|

시장보고서

상품코드

2073062

브랜치 라우터 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Branch Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

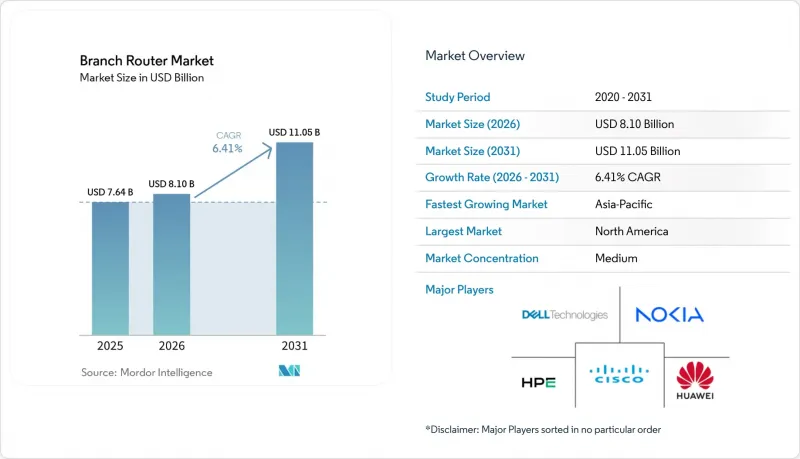

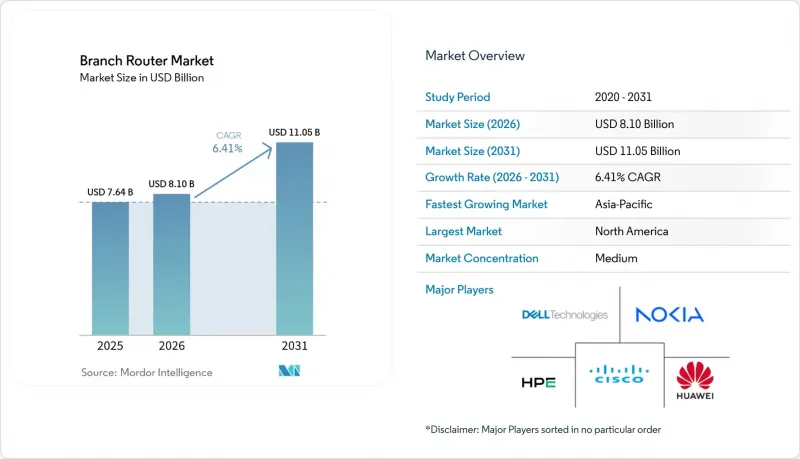

Mordor Intelligence에 의하면, 브랜치 라우터 시장 규모는 2025년 76억 4,000만 달러에서 2026년에는 81억 달러로 확대되어 2026년부터 2031년까지 CAGR 6.41%로 성장을 지속하여, 2031년에는 110억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 처리량 등급(저처리량 지점용 라우터, 중처리량 지점용 라우터, 고성능 지점용 라우터 등), 지점 규모(소규모 지점, 중규모 지점, 대규모 지점), 접속 방식(이더넷, 광대역 등), 최종 사용자 산업 분야(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 소매 및 전자상거래 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 브랜치 라우터 시장 동향 및 인사이트

팬데믹 이후 안전한 원격 접속에 대한 수요 증가

하이브리드 근무 방식의 확산으로 인해 모든 거점이 보안 대책의 실행 거점이 되면서, 조직은 라우팅, 방화벽, 제로 트러스트 기능을 하나의 기기에 통합해야 하는 상황에 직면해 있습니다. 현재 각 벤더사는 개별 어플라이언스에 의존하지 않고, 차세대 방화벽 엔진, 암호화 터널 오케스트레이션, AI를 활용한 가시화 기능을 브랜치 라우터에 직접 통합하고 있습니다. 시스코의 "통합 지점" 번들 및 포티넷의 "SASE Outpost"는 단일 벤더의 스택이 도입 주기를 단축하는 동시에 정책의 일관성을 높인다는 것을 보여줍니다. 또한, 플랫폼 로드맵에는 상용 양자 컴퓨팅의 등장을 대비해 포스트 양자암호화 제어 기능이 추가되어 있어, 키 교환 및 디바이스 관리가 앞으로도 지속적으로 지원될 수 있도록 보장되고 있습니다. 기업들이 하드웨어를 업데이트함에 따라, 보안 연결 기능의 중요성이 단순한 포트 수보다 점점 더 강조되고 있으며, 비용을 중시하는 부문에서도 사양 업그레이드가 진행되고 있습니다.

신흥 시장에서 소매 및 BFSI(은행, 금융, 보험 및 증권) 지점 네트워크 확대

은행, 패스트푸드점, 편의점 체인은 인도, 인도네시아, 이집트 및 걸프 국가들에 수천 개의 소규모 매장을 운영하고 있습니다. 이러한 전개에는 가혹한 환경 조건을 견디면서도 POS 단말기, 영상 분석, 디지털 사이니지를 구동할 수 있는 소형 라우터가 필요합니다. 정부의 광섬유 구축 사업과 전국적인 5G 확산에 힘입어, 지점 설립이 가능한 후보지가 더욱 늘어나고 있으며, 이제는 계산 비용이 아닌 네트워크 커버리지가 주요 제약 요인으로 대두되고 있습니다. 금융 서비스용 규정 준수 템플릿을 사전 탑재할 수 있고, 현지 통신 규정을 준수하는 하드웨어 인증을 획득한 공급업체는 입찰에서 타사를 압도하는 점유율을 확보하고 있습니다. 지점 수가 증가함에 따라 집중형 컨트롤러 플랫폼과 제로 터치 프로비저닝이 필수 요소가 되었으며, 관리 소프트웨어가 조달 시 결정적인 요인으로 작용하고 있습니다.

레거시 펌웨어로 인한 보안 취약점

코드가 최신 버전이 아니기 때문에 지점용 기기는 원격 조작을 통한 해킹 위험에 노출되어 있으며, 소비자용 모델의 CVE 건수는 기업용 기기의 평균보다 10배 이상 많습니다. 2025년부터 2026년까지 공개된 중대한 취약점은 라우터가 여전히 스파이 활동과 봇넷의 주요 표적임을 보여줍니다. 규제 당국은 현재 인증되지 않은 수입품을 차단하고 있어, 구매자들은 정기적으로 패치를 공개하고 모든 기기에 대한 자동 업데이트를 지원하는 브랜드를 우선적으로 선택할 수밖에 없는 상황입니다. 그 결과, 기업들은 그레이 마켓의 기기를 단계적으로 폐지하고 있지만, 많은 중소기업들은 교체 비용을 마련하는 데 어려움을 겪고 있으며, 이로 인해 단기적인 업그레이드 속도가 둔화되고 지점용 라우터 시장 전체의 성장세가 위축되고 있습니다.

부문별 분석

2025년, 고성능 어플라이언스는 브랜치 라우터 시장에서 41.88%의 점유율을 차지하며, 대역폭과 비용의 균형을 중시하는 중규모 브랜치 거점에 적합함을 입증하고 있습니다. 기업들이 엣지 AI 추론, 프라이빗 5G 코어, 풀 터널 SASE를 도입함에 따라, 이 부문은 2031년까지 연평균 성장률(CAGR) 7.12%로 확대될 것으로 전망됩니다. 이러한 워크로드에는 통합형 암호화 가속기나 멀티 기가비트 인터페이스가 필요하지만, 이러한 기능들은 이제 미드레인지급 칩에 기본으로 탑재되고 있습니다. 최대 95Gbps의 IPsec 처리량을 자랑하는 시스코의 "8000 시리즈 보안 라우터"는 계산 부하가 높은 엣지 기기로의 전환을 상징하는 사례입니다. 반면, 저처리량 모델은 범용 하드웨어에서 구동되는 가상화 네트워크 기능에 의해 중개자 역할을 빼앗길 위험이 있어, 브랜치 라우터 시장에서 차지할 수 있는 점유율이 축소될 우려가 있습니다.

초고성능 플랫폼은 캐리어 어그리게이션, 하이퍼스케일 상호 연결 및 AI 패브릭의 스파인을 대상으로 하며, 과거에는 코어 라우터에만 국한되었던 테라비트급 용량을 실현하고 있습니다. 아리스타의 7800R4 시스템은 하나의 섀시에 800 GbE 포트 576개를 탑재하고 있어, 실리콘 비용 감소에 따른 기술의 파급 효과를 예고하고 있습니다. 예측 기간 동안 컴퓨팅과 라우팅은 점점 더 융합될 것이며, 처리량 분류가 모호해짐에 따라 구매자들은 정적인 "초당 패킷 수" 같은 정격이 아니라, 사용 가능한 확장 슬롯이나 전력 예산을 바탕으로 섀시를 선택하게 될 것입니다.

2025년 브랜치 라우터 시장 규모 중 중규모 지점이 43.62%를 차지하고 있으며, 이는 소매 은행에서 지역 물류창고에 이르기까지를 아우르는 표준화된 도입 키트를 반영한 것입니다. 그럼에도 불구하고, 가장 높은 연평균 성장률(CAGR) 6.84%로 성장을 지속하고, 있는 것은 편의점 체인의 급증, 은행 키오스크, 팝업식 의료 클리닉에 의해 창출된 소규모 점포들입니다. 로우 터치 프로비저닝과 클라우드 우선 관리가 필수화됨에 따라, 각 벤더사는 제로 터치 온보딩 스크립트를 탑재하고 Wi-Fi 및 LTE 하드웨어를 하나의 섀시에 통합하고 있습니다. 그와 정반대인 대규모 지점은 중복화된 업링크, 엣지 데이터 스토리지, 로컬 분석 클러스터를 갖춘 집계 노드 역할을 수행하며, 모듈형 라인 카드와 1.2kW를 초과하는 PoE(Power over Ethernet) 전력을 지원하는 섀시에 대한 수요를 뒷받침하고 있습니다.

네트워크 팀은 현재, "브랜치 애즈 코드" 툴킷을 도입하여, 이를 통해 바람직한 상태를 Git 저장소에 저장하고, 업데이트를 자동으로 푸시하며, 실패한 커밋을 롤백할 수 있게 되었습니다. 이러한 변화로 인해 수백 개의 마이크로 지점을 운영하기 위한 추가 비용은 절감되지만, 인프라 엔지니어에게 요구되는 기술 수준은 높아지고 있으며, DevOps 수준의 인력이 부족한 다양한 조직에서 매니지드 SD-WAN 서비스에 대한 수요가 간접적으로 증가하고 있습니다.

지역별 분석

북미는 SD-WAN의 보급이 성숙 단계에 접어들었으며, CBRS의 상용화, 그리고 엣지 기기에 대한 포스트 양자암호화 대응을 규정하는 연방 정부의 제로 트러스트 의무화 정책에 힘입어 2025년 매출의 34.48%를 차지했습니다. 그러나 현재 조달 부서는 메모리 가격 급등과 리드타임 변동에 직면해 있어, 리프레시 주기의 총소유비용(TCO)이 상승하고 있습니다. 플랫폼 공급업체 간의 통합으로 인해 공급망에 대한 의존도가 높아지고 있지만, 대기업들은 멀티벤더 인증 프로그램이나 클라우드 비의존형 컨트롤러 전략을 통해 이를 관리하고 있습니다.

아시아태평양은 8.18%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 이러한 성장은 인도와 중국의 사설 5G 구축, 소매 체인의 확장, 그리고 인도네시아, 베트남, 필리핀 전역에 걸친 은행 지점 증가에 힘입어 이루어지고 있습니다. 2026년에 예정된 인도의 직접 주파수 대역 접근 관련 정책 변경으로 인해, 사설 네트워크 비용이 약 40% 절감될 가능성이 있습니다. 이로 인해 기업 소유 네트워크의 구축이 가속화되고, 클라우드 네이티브 5G 코어와의 유연한 통합은 물론, 방대한 수의 IoT 기기가 밀집된 환경을 지원할 수 있는 On-Premise형 지점용 라우터에 대한 수요가 창출될 것입니다. 각국 정부는 광섬유 설치 및 캠퍼스 5G 시범 사업에 보조금을 지원하고 있으며, 이를 통해 기본적인 연결 환경을 개선함으로써 2·3선 도시에서의 소규모 지점 확장을 현실화하고 있습니다. 현지 시스템 통합 업체들은 라우터와 관리형 서비스를 번들로 제공함으로써 채널의 복잡성을 해소하고, 클라우드 관리형 포트폴리오의 보급을 가속화하고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정) 준수, 데이터 주권 요건, 그리고 새로운 ASIC 설계를 촉진하는 에너지 효율 규제에 힘입어 꾸준한 업데이트 수요가 나타나고 있습니다. 경제적 역풍과 신중한 설비 투자로 인해 상승폭은 제한적이지만, 지속가능성에 관한 규제로 인해 기업들은 전력 소비가 많은 레거시 라우터를 폐지하고, CPU 클럭을 동적으로 조정하며, 미사용 포트를 유휴 상태로 전환하는 에너지 절약형 모델로의 전환을 촉진하고 있습니다. 중동 및 아프리카에서는 '디지털 이집트'와 같은 메가 프로젝트나 그린필드에서의 5G 확산에 힘입어, 절대적인 판매량은 적지만 지역에 따라 두 자릿수 성장을 보이고 있습니다. 남미 지역 시장 확대는 환율 변동과 광섬유 백홀 부족으로 인해 주춤하고 있지만, 공유 타워 계약과 클라우드 PoP(Point of Presence)의 보급에 힘입어 잠재적 수요가 서서히 발굴되기 시작하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the branch router market size is expected to grow from USD 7.64 billion in 2025 to USD 8.10 billion in 2026 and is forecast to reach USD 11.05 billion by 2031 at a 6.41% CAGR over 2026-2031.

This report is Segmented by Throughput Class (Low-Throughput Branch Routers, Mid-Range Branch Routers, High-Performance Branch Routers, and More), Branch Size (Small Branch, Medium Branch, and Large Branch), Access Connectivity (Ethernet, Broadband, and More), End User Industry (IT and Telecom, BFSI, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Branch Router Market Trends and Insights

Growing Demand For Secure Remote Connectivity Post Pandemic

Hybrid work has turned every site into a security enforcement point, pushing organizations to combine routing, firewall, and zero-trust functions in one device. Vendors now embed next-generation firewall engines, encrypted tunnel orchestration, and AI-driven visibility directly inside branch routers rather than relying on separate appliances. Cisco's Unified Branch bundle and Fortinet's SASE Outpost illustrate how single-vendor stacks shorten deployment cycles while tightening policy consistency. Platform roadmaps are also adding post-quantum cryptography controls in anticipation of commercial quantum computing, ensuring that key exchange and device management remain future-proof. As enterprises refresh hardware, secure connectivity features increasingly outweigh raw port counts, driving specification upgrades even in cost-sensitive tiers.

Expansion Of Retail And BFSI Branch Networks In Emerging Markets

Banks, quick-service restaurants, and convenience chains are rolling out thousands of compact outlets across India, Indonesia, Egypt, and the Gulf states. These footprints demand small-form-factor routers that can power point-of-sale devices, video analytics, and digital signage while surviving harsh environmental conditions. Government fiber programs and nationwide 5G launches further multiply the number of viable branch locations, making network coverage, not compute cost, the primary constraint. Vendors able to preload compliance templates for financial services and to certify hardware against local telecom rules capture a disproportionate share of tenders. As branch counts climb, centralized controller platforms and zero-touch provisioning become essential, turning management software into a deciding factor during procurement.

Security Vulnerabilities Due To Legacy Firmware

Out-of-date code leaves branch devices exposed to remote takeover, with consumer models averaging more than ten times the CVE count of enterprise units. High-severity flaws disclosed in 2025-2026 demonstrate that routers remain prime targets for espionage and botnets. Regulatory bodies now block uncertified imports, forcing buyers to prioritize brands that publish regular patches and support automated fleet-wide updates. Enterprises consequently phase out gray-market appliances, but many small businesses struggle to fund replacements, limiting near-term upgrade velocity and shaving growth off the overall branch router market.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Bandwidth Requirements With Cloud Migration

- Shift Toward SD-WAN And Software-Defined Branch Architectures

- Intense Price Competition And Commoditization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-performance appliances commanded 41.88% branch router market share in 2025, underscoring their suitability for medium branches that balance bandwidth and cost. The class is forecast to advance at a 7.12% CAGR through 2031 as enterprises adopt edge AI inference, private 5G cores, and full-tunnel SASE. These workloads demand integrated encryption accelerators and multi-gigabit interfaces, features that mid-range silicon increasingly embeds by default. Cisco's 8000 Series Secure Routers, with up to 95 Gbps IPsec throughput, exemplify the pivot toward compute-heavy edge gear. Conversely, low-throughput models risk disintermediation by virtualized network functions running on commodity boxes, shrinking their addressable slice of the branch router market size.

Ultra-high platforms target carrier aggregation, hyperscale interconnection, and AI fabric spines, shipping terabit capacities once reserved for core routers. Arista's 7800R4 system fits 576 ports of 800 GbE in one chassis, foreshadowing trickle-down effects as silicon costs fall. Over the forecast, compute and routing will increasingly converge, blurring throughput categories and encouraging buyers to select chassis based on available expansion slots and power budgets rather than on static packet-per-second ratings.

Medium branches delivered 43.62% of the 2025 branch router market size, reflecting standardized deployment kits that cover everything from retail banking to regional warehouses. Nonetheless, the fastest 6.84% CAGR belongs to small outlets created by proliferating convenience chains, bank kiosks, and pop-up healthcare clinics. Low-touch provisioning and cloud-first management are mandatory, leading vendors to embed zero-touch onboarding scripts and integrate Wi-Fi and LTE hardware into one enclosure. At the other extreme, large branches act as aggregation nodes with redundant uplinks, edge data storage, and local analytics clusters, sustaining demand for chassis that support modular line cards and power-over-Ethernet budgets above 1.2 kilowatts.

Network teams now deploy "branch as code" toolkits that store desired state in Git repositories, automatically push updates, and roll back failed commits. This shift lowers the incremental cost of operating hundreds of micro-branches but raises the skill threshold for infrastructure engineers, indirectly increasing demand for managed SD-WAN services among various organizations lacking DevOps-grade talent.

Complete Report Scope:

- By Throughput Class

- Low-throughput Branch Routers

- Mid-range Branch Routers

- High-performance Branch Routers

- Ultra-high Branch Routers

- By Branch Size

- Small Branch

- Medium Branch

- Large Branch

- By Access Connectivity

- Ethernet

- Broadband

- 4G/LTE

- 5G

- Hybrid

- By End User Industry

- IT and Telecom

- BFSI

- Retail and E-commerce

- Healthcare and Lifesciences

- Government and Public Sector

- Manufacturing

- Education

- Other End User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America controlled 34.48% of 2025 revenue, aided by mature SD-WAN uptake, CBRS commercialization, and federal zero-trust mandates that specify post-quantum readiness for edge devices. Procurement, however, now grapples with memory price inflation and lead-time volatility, raising the total cost of ownership for refresh cycles. Consolidation among platform suppliers creates additional supply-chain dependencies that large enterprises manage through multi-vendor qualification programs and cloud-agnostic controller strategies.

Asia-Pacific is projected to post the highest 8.18% CAGR. The growth is fueled by private 5G rollouts in India and China, retail chain expansion, and banking branch proliferation across Indonesia, Vietnam, and the Philippines. India's anticipated direct spectrum access policy changes in 2026 could lower private network costs by approximately 40%, accelerating enterprise-owned deployments and creating demand for on-premise branch routers with flexible integration to cloud-native 5G cores and support for massive IoT device density. Governments are subsidizing fiber builds and campus-5G pilots, lifting baseline connectivity and making small-branch deployment viable in secondary and tertiary cities. Local system integrators bundle routers with managed services, masking channel complexity and accelerating penetration of cloud-managed portfolios.

Europe exhibits steady replacement demand driven by GDPR compliance, data-sovereignty requirements, and energy-efficiency regulations that favor newer ASIC designs. Economic headwinds and cautious capital spending limit upside, yet sustainability mandates encourage enterprises to retire power-hungry legacy routers in favor of energy-aware models that dynamically scale CPU clocks and idle unused ports. Middle East and Africa, buoyed by mega-projects such as Digital Egypt and the prevalence of greenfield 5G rollouts, show double-digit local growth pockets despite lower absolute volume. South America's expansion is moderated by currency volatility and fiber backhaul gaps, but shared-tower agreements and cloud point-of-presence proliferation are beginning to unlock latent demand.

- Cisco Systems, Inc.

- Hewlett Packard Enterprise Company

- Huawei Technologies Co., Ltd.

- Dell Technologies Inc.

- Nokia Corporation

- Arista Networks, Inc.

- Extreme Networks, Inc.

- Ubiquiti Inc.

- Fortinet, Inc.

- Peplink International Limited

- Aruba Networks, LLC

- NETGEAR, Inc.

- TP-Link Technologies Co., Ltd.

- Advantech Co., Ltd.

- Teltonika Networks UAB

- Cradlepoint, Inc.

- Digi International Inc.

- Sierra Wireless, Inc.

- Edgecore Networks Corporation

- Allied Telesis Holdings K.K.

- MikroTikls SIA

- ZTE Corporation

- Ruijie Networks Co., Ltd.

- Cambium Networks Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Secure Remote Connectivity Post Pandemic

- 4.2.2 Expansion of Retail and BFSI Branch Networks in Emerging Markets

- 4.2.3 Increasing Bandwidth Requirements with Cloud Migration

- 4.2.4 Shift Toward SD-WAN and Software-Defined Branch Architectures

- 4.2.5 Edge AI Workload Offloading Necessitating On-Device Compute in Branch Routers

- 4.2.6 Availability of Private 5G/LTE Spectrum for Enterprises Accelerating Wireless WAN Routers

- 4.3 Market Restraints

- 4.3.1 Security Vulnerabilities Due to Legacy Firmware

- 4.3.2 Intense Price Competition and Commoditization

- 4.3.3 Chip Supply Chain Volatility Affecting Lead Times

- 4.3.4 Skills Shortage in Managing SD-WAN Policies at Scale

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Throughput Class

- 5.1.1 Low-throughput Branch Routers

- 5.1.2 Mid-range Branch Routers

- 5.1.3 High-performance Branch Routers

- 5.1.4 Ultra-high Branch Routers

- 5.2 By Branch Size

- 5.2.1 Small Branch

- 5.2.2 Medium Branch

- 5.2.3 Large Branch

- 5.3 By Access Connectivity

- 5.3.1 Ethernet

- 5.3.2 Broadband

- 5.3.3 4G/LTE

- 5.3.4 5G

- 5.3.5 Hybrid

- 5.4 By End User Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Retail and E-commerce

- 5.4.4 Healthcare and Lifesciences

- 5.4.5 Government and Public Sector

- 5.4.6 Manufacturing

- 5.4.7 Education

- 5.4.8 Other End User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Hewlett Packard Enterprise Company

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 Dell Technologies Inc.

- 6.4.5 Nokia Corporation

- 6.4.6 Arista Networks, Inc.

- 6.4.7 Extreme Networks, Inc.

- 6.4.8 Ubiquiti Inc.

- 6.4.9 Fortinet, Inc.

- 6.4.10 Peplink International Limited

- 6.4.11 Aruba Networks, LLC

- 6.4.12 NETGEAR, Inc.

- 6.4.13 TP-Link Technologies Co., Ltd.

- 6.4.14 Advantech Co., Ltd.

- 6.4.15 Teltonika Networks UAB

- 6.4.16 Cradlepoint, Inc.

- 6.4.17 Digi International Inc.

- 6.4.18 Sierra Wireless, Inc.

- 6.4.19 Edgecore Networks Corporation

- 6.4.20 Allied Telesis Holdings K.K.

- 6.4.21 MikroTikls SIA

- 6.4.22 ZTE Corporation

- 6.4.23 Ruijie Networks Co., Ltd.

- 6.4.24 Cambium Networks Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment