|

시장보고서

상품코드

2063777

베트남의 접이식 카톤 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Vietnam Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

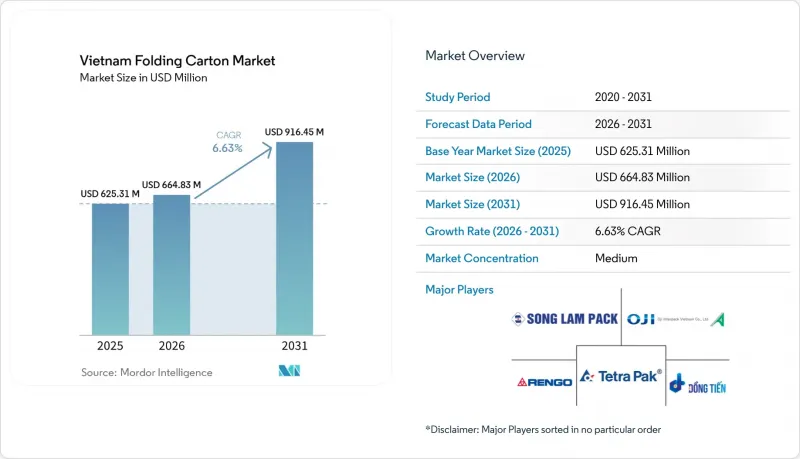

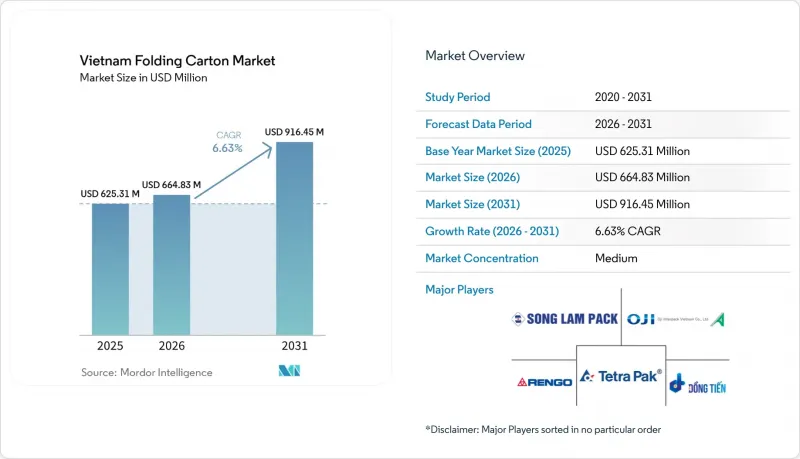

Mordor Intelligence에 의하면, 베트남의 접이식 카톤 시장 규모는 2025년에 6억 2,531만 달러로 평가되었습니다. 2026년 6억 6,483만 달러에서 2031년까지 9억 1,645만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 6.63%를 나타낼 전망입니다.

본 보고서는 원료 유형(고형 표백 황산 펄프, 접이식 카톤, 코팅 미표백 크라프트지, 화이트라인 칩보드 등), 인쇄 기술(오프셋 인쇄, 플렉소 인쇄, 디지털 인쇄 등), 그리고 최종 사용자 산업(식품 및 음료, 전자상거래 및 소매용 포장, 담배 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

베트남의 접이식 카톤 시장 동향 및 분석

전자상거래 분야 수요 증가

베트남의 온라인 소매 채널에서는 2023년에 33만 2,000톤의 포장 자재가 소비되었으며, 그중 접이식 카톤이 부피 기준으로 약 40%를 차지했습니다. 이 채널은 현재 소매 상품 매출의 12%를 차지하고 있으며, 불과 3년 만에 4포인트 상승했습니다. 판매업체들은 풀필먼트 업무 부담을 최대 20%까지 줄일 수 있는 ‘진열 대응’ 형식을 점점 더 선호하고 있으며, 이러한 추세에 따라 위조 방지 기술과 눈길을 끄는 그래픽을 결합할 수 있는 컨버터 업체에 안정적인 주문이 집중되고 있습니다. Lazada나 Shopee와 같은 크로스보더 전자상거래 플랫폼은 판매자 참여 요건에 FSC 인증을 포함시키고 있으며, 이에 따라 각 플랫폼의 네트워크를 통해 출고되는 모든 골판지 상자의 기준 사양이 즉시 재검토되고 있습니다. 따라서 베트남의 접이식 카톤 시장은 판매량의 절대적 증가와 더 높은 이익률을 가져다주는 고급 소재로의 전환이라는 두 가지 이점을 누리고 있습니다.

지속 가능한 포장을 위한 정부의 이니셔티브

2026년 제110호 정령은 생산자에게 사용 후 제품의 회수 및 재활용 비용 부담을 의무화하고, 2028년까지 종이 재활용률 30%라는 목표를 설정하고 있습니다. 한편, 정령 제05/2025호는 도시 지역의 외식 산업에서 일회용 플라스틱 사용을 규제하고 있습니다. 이러한 규제들이 복합적으로 작용하여 패스트푸드점, 전자기기 조립업체, 가정용품 제조업체들이 재생 섬유를 사용한 골판지 솔루션을 채택하도록 이끌고 있습니다. 위반 시 부과되는 벌금은 5,000만 VND(2,100달러)에서 1억 VND(4,200달러)에 달하기 때문에 브랜드 소유주들은 재생 소재를 50% 이상 함유한 접이식 판지나 표백하지 않은 코팅 크라프트지를 사용하도록 권장받고 있습니다. 초기 단계에서 탈잉크 및 폐지 집하 라인에 투자한 가공업체나, 생산자 책임 조직과 제휴한 가공업체는 현재 베트남의 접이식 카톤 시장에서 라이선싱 측면에서 뚜렷한 우위를 점하고 있습니다.

버진 펄프 가격 변동

2026년 1월 시세에서는 유럽산 표백 유칼립투스 크라프트지가 톤당 1,220-1,250달러, 북미산 표백 침엽수 크라프트지는 1,600달러를 기록했으며, 전가 조항에 상한선이 설정된 계약 하에서는 가공업체의 이익률이 최대 300베이시스포인트 축소되었습니다. 원목 펄프의 70%가 수입에 의존하고 있기 때문에 환율 변동이나 지정학적 요인으로 인한 운임 인상으로 인해 톤당 도착 가격이 80-120달러가 추가되고 있습니다. 선물 계약을 이용하는 변환업체는 고작 18%에 불과하며, 대다수는 분기별 가격 조정 영향을 받기 쉬워, 이때 가격이 10-15% 급등할 가능성이 있습니다. 이러한 압박은 백도 안정성 문제로 인해 대체재 사용이 제한되는 SBS(Solid Bleached Sulfate) 등급에서 가장 심각하며, 베트남의 접이식 카톤 시장 전체의 수익을 압박하고 있습니다.

부문별 분석

2025년, 솔리드 블리치드 설페이트는 베트남의 접이식 카톤 시장 점유율의 33.42%를 차지하며, 화장품, 의약품, 고급 과자 등의 프리미엄 용도 분야에서 확고한 입지를 다졌습니다. 브랜드 소유자는 88 GE를 초과하는 백도 수준과 사진 리소그래피가 가능한 인쇄면을 추구하여 이 등급을 선택했으며, 가격에 민감하면서도 그래픽을 많이 사용하는 카테고리에서 이 등급의 입지를 공고히 하고 있습니다. 폴딩 박스 보드는 패스트푸드점이나 전자상거래 물류 센터가 운송비 할증 요금을 억제하기 위해 250-300 gsm 범위의 평량(gsm)을 채택하고 있기 때문에 기판 소재 중 가장 높은 연평균 성장률(CAGR) 8.75%를 나타낼 것으로 예측됩니다. ‘미표백 크라프트지’는 정령 110/2026이 재생재 함유율 준수를 장려하고 있기 때문에 전자기기 및 가정용품 운송업체들 사이에서 입지를 공고히 하고 있습니다. 한편, ‘화이트 라인 칩보드’는 비용 효율을 중시하는 건조식품 충전 업체에 공급되고 있습니다.

테트라팩의 연간 생산량을 300억 팩으로 확대하려는 움직임은 무균 유제품 및 주스 생산 라인에서 배리어 코팅이 적용된 고형 표백 황산 펄프가 핵심적인 역할을 하고 있음을 여실히 보여주고 있습니다. 이는 펄프 가격 급등 속에서도 이익을 지켜내는 틈새 시장입니다. 재생 섬유 함유율 기준치가 상향 조정되는 가운데, 가공업체들은 비용 목표를 초과하지 않으면서 인장 강도를 유지하기 위해 버진 펄프와 재생 펄프를 혼합하고 있습니다. 인라인 평량 스캐너, 근적외선 수분 제어 장치, 고농도 리파이너는 대형 제지 공장이 보다 엄격한 평량 공차를 달성하는 데 도움이 됩니다. 이는 지불 조건을 통계적 공정 관리 지표와 연계하려는 다국적 기업에게 있어 필수적인 전제조건입니다. 이러한 설비 투자를 감당할 자금력이 없는 중소 컨버터는 수익성이 낮은 범용 골판지 상자 시장으로 밀려날 위험이 있습니다. 따라서 베트남의 접이식 카톤 시장에서 규모의 우위는 원자재의 범용성과 자본 집약적인 품질 관리 시스템을 모두 갖춘 사업자에게로 집중되는 경향을 보이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the vietnam folding carton market size was valued at USD 625.31 million in 2025 and is estimated to grow from USD 664.83 million in 2026 to reach USD 916.45 million by 2031, at a CAGR of 6.63% during 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, and More), and End-User Industry (Food and Beverage, E-Commerce and Retail-Ready Packaging, Tobacco, and More). The Market Forecasts are Provided in Terms of Value (USD).

Vietnam Folding Carton Market Trends and Insights

Rising Demand from the E-Commerce Sector

Vietnam's online retail channel consumed 332,000 tons of packaging materials in 2023, of which folding cartons supplied roughly 40% by volume. The channel now accounts for 12% of retail goods sales, having climbed 4% points in just 3 years. Merchants increasingly prefer shelf-ready formats that cut fulfillment labor by up to 20%, a dynamic that is funneling steady orders toward converters able to combine tamper-evident engineering with striking graphics. Cross-border platforms such as Lazada and Shopee embed FSC certification into seller eligibility, instantly redefining baseline specifications for every carton shipped through their networks. The Vietnam folding carton market, therefore, benefits twice: in higher absolute volumes and in the migration to premium substrates that command superior margins.

Government Push for Sustainable Packaging

Decree 110/2026 obliges producers to finance post-consumer collection and recycling, setting a 30% paper recovery target by 2028, while Decree 05/2025 restricts single-use plastics in urban food service. Together, the regulations are channeling quick-service restaurants, electronics assemblers, and household-goods makers toward recycled-fiber carton solutions. Penalties for non-compliance range from VND 50 million (USD 2,100) to VND 100 million (USD 4,200), spurring brand owners to specify Folding Boxboard and Coated Unbleached Kraft with at least 50% recycled content. Converters that invested early in de-inking and waste-paper aggregation lines, or that formed alliances with Producer Responsibility Organizations, now enjoy a distinct licensing edge in the Vietnamese folding carton market.

Volatility in Virgin Fiber Prices

January 2026 quotations moved European Bleached Eucalyptus Kraft to USD 1,220-1,250 per ton and Northern Bleached Softwood Kraft to USD 1,600, trimming converter margins by as much as 300 basis points under contracts that cap pass-through clauses. With 70% of virgin pulp imported, exchange-rate swings and geopolitical freight surcharges add USD 80-120 to every ton landed. Only 18% of converters use forward contracts, leaving most exposed to quarterly resets that can jump 10-15%. The squeeze is most acute for Solid Bleached Sulfate grades, where brightness consistency bars substitution, weighing on earnings across the Vietnam folding carton market.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Food and Beverage Exports

- Rising Disposable Income and Urbanization

- Intensifying Competition from Flexible Packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solid Bleached Sulfate captured 33.42% of the Vietnam folding carton market share in 2025, firmly anchoring premium applications in cosmetics, pharmaceuticals, and high-end confectionery. Brand owners select the grade for brightness levels above 88 GE and print surfaces that enable photographic lithography, reinforcing its grip on price-sensitive but graphics-intensive categories. Folding Boxboard is expected to post an 8.75% CAGR, the fastest rate among substrates, as quick-service restaurants and e-commerce fulfillment centers adopt weights in the 250-300 gsm range to curb freight surcharges. Coated Unbleached Kraft is strengthening its foothold in electronics and household-goods shippers because Decree 110/2026 rewards recycled-content compliance, while White Line Chipboard supplies cost-conscious dry-food fillers.

Tetra Pak's expansion to 30 billion packs annually highlights the centrality of barrier-coated Solid Bleached Sulfate to aseptic dairy and juice lines, a niche that shields profits even amid pulp inflation. As recycled-content thresholds climb, converters are blending virgin and secondary fiber to safeguard tensile integrity without breaching cost targets. Inline basis-weight scanners, near-infrared moisture controls, and high-consistency refiners help large mills deliver tighter grammage tolerances, a precondition for multinationals that link payout terms to statistical process control metrics. Smaller converters unable to finance such upgrades risk relegation to low-margin commodity cartons. The Vietnam folding carton market size advantage therefore gravitates toward operators that couple substrate versatility with capital-intensive quality systems.

List of Companies Covered in this Report:

- Dong Tien Packaging and Paper Co. Ltd.

- Oji Packaging (Vietnam) Co. Ltd.

- Rengo Co. Ltd.

- Marubeni-South East Asia Packaging Corp.

- Tetra Pak Vietnam JSC

- Song Lam Packaging JSC

- Siam Kraft Industry Co. Ltd.

- Lee & Man Paper Manufacturing Ltd.

- Thuan An Paper and Packaging JSC

- AnBinh Printing Carton Packaging Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand From the E-Commerce Sector

- 4.2.2 Government Push for Sustainable Packaging

- 4.2.3 Growth in Food and Beverage Exports

- 4.2.4 Rising Disposable Income and Urbanization

- 4.2.5 Rise of High-Color Digital Short Runs for SMEs

- 4.2.6 Premium Carton Demand From Domestic Craft Beer Brands

- 4.3 Market Restraints

- 4.3.1 Volatility in Virgin Fiber Prices

- 4.3.2 Intensifying Competition From Flexible Packaging

- 4.3.3 Logistics Bottlenecks at Key Port Facilities

- 4.3.4 Limited Advanced Paper Recycling Capacity

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Dong Tien Packaging and Paper Co. Ltd.

- 6.4.2 Oji Packaging (Vietnam) Co. Ltd.

- 6.4.3 Rengo Co. Ltd.

- 6.4.4 Marubeni-South East Asia Packaging Corp.

- 6.4.5 Tetra Pak Vietnam JSC

- 6.4.6 Song Lam Packaging JSC

- 6.4.7 Siam Kraft Industry Co. Ltd.

- 6.4.8 Lee & Man Paper Manufacturing Ltd.

- 6.4.9 Thuan An Paper and Packaging JSC

- 6.4.10 AnBinh Printing Carton Packaging Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment