|

시장보고서

상품코드

1782088

도우 기반 프리믹스 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Dough-Based Premixes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

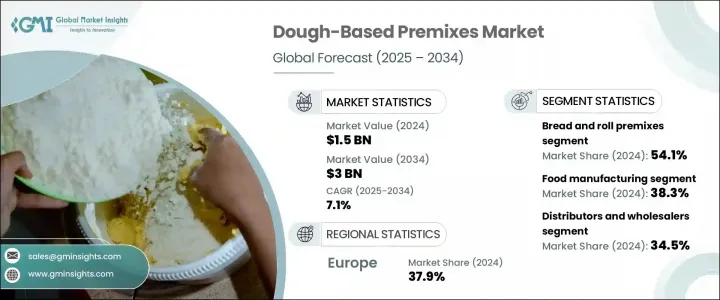

세계의 도우 기반 프리믹스 시장 규모는 2024년에 15억 달러로 평가되었고, CAGR 7.1%로 성장할 전망이며, 2034년에는 30억 달러에 이를 것으로 예측됩니다.

도우 기반 프리믹스는 밀가루, 강한 분말, 효소, 유화제 등의 제빵 원료의 기성품 혼합이며, 빵, 롤 케이크, 페이스트리, 피자, 머핀과 같은 제품의 반죽 준비를 단순화하도록 설계되었습니다. 이러한 프리믹스는 일관성을 보장하고 준비 시간을 절약하며 상업용 베이커와 가정 소비자 모두에게 편의성을 제공합니다. 시간 효율성 및 안정적인 품질을 제공하는 제품에 대한 수요가 증가함에 따라 시장은 꾸준히 성장하고 있습니다. 주요 비즈니스 기회는 클린 라벨 옵션, 글루텐 프리 블렌딩, 혁신적인 제품 출시, 강화 믹스에 있습니다. 이 성장은 외식 체인의 확대, 도시화, 신흥국의 홈 베이커리 동향 증가에 의해 더욱 촉진됩니다.

콜드체인 물류 혁신, 맞춤형 프리믹스 솔루션, 귀리 기반, 고단백질, 식이섬유 강화 블렌드와 같은 기능성 원료의 배합은 포장 식품, 빠른 서비스 레스토랑, 소매 시장에 새로운 길을 열고 있습니다. 건강 지향과 편리성의 동향이 세계적으로 높아지고 있는 가운데, 도우 기반 프리믹스는 차세대 베이커리 제품과 솔루션을 창조하는데 있어서 필수적인 요소라는 인식이 높아지고 있습니다. 소비자는 시간 절약뿐만 아니라 영양과 깨끗한 라벨의 원료에 대한 더 높은 기준을 충족하는 구운 과자를 찾고 있습니다. 이 시프트는 글루텐 프리, 비타민과 미네랄의 강화, 기능성 섬유와 단백질의 강화 등의 옵션을 포함한 프리믹스 배합의 혁신을 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 15억 달러 |

| 예측 금액 | 30억 달러 |

| CAGR | 7.1% |

2024년 시장 규모는 빵 롤용 프리믹스 부문이 54.1%의 점유율을 차지했으며, 8억 2,740만 달러였습니다. 이 부문이 주도권을 잡고 있는 것은 백빵, 통밀 빵, 특수 빵, 장인기 빵 믹스에 대한 수요가, 소매업이나 산업제 빵 부문에 널리 침투하고 있는 것에 기인하고 있습니다. 소비자는 시간을 절약할 수 있을 뿐만 아니라 영양가가 높고 건강 동향과 전통적인 선호도를 모두 충족하기에 충분한 다재다능한 빵 옵션을 점점 더 추구하고 있습니다.

식품 제조 부문은 38.3%의 점유율을 차지했으며, 2024년에는 5억 8,730만 달러를 창출했습니다. 이 분야가 리드하고 있는 것은, 일관성 있고, 확장성 있고, 커스터마이즈 가능한 원단 처방을 필요로 하는 포장 식품 및 냉동 식품 제조업체나 프라이빗 브랜드로부터의 수요가 높아지고 있기 때문입니다. 프리믹스는 대규모 베이커리 사업에 있어서 생산 공정의 합리화와 균일성의 확보에 공헌하고 있습니다. 대규모 공업용, 중규모, 장인적인 베이커리를 포함한 상업용 제빵도, 바로 사용할 수 있는 프리믹스 혁신의 혜택을 받고 있습니다. 한편, 체인 레스토랑, 독립형 음식점, 업소용 주방 등의 외식 산업은, 편리성의 향상과 조리 시간의 단축을 위해서 프리믹스를 이용하고 있습니다.

유럽의 도우 기반 프리믹스 2024년 시장 점유율은 37.9%였습니다. 이 대륙은 베이커리 문화가 뿌리 깊고, 장인기술을 구사한 구운 과자와 업무용 구운 과자의 소비가 높은 것, Lesaffre, Puratos, Eurogerm과 같은 베이커리 솔루션의 노포 기업이 존재하는 것이, 이 대륙의 우위성에 기여하고 있습니다. 독일, 프랑스, 영국과 같은 나라들은, 편리성이 높고, 클린 라벨로, 건강 증진에 도움이 되는 빵 생지 제품에 대한 수요에 힘입어, 주요한 견인역이 되고 있습니다. 유럽연합(EU)이 정하는 엄격한 품질 기준이나, 영양 강화, 글루텐 프리, 유기 베이커리용 프리믹스에의 관심의 고조가, 제품 혁신 및 시장 성장을 계속해 뒷받침하고 있습니다.

Archer Daniels Midland Company(ADM), General Mills, Cargill Incorporated, Dawn Foods, and Puratos 그룹과 같은 주요 기업은 기술 혁신 능력과 광범위한 유통망으로 두드러지며 시장 환경 형성에 매우 중요한 역할을 합니다. 도우 기반 프리믹스 시장에 있어서의 발판을 굳히기 위해, 각사는 현재의 건강 동향에 따른 클린 라벨, 글루텐 프리, 영양 강화 제제를 개발해, 계속적인 제품 혁신에 주력하고 있습니다. 각사는 연구 개발에 투자해, 여러가지 지역의 기호나 용도에 맞춘 커스터마이즈 가능한 프리믹스를 개발하고 있습니다. 외식업체, 소매 체인, 대규모 베이커리와의 전략적 파트너십 및 협력 관계에 의해, 이러한 기업은 사업 범위를 확대해, 시장의 요구에 신속하게 대응할 수 있습니다. 게다가 각사는, 제품의 품질을 유지해 세계의 유통을 서포트하기 위해서, 고도의 콜드 체인 로지스틱스를 채용해 공급망을 강화하고 있습니다. 마케팅 활동도, 편리성, 영양, 지속 가능성에 관한 소비자 교육을 중시해, 브랜드 로열티와 시장 침투를 높이고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 유형별

- 장래 시장 동향

- 기술 및 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에서 에너지 효율

- 환경 친화적인 노력

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 빵 및 롤 믹스

- 화이트 빵 믹스

- 통밀 및 특제 팬믹스

- 수제 팬믹스

- 케이크 및 머핀 믹스

- 레이어 케이크 믹스

- 컵케이크 및 머핀 믹스

- 특제 케이크 믹스

- 피자 도우 믹스

- 전통적인 피자 도우

- 얇은 크러스트의 유형

- 글루텐 프리 피자 도우

- 페이스트리 및 쿠키 믹스

- 데니쉬 및 크로와상 믹스

- 쿠키 및 비스킷 믹스

- 특제 패스트리 믹스

- 특수 및 기능성 믹스

- 글루텐 프리 처방

- 유기농 및 깨끗한 라벨 제품

- 고단백질 및 강화 믹스

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 상업용 베이킹

- 대규모 상업용 빵 공장

- 중규모 상업용 빵집

- 작은 장인 빵집

- 푸드 서비스

- 레스토랑 체인

- 독립계 레스토랑

- 시설 내 푸드 서비스

- 식품 제조

- 포장 식품 제조업체

- 냉동 식품 제조업체

- 프라이빗 라벨 제조업체

- 소매 및 소비자

- 식료품점 및 슈퍼마켓 체인

- 전문 식품점

- 온라인 소매 플랫폼

제7장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접 판매

- 제조업체에서 최종 사용자로

- 계약 제조

- 판매자 및 도매업체

- 푸드 서비스 판매자

- 특수 원료 판매자

- 소매 채널

- 슈퍼마켓 및 하이퍼마켓

- 전문 식품점

- 온라인 소매 플랫폼

- 설비 및 기술 파트너십

- 통합 솔루션 제공업체

- 기술 플랫폼 파트너십

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Dawn Foods

- Lesaffre Group

- Puratos Group

- Kerry Group

- General Mills(North America)

- ADM(Archer Daniels Midland)

- Cargill, Incorporated

- Goodman Fielder Food Service(Asia-Pacific)

- Eurogerm KB

- Ardent Mills

- Lallemand Baking

- FRITSCH Group

- Rheon Automatic Machinery

- Rondo AG

The Global Dough-Based Premixes Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 3 billion by 2034. Dough-based premixes are ready-made blends of baking ingredients such as flour, leavening agents, enzymes, and emulsifiers designed to simplify dough preparation for products like bread, rolls, pastries, pizzas, and muffins. These premixes ensure consistency, save preparation time, and provide convenience for both commercial bakers and home consumers. The market is steadily growing as demand rises for products that offer time efficiency and consistent quality. Key opportunities lie in clean-label options, gluten-free formulations, innovative product launches, and fortified mixes. This growth is further fueled by the expansion of foodservice chains, urbanization, and the rising trend of home baking in emerging economies.

Innovations in cold chain logistics, customizable premix solutions, and the inclusion of functional ingredients like oat-based, high-protein, and fiber-enriched blends are creating new avenues in packaged foods, quick-service restaurants, and retail markets. As health consciousness and convenience trends continue to rise worldwide, dough-based premixes are increasingly recognized as vital components in creating the next generation of bakery products and solutions. Consumers are demanding baked goods that not only save time but also meet higher standards for nutrition and clean-label ingredients. This shift is driving innovation in premix formulations to include options that are gluten-free, fortified with vitamins and minerals, and enriched with functional fibers and proteins.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $3 Billion |

| CAGR | 7.1% |

The bread and roll premixes segment dominated the market in 2024, holding a 54.1% share and was valued at USD 827.4 million. This segment's leadership stems from the widespread demand for white, whole grain, specialty, and artisanal bread mixes across retail and industrial baking sectors. Consumers increasingly seek bread options that are not only timesaving but also nutritious and versatile enough to meet both health trends and traditional preferences.

The food manufacturing segment held a 38.3% share and generated USD 587.3 million in 2024. This sector leads due to rising demand from packaged and frozen food producers as well as private label brands requiring consistent, scalable, and customizable dough formulas. Premixes contribute to streamlining production processes and ensuring uniformity in large-scale bakery operations. Commercial baking-which includes large industrial, medium-scale, and artisanal bakeries-also benefits from ready-to-use premix innovations. Meanwhile, foodservice establishments such as chain restaurants, standalone eateries, and institutional kitchens rely on premixes to enhance convenience and reduce preparation time.

Europe Dough-Based Premixes Market held a 37.9% share in 2024. The continent's strong baking culture, high consumption of both artisanal and industrial baked goods, and the presence of established bakery solutions companies like Lesaffre, Puratos, and Eurogerm contribute to its dominance. Countries like Germany, France, and the United Kingdom are key drivers, propelled by demand for convenient, clean-label, and health-enhanced dough products. Strict quality standards set by the European Union and rising interest in fortified, gluten-free, and organic bakery premixes continue to fuel product innovation and market growth.

Leading players such as Archer Daniels Midland Company (ADM), General Mills, Cargill Incorporated, Dawn Foods, and Puratos Group stand out for their innovation capabilities and broad distribution networks, playing pivotal roles in shaping the market landscape. To strengthen their foothold in the dough-based premixes market, companies focus on continuous product innovation by developing clean-label, gluten-free, and fortified formulations that align with current health trends. They invest in R&D to create customizable premixes tailored to different regional tastes and applications. Strategic partnerships and collaborations with foodservice providers, retail chains, and large-scale bakers allow these firms to expand their reach and respond quickly to market needs. Additionally, companies enhance their supply chains by adopting advanced cold chain logistics to maintain product quality and support global distribution. Marketing efforts also emphasize consumer education around convenience, nutrition, and sustainability to boost brand loyalty and market penetration.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Bread and roll mixes

- 5.2.1 White bread mixes

- 5.2.2 Whole grain and specialty bread mixes

- 5.2.3 Artisanal bread mixes

- 5.3 Cake and muffin mixes

- 5.3.1 Layer cake mixes

- 5.3.2 Cupcake and muffin mixes

- 5.3.3 Specialty cake mixes

- 5.4 Pizza dough mixes

- 5.4.1 Traditional pizza dough

- 5.4.2 Thin crust varieties

- 5.4.3 Gluten-free pizza dough

- 5.5 Pastry and cookie mixes

- 5.5.1 Danish and croissant mixes

- 5.5.2 Cookie and biscuit mixes

- 5.5.3 Specialty pastry mixes

- 5.6 Specialty and functional mixes

- 5.6.1 Gluten-free formulations

- 5.6.2 Organic and clean label products

- 5.6.3 High-protein and fortified mixes

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Commercial baking

- 6.2.1 Large-scale industrial bakeries

- 6.2.2 Medium-scale commercial bakeries

- 6.2.3 Small artisanal bakeries

- 6.3 Food service

- 6.3.1 Restaurant chains

- 6.3.2 Independent restaurants

- 6.3.3 Institutional food service

- 6.4 Food manufacturing

- 6.4.1 Packaged food producers

- 6.4.2 Frozen food manufacturers

- 6.4.3 Private label manufacturers

- 6.5 Retail and consumer

- 6.5.1 Grocery and supermarket chains

- 6.5.2 Specialty food stores

- 6.5.3 Online retail platforms

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Direct sales

- 7.2.1 Manufacturer to end-user

- 7.2.2 Contract manufacturing

- 7.3 Distributors and wholesalers

- 7.3.1 Food service distributors

- 7.3.2 Specialty ingredient distributors

- 7.4 Retail channels

- 7.4.1 Supermarkets and hypermarkets

- 7.4.2 Specialty food stores

- 7.4.3 Online retail platforms

- 7.5 Equipment and technology partnerships

- 7.5.1 Integrated solutions providers

- 7.5.2 Technology platform partnerships

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 1.1 Key trends

- 1.2 North America

- 1.2.1 U.S.

- 1.2.2 Canada

- 1.3 Europe

- 1.3.1 Germany

- 1.3.2 UK

- 1.3.3 France

- 1.3.4 Spain

- 1.3.5 Italy

- 1.3.6 Netherlands

- 1.3.7 Rest of Europe

- 1.4 Asia Pacific

- 1.4.1 China

- 1.4.2 India

- 1.4.3 Japan

- 1.4.4 Australia

- 1.4.5 South Korea

- 1.4.6 Rest of Asia Pacific

- 1.5 Latin America

- 1.5.1 Brazil

- 1.5.2 Mexico

- 1.5.3 Argentina

- 1.5.4 Rest of Latin America

- 1.6 Middle East and Africa

- 1.6.1 Saudi Arabia

- 1.6.2 South Africa

- 1.6.3 UAE

- 1.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Dawn Foods

- 9.2 Lesaffre Group

- 9.3 Puratos Group

- 9.4 Kerry Group

- 9.5 General Mills (North America)

- 9.6 ADM (Archer Daniels Midland)

- 9.7 Cargill, Incorporated

- 9.8 Goodman Fielder Food Service (Asia-Pacific)

- 9.9 Eurogerm KB

- 9.10 Ardent Mills

- 9.11 Lallemand Baking

- 9.12 FRITSCH Group

- 9.13 Rheon Automatic Machinery

- 9.14 Rondo AG