|

시장보고서

상품코드

1906909

이탈리아의 화물 및 물류 : 시장 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Italy Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

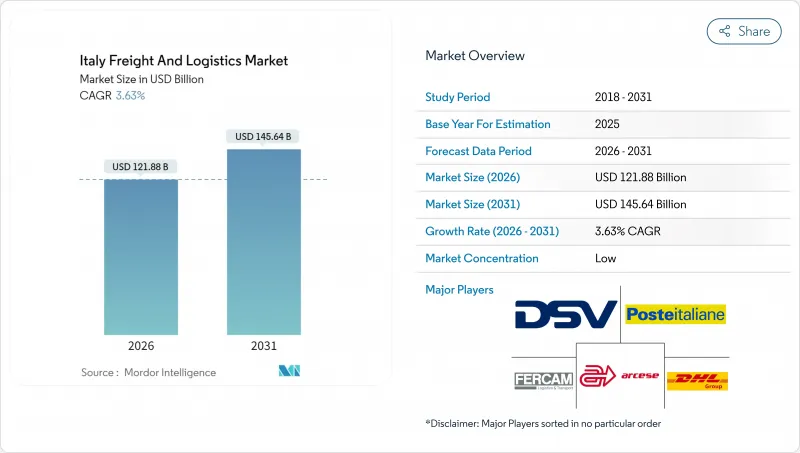

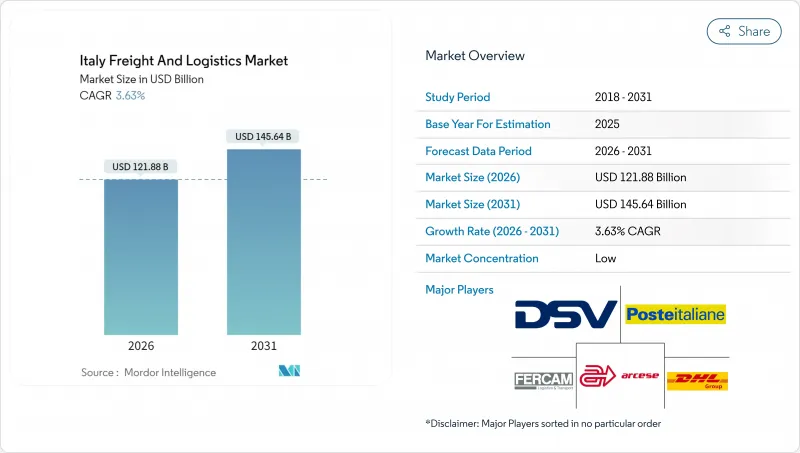

2026년 이탈리아의 화물 및 물류 시장 규모는 1,218억 8,000만 달러로 평가되었고, 2025년 1,176억 1,000만 달러에서 성장을 계속하고 있습니다.

2031년까지의 예측으로는 1,456억 4,000만 달러에 이를 것으로 예측되며, 2026-2031년에 걸쳐 CAGR 3.63%로 성장이 전망됩니다.

국가회복탄력성계획(NRRP) 연계 투자는 항만 및 철도 역량을 확장하는 한편, 전자상거래 수요 증가는 기존 장거리 네트워크에 부담을 주는 택배 물량을 가속화하고 있습니다. 이탈리아의 화물 및 물류 시장은 유럽과 지중해를 잇는 관문 역할로 혜택을 보지만, 노동력 부족과 노후화된 차량으로 인해 비용 부담이 증가하고 있습니다. 제약 및 프리미엄 식품 수출로 인한 콜드체인 수요 증가가 온도 제어 창고 시설을 촉진하고 있으며, 인더스트리 4.0 기반 자동화 인센티브가 북부 허브의 현대화를 지원하고 있습니다. DACHSER가 Fercam Italia 지분 80%를 인수하는 등 통합 움직임은 복잡한 복합 운송 흐름을 처리할 수 있는 대형 통합 공급업체로의 전환을 보여줍니다.

이탈리아의 화물 및 물류 시장 동향 및 분석

전자상거래 소포급증과 라스트마일 투자

CEP 내 국내 소포는 2024년에 66.54%의 점유율을 차지했으며, 이는 588억 유로(649억 달러)에 달하고 전년 대비 6% 성장한 온라인 소매의 급증을 반영합니다. 이탈리아의 화물 및 물류 시장은 밀집형 보관함 그리드를 추가하여 대응하고 있으며, DHL-Poste Italiane 합작 투자는 10,000개의 자동 픽업 지점을 목표로 하고 소포당 도시 배송 비용을 30% 절감합니다. 아마존 물류는 당일 배송 서비스를 15개 도시로 확대하며 기존 운송사들이 소형 물류센터와 전기차량 도입을 촉진했습니다. 운송사들은 전자상거래 물류의 주류를 이루는 100kg 미만 소형 화물 처리를 위해 허브 앤 스포크(hub-and-spoke) 구조를 재설계 중입니다. 무공해 차량에 대한 도시 정책 인센티브는 운영사들의 차량 교체 전략과 부합합니다. 쇼핑 성수기에는 여전히 처리량 한계가 발생해 초과 물량을 흡수하기 위해 크라우드 배송 플랫폼과의 협력이 확대되고 있습니다.

식품, 의약품 수출에 의한 콜드체인 수요

2024년 의약품 수출 가치의 80% 이상을 의약품이 차지하며 온도 관리 유통 수요를 견인했습니다. UPS는 Frigo-Trans와 BPL을 인수해 유럽 GDP 등급 콜드체인 커버리지를 강화하고 밀라노 제약 클러스터를 신흥 시장 물류 허브로 포지셔닝했습니다. 2024년 총 물류 용량 중 온도 관리 창고는 7.81%에 불과했으나, 백신 물류 및 생물학적 제제 생산 확대로 수요가 증가함에 따라 2025-2030년 연평균 3.53% 성장률이 예상됩니다. 밀라노, 로마, 볼로냐 공항 화물 구역은 바이오테크 물류 흐름을 포착하기 위해 냉장 공간을 추가하고 있습니다. 지역별 특화 운영을 통해 운영사들은 능동형 포장재를 활용한 검증된 종단간 운송 경로로 가치를 창출할 수 있습니다. 에너지 효율형 냉동 시스템은 지속가능한 물류 시설을 위해 배정된 NRRP 보조금의 혜택을 받습니다.

운전자 부족과 트럭 차량의 고령화

이탈리아 전문 운전자의 2.2%만이 25세 미만으로, 베테랑 운전사들의 은퇴로 인해 후계자 부족 위험이 발생하고 있습니다. 평균 19.1년의 대형 차량 연령은 EU 평균을 초과하며 차량 신뢰도를 저하시키고 유지보수 비용을 증가시킵니다. 2024년 로마에서 발생한 시위는 서비스 품질 저하를 부각시켰으며 외국인 운전자의 면허 신속 인정을 촉구했습니다. 보조금 프로그램은 운전자당 최대 24,000유로(26,487달러)의 교육비를 지원하나, 복잡한 신청 절차로 인해 활용도가 저조합니다. 리스 업체들은 차량 갱신을 촉진하기 위해 유연한 주행 거리당 요금제를 홍보하고 있으나, 이탈리아의 화물 및 물류 시장을 주도하는 소규모 차량 보유 업체들 사이에서는 자본 제약이 지속되고 있습니다.

부문 분석

제조업은 2025년 매출의 31.12%를 차지했으며, 이는 롬바르디아, 피에몬테, 에밀리아로마냐 지역의 자동차, 기계, 생명과학 생산 거점에 기반을 두고 있습니다. 부품 흐름은 순차적 납품(JIS)을 위한 동기화된 배송을 요구하여 운송업체와 1차 공급업체 간의 협력을 촉진합니다. 도매 및 소매 무역은 옴니채널 브랜드의 전국적 익일 배송 수요로 2026-2031년 연평균 3.86% 성장률로 가장 빠르게 성장합니다. 건설 물류는 NRRP 사업으로 인해 철도 및 고속도로 현장에 골재, 철강, 프리패브 모듈을 운송하며 성장합니다.

에너지 전환 정책으로 석유·가스 운송 투자가 감소하면서 운송사들은 재생에너지 프로젝트 화물로 전환하고 있습니다. 농업·어업·임업 분야는 프리미엄 올리브 오일과 와인 수출 기반을 강화하며 콜드체인 및 냉동 컨테이너 수요를 증가시키고 있습니다. 재생에너지 기술 조립 및 디지털 서비스 등 신흥 분야가 이탈리아의 화물·물류 시장의 고객 기반을 다각화하여 경기 변동 위험을 완화하고 있습니다.

화물 운송은 2025년 매출의 62.88%를 차지하며, 이탈리아의 화물 및 물류 시장에서 도로, 철도, 해상, 항공 운송의 핵심적 위치를 부각시켰습니다. 이 부문은 북부 산업 클러스터에서 전국 소비자 시장으로의 물류 흐름을 포착합니다. 온라인 쇼핑이 배송 빈도 기준을 재설정하고 네트워크 밀집화를 가속화함에 따라 CEP 서비스는 2026-2031년 사이 연평균 4.17% 성장률을 기록할 전망입니다. 창고 및 보관 서비스는 산업 4.0 인센티브를 활용해 북부 시설에 다단계 자동화를 도입함으로써 처리량을 높이고 확장성을 보장합니다. 화물 운송은 아시아-유럽 노선의 이탈리아의 입지를 활용해 복합 운송을 조율하며, 기타 서비스에는 프로젝트 화물 조율 및 위험물 취급이 포함됩니다.

통합 서비스 제공으로 운송사가 운송 계약에 통관 대행 및 재고 관리를 포함시키면서 기능 경계가 모호해지고 있습니다. 포스테 이탈리아네의 전환에서 다각화 추세가 뚜렷하다. 2025년 물류 운영 수익이 우편 서비스를 추월하며 서비스 확장의 타당성을 입증했습니다. 산업 고객이 문간 가시성과 규정 준수를 요구함에 따라 교차 판매가 고객 충성도를 높입니다. 이탈리아의 화물 및 물류 시장은 운송, 창고, 부가가치 서비스를 통합 디지털 플랫폼 아래 융합하는 사업자에게 유리하다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 인구동태

- 경제 활동별 GDP 분포

- 경제활동별 GDP 성장률

- 인플레이션

- 경제적 성능과 프로파일

- 전자상거래 업계 동향

- 제조업의 동향

- 운수, 창고업 부문의 GDP

- 수출 동향

- 수입 동향

- 연료 가격

- 트럭 운송 운영 비용

- 트럭 운송 차량 규모(유형별)

- 주요 트럭 공급업체

- 물류 성능

- 운송 모드별 점유율

- 해상 운송선대의 적재능력

- 정기선 운송의 접속성

- 기항지와 성능

- 화물운임 동향

- 화물 톤수 동향

- 인프라

- 규제 프레임워크(도로, 철도)

- 규제 프레임워크(해상, 항공)

- 밸류체인과 유통채널 분석

- 시장 성장 촉진요인

- 전자상거래 소포 급증과 라스트마일 투자

- 식품, 의약품 수출에 의한 콜드체인 수요

- NRRP 및 TEN-T 회랑 하의 인프라 업그레이드

- 인더스트리 4.0 세제 우대조치가 스마트 물류 기술을 촉진

- 도시 PUDO 혼합을 변화시키는 보관함 네트워크

- 철도 업그레이드 차질로 인한 도로 운송량 증가

- 시장 성장 억제요인

- 운전자 부족과 트럭 차량의 노후화

- 남북 간의 높은 운영 비용 격차

- 주요 항만 회랑의 2025년의 철도 공사에 의한 운송 능력 부족

- 전지, 위험물 규제에 의한 EV 물류 규정 준수 비용 증가

- 시장의 기술 혁신

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 최종 사용자 산업

- 농업, 어업, 임업

- 건설업

- 제조업

- 석유 및 가스, 광업, 채석

- 도매, 소매업

- 기타

- 물류 기능

- 택배, 특송, 소포(CEP)

- 목적지별

- 국내

- 국제

- 목적지별

- 화물 운송

- 운송 수단별

- 항공

- 해상, 내륙 수로

- 기타

- 운송 수단별

- 화물 운송

- 운송 수단별

- 항공

- 파이프라인

- 철도

- 도로

- 해상, 내륙 수로

- 운송 수단별

- 창고 보관

- 온도 관리별

- 비온도 관리

- 온도 관리

- 온도 관리별

- 기타 서비스

- 택배, 특송, 소포(CEP)

제6장 경쟁 구도

- 시장 집중도

- 주요 전략적 움직임

- 시장 점유율 분석

- 기업 프로파일

- Amazon

- Arcese Trasporti SpA

- BRT SpA

- CMA CGM Group(Including CEVA Logistics)

- DHL Group

- DSV A/S(Including DB Schenker)

- FedEx

- Fercam SpA

- International Distributions Services PLC(Including GLS)

- Grimaldi Group

- GRUBER Logistics SpA

- Italsempione

- Italtrans

- Kuehne Nagel

- Mercitalia Rail

- MSC Mediterranean Shipping Company SAA

- Poste Italiane

- Savino Del Bene SpA

- Transmec Group

- United Parcel Service of America, Inc.(UPS)

제7장 시장 기회와 장래의 전망

HBR 26.02.04Italy freight and logistics market size in 2026 is estimated at USD 121.88 billion, growing from 2025 value of USD 117.61 billion with 2031 projections showing USD 145.64 billion, growing at 3.63% CAGR over 2026-2031.

Investment tied to the National Recovery and Resilience Plan (NRRP) is expanding port and rail capacity, while e-commerce demand accelerates parcel volumes that challenge traditional long-haul networks. The Italy freight and logistics market benefits from the country's gateway role between Europe and the Mediterranean, yet labor shortages and an aging vehicle fleet raise cost pressures. Rising cold-chain needs from pharmaceutical and premium food exports stimulate temperature-controlled warehousing, and automation incentives under Industry 4.0 support modernization in northern hubs. Consolidation activities, such as DACHSER acquiring 80% of Fercam Italia, highlight a shift toward larger, integrated providers capable of handling complex multimodal flows.

Italy Freight And Logistics Market Trends and Insights

E-Commerce Parcel Surge and Last-Mile Investments

Domestic parcels within CEP captured a 66.54% share in 2024, reflecting surging online retail that hit EUR 58.8 billion (USD 64.9 billion) and grew 6% year over year. The Italy freight and logistics market responds by adding dense locker grids; the DHL-Poste Italiane venture targets 10,000 automated pickup points and cuts per-parcel urban delivery cost by 30%. Amazon Logistics extended same-day coverage to 15 more cities, compelling traditional carriers to invest in micro-fulfillment and electric fleets. Carriers reengineer hub-and-spoke layouts to support sub-100-kilogram shipments that dominate e-commerce flows. Urban policy incentives for zero-emission vehicles align with operator fleet renewal strategies. Capacity challenges persist on peak shopping days, driving collaboration with crowd-shipping platforms to absorb overflow volumes.

Cold-Chain Demand from Food and Pharma Exports

Medicinal drugs sustained above 80% of the pharmaceutical export value in 2024, anchoring demand for temperature-controlled distribution. UPS acquired Frigo-Trans and BPL, bolstering European GDP-grade cold-chain coverage and positioning Milan's pharma cluster as a hub for emerging-market shipments. Temperature-controlled warehousing claims only 7.81% of total capacity in 2024, yet it is expected to expand at a 3.53% CAGR (2025-2030) as vaccine logistics and biologics production widen demand. Airport cargo zones in Milan, Rome, and Bologna add cool-room space to capture biotech flows. Regional specialization enables operators to capture value via end-to-end validated lanes with active packaging. Energy-efficient refrigeration systems benefit from NRRP grants earmarked for sustainable logistics facilities.

Driver Shortages and Aging Truck Fleet

Only 2.2% of professional drivers in Italy are under 25, creating succession risk as veteran operators retire. The average heavy-duty vehicle age of 19.1 years exceeds the EU average and lowers fleet reliability, inflating maintenance costs. Protests in Rome during 2024 spotlighted declining service quality and urged fast-track license recognition for foreign drivers. Grant programs cover up to EUR 24,000 (USD 26,487) per driver for training, yet uptake lags amid cumbersome application rules. Leasing firms promote flexible pay-per-kilometer schemes to accelerate fleet renewal, but capital constraints persist among micro-fleets dominating the Italy freight and logistics market.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Upgrades Under NRRP and TEN-T Corridors

- Industry 4.0 Tax Credits Boosting Smart-Logistics Tech

- High North-South Operating-Cost Differential

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing accounted for 31.12% of 2025 revenue, anchored in automotive, machinery, and life-science production hubs across Lombardy, Piedmont, and Emilia-Romagna. Component flows require synchronized just-in-sequence deliveries, fostering collaboration between hauliers and tier-one suppliers. Wholesale and retail trade grows fastest at 3.86% CAGR (2026-2031) as omnichannel brands demand nationwide next-day fulfillment. Construction logistics gains from NRRP works, shipping aggregates, steel, and prefabricated modules to rail and highway sites.

Energy transition policies taper investments in oil and gas haulage, nudging carriers toward renewables project cargo. Agriculture, fishing, and forestry strengthen export footprints in premium olive oil and wine, raising cold-chain and reefer container needs. Emerging sectors such as renewable technology assembly and digital services diversify the Italy freight and logistics market's customer base, cushioning cyclical risk.

Freight transport generated 62.88% of 2025 revenue, underscoring the centrality of road, rail, sea, and air moves in the Italy freight and logistics market. The segment captures flows from industrial clusters in the North to consumer markets nationwide. CEP services record a 4.17% CAGR between 2026-2031 as online shopping resets delivery frequency benchmarks and accelerates network densification. Warehousing and storage rides Industry 4.0 incentives to add multi-level automation in northern facilities, lifting throughput and assuring scalability. Freight forwarding leverages Italy's positioning on Asia-Europe lanes to orchestrate multimodal movements, while other services encompass project cargo orchestration and hazardous goods handling.

Integrated offerings now blur function lines as carriers embed customs brokerage and inventory control within transport contracts. Diversification is visible in Poste Italiane's pivot: revenue from logistics operations outpaced mail services in 2025, validating service expansion. Cross-selling boosts stickiness with industrial clients demanding door-to-door visibility and compliance. The Italy freight and logistics market rewards operators that fuse transport, warehousing, and value-added services under unified digital platforms.

The Italy Freight and Logistics Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others) and by Logistics Function (Courier, Express, and Parcel (CEP), Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amazon

- Arcese Trasporti SpA

- BRT SpA

- CMA CGM Group (Including CEVA Logistics)

- DHL Group

- DSV A/S (Including DB Schenker)

- FedEx

- Fercam SpA

- International Distributions Services PLC (Including GLS)

- Grimaldi Group

- GRUBER Logistics SpA

- Italsempione

- Italtrans

- Kuehne+Nagel

- Mercitalia Rail

- MSC Mediterranean Shipping Company S.A.A

- Poste Italiane

- Savino Del Bene SpA

- Transmec Group

- United Parcel Service of America, Inc. (UPS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Logistics Performance

- 4.15 Modal Share

- 4.16 Maritime Fleet Load Carrying Capacity

- 4.17 Liner Shipping Connectivity

- 4.18 Port Calls and Performance

- 4.19 Freight Pricing Trends

- 4.20 Freight Tonnage Trends

- 4.21 Infrastructure

- 4.22 Regulatory Framework (Road and Rail)

- 4.23 Regulatory Framework (Sea and Air)

- 4.24 Value Chain and Distribution Channel Analysis

- 4.25 Market Drivers

- 4.25.1 E-Commerce Parcel Surge and Last-Mile Investments

- 4.25.2 Cold-Chain Demand from Food and Pharma Exports

- 4.25.3 Infrastructure Upgrades Under NRRP and TEN-T Corridors

- 4.25.4 Industry 4.0 Tax Credits Boosting Smart-Logistics Tech

- 4.25.5 Locker Networks Altering Urban PUDO Mix

- 4.25.6 Rail-Upgrade Disruptions Shifting Volumes to Road

- 4.26 Market Restraints

- 4.26.1 Driver Shortages and Ageing Truck Fleet

- 4.26.2 High North-South Operating-Cost Differential

- 4.26.3 2025 Rail-Works Capacity Crunch on Key Port Corridors

- 4.26.4 Battery-Hazmat Rules Raising EV-Logistics Compliance Cost

- 4.27 Technology Innovations in the Market

- 4.28 Porter's Five Forces Analysis

- 4.28.1 Threat of New Entrants

- 4.28.2 Bargaining Power of Buyers

- 4.28.3 Bargaining Power of Suppliers

- 4.28.4 Threat of Substitutes

- 4.28.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.1.1 By Destination Type

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.2.1 By Mode of Transport

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.3.1 By Mode of Transport

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.4.1 By Temperature Control

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon

- 6.4.2 Arcese Trasporti SpA

- 6.4.3 BRT SpA

- 6.4.4 CMA CGM Group (Including CEVA Logistics)

- 6.4.5 DHL Group

- 6.4.6 DSV A/S (Including DB Schenker)

- 6.4.7 FedEx

- 6.4.8 Fercam SpA

- 6.4.9 International Distributions Services PLC (Including GLS)

- 6.4.10 Grimaldi Group

- 6.4.11 GRUBER Logistics SpA

- 6.4.12 Italsempione

- 6.4.13 Italtrans

- 6.4.14 Kuehne+Nagel

- 6.4.15 Mercitalia Rail

- 6.4.16 MSC Mediterranean Shipping Company S.A.A

- 6.4.17 Poste Italiane

- 6.4.18 Savino Del Bene SpA

- 6.4.19 Transmec Group

- 6.4.20 United Parcel Service of America, Inc. (UPS)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment