|

시장보고서

상품코드

1844381

고정식 해상 풍력에너지 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Fixed Offshore Wind Energy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

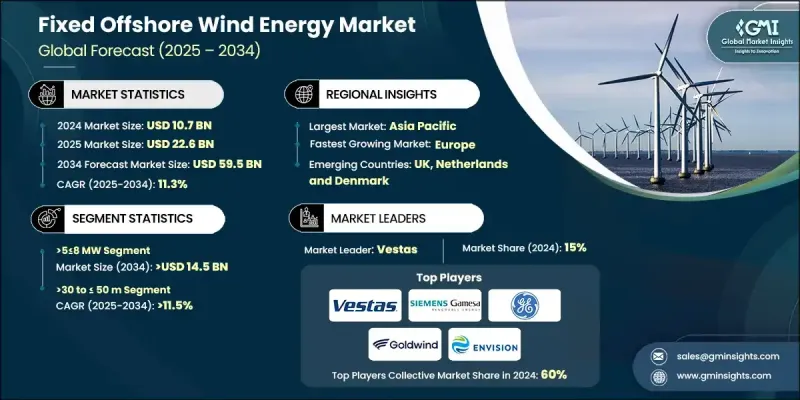

세계의 고정식 해상 풍력에너지 시장은 2024년 107억 달러로 평가되었으며 CAGR 11.3%를 나타내 2034년 595억 달러에 이를 것으로 추정됩니다.

성장의 주요 요인은 정부의 지원책, 연안지역에서의 에너지 수요 증가, 이산화탄소 배출량 감축에 대한 관심 증가 등입니다. 일부 지역의 정책 입안자들은 해양 풍력 개발을 가속화하기 위해 신재생 에너지 의무화, 재정적인센티브, 경매 틀을 전개하고 있습니다. 인구밀도가 높은 해안지역에서는 깨끗하고 효율적인 에너지원이 필요하며, 강력하고 안정적인 해상풍력자원을 이용할 수 있기 때문에 해상풍력은 계속 현실적인 선택이 되고 있습니다. 또한 이 프로젝트는 송전 손실을 줄이고 도시 지역과 산업 지역으로의 전력 공급 효율을 향상시킵니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 107억 달러 |

| 예측 금액 | 595억 달러 |

| CAGR | 11.3% |

보다 큰 용량의 터빈은 신뢰성과 성능을 높이고 유지 보수 비용을 줄이는 최신 기술을 통해 운전 출력을 밀어 올리는 데 큰 역할을합니다. 기초 구조, 블레이드 설계 및 건설 기술의 혁신은 설치 일정을 최적화하고 자본 지출을 줄입니다. 또한 주요 시장 진출 기업은 장기적인 비용 경쟁력을 확보하면서 생산 규모를 확대하기 위해 연구 개발에 투자하고 있습니다. 그리드 통합 개선과 용량 활용도 극대화를 위한 전략적 진보는 고정식 해상 풍력에너지분야의 지속적인 성장을 위한 기반을 구축하고 있습니다.

2MW 이하의 분야는 섬섬 설치, 얕은 연안지대, 계통 인프라가 제한된 저 수요 지역 등 소규모 프로젝트에 대한 적응성에 의해 지원되며, 2034년까지 80억 달러에 달할 것으로 예측됩니다. 이 터빈은 본격적인 해상 농장이 실행 불가능한 시장에 이상적입니다.

30m 이상 50m 이하의 분야는 깊은 수심에서의 전개를 가능하게 하는 기술의 진보에 추진되어 270억 달러에 달할 것으로 예측되고 있습니다. 해안 풍력 발전 프로젝트는 발전 용량을 늘리기 위해 수심이 깊은 곳에서 빠르게 확대되고 있습니다. 게다가 부유식 플랫폼과 보다 심해의 해상 터빈 프로젝트를 촉진하는 것을 목적으로 하는 정부의 지원에 의한 보조금이 업계를 재형성해, 이전에는 고정 구조물에서는 실현 불가능하다고 생각되었던 지역에서의 비즈니스 기회를 끌어내고 있습니다.

미국의 고정식 해상 풍력에너지 시장은 2024년 18억 달러로 평가됐습니다. 미국은 해상풍력발전의 성장거점으로서 임대와 허가 등의 인센티브제도와 프로젝트 고유의 틀을 지속적으로 실시하고 있으며, 주요 연안지역에서의 전개를 강화하고 있습니다. 에너지 대기업은 동해안의 설비투자를 통해 장기적인 헌신을 하고 있으며, 이 지역의 산업이 힘차게 전진하고 있음을 보여주고 있습니다.

세계 고정식 해상 풍력에너지 시장의 주요 기업으로는 Southwire Company, Impsa, Iberdrola, Enessere, Equinor, Siemens Gamesa Renewable Energy, Vattenfall, Goldwind, 스미토모 전기공업, Nexans, General Electric, GE Vernova, China Three Gorges, RWE & System, 후루카와 전공, SSE Renewables, Vestas 등이 있습니다. 고정식 해상 풍력에너지 시장의 지위를 강화하기 위해 기업은 장기적인 합작사업, 제조능력 확대, 비용구조 개선을 위한 공급망 현지화에 주력하고 있습니다. 많은 기업들이 대규모 해외 허브에 투자하고 장기 계약을 보장하기 위해 정부 및 지역 전력 회사와 전략적 파트너십을 구축하고 있습니다. 터빈 포트폴리오의 다양화, 모듈 설계 개선, 스마트 모니터링 기술의 통합도 전략의 중심이 되었습니다. 터빈의 효율, 기초의 유형, 디지털 자산 관리의 기술 혁신에 대한 주력을 강화함으로써, 이들 기업은 에너지 수율과 운영 효율성을 향상시키고, 궁극적으로 해상 풍력 발전의 전개에서 국제 경쟁력을 강화할 수 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 에코시스템

- 규제 상황

- 가격 동향 분석(2021-2034년)

- 터빈 정격별

- 지역별

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석 : 지역별

- 북미

- 유럽

- 아시아태평양

- 세계 기타 지역

- 전략적 대시보드

- 전략적 노력

- 기업 벤치마킹

- 혁신과 기술의 상황

제5장 시장 규모와 예측 : 터빈 정격별(2021-2034년)

- 주요 동향

- 2MW 미만

- 2-5MW 이상

- 5-8MW

- 8-10MW 이상

- 10-12MW

- 12MW 이상

제6장 시장 규모와 예측 : 축별(2021-2034년)

- 주요 동향

- 수평형

- 상풍형

- 하풍형

- 수직

제7장 시장 규모와 예측 : 구성 요소별(2021-2034년)

- 주요 동향

- 블레이드

- 타워

- 기타

제8장 시장 규모와 예측 : 깊이별(2021-2034년)

- 주요 동향

- 0-30m

- 30-50m 이상

- 50m 이상

제9장 시장 규모와 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 스페인

- 영국

- 프랑스

- 이탈리아

- 스웨덴

- 폴란드

- 덴마크

- 포르투갈

- 네덜란드

- 아일랜드

- 벨기에

- 아시아태평양

- 중국

- 인도

- 호주

- 일본

- 한국

- 베트남

- 필리핀

- 대만

제10장 기업 프로파일

- China Three Gorges

- Enessere

- Equinor

- Furukawa Electric

- General Electric

- GE Vernova

- Goldwind

- Impsa

- Iberdrola

- JERA

- Ls Cable &System

- Nexans

- Prysmian Group

- RWE Renewables

- SSE Renewables

- Sumitomo Electric Industries

- Southwire Company

- Siemens Gamesa Renewable Energy

- Vestas

- Vattenfall

The Global Fixed Offshore Wind Energy Market was valued at USD 10.7 billion in 2024 and is estimated to grow at a CAGR of 11.3% to reach USD 59.5 billion by 2034.

The growth is primarily driven by a combination of supportive government initiatives, rising energy demand in coastal zones, and heightened focus on cutting carbon emissions. Policymakers across several regions are rolling out renewable energy mandates, financial incentives, and auction frameworks to accelerate offshore wind development. With densely populated coastal regions requiring clean and efficient energy sources, the availability of strong and consistent offshore wind resources continues to make this technology a practical choice. These projects also reduce transmission losses and improve electricity delivery efficiency to urban and industrial zones.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.7 Billion |

| Forecast Value | $59.5 Billion |

| CAGR | 11.3% |

Higher-capacity turbines are playing a major role in pushing operational output, with newer technologies enhancing reliability, performance, and lowering maintenance costs. Innovations in foundation structures, blade design, and construction techniques are optimizing installation timelines and reducing capital expenditure. Moreover, major market players are channeling investments into R&D to scale up production while ensuring long-term cost competitiveness. Strategic advancements, aimed at improving grid integration and maximizing capacity utilization, are laying the foundation for sustained growth in the fixed offshore wind energy space.

The <= 2 MW segment is expected to reach USD 8 billion by 2034, supported by its adaptability in smaller-scale projects such as island installations, shallow coastal zones, and low-demand areas with limited grid infrastructure. These turbines are ideal for markets where full-scale offshore farms are not viable. Increased interest in hybrid energy systems and incentives across developing countries will add further momentum to this segment's growth trajectory.

The >30 to <=50 m segment is forecast to reach USD 27 billion, fueled by technological advancements that allow for deployment at greater water depths. Coastal wind projects are expanding rapidly in deeper waters to increase power generation capacity. Additionally, government-backed subsidies aimed at promoting floating platforms and deeper offshore turbine projects are reshaping the industry, unlocking opportunities in areas previously considered non-viable for fixed structures.

U.S. Fixed Offshore Wind Energy Market was valued at USD 1.8 billion in 2024. As a growing hub for offshore wind, the U.S. continues to implement incentive schemes and project-specific frameworks, such as leasing and permitting initiatives, that are bolstering deployment along key coastal regions. Energy giants are making long-term commitments through capital investments along the East Coast, signaling strong forward momentum in the regional industry.

Leading companies in the Global Fixed Offshore Wind Energy Market include Southwire Company, Impsa, Iberdrola, Enessere, Equinor, Siemens Gamesa Renewable Energy, Vattenfall, Goldwind, Sumitomo Electric Industries, Nexans, General Electric, GE Vernova, China Three Gorges, RWE Renewables, JERA, Prysmian Group, LS Cable & System, Furukawa Electric, SSE Renewables, and Vestas. To strengthen their position in the fixed offshore wind energy market, companies are focusing on long-term joint ventures, expanding manufacturing capabilities, and localizing supply chains to improve cost structures. Many are investing in large-scale offshore hubs and building strategic partnerships with governments and regional utilities to secure long-term contracts. Diversifying turbine portfolios, improving modular design, and integrating smart monitoring technologies have also become central to their strategy. Enhanced focus on innovation in turbine efficiency, foundation types, and digital asset management allows these firms to improve energy yield and operational efficiency, ultimately reinforcing their global competitiveness in offshore wind deployment.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.1.3 Base estimates and calculations

- 1.1.4 Base year calculation

- 1.1.5 Key trends for market estimates

- 1.2 Forecast model

- 1.3 Primary research & validation

- 1.3.1 Primary sources

- 1.4 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360-degree synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Turbine rating trends

- 2.4 Axis trends

- 2.5 Component trends

- 2.6 Depth trends

- 2.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Price trend analysis, 2021-2034

- 3.3.1 By turbine rating

- 3.3.2 By region

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Rest of World

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Turbine rating, 2021 - 2034 (USD Million & MW)

- 5.1 Key trends

- 5.2 ≤ 2 MW

- 5.3 >2≤ 5 MW

- 5.4 >5≤ 8 MW

- 5.5 >8≤10 MW

- 5.6 >10≤ 12 MW

- 5.7 > 12 MW

Chapter 6 Market Size and Forecast, By Axis, 2021 - 2034 (USD Million & MW)

- 6.1 Key trends

- 6.2 Horizontal

- 6.2.1 Up-wind

- 6.2.2 Down-wind

- 6.3 Vertical

Chapter 7 Market Size and Forecast, By Component, 2021 - 2034 (USD Million & MW)

- 7.1 Key trends

- 7.2 Blades

- 7.3 Towers

- 7.4 Others

Chapter 8 Market Size and Forecast, By Depth, 2021 - 2034 (USD Million & MW)

- 8.1 Key trends

- 8.2 >0 ≤ 30 m

- 8.3 >30 ≤ 50 m

- 8.4 > 50 m

Chapter 9 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & MW)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 Spain

- 9.3.3 UK

- 9.3.4 France

- 9.3.5 Italy

- 9.3.6 Sweden

- 9.3.7 Poland

- 9.3.8 Denmark

- 9.3.9 Portugal

- 9.3.10 Netherlands

- 9.3.11 Ireland

- 9.3.12 Belgium

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Australia

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.4.6 Vietnam

- 9.4.7 Philippines

- 9.4.8 Taiwan

Chapter 10 Company Profiles

- 10.1 China Three Gorges

- 10.2 Enessere

- 10.3 Equinor

- 10.4 Furukawa Electric

- 10.5 General Electric

- 10.6 GE Vernova

- 10.7 Goldwind

- 10.8 Impsa

- 10.9 Iberdrola

- 10.10 JERA

- 10.11 Ls Cable & System

- 10.12 Nexans

- 10.13 Prysmian Group

- 10.14 RWE Renewables

- 10.15 SSE Renewables

- 10.16 Sumitomo Electric Industries

- 10.17 Southwire Company

- 10.18 Siemens Gamesa Renewable Energy

- 10.19 Vestas

- 10.20 Vattenfall