|

시장보고서

상품코드

1683961

북미의 자동차용 LED 조명 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)North America Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

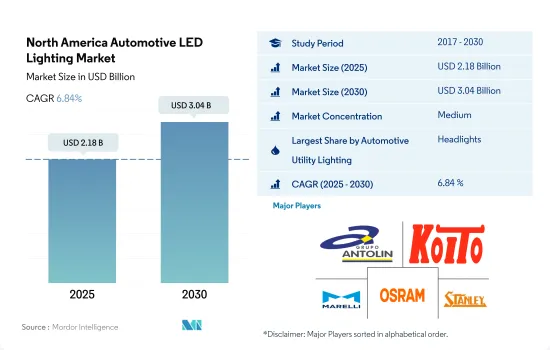

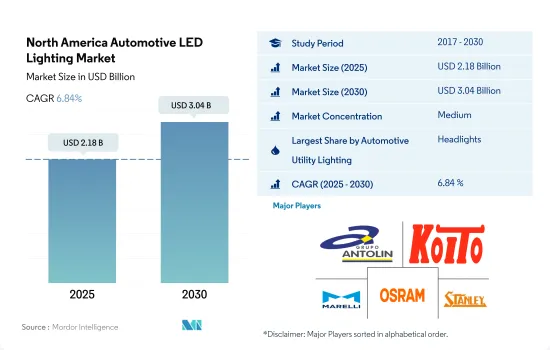

북미의 자동차용 LED 조명 시장 규모는 2025년에 21억 8,000만 달러에 달할 것으로 추정됩니다. 2030년에는 30억 4,000만 달러에 이를 것으로 예상되며, 예측 기간 중(2025-2030년) CAGR은 6.84%를 나타낼 것으로 전망됩니다.

사고 동향 증가, 안개 LED 램프의 보급률, 전기자동차 판매 증가가 시장 성장을 견인

- 금액 기준으로는 2022년에 전조등이 큰 점유율을 차지한 다음 그 밖에(소형 LED 라이트, LED 넘버 플레이트 라이트, 안개등, 실내 LED 라이트), 방향지시등(DSL), 정지등이 뒤를 이었습니다. 시장 점유율은 모든 빛에 평평하고, 기타와 DSL은 약간 감소, 전조등은 늘어날 것으로 예상됩니다. 사고 동향의 상승에 따라 안개 LED 램프의 보급률도 상승할 것으로 예상됩니다. 미국에서는 자동차 사고로 인한 사망자 수가 2022년에는 유행 전 사망률에 비해 추정 4만 6,000명에 달하고, 22% 가까이 증가했습니다.

- 수량 기준으로 2022년에 방향지시등이 큰 점유율을 차지한 다음 전조등, 기타(소형 LED 라이트, LED 번호판 라이트, 안개등, 실내 LED 라이트), 정지등의 순서가 되었습니다. 외등은 모든 유형의 자동차에서 경미한 사고에서 큰 사고까지 영향을 받을 확률이 높고 교체가 필요한 주요 부품입니다.

- 2022년 경차 신차 판매량은 1,370만대에 달했습니다. 2022년 신차 판매 대수는 전년 대비 8.2% 감소했지만, 이것은 주로 마이크로칩 부족의 계속과 추가 공급망의 혼란에 의한 것입니다. 2022년 전신차 판매 대수에서 차지하는 하이브리드차, 플러그인 하이브리드차, 배터리 전기차(BEV)의 비율은 12.3%로 2021년부터 2.7% 증가했습니다. 이와 같이 자동차 판매량 증가로 LED 조명 수요가 증가했습니다.

신흥 국가에서 EV 개발과 지역 자동차 산업을 발전시키는 유리한 법률이 LED 조명 수요를 촉진

- 금액 기준으로 2022년 미국 LED 조명 시장이 점유율의 대부분을 차지한 다음 북미(RONA)가 뒤를 이었습니다. 시장 점유율은 미국이 감소하고 북미 등이 증가할 것으로 예상되며 앞으로 수년간 변동이 적습니다. 미국의 국내 자동차 생산량은 2021년 910만대에서 2022년에는 1,006만대로 증가했습니다. 자동차 생산에는 승용차와 상용차가 포함됩니다. 캐나다에서는 2022년 자동차 생산 대수가 2021년 대비 10.2% 증가하여 120만대가 되었습니다. 국내 자동차 생산량 증가는 시장에 자동차 LED 수요 증가를 가져옵니다.

- EV 수요는 북미의 많은 나라에서 성장했습니다. 멕시코의 2022년 신차 판매 대수는 108만대로 2021년부터 7% 개선되었으며 미국 EV 판매 대수는 2022년 65% 증가했습니다.

- 자동차 산업의 하위 부문에서 미국과 멕시코의 상업 서비스는 OE 부품, 애프터마켓, 전기자동차(EV) 부품에서 강력한 기회를 경험했습니다. 멕시코의 OEM 및 애프터마켓용 자동차 부품 생산량은 2020년 784억 달러에서 2021년 947억 달러로 증가했으며 2022년 1,010억 달러 이상에 이르렀습니다.

- 미국·멕시코·캐나다 협정(USMCA)은 2020년 7월 1일에 발효했습니다. USMCA의 요건은 자동차 내용물의 75%를 북미에서 생산하고, 핵심이 되는 자동차 부품은 미국, 캐나다, 멕시코 중 하나를 원산지로 하는 것입니다. EV의 채용과 현지 자동차 산업의 발전을 위한 유리한 법률 등 위의 요인을 고려하면 향후 수년간 북미 전역에서 LED의 성장이 기대됩니다.

북미의 자동차용 LED 조명 시장 동향

LED 시장을 견인하는 것은 EV와 배터리 제조업체에 의한 자동차 생산 대수 증가를 위한 투자

- 북미의 총 자동차 생산량은 2022년 1,454만대, 2023년 1,506만대에 이르렀습니다. 북미에서 가장 큰 제조 부문 중 하나가 자동차 부문입니다. 그러나 COVID-19 팬데믹은 이 지역의 자동차 산업에 두 가지 큰 충격을 주었으며 2020년과 2021년 생산, 판매, 대외 무역에 큰 악영향을 미쳤습니다. 따라서 자동차 공급망과 생산 혼란은 이 지역의 LED 조명 사업에 부정적인 영향을 미쳤습니다.

- 3월 미국의 경차 생산량은 전년 동월 대비 31% 가까이 감소했습니다. 4월 말 1주일 가동한 공장은 1개뿐이었기 때문에 보다 높은 수준의 경차 생산이 필요했습니다. 자동차 업계에서는 공급망에 대한 우려의 목소리도 올랐습니다. 독일공급업체인 ZF는 미국에 시설을 보유하고 있으며 2020년 5월 말까지 전 세계 고용을 10% 줄일 계획을 밝혔습니다. 세계 공급망의 혼란은 미국 제조에 영향을 미쳤습니다. 이 혼란은 자동차 산업에서 사용되는 반도체에 침체를 가져왔습니다.

- 또한 북미에서는 정부 주도로 EV 수요가 급증하고 있습니다. 인플레이션 감소법이 2022년 8월에 성립되었으며, 그 시점부터 2023년 3월까지 주요 EV 및 배터리 제조업체가 북미 EV 공급망에 최소 520억 달러 상당의 투자를 발표했습니다. 이러한 소비자와 제조업체의 이익으로 이어지는 노력은 이 지역의 LED 조명 사업을 뒷받침할 것으로 보입니다.

전기차 판매 및 LED 조명 성장을 가속하는 정부 투자

- 북미에서 EV 판매의 대부분은 미국, 캐나다, 멕시코에서 가져온 것입니다. 2022년 미국의 BEV 판매 대수는 2021년 대비 65% 증가해 테슬라가 EV 시장을 계속 독점했습니다. 2022년 멕시코의 판매 대수는 총 판매 대수 109만 대 중 완전 전기자동차는 불과 0.5%로, 이 비율은 중국, 유럽, 미국 등 다른 시장을 크게 밑돌았습니다. 캐나다에서는 2022년 4분기에 배터리 전기자동차(BEV)만으로 2만 7,754대, 플러그인 하이브리드 전기자동차(PHEV)에서 5,645대의 신규 등록이 있었습니다.

- 더욱 확대하기 위해 미국 정부는 2021년에 1조 달러 규모의 인프라 법안을 발표했고, 2030년까지 공공 EV 충전기를 50만대 증설하기 위해 75억 달러를 할당했고, 또한 미국 내에서 조립된 EV를 구입하면 7,500 달러의 세제 우대를 제공함으로써 EV 제조에 투자를 했습니다. 또한 EV의 주요 기업 중 하나인 테슬라는 2024년 말까지 미국에서 약 3,500개 슈퍼차저 스테이션과 4,000개 레벨 2 충전 도크를 모든 브랜드의 전기자동차에 제공할 것을 약속했습니다.

- GM 캐나다는 잉가솔과 오샤와 제조 시설을 개조하기 위해 캐나다에 20억 달러 이상을 투자하고 2022년 말까지 전기자동차를 생산했습니다. 2030년까지 미국에서는 조지아, 켄터키, 미시간이 전기자동차 배터리 제조의 대부분을 차지할 것으로 예상됩니다. 이 전기자동차 배터리 제조 능력은 연간 1,000만-1,300만개의 전 전기자동차 배터리의 생산을 촉진하고, 미국을 세계의 EV 경쟁 상대로 자리매김할 것으로 보입니다. 이와 같이 위와 같은 사례는 EV 수요 증가에 따른 새로운 발전소의 개발과 생산으로 이어지며, 이 지역의 자동차용 LED 수요를 끌어올립니다.

북미의 자동차용 LED 조명 산업 개요

북미의 자동차용 LED 조명 시장은 적당히 통합되어 상위 5개사에서 52.69%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. GRUPO ANTOLIN IRAUSA, SA, KOITO MANUFACTURING, Marelli Holdings, OSRAM GmbH. and Stanley Electric(알파벳순 정렬).

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 자동차 생산 대수

- 인구

- 1인당 소득

- 자동차 대출 금리

- 충전소 수

- 자동차 보유 대수

- LED 총 수입량

- 가구수

- 도로 네트워크

- 보급률

- 규제 프레임워크

- 미국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 자동차용 유틸리티 조명

- 주간 주행등(DRL)

- 방향지시등

- 전조등

- 후진등

- 정지등

- 후미등

- 기타

- 자동차용 조명

- 이륜차

- 상용차

- 승용차

- 국가명

- 미국

- 기타 북미

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일(세계 수준 개요, 시장 수준 개요, 주요 사업 부문, 재무, 직원 수, 주요 정보, 시장 순위, 시장 점유율, 제품 및 서비스, 최근 동향 분석 포함)

- GRUPO ANTOLIN IRAUSA, SA

- HELLA GmbH & Co. KGaA(FORVIA)

- 현대모비스

- KOITO MANUFACTURING CO., LTD.

- Marelli Holdings Co., Ltd.

- Nichia Corporation

- OSRAM GmbH.

- Stanley Electric Co., Ltd.

- Valeo

- ZKW Group

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계의 개요

- 개요

- Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The North America Automotive LED Lighting Market size is estimated at 2.18 billion USD in 2025, and is expected to reach 3.04 billion USD by 2030, growing at a CAGR of 6.84% during the forecast period (2025-2030).

Rising accident trend, penetration rate of fog LED lamps, and increasing sales of electric vehicles drive market growth

- In terms of value, in 2022, headlights accounted for a major share, followed by others (miniature LED lights, LED license plate lights, fog lights, and interior LED lights), directional signal lights (DSLs), daytime running lights, and stop lights. The market share is expected to remain the same for all lights, with a small reduction in others and DSLs, and grow for headlights. With the rising accident trend, the penetration rate of fog LED lamps is anticipated to rise. In the US, the number of motor vehicle deaths reached an estimated 46,000 in 2022 compared to the pre-pandemic death rate, an increase of nearly 22%.

- In terms of volume, in 2022, directional signal lights accounted for a major share, followed by headlights, others (miniature LED lights, LED license plate lights, fog lights, and interior LED lights), and stop lights. External lights are the prime parts that have a high probability of getting affected in minor to major accidents in all types of vehicles and require replacement.

- The year 2022 ended with new light-vehicle sales reaching 13.7 million units. The Y-o-Y 2022 sales decreased by 8.2% compared to 2021, with the decrease primarily attributed to the ongoing microchip shortage and additional supply chain disruptions. With sales of hybrid, plug-in hybrid, and battery electric vehicles (BEVs) accounting for 12.3% of all new vehicle sales in 2022, an increase of 2.7% from 2021, alternative fuel vehicles gained market share. Thus, the increase in vehicle sales resulted in an increase in the requirement for LED lights.

Adoption of EVs across countries and favorable laws to develop local automotive industry drive the demand for LED lighting

- In terms of value, in 2022, the US LED light market accounted for the majority of the share, followed by the Rest of North America (RONA). The market share is expected to decline for the US and increase for the Rest of North America, with less fluctuation in the coming years. The domestic vehicle production in the US increased from 9.1 million units in 2021 to 10.06 million units in 2022. The vehicle production includes cars and commercial vehicles. In Canada, in 2022, vehicle production increased by 10.2% compared to 2021, accounting for 1.2 million units. The increase in domestic vehicle production creates more demand for automotive LEDs in the market.

- The demand for EVs grew across many countries in North America. Mexico saw 1.08 million new car sales in 2022, a 7% improvement from 2021, and US EV sales increased by 65% in 2022.

- In sub-sectors of the automotive industry, the US and Mexican commercial services experienced strong opportunities in OE parts, aftermarket, and electric vehicle (EV) parts. The value of Mexican automotive parts for OEMs and aftermarket production increased from USD 78.4 billion in 2020 to USD 94.7 billion in 2021, and it is expected to reach more than USD 101 billion by 2022.

- The United States, Mexico, Canada Agreement (USMCA) went into effect on July 1, 2020. The USMCA requirement stated that 75% of a vehicle's content must be produced in North America and that core auto parts originate from the United States, Canada, or Mexico. Considering the above-mentioned factors, such as the adoption of EVs and favorable laws to develop the local automotive industry, the growth of LEDs is expected across North America in the coming years.

North America Automotive LED Lighting Market Trends

The LED market is driven by investments by EVs and battery producers to increase automotive production

- The total automobile vehicle production in North America was 14.54 million units in 2022, and it is expected to reach 15.06 million units in 2023. One of the biggest manufacturing sectors in North America is the automotive sector. However, the COVID-19 pandemic caused two significant shocks to the region's automobile industry, which had a significant negative impact on production, sales, and foreign trade in 2020 and 2021. Thus, the disruption in the supply chain and production of automotive vehicles negatively affected the LED lighting business in the region.

- March saw an almost 31% year-over-year fall in the US light car production. Only one plant was operating for one week at the end of April, so there needed to be a higher level of light vehicle production. The auto industry also voiced concerns regarding its supply networks. ZF, a German supplier, has facilities in the United States and revealed plans to reduce its global employment by 10% by the end of May 2020. Several worldwide supply chain disruptions impacted manufacturing in the United States: Mercedes-Benz resumed its Vance, Alabama, facility on April 27; however, due to a scarcity of parts, production had to be briefly halted on May 15. This disruption created a downfall in semiconductors used in the automotive industry.

- Further, the demand for EVs is rapidly increasing in North America due to government initiatives. The Inflation Reduction Act was passed in August 2022, and between that time and March 2023, major EV and battery producers announced investments in North American EV supply chains worth at least USD 52 billion. Such initiatives in the interest of consumers and manufacturers will boost the LED lighting business in the region.

Government investments to drive the sales of electric vehicle and propel the growth of LED lighting

- Most of the EV sales in the North American region come from the US, Canada, and Mexico. In 2022, US BEV sales increased by 65% compared to 2021, and Tesla continues to dominate the EV market. In 2022, Mexico sales were only 0.5% of 1,090,000 total vehicle sales were fully electric, a percentage that falls well below other markets, such as China, Europe, and the United States. In Canada, during Q4 2022, battery electric vehicles (BEVs) alone had 27,754 new registrations, and plug-in hybrid electric vehicles (PHEVs) had 5,645 new registrations.

- To expand further, the US government issued a trillion-dollar infrastructure bill in 2021 that allocates USD 7.5 billion toward building 500,000 more public EV chargers by 2030 and also made investments in EV manufacturing by providing tax benefits of USD 7,500 for purchasing an EV assembled in the US. Also, Tesla, one of the significant players in EVs, committed to delivering around 3,500 of its US Supercharger stations and 4,000 Level 2 charging docks available to all brands of electric vehicles by the end of 2024.

- GM Canada invested more than USD 2 billion in Canada to transform manufacturing facilities in Ingersoll and Oshawa and expects electric vehicle production by the end of 2022. By 2030, Georgia, Kentucky, and Michigan are expected to dominate electric vehicle battery manufacturing in the United States. This EV battery manufacturing capacity will facilitate the production of 10 to 13 million batteries for all-electric vehicles per year, positioning the United States as a global EV competitor. Thus, the above instances lead to the development and production of new power stations because of the growing demand for EVs, which boosts the demand for automotive LEDs in the region.

North America Automotive LED Lighting Industry Overview

The North America Automotive LED Lighting Market is moderately consolidated, with the top five companies occupying 52.69%. The major players in this market are GRUPO ANTOLIN IRAUSA, S.A., KOITO MANUFACTURING CO., LTD., Marelli Holdings Co., Ltd., OSRAM GmbH. and Stanley Electric Co., Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 United States

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

- 5.3 Country

- 5.3.1 United States

- 5.3.2 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 GRUPO ANTOLIN IRAUSA, S.A.

- 6.4.2 HELLA GmbH & Co. KGaA (FORVIA)

- 6.4.3 Hyundai Mobis

- 6.4.4 KOITO MANUFACTURING CO., LTD.

- 6.4.5 Marelli Holdings Co., Ltd.

- 6.4.6 Nichia Corporation

- 6.4.7 OSRAM GmbH.

- 6.4.8 Stanley Electric Co., Ltd.

- 6.4.9 Valeo

- 6.4.10 ZKW Group

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms