|

시장보고서

상품코드

2063760

북미의 접이식 카톤 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

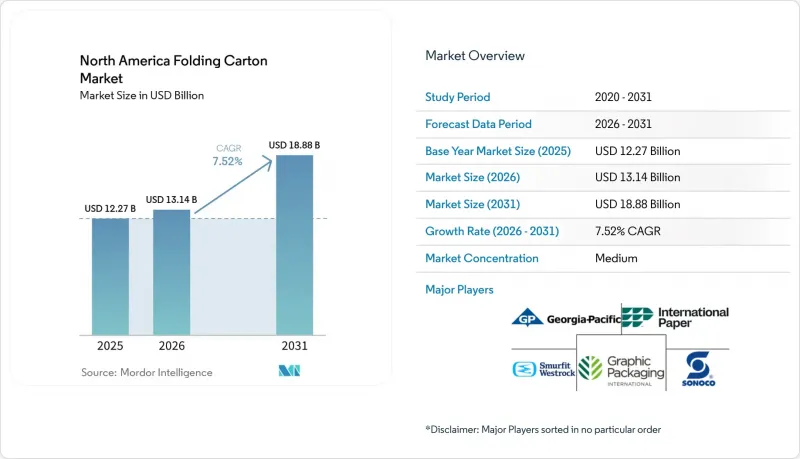

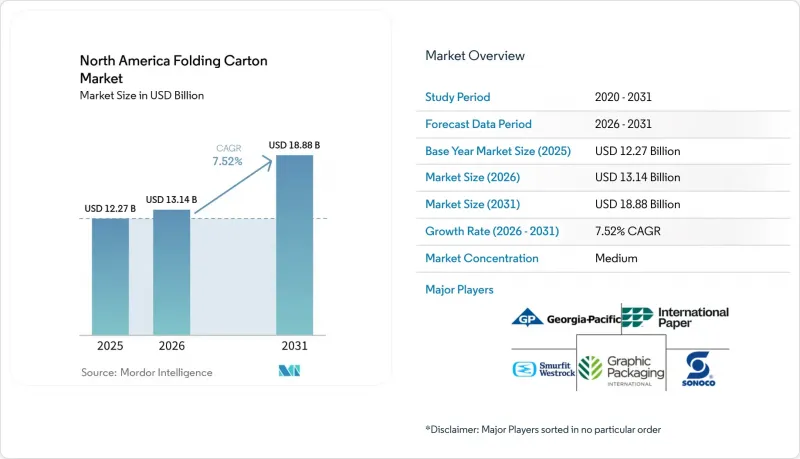

Mordor Intelligence에 의하면, 북미의 접이식 카톤 시장 규모는 2025년 122억 7,000만 달러로 평가되었습니다. 2026년 131억 4,000만 달러에서 2031년까지 188억 8,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 7.52%를 나타낼 것으로 예측됩니다.

본 보고서는 원료 유형(고형 표백 황산 펄프, 접이식 카톤, 코팅 미표백 크라프트지 등), 인쇄 기술(오프셋 인쇄, 플렉소 인쇄, 디지털 인쇄 등), 최종 사용자 산업(식품 및 음료, 헬스케어 및 의약품, 퍼스널케어 및 화장품, 전기 및 전자기기 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미의 접이식 카톤 상자 시장 동향 및 인사이트

전자상거래 출하량이 급증함에 따라, 매장 진열이 가능한 포장이 요구되고 있습니다.

현재 전자상거래 소매업체들은 공급업체에 입고 도크에서 매장 진열대로 직접 이동할 수 있는 접이식 상자를 납품해 줄 것을 요구하고 있으며, 이를 통해 2차 취급 작업을 없애고 있습니다. 아마존, 월마트, 타겟은 2025년부터 스캔이 가능한 사전 인쇄된 골판지 상자 사용을 의무화했습니다. 이로 인해 각 변환기 제조업체들은 RFID 태그 부착에 대응할 수 있는 고화질 디지털 인쇄 및 오프셋 인쇄에 대한 투자를 서둘러야 하는 상황에 놓여 있습니다. 당일 납품은 결정적인 차별화 요소로 자리 잡고 있으며, 풀필먼트 허브 근처에 자동화된 다이 커팅 기계를 보유한 컨버터들이 북미의 접이식 카톤 상자 시장에서 점유율을 확대되고 있습니다. 몬테레이와 과달라하라에 새로운 제조 클러스터가 형성되면서, 현지 생산이 가능한 진열용 포장에 대한 수요가 증가하는 가운데, 멕시코에서도 그 영향이 뚜렷해지고 있습니다.

플라스틱을 대체할 수 있는 지속 가능한 섬유 소재에 대한 선호도 증가

캘리포니아주와 캐나다의 확대 생산자 책임법에 따라 각 브랜드 기업들은 플라스틱에서 재활용 가능한 판지로 전환할 수밖에 없게 되었으며, 이에 따라 산림관리협의회(FSC) 및 지속가능한 임업 이니셔티브(SFI) 인증을 받은 고품질 섬유 등급 원료에 대한 수요가 증가하고 있습니다. 스트라 엔소(Stora Enso)사의 ‘Performa Lumi’ 판지는 뛰어난 인쇄 재현성과 높은 재활용 소재 함유율을 모두 갖추고 있어, 2025년까지 화장품 업계에서 널리 채택되었습니다. 통합형 제조업체는 제품 포트폴리오 전반에 걸친 ‘플라스틱에서 종이로’ 전환 프로그램을 통해 이에 대응하며, 북미의 접이식 카톤 상자 시장 규모를 더욱 확대되고 있습니다.

재생 섬유 공급 가격의 변동

중국의 제지 공장 폐쇄와 아시아 지역의 새로운 수출 규제로 인해 폐지 공급량이 감소함에 따라, 북미의 재활용 판지 가격은 4분기 연속 두 자릿수 등락을 보였습니다. 가정용 쓰레기 수거를 관리하고 펄프 공장을 보유한 통합 제조업체는 장기 섬유 계약을 체결함으로써 이익률을 유지하고, 북미의 접이식 카톤 시장 점유율을 선두 기업에 집중시키고 있습니다. 이러한 가격 변동은 브랜드 소유주들에게 조달 전략의 다각화를 촉진하고, 안정적인 섬유 공급원과 가격 투명성을 갖춘 공급업체를 우선적으로 선택하도록 요구하고 있습니다.

부문별 분석

화이트 라인 칩보드는 전자상거래 소매업체들이 2차 가공 및 매장 진열 용도로 사용함에 있어 낮은 광택도를 수용하게 됨에 따라, 시장 전체의 7.52% 성장률을 상회하는 7.94%의 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 2025년, 북미의 접이식 카톤 상자 시장에서 고형 표백 황산 펄프(SBS)는 34.21%라는 최대 점유율을 유지했으며, 이러한 입지는 의약품 및 화장품 분야의 연속 생산 수요에 힘입어 더욱 공고해지고 있습니다. 스마핏 웨스트록(SmartFit Westlock)사가 퀘벡주의 SBS 생산 라인을 폐쇄함에 따라 공급이 부족해지고 가격 규율이 강화되었기 때문에 인쇄의 정밀도가 그리 중요하지 않은 경우 컨버터들은 칩보드로 전환하고 있습니다. 접이식 박스 보드는 식품 및 음료 분야에서 주문이 호조를 보이고 있지만, 스낵 브랜드들은 휴대 편의성을 추구하며 경량 파우치로 계속 전환하고 있습니다. 표백하지 않은 코트 크라프트지는 자연스러운 갈색을 중시하는 틈새 시장인 유기농 식품 라벨에 사용됩니다. 전반적으로, 소재 선정은 기존의 기판에 대한 애착보다는 총 납품 비용이나 재활용 가능성 인증을 중시하는 방향으로 전환되고 있습니다. 브랜드 소유자의 우선순위가 변화하는 가운데, 등급을 신속하게 전환할 수 있는 가공업체는 북미의 접이식 카톤 상자 시장에서 새로운 비즈니스 기회를 포착할 수 있습니다.

화이트라인 칩보드에 대한 수요는 2025년에 소매 매출의 15%를 넘어선 전자상거래 보급률을 자랑하는 미국에서 가장 두드러집니다. 소매업체들이 비용 관리에 주력함에 따라, 브랜드 소유주들은 진열 효과를 저해하지 않으면서 더 저렴한 소재로 전환하고 있습니다. 멕시코에서는 니어쇼어링의 확산에 따라 가전제품용 골판지 상자에 사용되는 칩보드에 대한 관심이 높아지고 있습니다. 이는 저비용 원자재가 물류 비용 상승을 상쇄하기 때문입니다. 캐나다에서는 규제 대상 의약품을 위한 프리미엄 SBS에 대한 수요가 여전히 견조하지만, 운임 급등과 달러 강세를 배경으로 칩보드로의 대체가 검토되기 시작하고 있습니다. 공급망의 지역화가 진행되는 가운데, 단일 복합 시설에서 여러 등급의 제품을 공급할 수 있는 제지 공장은 생산량 조정을 보다 신속하게 수행하고, 수익성을 유지하면서 북미의 접이식 카톤 상자 시장 전반에 대한 참여도를 높일 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the north america folding cartons market size is projected to expand from USD 12.27 billion in 2025 and USD 13.14 billion in 2026 to USD 18.88 billion by 2031, registering a CAGR of 7.52% between 2026 to 2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, Digital, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America Folding Carton Market Trends and Insights

Surge in E-Commerce Shipments Requiring Shelf-Ready Packaging

E-commerce retailers now ask suppliers to deliver folding cartons that move straight from inbound docks to store shelves, eliminating secondary handling. Amazon, Walmart, and Target introduced mandatory scannable, pre-printed carton specifications in 2025, prompting converters to invest in high-graphic digital and litho printing that supports RFID tagging. Same-day turnaround has become a decisive differentiator, and converters with automated die-cutters near fulfillment hubs are gaining a growing share of the North America folding cartons market. Mexico is feeling the pull as new manufacturing clusters in Monterrey and Guadalajara demand localized, shelf-ready packaging.

Growing Preference for Sustainable Fiber-Based Substitutes to Plastics

Extended producer responsibility laws in California and Canada compel brands to switch from plastic to recyclable paperboard, lifting demand for premium fiber grades certified by the Forest Stewardship Council and the Sustainable Forestry Initiative. Stora Enso's Performa Lumi paperboard achieved broad adoption in cosmetics by 2025 because it pairs high graphic fidelity with high recycled content. Integrated producers have responded with portfolio-wide "plastic-to-paper" programs, further enlarging the North America folding cartons market footprint.

Volatility in Recycled Fiber Supply Prices

Mill closures in China and new Asian export restrictions cut recovered-paper availability, pushing North American recycled-paperboard prices up or down by double digits in back-to-back quarters. Integrated producers that control curbside collection and possess pulp mills lock in long-term fiber contracts, shielding margins and concentrating North America's folding cartons market share among the top tier. This volatility is also prompting brand owners to diversify sourcing strategies and prioritize suppliers with stable fiber access and pricing visibility.

Other drivers and restraints analyzed in the detailed report include:

- Advances in Water-Based Barrier Coatings Enabling Frozen Food Cartons

- Automation of High-Speed Die-Cutting and Gluing Lines

- Capital-Intensive Compliance With PFAS Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

White Line Chipboard is projected to grow at a 7.94% CAGR, outpacing the overall 7.52% expansion, as e-commerce retailers accept its lower brightness for secondary and shelf-ready applications. Solid Bleached Sulfate retained the largest 34.21% share of the North America folding cartons market in 2025, a position secured by pharmaceutical and cosmetic serialization demands. Supply tightened when Smurfit WestRock shuttered its Quebec SBS machine, lifting price discipline and nudging converters toward chipboard when print fidelity is less critical. Folding Boxboard maintains steady food and beverage orders, yet snack brands continue to migrate to lightweight pouches for on-the-go convenience. Coated Unbleached Kraft serves niche organic food labels that value the natural brown appearance. Overall, material decisions now pivot more on total delivered cost and recyclability certification than on historical substrate loyalties. Converters that can switch grades quickly capture incremental opportunities in the North America folding carton market as brand-owner priorities evolve.

Demand for White Line Chipboard is most visible in the United States, where e-commerce penetration breached 15% of retail sales in 2025. Retailers' focus on cost control encourages brand owners to trade down to a lower-cost substrate without sacrificing shelf impact. In Mexico, nearshoring has sparked interest in chipboard for consumer electronics cartons, as a low-cost substrate offsets higher logistics overhead. Canada continues to support premium SBS for regulated pharmaceuticals, but rising freight costs and a strong U.S. dollar are opening conversations about chipboard substitution. As supply chains regionalize, mills able to furnish multiple grades from a single complex can rebalance output faster, protecting margins and deepening engagement across the North America folding cartons market.

List of Companies Covered in this Report:

- Graphic Packaging Holding Company

- Smurfit Westrock plc

- International Paper Company

- Georgia-Pacific LLC

- Sonoco Products Company

- Huhtamaki Oyj

- Packaging Corporation of America

- Cascades Inc.

- Pratt Industries Inc.

- Rengo Co., Ltd.

- Mayr-Melnhof Karton AG

- AR Packaging Group AB

- Multi Packaging Solutions International LLC

- Caraustar Industries, Inc. (Greif, Inc.)

- Americraft Carton, Inc.

- Edelmann Group

- Great Little Box Company Ltd.

- Unicorr Packaging Group

- Bell Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in E-commerce Shipments Requiring Shelf-Ready Packaging

- 4.2.2 Growing Preference for Sustainable Fiber-Based Substitutes to Plastics

- 4.2.3 Lightweighting of Paperboard to Cut Logistics Costs

- 4.2.4 Advances in Water-Based Barrier Coatings Enabling Frozen Food Cartons

- 4.2.5 Automation of High-Speed Die-Cutting and Gluing Lines

- 4.2.6 Retailer Mandates for Scannable, High-Graphic Packaging

- 4.3 Market Restraints

- 4.3.1 Volatility in Recycled Fiber Supply Prices

- 4.3.2 Competition From Flexible Pouch Formats in Snacks

- 4.3.3 Capital-Intensive Compliance With PFAS Regulations

- 4.3.4 Limited Commercial Scaling of Digital Print for Long Runs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Mexico

- 5.4.3 Canada

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Graphic Packaging Holding Company

- 6.4.2 Smurfit Westrock plc

- 6.4.3 International Paper Company

- 6.4.4 Georgia-Pacific LLC

- 6.4.5 Sonoco Products Company

- 6.4.6 Huhtamaki Oyj

- 6.4.7 Packaging Corporation of America

- 6.4.8 Cascades Inc.

- 6.4.9 Pratt Industries Inc.

- 6.4.10 Rengo Co., Ltd.

- 6.4.11 Mayr-Melnhof Karton AG

- 6.4.12 AR Packaging Group AB

- 6.4.13 Multi Packaging Solutions International LLC

- 6.4.14 Caraustar Industries, Inc. (Greif, Inc.)

- 6.4.15 Americraft Carton, Inc.

- 6.4.16 Edelmann Group

- 6.4.17 Great Little Box Company Ltd.

- 6.4.18 Unicorr Packaging Group

- 6.4.19 Bell Incorporated

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment