|

시장보고서

상품코드

2073080

사지 보철 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Limb Prosthetics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

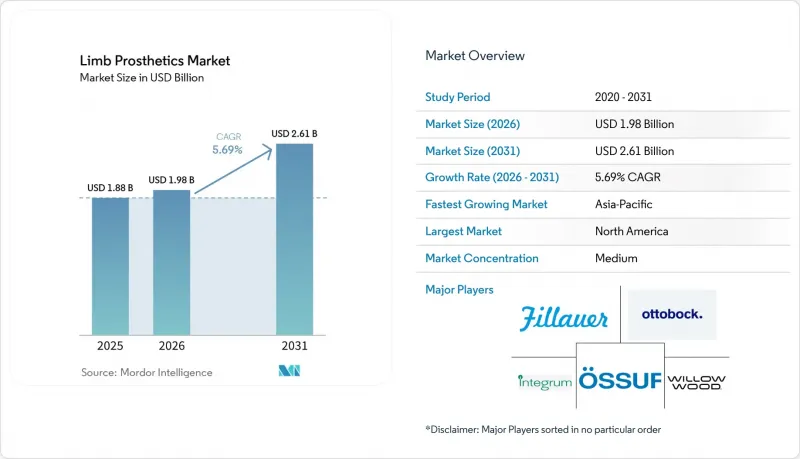

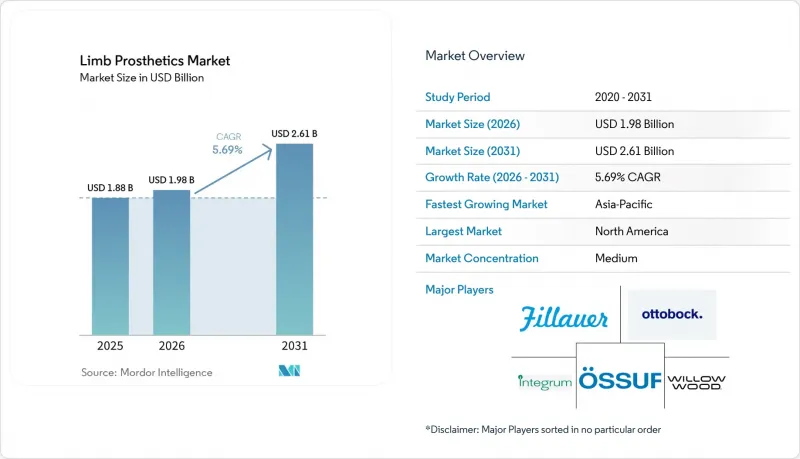

Mordor Intelligence에 의하면, 사지 보철 시장 규모는 2025년 18억 8,000만 달러에서 2026년에는 19억 8,000만 달러로 확대되어 2031년까지 26억 1,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 5.69%로 성장할 전망입니다.

본 보고서는 유형별(상지, 하지, 기타), 소재별(CFRP, 티타늄, 폴리에틸렌, 실리콘), 제어 방식별(근전도식, 신체 구동식, 케이블 구동식), 구성 부품별(소켓, 부속 장치, 관절, 기타), 용도(절단, 외상, 선천성 기형), 최종 사용자(병원 등), 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계 사지 보철 시장 동향 및 인사이트

외상 및 질환과 관련된 절단 발생률 증가

사지 보철 시장은 외상, 혈관 질환 및 당뇨병과 관련된 사지 상실로 인해 확대되는 수요 기반에 힘입어 지속적으로 성장하고 있습니다. National Inpatient Sample 데이터를 바탕으로 한 2025년 조사에 따르면, 230만 9,000명의 미국인이 사지 상실 상태로 생활하고 있는 것으로 추정되며, 이 수치는 2050년까지 2배로 증가하고, 2060년까지는 145% 증가할 것으로 예측됩니다. 전 세계의 부담은 이미 더욱 커졌으며, 2021년에는 4억 4,520만 명이 외상으로 인한 절단 상태를 안고 생활하고 있었고, 이러한 상태와 관련된 장애로 인해 보낸 연수는 590만 년에 달할 전망입니다. 일리노이주 병원 데이터에 따르면, 2016년부터 2023년 사이에 하지 및 발 절단 건수가 65% 증가한 것으로 나타났으며, 이는 더 광범위하게 나타나는 당뇨병 및 말초동맥질환으로 인한 유사한 압박을 반영하고 있습니다. 당뇨병과 관련된 하지 절단은 의족 시장에 반복적인 교체 주기를 초래하고 있습니다. 이는 전 세계적으로 매년 150만 건의 유사한 절단 수술이 이루어지고 있으며, 그중 50%에서 70%가 당뇨병으로 인한 것이기 때문입니다.

마이크로프로세서, 근전도 제어 및 생체모방 제어 시스템의 발전

사지 보철 시장은 단순히 상실된 해부학적 구조를 대체하는 데 그치지 않고, 제어성, 안정성, 기능 범위를 향상시키는 장치로 전환되고 있습니다. 2026년에 실시된 연구에서는 근내 전극 및 작용제·길항제 근육-신경 인터페이스 수술을 통해, 골고정형 신경 제어 무릎 의족의 성능이 입증되었습니다. 이는 신경 제어 기술이 실험실 단계의 가능성을 넘어서는 중임을 보여줍니다. 이러한 진전은 하이엔드 기기의 성능 상한선을 높이고, 보다 광범위한 임상 활용을 위한 장기적인 근거를 뒷받침한다는 점에서 중요합니다. 오토복(Ottobock)사 역시 사지 보철 시장의 이 분야에서 상업적인 성장세를 보이고 있으며, 2025년의 성장은 마이크로프로세서가 탑재된 무릎 의족의 출시와 북미·남미 및 EMEA 지역에서의 채택 확대에 힘입은 바 컸습니다. 2026년 1월 1일부터 HCSC가 미국 5개 주에서 K2 마이크로프로세서 방식 무릎 의족에 대한 보험 적용을 시작함에 따라, 보험 적용 범위의 확대가 수요를 더욱 직접적으로 뒷받침하고 있습니다. 이러한 기술적 검증과 보험사의 수용이 맞물리면서, 사지 보철 시장에서 제품 차별화의 핵심은 앞으로도 계속해서 첨단 시스템이 될 것입니다.

고급 사지 보철 및 소모품에 대한 고액의 본인 부담금

합리적인 가격 확보는 여전히 사지 보철 시장의 큰 걸림돌이 되고 있습니다. 특히, 첨단 의료기기의 경우 일부에만 보험이 적용되거나 아예 적용되지 않는 경우에는 더욱 그렇습니다. 또한, 접근성 격차도 고르지 않습니다. 미국의 공중보건 데이터에 따르면, 절단 위험이 높거나 의료 접근성이 낮은 상황은 사회경제적으로 취약한 지역과 당뇨병을 앓고 있는 흑인 성인에게 집중되어 있는 것으로 나타났습니다. 주요 기기에 대해 보험이 적용되는 경우에도, 라이너나 교체용 소켓 등의 소모품은 반복적으로 발생하기 때문에 이용자에게는 지속적인 경제적 부담이 발생합니다. 이러한 비용 부담이 문제가 되는 이유는 고성능 근전도식, 생체공학식 및 마이크로프로세서가 탑재된 의수가 일회성 구매 품목이 아니라, 장기적인 유지 관리 비용 부담으로 인해 환자들이 더 단순한 대체품으로 눈을 돌릴 가능성이 있기 때문입니다. 그 결과, 의수 시장은 충분한 보험에 가입한 고급 사용자층과 내구성, 수리 용이성, 그리고 총 소유 비용의 낮음을 우선시하는 비용에 민감한 사용자층으로 나뉘는 경우가 많습니다.

부문별 분석

2025년, 상지 의수는 41.21%의 시장 점유율을 차지하고 있으며, 이러한 선두 위상은 정교함을 중시하는 시스템에 따른 높은 평균 판매 가격을 반영한 것입니다. 의수 시장에서 상지용 기기는 많은 하지용 시스템보다 더 엄격한 요건 하에서 미세한 운동 기능, 다양한 잡기 동작, 그리고 외관상의 기대치를 재현해야 하기 때문에 종종 더 높은 가격대에 제공됩니다. 따라서 임상 대상자 수가 하지용 사용자보다 적더라도, 이 부문은 중요한 수익원이 되고 있습니다. 이 부문에서는 제품 개발 활동이 여전히 활발하며, 각 제조업체들은 다단계 그립 제어, 모듈식 손목, 경량 구조, 보다 자연스러운 사용자 조작성 등을 둘러싸고 경쟁을 펼치고 있습니다. Open Bionics사는 2026년, Hero FLEX의 적용 대상을 팔꿈치 위 절단 환자로 확대하고, 미국, 영국, 유럽, 호주, 뉴질랜드의 800곳 이상의 의료기관을 통해 판매를 지속함으로써 이러한 방향성을 더욱 강화했습니다.

하지 의족 시장은 여전히 가장 빠른 성장세를 보일 것으로 예상되며, 이 하위 유형의 의족 시장 규모는 2031년까지 연평균 성장률(CAGR) 7.14%로 확대될 것으로 전망됩니다. 이러한 증가는 하지 절단 환자 수가 훨씬 더 많다는 실정을 반영한 것으로, 과거 역학 조사에 따르면 미국의 절단 사례 중 91%가 하지와 관련되어 있습니다. 당뇨병도 이러한 전망을 뒷받침하고 있습니다. 이는 하지 절단이 여전히 만성 질환의 진행이나 혈관 합병증과 밀접한 관련이 있기 때문입니다. 부분 발 의수, 부분 손 의수, 중족골 절단 의수 등 기타 의수 유형은 시장 규모는 작지만, 하지 의수 업계에서 임상적으로 중요한 범주로 자리 잡고 있습니다. 이는 부분 절단 후 관리가 당뇨병성 족부 병변 관리에 있어 일반적이며, 다양한 사이즈에 대한 경제성이 요구되기 때문입니다. 하반신 의지 시스템의 성장은 더 광범위한 사지 보철 시장 전체에서 소켓, 라이너, 파이론 및 이후 교체 부품에서 발생하는 부수적인 수익도 뒷받침하고 있습니다.

2025년에는 탄소섬유 강화 폴리머가 37.83%의 점유율을 차지했으며, 이에 따라 복합재료는 사지 보철 시장 전체에서 구조적 성능 측면에서 계속해서 핵심적인 위치를 차지했습니다. 경량화와 에너지 반환은 사용자의 쾌적성과 기능적 효율성에 있어 매우 중요하기 때문에 탄소 복합재료는 의족과 철탑에 널리 사용되고 있습니다. 2026년에 실시된 러닝용 의족에 관한 연구에 따르면, 허니콤 샌드위치 구조의 탄소 복합재 설계가 안전 계수 1.95를 유지하면서, 고체 구조의 기준 설계와 비교해 에너지 저장 용량을 57.4% 향상시킨 것으로 나타났습니다. 이 결과는 이미 확립된 복합재료 시스템에서도 여전히 의미 있는 성능 향상의 여지가 있음을 시사합니다. 또한, 이는 사지 보철 시장 내 고급 하지 제품 분야에서 CFRP가 여전히 필수 불가결한 이유를 설명하는 데 도움이 됩니다.

티타늄 합금은 2031년까지 연평균 성장률(CAGR) 6.32%로 확대될 것으로 예측되며, 사지 보철 시장에서 가장 빠르게 성장하는 소재 그룹이 될 전망입니다. 이러한 매력은 강도 대 중량 비율, 내식성, 생체 적합성과 관련이 있으며, 기기가 장기간 착용, 고부하 및 골유합에 대응하는 설계로 전환됨에 따라 이러한 요소들은 모두 점점 더 중요해지고 있습니다. 이러한 추세는 골고정형 의수에 대한 관심이 높아짐에 따라 더욱 가속화되고 있으며, 이 분야에서는 인터페이스의 안정성이 장치의 구조에서 매우 중요합니다. 폴리에틸렌과 실리콘은 여전히 중요한 틈새 시장을 차지하고 있으며, 폴리에틸렌은 비용 효율성이 중요한 라이너나 소프트 소켓 용도로, 실리콘은 피부 친화성이나 개별적인 착용감이 더욱 중요시되는 상황에서 선호되고 있습니다. 따라서 사지 보철 업계에서 재료 간의 경쟁은 단순한 비용 비교에서 벗어나, 무게, 내구성, 임상적 편안함, 디지털 제조와의 호환성 등 다양한 요소를 종합적으로 고려한 비교로 점차 전환되고 있습니다.

지역별 분석

2025년, 북미는 42.23%의 점유율을 차지하며, 사지 보철 시장에서 지역별 1위를 기록하고 있습니다. 이 지역은 탄탄한 임상 인프라, 확립된 보험 환급 제도, 그리고 대규모 군인 및 퇴역 군인 환자층이라는 강점을 갖추고 있습니다. 재향군인부(VA)의 '절단 치료 시스템(Amputation System of Care)'은 대상 퇴역 군인들에게 종합적인 접근성을 지속적으로 지원하고 있으며, 사지 보철 치료에 드는 환자의 직접적인 비용 부담을 줄이는 데 기여하고 있습니다. 민간 보험사들의 정책도 지원적인 방향으로 바뀌고 있으며, HCSC는 2026년 1월 1일부터 미국 5개 주에서 K2 마이크로프로세서 무릎 관절의 보험 적용 범위를 확대할 예정입니다. 이 지역 내에서 미국이 사지 보철 시장 규모의 대부분을 차지하고 있지만, 캐나다와 멕시코는 여전히 제한적인 기회에 그치고 있으며, 보험 적용 범위의 폭은 여전히 미국의 수준에 미치지 못하고 있습니다.

유럽은 공적 의료 제도가 장기적인 의지 관리를 지원하고 있을 뿐만 아니라, 고령화에 따라 만성 질환의 부담이 계속 증가하고 있기 때문에 의지 시장에서 구조적으로 중요한 위치를 차지하고 있습니다. 독일, 영국, 프랑스는 재활 네트워크가 잘 갖춰져 있고, 보조기 및 의지 관련 인프라가 더욱 확립되어 있어 여전히 핵심 시장으로 자리 잡고 있습니다. 또한, 이 지역은 임상 표준화와 첨단 기술 개발의 오랜 역사를 가지고 있으며, 이것이 고품질의 하지 및 상지 시스템의 보급을 뒷받침하고 있습니다. 한편, 보험 환급에 대한 압박과 공급에 대한 의존으로 인해 국가별로 접근성에 차이가 발생하고 있으며, 이는 고급 의족의 보급이 균일하게 진행되지 않는 요인이 되고 있습니다. 이 때문에 유럽의 사지 보철 시장은 견조한 임상 수요가 있는 반면, 엄격한 비용 관리와 국가별 차이도 존재하는 등, 안정적인 상황과 복잡한 상황이 뒤섞인 시장 양상을 보이고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 7.74%를 기록하며 가장 빠른 성장세를 보일 것으로 전망되어, 사지 보철 시장의 주요 성장 지역으로 부상하고 있습니다. 당뇨병 유병률 증가, 의료 투자 확대, 그리고 사지 보철 서비스 제공 능력의 향상으로 인해 중국, 인도, 한국, 호주 전역에서 이러한 추세가 가속화되고 있습니다. 중국과 인도는 가장 큰 판매량 기회를 제공하고 있지만, 고급 근전도 방식 기기에 비해 자체 구동형 및 모듈식 하지용 제품의 보급이 더 빠르게 진행되고 있습니다. 호주와 이 지역의 다른 선진 지역에서는 프리미엄 제품의 보급률이 높아지고 있으며, 오토복(Ottobock)사의 아시아태평양 사업도 2025년 호주의 노던 프로스테틱스(Northern Prosthetics)사를 인수함으로써 그 혜택을 누리고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the limb prosthetics market size is expected to increase from USD 1.88 billion in 2025 to USD 1.98 billion in 2026 and reach USD 2.61 billion by 2031, growing at a CAGR of 5.69% over 2026-2031.

This report is Segmented by Type (Upper, Lower Limb, Other), Material (CFRP, Titanium, Polyethylene, Silicone), Control (Myoelectric, Body-Powered, Cable-Powered), Component (Socket, Appendage, Joint, Other), Application (Amputation, Traumatic Injury, Congenital Deformity), End User (Hospitals, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Value (USD).

Global Limb Prosthetics Market Trends and Insights

Rising Incidence of Traumatic and Disease-Linked Amputations

The limb prosthetics market continues to rest on a widening demand base created by trauma, vascular disease, and diabetes related limb loss. A 2025 study using National Inpatient Sample data estimated that 2.309 million Americans were living with limb loss, and it projected that this number will double by 2050 and rise by 145% by 2060. The global burden is already much larger, with 445.2 million people living with traumatic amputation in 2021 and 5.9 million years lived with disability linked to that condition. Hospital evidence in Illinois also showed a 65% rise in leg and foot amputations between 2016 and 2023, which reflects the same pressure from diabetes and peripheral artery disease seen more broadly. Diabetes related lower extremity amputations add a recurring replacement cycle to the limb prosthetics market because 1.5 million such amputations occur each year worldwide, and diabetes accounts for 50% to 70% of them.

Advancing Microprocessor, Myoelectric, and Bionic Control Systems

The limb prosthetics market is moving toward devices that improve control, stability, and functional range rather than only replacing lost anatomy. A 2026 study validated bone-anchored, neurally controlled knee prosthesis performance through intramuscular electrodes and agonist-antagonist myoneural interface surgery, which shows that neural control is moving beyond laboratory promise. That progress matters because it raises the performance ceiling for premium devices and supports the long-term case for broader clinical use. Ottobock also showed commercial traction in this part of the limb prosthetics market, with 2025 growth supported by microprocessor knee launches and stronger adoption in the Americas and EMEA. Coverage expansion is beginning to support demand more directly, as HCSC started covering K2 microprocessor knees across 5 U.S. states from January 1, 2026. This combination of technical validation and payer acceptance should keep advanced systems at the center of product differentiation in the limb prosthetics market.

High Out-of-Pocket Cost for Advanced Prosthetics and Consumables

Affordability remains a major brake on the limb prosthetics market, especially when advanced devices are only partly covered or not covered at all. The access gap is also uneven, since U.S. public health data links higher amputation risk and poorer access conditions to low socioeconomic neighborhoods and to Black adults with diabetes. Even where primary devices are reimbursed, recurring consumables such as liners and replacement sockets still create repeated spending pressure for users. That cost burden matters because premium myoelectric, bionic, and microprocessor devices are not one-time purchases, and long-term upkeep can steer patients toward simpler alternatives. As a result, the limb prosthetics market often splits between well-insured premium users and cost-sensitive users who prioritize durability, repairability, and lower total ownership cost.

Other drivers and restraints analyzed in the detailed report include:

- Greater Access Through Reimbursement, Subsidy, and Veteran Support Programs

- 3D Scanning, Additive Manufacturing, and Rapid Customization at Scale

- Fit Failure, Socket Intolerance, and Revision Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Upper limb prosthetics held 41.21% share in 2025, and that leadership reflected the higher average selling prices associated with dexterity-focused systems. In the limb prosthetics market, upper limb devices often carry more premium pricing because they must replicate fine motor movement, grip variation, and cosmetic expectations in a more demanding way than many lower limb systems. This makes the category an important revenue anchor even when the clinical population is smaller than that of lower extremity users. Product development activity also remains intense in this segment, with manufacturers competing on multi-grasp control, modular wrists, lighter structures, and more natural user interaction. Open Bionics strengthened that direction in 2026 when it expanded Hero FLEX to above-elbow amputees and continued distribution through more than 800 clinical locations across the United States, the United Kingdom, Europe, Australia, and New Zealand.

Lower limb prosthetics are still expected to record the fastest growth, with the limb prosthetics market size for this subtype projected to rise at a 7.14% CAGR through 2031. That growth reflects the much larger base of lower extremity limb loss, with prior epidemiology showing that 91% of U.S. limb loss cases involve the lower extremity. Diabetes also reinforces this outlook because lower extremity amputations remain heavily tied to chronic disease progression and vascular complications. Other prosthetic types, including partial foot, partial hand, and transmetatarsal devices, remain smaller but clinically meaningful categories in the limb prosthetics industry because partial amputation care is common in diabetic foot management and requires different fitting economics. Growth in lower limb systems also supports adjacent revenue from sockets, liners, pylons, and follow-up replacements across the broader limb prosthetics market.

Carbon fiber reinforced polymers held 37.83% share in 2025, which kept composites at the center of structural performance across the limb prosthetics market. Carbon composites remain deeply embedded in prosthetic feet and pylons because weight reduction and energy return are central to user comfort and functional efficiency. A 2026 study on running prosthetic feet showed that honeycomb sandwich carbon composite designs delivered a 57.4% increase in energy storage capacity versus solid reference designs while maintaining a 1.95 safety factor. That result suggests there is still room for meaningful performance gains within established composite material systems. It also helps explain why CFRPs remain critical to premium lower limb products in the limb prosthetics market.

Titanium alloys are projected to expand at a 6.32% CAGR through 2031, making them the fastest-growing material group in the limb prosthetics market. Their appeal is tied to strength-to-weight performance, corrosion resistance, and biocompatibility, all of which matter more as devices move toward long-wear, higher-load, and osseointegration-compatible designs. The same trend is supported by growing interest in bone-anchored prosthetic approaches, where interface stability becomes central to the device architecture. Polyethylene and silicone still hold important niches, with polyethylene used in cost-sensitive liners and soft socket applications, and silicone favored where skin compliance and individualized fit matter more. Material competition in the limb prosthetics industry is therefore shifting from simple cost comparison toward a broader mix of weight, durability, clinical comfort, and digital fabrication compatibility.

Complete Report Scope:

- By Prosthetic Type

- Upper Limb Prosthetics

- Lower Limb Prosthetics

- Other Prosthetic Types

- By Material

- Carbon Fiber Reinforced Polymers

- Titanium Alloys

- Polyethylene

- Silicone

- By Control Mechanism

- Myoelectric Prosthetics

- Body-Powered Prosthetics

- Cable-Powered Prosthetics

- By Component

- Socket

- Appendage

- Joint

- Connecting Module

- Other Prosthetic Components

- By Application

- Amputation Surgery

- Traumatic Injury

- Congenital Limb Deformity

- By End User

- Hospitals

- Prosthetics Clinics

- Rehabilitation Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 42.23% share in 2025, which gave it the leading regional position in the limb prosthetics market. The region benefits from strong clinical infrastructure, established reimbursement pathways, and a sizeable military and veteran patient base. The VA's Amputation System of Care continues to support comprehensive access for eligible veterans and helps reduce direct patient cost exposure for prosthetic care. Private payer policy is also moving in a supportive direction, with HCSC expanding K2 microprocessor knee coverage across 5 U.S. states from January 1, 2026. Within the region, the United States anchors most of the limb prosthetics market size, while Canada and Mexico remain more selective opportunities where advanced coverage depth still trails the U.S. benchmark.

Europe remains a structurally important part of the limb prosthetics market because its public health systems support long-term prosthetic care and because aging populations continue to raise chronic disease burden. Germany, the United Kingdom, and France remain the core markets due to stronger rehabilitation networks and more established orthotics and prosthetics infrastructure. The region also has a long history of clinical standardization and engineering depth, which supports adoption of premium lower limb and upper limb systems. At the same time, reimbursement pressure and supply dependence can create uneven access conditions across countries, which limits how evenly premium devices scale. This leaves Europe as a stable but mixed landscape in the limb prosthetics market, where strong clinical demand exists alongside tighter cost control and country level variation.

Asia-Pacific is projected to record the fastest growth at a 7.74% CAGR through 2031, and it is becoming a key expansion zone for the limb prosthetics market. Rising diabetes prevalence, broader healthcare investment, and improving prosthetic service capacity are supporting this direction across China, India, South Korea, and Australia. China and India offer the largest volume opportunity, but adoption remains stronger in body-powered and modular lower limb products than in high-end myoelectric devices. Australia and other developed pockets of the region are showing stronger premium penetration, and Ottobock's APAC business also benefited from its 2025 acquisition of Northern Prosthetics in Australia.

- ALIMCO (Artificial Limbs Manufacturing Corporation of India)

- Blatchford

- Coapt

- College Park Industries

- Endolite India Ltd.

- Fillauer

- Freedom Innovations LLC

- Hanger, Inc.

- Integrum AB

- Mobius Bionics

- Motorica

- Open Bionics Ltd.

- Ortho Europe Ltd.

- Ottobock

- Ossur hf.

- Proteor SAS

- Steeper Group

- Streifeneder USA

- Trulife India Private Limited

- Willow Wood Global

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Traumatic and Disease-Linked Amputations

- 4.2.2 Advancing Microprocessor, Myoelectric, and Bionic Control Systems

- 4.2.3 Greater Access Through Reimbursement, Subsidy, and Veteran Support Programs

- 4.2.4 3D Scanning, Additive Manufacturing, and Rapid Customization at Scale

- 4.2.5 Pediatric Replacement Cycles and Growth Accommodating Device Demand

- 4.2.6 Expansion of Remote Fitting, Tele-Rehabilitation, and Connected Follow-Up Care

- 4.3 Market Restraints

- 4.3.1 High Out-of-Pocket Cost for Advanced Prosthetics and Consumables

- 4.3.2 Fit Failure, Socket Intolerance, and Revision Complexity

- 4.3.3 Limited Access to Certified Prosthetists in Secondary and Tertiary Cities

- 4.3.4 Weak Supply Chain Depth for Precision Components and Advanced Materials

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Prosthetic Type

- 5.1.1 Upper Limb Prosthetics

- 5.1.2 Lower Limb Prosthetics

- 5.1.3 Other Prosthetic Types

- 5.2 By Material

- 5.2.1 Carbon Fiber Reinforced Polymers

- 5.2.2 Titanium Alloys

- 5.2.3 Polyethylene

- 5.2.4 Silicone

- 5.3 By Control Mechanism

- 5.3.1 Myoelectric Prosthetics

- 5.3.2 Body-Powered Prosthetics

- 5.3.3 Cable-Powered Prosthetics

- 5.4 By Component

- 5.4.1 Socket

- 5.4.2 Appendage

- 5.4.3 Joint

- 5.4.4 Connecting Module

- 5.4.5 Other Prosthetic Components

- 5.5 By Application

- 5.5.1 Amputation Surgery

- 5.5.2 Traumatic Injury

- 5.5.3 Congenital Limb Deformity

- 5.6 By End User

- 5.6.1 Hospitals

- 5.6.2 Prosthetics Clinics

- 5.6.3 Rehabilitation Centers

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 Australia

- 5.7.3.5 South Korea

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East & Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East & Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 ALIMCO (Artificial Limbs Manufacturing Corporation of India)

- 6.3.2 Blatchford Limited

- 6.3.3 Coapt LLC

- 6.3.4 College Park Industries

- 6.3.5 Endolite India Ltd.

- 6.3.6 Fillauer LLC

- 6.3.7 Freedom Innovations LLC

- 6.3.8 Hanger, Inc.

- 6.3.9 Integrum AB

- 6.3.10 Mobius Bionics

- 6.3.11 Motorica

- 6.3.12 Open Bionics Ltd.

- 6.3.13 Ortho Europe Ltd.

- 6.3.14 Ottobock SE & Co. KGaA

- 6.3.15 Ossur hf.

- 6.3.16 Proteor SAS

- 6.3.17 Steeper Group

- 6.3.18 Streifeneder USA

- 6.3.19 Trulife India Private Limited

- 6.3.20 WillowWood Global LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment