|

시장보고서

상품코드

2071209

자동차용 5G 모듈 및 안테나 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2026-2035년)Automotive 5G Modules and Antenna Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

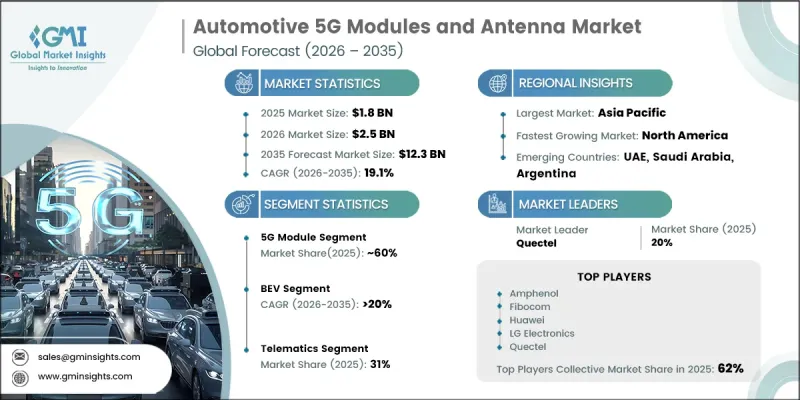

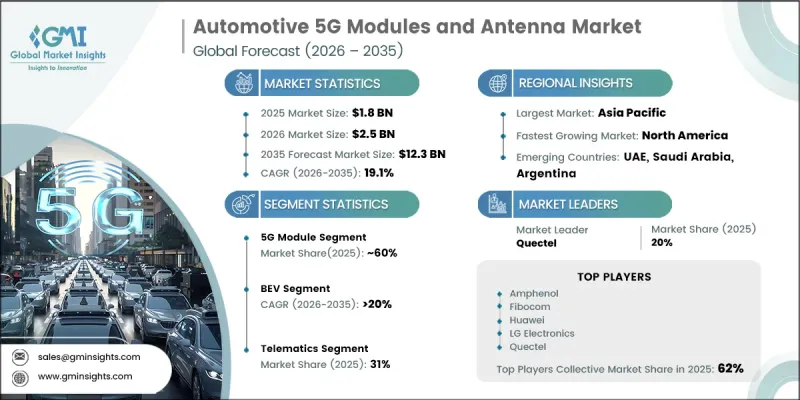

세계의 자동차용 5G 모듈 및 안테나 시장은 2025년에 18억 달러 규모에 달하고, CAGR 19.1%로 성장하여 2035년까지 123억 달러에 달할 것으로 추정됩니다.

자동차 업계가 커넥티드카 및 자율주행차 기술의 통합을 가속화하고 있는 가운데, 해당 시장은 급속한 성장을 이루고 있습니다. 현대 자동차의 디지털화가 진전됨에 따라, 지속적인 데이터 전송과 실시간 연결성을 지원할 수 있는 고속 통신 솔루션에 대한 수요가 크게 증가하고 있습니다. 자동차 제조사들은 차량의 지능화, 운영 효율성 및 연결 기능을 향상시키기 위해 첨단 통신 시스템을 점점 더 많이 도입하고 있습니다. 클라우드 기반 서비스, 소프트웨어 주도형 차량 기능, 그리고 차세대 모빌리티 플랫폼에 대한 의존도가 높아짐에 따라, 견고한 5G 모듈 및 안테나 기술에 대한 수요는 더욱 증가하고 있습니다. 이러한 솔루션은 차량과 외부 네트워크 간의 신뢰할 수 있는 통신을 가능하게 할 뿐만 아니라, 커넥티드 교통 생태계 전반에 걸친 원활한 데이터 교환을 지원합니다. 지능형 모빌리티로의 전환은 통신 인프라 및 차량 연결 기술에 대한 투자도 촉진하고 있습니다. 자동차 제조사들이 사용자 경험 향상, 안전 기능 강화, 그리고 첨단 디지털 서비스 제공에 주력함에 따라, 자동차용 5G 모듈 및 안테나 시스템에 대한 수요는 크게 증가할 것으로 예상됩니다. 무선 통신 기술의 지속적인 발전과 커넥티드카 네트워크의 확대는 전 세계 자동차용 5G 모듈 및 안테나 시장에 계속해서 유리한 성장 기회를 창출하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 18억 달러 |

| 예측 금액 | 123억 달러 |

| CAGR | 19.1% |

자동차용 5G 모듈 및 안테나 시장은 커넥티드 모빌리티 네트워크의 급속한 확장에 힘입어 성장하고 있습니다. V2X(Vehicle-to-Everything) 통신 프레임워크의 도입 확대에 따라, 운송 분야 전반에서 자동차용 5G 통신 기술의 도입이 가속화되고 있습니다. 지능형 교통 인프라에 대한 공공 및 민간 투자를 통해, 차량은 주변 모빌리티 네트워크와 실시간으로 데이터를 교환할 수 있게 되었습니다. 커넥티드 교통 시스템이 지속적으로 발전함에 따라, 초저지연, 네트워크 신뢰성 향상, 통신 효율 향상을 실현할 수 있는 첨단 5G 모듈 및 멀티밴드 안테나 솔루션에 대한 수요가 증가하고 있습니다. 이러한 기술들은 스마트 모빌리티 생태계와 미래 교통 네트워크의 확장을 뒷받침하는 데 중요한 역할을 하고 있습니다.

5G 모듈 부문은 2025년에 60%의 시장 점유율을 차지했으며, 2026년부터 2035년까지 연평균 성장률(CAGR) 19%를 기록할 것으로 전망됩니다. 커넥티드카 기능에 대한 수요 증가가 이 부문의 성장을 이끄는 주요 요인이 되고 있습니다. 현대 차량에서는 다양한 디지털 서비스와 데이터 집약형 애플리케이션을 지원하기 위해 고속 연결에 대한 끊김 없는 접근이 점점 더 요구되고 있습니다. 기존 통신 기술에 비해 5G 모듈은 훨씬 더 넓은 대역폭과 낮은 지연 시간을 실현하여, 차량, 디지털 플랫폼, 모빌리티 생태계 간의 효율적인 통신을 가능하게 합니다. 이러한 기능 덕분에 5G 모듈은 차세대 자동차용 커넥티비티 솔루션에서 필수적인 구성요소가 되었습니다.

배터리 전기자동차(BEV) 부문은 2025년에 44%의 시장 점유율을 차지했으며, 2035년까지 연평균 성장률(CAGR) 20%로 성장할 것으로 전망됩니다. BEV의 보급이 확대됨에 따라, 점점 더 고도화되는 차량 기능을 지원할 수 있는 첨단 통신 하드웨어에 대한 수요가 크게 증가하고 있습니다. 커넥티드 기술은 전기자동차 분야에서 차량 성능 최적화, 운영 효율 향상, 그리고 디지털 서비스 제공에 없어서는 안 될 요소가 되고 있습니다. 5G 연결을 통한 속도 향상과 응답성 개선으로 인해, 커넥티드 모빌리티 네트워크 전반에 걸쳐 원활한 상호작용이 가능해졌으며, 차량 기능, 고객 편의성 및 전기 교통 시스템 전체의 효율성이 향상되고 있습니다.

중국의 자동차용 5G 모듈 및 안테나 시장은 45%의 점유율을 차지했으며, 2025년에는 2억 7,870만 달러의 시장 규모를 기록했습니다. 이 나라의 확고한 입지는 5G 네트워크 인프라에 대한 대규모 투자와 차세대 통신 구축에 있어 보여준 리더십에 힘입은 것입니다. 첨단 무선 네트워크의 광범위한 보급은 커넥티드카 기술과 디지털 모빌리티 서비스를 위한 견고한 기반을 마련했습니다. 이러한 첨단 연결성을 통해 자동차 제조사들은 국내에서 급속히 성장하고 있는 자동차 생태계 전반에 걸쳐 첨단 텔레매틱스 솔루션, 클라우드 기반 차량 서비스 및 V2X 통신 기능을 확대할 수 있게 되었습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품별, 2022-2035년

제6장 시장 추정 및 예측 : 추진력별, 2022-2035년

제7장 시장 추정 및 예측 : 용도별, 2022-2035년

제8장 시장 추정 및 예측 : 차량별, 2022-2035년

제9장 시장 추정 및 예측 : 판매 채널별, 2022-2035년

제10장 시장 추정 및 예측 : 지역별, 2022-2035년

제11장 기업 개요

KSMThe Global Automotive 5G Modules and Antenna Market was valued at USD 1.8 billion in 2025 and is estimated to grow at a CAGR of 19.1% to reach USD 12.3 billion by 2035.

The market is experiencing rapid growth as the automotive industry accelerates the integration of connected and autonomous vehicle technologies. Increasing digitalization across modern vehicles is creating strong demand for high-speed communication solutions capable of supporting continuous data transmission and real-time connectivity. Automakers are increasingly incorporating advanced communication systems to improve vehicle intelligence, operational efficiency, and connectivity capabilities. The growing reliance on cloud-based services, software-driven vehicle functions, and next-generation mobility platforms is further strengthening the need for robust 5G modules and antenna technologies. These solutions enable reliable communication between vehicles and external networks while supporting seamless data exchange across connected transportation ecosystems. The shift toward intelligent mobility is also encouraging investments in communication infrastructure and vehicle connectivity technologies. As automotive manufacturers focus on delivering enhanced user experiences, improved safety features, and advanced digital services, demand for automotive 5G modules and antenna systems is expected to increase substantially. Ongoing advancements in wireless communication technologies and the expansion of connected vehicle networks continue to create favorable growth opportunities for the Automotive 5G Modules and Antenna Market worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.8 Billion |

| Forecast Value | $12.3 Billion |

| CAGR | 19.1% |

The Automotive 5G Modules and Antenna Market is benefiting from the rapid expansion of connected mobility networks. The growing deployment of Vehicle-to-Everything (V2X) communication frameworks is accelerating the adoption of automotive 5G communication technologies across the transportation sector. Public and private investments in intelligent transportation infrastructure are enabling vehicles to exchange data with surrounding mobility networks in real time. As connected transportation systems continue to evolve, demand is increasing for advanced 5G modules and multi-band antenna solutions capable of delivering ultra-low latency, improved network reliability, and enhanced communication efficiency. These technologies play an important role in supporting the expansion of smart mobility ecosystems and future transportation networks.

The 5G module segment accounted for 60% share in 2025 and is anticipated to register a CAGR of 19% between 2026 and 2035. Rising demand for connected vehicle functionalities is a primary factor driving segment growth. Modern vehicles increasingly require uninterrupted access to high-speed connectivity to support a wide range of digital services and data-intensive applications. Compared with previous communication technologies, 5G modules deliver significantly higher bandwidth and reduced latency, enabling efficient communication between vehicles, digital platforms, and mobility ecosystems. These capabilities are making 5G modules a critical component of next-generation automotive connectivity solutions.

The battery electric vehicle (BEV) segment held a 44% share in 2025 and is projected to grow at a CAGR of 20% through 2035. The rising adoption of BEVs is creating substantial demand for advanced communication hardware that can support increasingly sophisticated vehicle functions. Connected technologies have become essential for optimizing vehicle performance, improving operational efficiency, and delivering digital services in electric vehicles. The enhanced speed and responsiveness of 5G connectivity enable seamless interaction across connected mobility networks, improving vehicle functionality, customer convenience, and the overall efficiency of electric transportation systems.

China Automotive 5G Modules and Antenna Market held 45% share, generating USD 278.7 million in 2025. The country's strong position is supported by extensive investments in 5G network infrastructure and its leadership in next-generation communication deployment. The widespread availability of advanced wireless networks has established a strong foundation for connected vehicle technologies and digital mobility services. This high level of connectivity is enabling automotive manufacturers to scale advanced telematics solutions, cloud-enabled vehicle services, and V2X communication capabilities across the country's rapidly growing automotive ecosystem.

Key companies operating in the Global Automotive 5G Modules and Antenna Market include Amphenol, Fibocom, Huawei, HUBER+SUHNER, LG Electronics, Quectel, Taoglas, WISI Automotive, Yokowo, and ZTE. Companies operating in the Automotive 5G Modules and Antenna Market are focusing on innovation, strategic collaborations, and geographic expansion to strengthen their competitive position. Leading players are investing heavily in research and development to introduce high-performance 5G modules and advanced antenna solutions capable of supporting evolving connected vehicle requirements. Partnerships with automotive manufacturers, telecommunications providers, and mobility technology companies are helping businesses accelerate product deployment and expand market reach. Many companies are also enhancing manufacturing capabilities and strengthening supply chain networks to meet rising global demand.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 Propulsion

- 2.2.5 Vehicle

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of connected and autonomous vehicles

- 3.2.1.2 Expansion of V2X communication deployments

- 3.2.1.3 Rising demand for software-defined vehicles and OTA updates

- 3.2.1.4 Increasing global 5G network coverage

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High hardware costs limiting mass-market adoption

- 3.2.2.2 Lengthy OEM validation and certification processes

- 3.2.2.3 Spectrum fragmentation across regions

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of 5G mmWave for ADAS and autonomous driving

- 3.2.3.2 Growing BEV and PHEV adoption

- 3.2.3.3 Expansion of smart city and intelligent transportation infrastructure

- 3.2.3.4 Increasing aftermarket retrofit opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Environmental Protection Agency (EPA)

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.3 Federal Communications Commission (FCC)

- 3.4.1.4 U.S. Department of Transportation (DOT)

- 3.4.1.5 Innovation, Science and Economic Development Canada (ISED)

- 3.4.2 Europe

- 3.4.2.1 EU Radio Equipment Directive (RED)

- 3.4.2.2 UNECE WP.29 Cybersecurity Regulation (R155)

- 3.4.2.3 UNECE WP.29 Software Update Regulation (R156)

- 3.4.2.4 CE Marking Compliance

- 3.4.2.5 General Data Protection Regulation (GDPR)

- 3.4.3 Asia Pacific

- 3.4.3.1 China Compulsory Certification (CCC)

- 3.4.3.2 Ministry of Industry and Information Technology (MIIT) 5G Regulations

- 3.4.3.3 Indian Telecommunication Engineering Centre (TEC) Certification

- 3.4.3.4 Japanese Radio Act Certification

- 3.4.3.5 Australian Communications and Media Authority (ACMA) Regulations

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Telecommunications Agency (ANATEL) Certification

- 3.4.4.2 Brazilian National Traffic Council (CONTRAN)

- 3.4.4.3 Mexican Federal Telecommunications Institute (IFT) Regulations

- 3.4.4.4 Regional Telecommunications Equipment Certification Requirements

- 3.4.4.5 Vehicle Connectivity and Spectrum Compliance Regulations

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Telecommunications Regulatory Framework

- 3.4.5.2 Saudi Communications, Space & Technology Commission (CST)

- 3.4.5.3 Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.5.4 South African Independent Communications Authority (ICASA)

- 3.4.5.5 National Vehicle Connectivity and Telecommunications Compliance Requirements

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Trade data analysis (Driven by Paid Research)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis (Driven by Primary Research)

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 5G Modules

- 5.2.1 Embedded Modules

- 5.2.2 Integrated / Multi-band Modules

- 5.2.3 External Modules

- 5.3 Antennas

- 5.3.1 Shark-Fin Antenna

- 5.3.2 Glass / Integrated Antenna

- 5.3.3 Patch & Blade Antenna

- 5.3.4 MIMO Antenna

- 5.3.5 Intelligent Antenna Modules (IAM)

- 5.3.6 Others

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 BEV

- 6.4 PHEV

- 6.5 HEV

- 6.6 FCEV

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Telematics

- 7.3 Infotainment

- 7.4 V2X Communication

- 7.5 ADAS & Autonomous Driving

- 7.6 Emergency & Safety Services

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Passenger car

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial Vehicle

- 8.3.1 Light duty

- 8.3.2 Medium duty

- 8.3.3 Heavy duty

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Southeast Asia

- 10.4.5.1 Indonesia

- 10.4.5.2 Malaysia

- 10.4.5.3 Singapore

- 10.4.5.4 Thailand

- 10.4.5.5 Vietnam

- 10.4.6 ANZ

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Argentina

- 10.5.3 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Amphenol

- 11.1.2 Huawei

- 11.1.3 HUBER+SUHNER

- 11.1.4 Huf

- 11.1.5 LG Electronics

- 11.1.6 MD Elektronik

- 11.1.7 Taoglas

- 11.1.8 WISI Automotive

- 11.1.9 Yokowo

- 11.1.10 ZTE

- 11.2 Regional Players

- 11.2.1 Ace Technologies

- 11.2.2 Calearo

- 11.2.3 Fibocom

- 11.2.4 MeiG Smart

- 11.2.5 Neoway

- 11.2.6 Quectel

- 11.2.7 SIMCom

- 11.3 Emerging Players

- 11.3.1 Flaircomm

- 11.3.2 GosuncnWelink

- 11.3.3 Longsung