스 공군·우주군은 라팔 전투기 286대로의 전환을 추진 중이며, 사베나 테크닉스는 2025년 12월, 프랑스와 독일이 공동 운용하는 C-130J 및 KC-130J 기단을 대상으로 한 10년간의 CAROLUS 지원 계약을 수주했습니다. 또한, AFI KLM 엔지니어링 앤드 유지관리(AFI KLM Engineering & Maintenance)도 2025년 12월, 프랑스의 AWACS 기체 4대를 대상으로 한 10년간의 통합 지원 계약을 체결했습니다. 계약 기간이 장기화됨에 따라 공급업체들은 더 많은 부품 재고를 확보하고 지원 팀을 운영 현장 근처에 배치해야 하는 압박을 받고 있으며, 그 결과 국내 물류 전문 업체에 대한 부가가치가 더욱 높아지고 있습니다. A400M의 예측 유지보수 결과, 이미 가용 비행 시간이 9% 증가하고 정비 시간이 7% 감소한 것으로 나타났으며, 이는 프랑스 방위 물류 시장에서 데이터 연계형 공급망의 보다 광범위한 활용을 뒷받침하고 있습니다.

SIMMAD 및 MCO 서비스 계약의 외부 위탁

군사 항공 지원이 아웃소싱 및 번들형 서비스 모델로 더욱 전환됨에 따라, 프랑스의 방위 물류 시장은 확대되고 있습니다. 프랑스의 “LPM 2024-2030”에서는, 항공기 MCO에 490억 유로(565억 달러)가 배정되었으며, 이는 이전 계획보다 40% 증가한 금액입니다. 또한, 예비 부품 및 아웃소싱 서비스에 대해 연간 30억 유로(35억 달러)를 지불할 예정입니다. DMAe는 2028년 이후, 업종별 계약에서 보다 광범위한 세계 지원 계약으로 전환할 것이라고 밝혔습니다. 이를 통해 공급망 관리, 지속적인 항공 적합성, 24시간 기술 지원을 보다 제한된 상업적 관계 속에서 통합하게 됩니다. 이러한 변경 사항은 소규모 공급업체 시장 진입 장벽을 높이는 한편, 물류 성과 전반을 관리할 수 있는 기업에게는 더 광범위한 계약 범위를 창출하는 결과로 이어집니다. 프랑스 회계감사원(Cour des comptes)도 현행 계약 구조에는 경쟁력 향상의 여지가 있다고 지적하며, 향후 계약 체결 시에는 보다 엄격한 벤치마크를 설정하고 위험 분담을 확대할 것을 제안하고 있습니다.

사회 지출과의 상충 관계로 인한 예산적 압박

프랑스의 국방 물류 시장은 승인된 예산과 실제 계약 체결 과정 사이에 여전히 시기적 압박에 직면해 있습니다. 『폴리티코』의 보도에 따르면, 프랑스는 우크라이나 전쟁 발발 이후, 그 '전시 경제'라는 메시지가 시사하는 속도로는 계약을 체결하지 않았고, 일부 DTIB(방위산업 관련) 기업들은 생산 확대를 위해 이미 투자를 진행했음에도 불구하고 계약 체결을 기다려야 하는 상황이 되었습니다. 물류 사업자에게 있어 이러한 격차는 방위 계획의 총액 전망이 양호하더라도 창고, 운송, 유통 관련 발주를 지연시키는 요인이 될 수 있습니다. 이러한 영향이 가장 큰 곳은 중규모 하청 기업입니다. 대형 프라임 기업에 비해 운전자금에 대한 압박을 더 직접적으로 받고 있기 때문입니다. 또한, 프랑스의 공공 부채가 GDP의 110%를 초과하고 있다는 점도 국방 관련 추가 지출을 정치적으로 민감한 문제로 만들고 있으며, 이로 인해 수요 실현이 예측 기간까지 지연될 가능성이 있습니다.

부문별 분석

2025년, 프랑스 방위 물류 시장에서 무기 서비스가 39.77%의 점유율을 차지했습니다. 이는 탄약의 취급, 보관, 수송 및 유통이 현재 방위 태세 계획의 핵심으로 자리 잡고 있기 때문입니다. 프랑스의 탄약 비축량 확대 및 계획 중인 '프랑스 탄약 조달 플랫폼'은 2031년까지 탄약 물류에 대한 지속적인 수요를 뒷받침하고 있습니다. 군 부대의 이동, 지원, 기술 지원 및 정비 업무는 물류 차량의 교체와 보다 광범위한 통합 MCO(운용·유지보수·정비) 활동에 힘입어 두 번째로 큰 비중을 차지하고 있습니다. 소화·방호 및 기타 서비스는 실전 투입 빈도보다는 기지 지원이나 고정 시설의 요건과 밀접하게 관련되어 있기 때문에 여전히 규모는 작은 임베디드니다.

의료 지원 및 보건 서비스는 2026년부터 2031년까지 연평균 성장률(CAGR) 8.61%를 나타낼 것으로 예측되며, 프랑스 국방 물류 시장에서 가장 빠르게 성장하는 서비스 분야가 될 전망입니다. 2025년 10월, 프랑스군 보건국(Service de sante des armees)과 보건총국은 공동 비상사태 대응 헌장에 서명함으로써, 대량 사상자 발생 시나리오에 대비한 민간과 군 간의 협력을 공식적으로 확립했습니다. "ORION 26" 훈련에서는 60일 동안 지속되는 작전 상황에서 하루 최대 250명의 환자를 수용할 수 있는 의료 물류 체계가 검증되었으며, 콜드체인 의약품, 사전에 배치된 외과용 키트, 그리고 조율된 대피의 필요성이 부각되었습니다. 이로 인해 프랑스 방위 물류 업계에는 수요가 급속히 증가하고 있는 분야와, 전문적인 대응 능력이 여전히 제한적인 것으로 보이는 서비스의 틈새 시장이 남아 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액, 2026-2031년)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the france defense logistics market size is expected to grow from USD 3.43 billion in 2025 to USD 3.64 billion in 2026 and is forecast to reach USD 4.82 billion by 2031 at 5.77% CAGR over 2026-2031.

This report is Segmented by Service Type (Armament, Military Troops Movement Support, Technical Support & Maintenance, and More), by Logistics Function (Transportation, Warehousing & Distribution, and More), by End User (Army, Air Force, and More), and by Region (Ile-De-France, Auvergne-Rhone-Alpes, Provence-Alpes-Cote D'Azur, Occitanie, and More). The Market Forecasts are Provided in Terms of Value (USD).

France Defense Logistics Market Trends and Insights

Modernization of Strategic Air- and Sea-Lift Fleets

The France defense logistics market is seeing larger service volumes as France renews its strategic lift and support fleets. The French Air and Space Force is moving toward 286 Rafale combat aircraft, and Sabena technics secured a 10-year CAROLUS support contract in December 2025 for the Franco-German C-130J and KC-130J fleet. AFI KLM Engineering and Maintenance also signed a 10-year integrated support contract in December 2025 for France's 4 AWACS aircraft. Longer contract terms are pushing suppliers to hold deeper parts inventories and place support teams closer to operations, shifting more value toward domestic logistics specialists. A400M predictive maintenance results have already shown a 9% increase in available flight hours and a 7% decrease in maintenance hours, which support the wider use of data-linked supply chains in the France defense logistics market.

Outsourcing of SIMMAD and MCO Service Contracts

The France defense logistics market is expanding as military aviation support moves further toward outsourced and bundled service models. France's LPM 2024-2030 allocates EUR 49 billion (USD 56.5 billion) to aeronautical MCO, which is 40% above the prior plan, and directs annual payments of EUR 3 billion (USD 3.5 billion) toward spare parts and outsourced services. DMAe has stated that it will move from verticalized contracts to broader global support contracts from 2028, combining supply chain management, continuing airworthiness, and round-the-clock technical support within fewer commercial relationships. That change raises entry barriers for smaller providers, but it also creates larger contract scopes for companies that can manage full logistics performance. The Cour des comptes also pointed to room for competitiveness gains in current contract structures, suggesting tighter benchmarks and greater risk sharing in future awards.

Budgetary Pressure from Social-Spending Trade-Offs

The France defense logistics market still faces timing pressure between approved budgets and actual contract flow. Politico reported that France did not sign contracts at the pace implied by its war-economy messaging after the start of the Ukraine war, leaving some DTIB companies waiting after they had already invested to increase output. For logistics providers, that gap can delay warehouse, transport, and distribution orders even when top-line defense plans look strong. The effect is strongest on medium-sized subcontractors, because they carry working capital pressure more directly than large primes. France's public debt level above 110% of GDP also keeps supplementary defense disbursements politically sensitive, which can delay realized demand into the forecast period.

Other drivers and restraints analyzed in the detailed report include:

- NATO Readiness Stockpile Mandates

- Predictive-Maintenance Rollout (Plan SICS-SC2)

- Global Raw-Material and Component Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Armament services held 39.77% of the France defense logistics market share in 2025, because ammunition handling, storage, transport, and distribution now sit closer to the center of defense readiness planning. France's munitions buildup and the planned France Munitions procurement platform support sustained demand for ordnance logistics through 2031. Military troops movement, support, technical support, and maintenance form the next tier, supported by logistics fleet renewal and broader integrated MCO activity. Fire-fighting protection and other services remain smaller because they are more closely linked to base support and fixed-site requirements than to field-deployment intensity.

Medical aid and health services are projected to grow at 8.61% CAGR from 2026 to 2031, making it the fastest-growing service line in the France defense logistics market. The Service de sante des armees and the General Directorate for Health signed a joint emergency preparedness charter in October 2025, which formalized civil-military coordination for mass-casualty scenarios. ORION 26 tested medical logistics for up to 250 patients per day over 60 days of sustained operations, underscoring the need for cold-chain drugs, pre-positioned surgical kits, and coordinated evacuation. That leaves the France defense logistics industry with a service niche where demand is rising quickly, but specialist capacity still looks limited.

Complete Report Scope:

- By Service Type

- Armament

- Military Troops Movement Support

- Technical Support & Maintenance

- Medical Aid & Health Services

- Fire-fighting Protection

- Other Services

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing & Distribution

- Value-added Services (Labelling, Kitting, Consulting)

- Transportation

- By End User

- Army

- Navy

- Air Force

- Others

- By Region

- Ile-de-France

- Auvergne-Rhone-Alpes

- Provence-Alpes-Cote d'Azur

- Hauts-de-France

- Nouvelle-Aquitaine

- Occitanie

- Grand Est

- Brittany

- Others

List of Companies Covered in this Report:

- Airbus Defence and Space

- Thales Group

- Safran

- Naval Group

- Arquus

- Dassault Aviation

- MBDA

- CMA CGM Group

- GEODIS

- Daher

- Sabena technics

- KNDS

- SPIE

- Kuehne+Nagel

- DHL Supply Chain

- DSV (Incl. DB Schenker)

- Turgis Gaillard

- MROD

- Alstef Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview & Role of Logistics in Modern Warfare

- 4.2 Defense Spending Trends

- 4.3 Market Drivers

- 4.3.1 Modernization of Strategic Air- and Sea-Lift Fleets

- 4.3.2 Outsourcing of SIMMAD and MCO Service Contracts

- 4.3.3 NATO Readiness Stockpile Mandates

- 4.3.4 Predictive-Maintenance Rollout (Plan SICS-SC2)

- 4.3.5 Climate-Resilient Logistics Infrastructure Upgrades

- 4.3.6 Dual-Use Hubs for Space and Drone Operations Near Toulouse

- 4.4 Market Restraints

- 4.4.1 Budgetary Pressure from Social-Spending Trade-Offs

- 4.4.2 Global Raw-Material and Component Shortages

- 4.4.3 EU Carbon-Emission Caps on Military Transport

- 4.4.4 Ageing Workforce in Logistics Corps

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Defense Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Service Type

- 5.1.1 Armament

- 5.1.2 Military Troops Movement Support

- 5.1.3 Technical Support & Maintenance

- 5.1.4 Medical Aid & Health Services

- 5.1.5 Fire-fighting Protection

- 5.1.6 Other Services

- 5.2 By Logistics Function

- 5.2.1 Transportation

- 5.2.1.1 Road

- 5.2.1.2 Air

- 5.2.1.3 Sea and Inland Waterways

- 5.2.1.4 Rail

- 5.2.2 Warehousing & Distribution

- 5.2.3 Value-added Services (Labelling, Kitting, Consulting)

- 5.2.1 Transportation

- 5.3 By End User

- 5.3.1 Army

- 5.3.2 Navy

- 5.3.3 Air Force

- 5.3.4 Others

- 5.4 By Region

- 5.4.1 Ile-de-France

- 5.4.2 Auvergne-Rhone-Alpes

- 5.4.3 Provence-Alpes-Cote d'Azur

- 5.4.4 Hauts-de-France

- 5.4.5 Nouvelle-Aquitaine

- 5.4.6 Occitanie

- 5.4.7 Grand Est

- 5.4.8 Brittany

- 5.4.9 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Airbus Defence and Space

- 6.4.2 Thales Group

- 6.4.3 Safran

- 6.4.4 Naval Group

- 6.4.5 Arquus

- 6.4.6 Dassault Aviation

- 6.4.7 MBDA

- 6.4.8 CMA CGM Group

- 6.4.9 GEODIS

- 6.4.10 Daher

- 6.4.11 Sabena technics

- 6.4.12 KNDS

- 6.4.13 SPIE

- 6.4.14 Kuehne+Nagel

- 6.4.15 DHL Supply Chain

- 6.4.16 DSV (Incl. DB Schenker)

- 6.4.17 Turgis Gaillard

- 6.4.18 MROD

- 6.4.19 Alstef Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment