|

시장보고서

상품코드

2065577

계약업체 공식대리인(AOR) 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Agent Of Record (AOR) For Contractors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

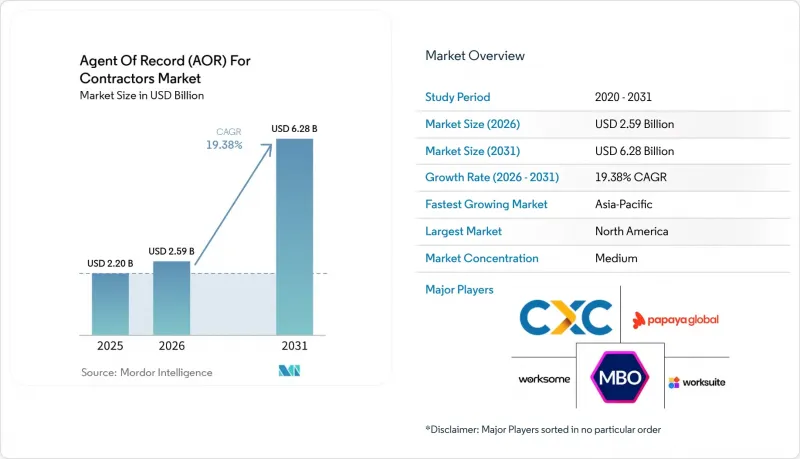

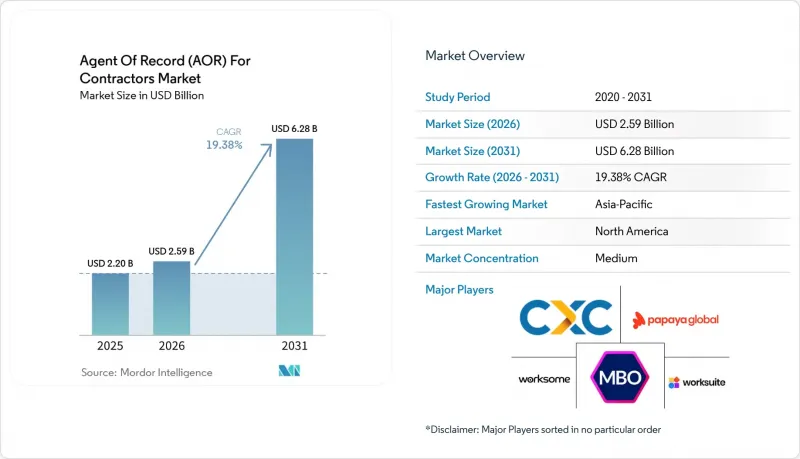

Mordor Intelligence에 의하면, 계약업체 공식대리인(AOR) 시장은 2025년 22억 달러로 평가되었고, 2026년에는 25억 9,000만 달러로 추정되고, 2026-2031년 CAGR 19.38%로 성장을 지속할 전망이며, 2031년까지 62억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 서비스 유형별(컴플라이언스, 근로자 분류 등), 기업 규모별(중소기업 등), 도입 모델별(클라우드 기반, 하이브리드형 등), 인력 유형별(독립형 업무 위탁 및 프리랜서 등), 최종 사용자 산업별(BFSI 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 계약업체 공식대리인(AOR) 시장 동향 및 인사이트

증가하는 국경을 초월한 원격 업무 위탁 채용

국경을 넘는 업무 위탁의 도입은 틈새 관행에서 출발해, 규모가 급속히 확대되는 기업들의 표준 운영 모델로 변화했습니다. 자금 조달 규모가 큰 스타트업의 88%는 설립 후 18개월 이내에 여러 국가에서 사업을 전개하고 있으며, 2025년에는 국경을 초월한 AI 트레이너 채용이 283% 증가했습니다. 이로 인해 기업이 현지 업무 위탁 관련 규정이나 세무 절차를 파악하지 못한 국가에서 채용을 진행하게 됨에 따라, 구매 관련 과제가 변화하고 있습니다. AOR 플랫폼은 계약, 원천징수, 관할 구역을 넘나드는 규정 준수 대응에 있어 법적 중개자 역할을 수행함으로써 이러한 격차를 해소하고 있습니다. 그 결과, 계약업체 공식대리인(AOR) 시장은 채용 규모와 마찬가지로 법적 복잡성에 의해서도 성장하고 있습니다.

근로자 분류 오류에 대한 단속 강화

오분류의 위험은 몇년전과 비교해 재무·법무 부문의 우선 과제 중 훨씬 더 높은 순위를 차지하게 되었습니다. 미국 국세청(IRS)은 세무 절차 2025-10에서 고용세 미납액이 연간 1,190억 달러에 달한다고 밝히며, 감독을 강화하겠다는 분명한 의향을 나타냈습니다. 또한, 미국 노동부도 2024년 1월 9일 독립 계약자 지위에 관한 최종 규정을 발표하여, 과도한 분류 관행의 여지를 좁혔습니다. ‘현장 지원 공문(Field Assistance Bulletin) 2025-1’에 따라 2025년 5월에 직접적인 집행이 일시 중단되기는 했으나, 구매자 입장에서의 근본적인 불확실성은 해소되지 않았습니다. 이러한 불확실성으로 인해, 활동이 여러 주나 국가에 걸쳐 있는 경우, 자율 관리형 업무 위탁 프로그램을 정당화하기 어려워집니다. 현재 책임 전가가 구매 분야의 최우선 과제로 대두됨에 따라, 이러한 상황은 계약업체 공식대리인(AOR) 시장 수요를 지속적으로 뒷받침하고 있습니다.

AOR, EOR, 결제 전용 도구에 대한 구매자의 혼란

구매자 측의 혼란은 계약업체 공식대리인(AOR) 시장에서 여전히 실질적인 판매 장벽으로 작용하고 있습니다. 많은 조달 부서와 법무 팀은 AOR, EOR, 지급 기능만을 제공하는 도구를 마치 그 도구들이 동일한 문제를 해결하는 것처럼 취급하고 있습니다. 그 결과, 구매 범위가 불충분해지거나, 계약 체결까지의 절차가 지연되거나, 규정 준수 심사나 감사 후에 전환 비용이 높아지는 사태를 초래하고 있습니다. 뉴욕주 금융서비스국은 2025년 10월, 금융기관에 제3자 위험 심사를 강화할 것을 요청함으로써 규제를 한층 더 강화했습니다. 이로 인해 규제 대상 구매 주기에서 제품 간의 차이가 더욱 중요해지고 있습니다. 법적 대표자로서의 지위, 분류 범위, 보상 조항을 명확하게 설명하는 공급업체는 나중에 규정 준수 조항을 추가하기만 한 ‘지급 우선’ 공급업체보다 계약 성사율이 더 높습니다.

부문별 분석

2025년, 보험, 배상 책임, 리스크 완화 부문은 서비스 수익의 31.42%를 차지했으며, 계약업체 공식대리인(AOR) 시장에서 가장 큰 점유율을 기록했습니다. 이러한 선두 위치는 구매자들의 명확한 선호도를 반영하고 있습니다. 즉, 기업들은 컴플라이언스 관련 위험을 단순히 문서화하는 데 그치지 않고, 이를 흡수해 줄 수 있는 서비스 제공업체를 찾고 있는 것입니다. 어떤 국가에서 오분류에 대한 벌칙이 강화되면, 일반적으로 보험을 통한 보상 수요도 그에 따라 증가합니다. ‘업무 위탁 온보딩 및 계약 관리’ 시장은 발주처가 각 단계에서 법적 심사를 반복하지 않고 업무 위탁의 가동을 가속화하고자 함에 따라, 2031년까지 연평균 성장률(CAGR) 21.47%를 나타낼 것으로 예측됩니다.

규정 준수 및 근로자 분류 관리, 그리고 전 세계적인 업무 위탁에 대한 대금 지급 및 세무 서류 작성은 여전히 대부분의 플랫폼 스택 운영의 핵심을 이루고 있습니다. 여러 국가에 걸쳐 세무 서류 및 청구서 관련 규정을 동시에 관리하기가 어려워짐에 따라, 이러한 기능의 중요성은 더욱 커지고 있습니다. 업무 위탁의 라이프사이클 관리, 인력 분석 및 보고서 작성은 여전히 규모가 작은 서비스 분야이지만, 다수의 업무 위탁을 담당하고 있는 기업들로부터 주목을 받기 시작하고 있습니다. AOR 업계에서는 배상책임보험에서 분석 기능으로 서비스를 확장할 수 있는 벤더가, 단순히 규정 준수 서비스만을 제공하는 업체보다 고객 유지율이 더 높은 입지를 다져가고 있습니다.

2025년 기준으로 중소기업(SME)은 계약업체 공식대리인(AOR) 시장의 58.27%를 차지했으나, 대기업의 경우 2031년까지 연평균 성장률(CAGR) 22.63%로 확대될 것으로 전망됩니다. 중소기업은 핵심적인 인력 배치 모델로 업무 위탁에 의존하는 경우가 많기 때문에 각 계약에는 기업 차원에서 더욱 뚜렷하게 드러나는 컴플라이언스 리스크가 수반됩니다. 대기업들은 사내 검토를 통해 계약직 직원에 대한 관리 체제가 세무상 위험 및 고정사업장(PE) 위험과 관련이 있다는 사실이 밝혀진 후, 이 분야에 대한 진출을 가속화했습니다. 현재 많은 다국적 기업들은 인력의 유연성을 유지하면서 가장 위험이 큰 격차를 해소할 수 있기 때문에 광범위한 재분류보다는 AOR 조달을 선호하는 추세입니다.

주요 고객사에 서비스를 제공하는 각 벤더사는 독립형 대시보드가 아닌, 주요 HCM(인적 자원 관리) 시스템 및 재무 시스템과의 통합을 통해 차별화를 꾀하고 있습니다. 조달팀은 데이터 중복을 방지하고, 법무, 재무, 인사 각 부서 간에 기록이 일치하도록 요구하고 있습니다. 인도, 베트남, 필리핀에서의 사업 확장 속도도 중요합니다. 왜냐하면, 전 세계의 업무 위탁 프로그램이 현재 여러 국가에서 동시에 시작되고 있기 때문입니다. 이로 인해 계약업체 공식대리인(AOR) 시장이 지역 차원의 활용 사례에서 전사적 거버넌스로 전환될 때, 풀스택형 제공업체에게 경쟁 우위가 생깁니다.

지역별 분석

2025년, 북미는 계약업체 공식대리인(AOR) 시장 점유율의 47.19%를 차지했으며, 지역별로는 가장 큰 기여를 한 지역이 되었습니다. 미국이 이러한 위치를 주도하고 있는 이유는 오랫동안 업무 위탁이 일반화되어 왔고, 법규 집행에 대한 압박도 크기 때문입니다. ‘Revenue Procedure 2025-10’은 수십년만에 섹션 530의 세이프하버 기준을 개정함으로써, 분류 위험에 대한 가시성을 높였습니다. 2024년 독립 계약자 지위에 관한 연방 규정과 2025년의 집행 유예 조치가 맞물리면서, 법적 환경은 완화되기는커녕 불안정한 상태가 지속되었습니다. 캐나다와 멕시코에서는 긱 워크에 대한 규제가 발전하고, 니어쇼어 업무 위탁의 활용이 확대됨에 따라 지역적 수요가 더욱 높아졌습니다.

아시아태평양은 계약업체 공식대리인(AOR) 시장에서 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR)이 24.37%를 나타낼 것으로 전망됩니다. 인도는 특히 두드러지는데, Quess Corp에 따르면 2026년 기준으로 인도에는 전 세계 약 2,000개의 역량 센터가 존재하며, 노동력의 24%가 계약직 형태로 고용되어 있었다고 합니다. 인도 인력파견연맹(Indian Staffing Federation)의 보고서에 따르면, 2026년도 2분기 유연 노동력 인구는 191만 명으로, 비정규직을 포함하지 않더라도 정규 계약직의 기반이 매우 크다는 사실이 드러났습니다. 호주 및 뉴질랜드는 도입이 비교적 성숙한 시장인 반면, 동남아시아 시장에서는 급여, 세금, 서류 처리 관련 규정을 신속하게 조정할 수 있는 서비스 제공업체가 높이 평가받고 있습니다.

유럽은 지역별 기준으로 두 번째로 큰 시장이며, 그 규제의 성숙도는 수요를 뒷받침하는 한편, 서비스 제공업체에 대한 진입 장벽도 높이고 있습니다. EU의 ‘플랫폼 노동 지침’은 2026년 12월을 국내법 반영 기한으로 정하고 있으며, 이에 따라 업무 위탁 관계에 대한 문서화 및 보다 명확한 법적 구조의 필요성이 대두되고 있습니다. 영국에서는 IR35와 유사한 엄격한 심사가 계속 이루어지고 있지만, 남미, 중동 및 아프리카는 도입 초기 단계에 있는 지역이며, 브라질, UAE, 남아프리카공화국에서는 수요가 확대되고 있습니다. 또한, 독일, 벨기에, 프랑스에서 전자 청구서 사용이 의무화된 것도 업무 위탁 대금 지급 워크플로우를 구조화된 데이터로 전환하는 요인이 되고 있으며, 이는 규정 준수 체제가 잘 갖춰진 공급업체에 유리하게 작용하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the agent of Record (AOR) for contractors market is expected to grow from USD 2.20 billion in 2025 to USD 2.59 billion in 2026, and is forecast to reach USD 6.28 billion by 2031 at a 19.38% CAGR over 2026-2031.

This report is Segmented by Service Type (Compliance and Worker Classification, and More), Enterprise Size (Small and Medium-Sized Enterprises, and More), Deployment Model (Cloud-Based, Hybrid, and More), Workforce Type (Independent Contractors and Freelancers, and More), End-User Industry (BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agent Of Record (AOR) For Contractors Market Trends and Insights

Rising Cross-Border Remote Contractor Hiring

Cross-border contractor hiring has shifted from a niche practice to a standard operating model for fast-scaling companies. 88% of the top-funded startups operated across multiple countries within 18 months of founding, and AI trainer roles grew 283% in cross-border engagements in 2025. This changes the buying problem because enterprises are now hiring in countries where they do not know the local contractor rules or tax processes. AOR platforms fill that gap by acting as the legal intermediary for contracts, withholding, and compliance handling across jurisdictions. As a result, the Agent of Record (AOR) for contractors market is being driven as much by legal complexity as by hiring volume.

Tighter Worker Misclassification Enforcement

Misclassification risk now sits much higher on finance and legal agendas than it did a few years ago. The Internal Revenue Service said the employment tax gap was USD 119 billion per year in Revenue Procedure 2025-10, which signaled a clear intent to tighten oversight. The U.S. Department of Labor also issued its final rule on independent contractor status on January 9, 2024, which narrowed the room for aggressive classification practices. Even though Field Assistance Bulletin 2025-1 paused direct enforcement in May 2025, it did not remove the underlying uncertainty for buyers. That uncertainty makes self-managed contractor programs harder to defend once the activity spans many states or countries. This continues to support the Agent of Record (AOR) for Contractors market because liability transfer is now a purchasing priority.

Buyer Confusion Between AOR, EOR, and Payment-Only Tools

Buyer confusion remains a real sales barrier in the Agent of Record (AOR) for contractors market. Many procurement and legal teams still treat AOR, EOR, and payment-only tools as if they solve the same problem. That leads to under-scoped purchases, slower conversions, and higher switching costs after a compliance review or audit. The New York State Department of Financial Services added another layer in October 2025 by asking financial institutions to strengthen third-party risk review, which makes product differences more material in regulated buying cycles.Providers that clearly explain legal-principal status, classification coverage, and indemnification terms are converting better than payment-first vendors with retrofitted compliance language.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise Shift Toward Blended Workforce Models

- Demand for Unified Contractor Onboarding, Tax, And Payment Workflows

- Fragmented Local Labor and Tax Rules Across Jurisdictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Insurance, Liability, and Risk Mitigation accounted for 31.42% of service revenue in 2025, giving it the largest position within the Agent of Record (AOR) for contractors market. That lead reflects a clear buyer preference: enterprises want providers that absorb compliance exposure rather than only document it. When misclassification penalties rise in a country, demand for insurance-backed coverage usually rises with them. Contractor Onboarding and Contract Administration is projected to grow at a 21.47% CAGR through 2031, as buyers seek to accelerate contractor activation without repeating legal review at every step.

Compliance and Worker Classification Management and Global Contractor Payments and Tax Documentation remain the operational center of most platform stacks. These functions matter more as tax documentation and invoice rules become harder to manage across multiple countries simultaneously. Contractor Lifecycle Management and Workforce Analytics and Reporting are still smaller service lines, but they are gaining more attention from enterprises with large contractor populations. In the Agent of Record (AOR) industry, vendors that can extend from liability coverage into analytics are building a stickier position than compliance-only providers.

SMEs held 58.27% of the Agent of Record (AOR) for contractors market share in 2025, while Large Enterprises are projected to expand at a 22.63% CAGR through 2031. SMEs often depend on contractors as a core staffing model, so each engagement carries more visible compliance risk at the company level. Large enterprises moved faster into this category after internal reviews linked contractor governance to tax and permanent establishment exposure. Many multinationals now prefer AOR procurement over broad reclassification because it preserves workforce flexibility while closing the most exposed gaps.

Vendors serving larger accounts are differentiating through integration with major HCM and finance systems rather than through standalone dashboards. Procurement teams want synchronized records across legal, finance, and workforce functions, not duplicate data layers. Speed of rollout across India, Vietnam, and the Philippines also matters because global contractor programs are now launched across several countries at once. This gives full-stack providers an advantage when the Agent of Record (AOR) for Contractors market shifts from local use cases to enterprise-wide governance.

Geography Analysis

North America held 47.19% of the Agent of Record (AOR) market share for contractors in 2025, making it the largest regional contributor. The United States anchors that position because contractor engagement has been common for years, and enforcement pressure is high. Revenue Procedure 2025-10 heightened visibility into classification risk by updating Section 530 safe-harbor standards for the first time in decades. The 2024 federal rule on independent contractor status and the 2025 enforcement pause together kept the legal environment unsettled rather than relaxed. Canada and Mexico added to regional demand as gig-work regulation evolved and nearshore contractor use expanded.

Asia-Pacific is the fastest-growing region in the Agent of Record (AOR) for contractors market, with a projected 24.37% CAGR through 2031. India stands out because Quess Corp said the country had around 2,000 global capability centers in 2026, and 24% of its workforce was in contract arrangements. The Indian Staffing Federation reported a flexi-workforce population of 1.91 million in Q2 FY2026, indicating a large formal contractor base, even before informal hiring is counted. Australia and New Zealand are more mature adopters, while Southeast Asian markets reward providers that can quickly adjust pay, tax, and documentation logic.

Europe is the second-largest regional market, and its regulatory maturity both supports demand and raises the bar for providers. The EU Platform Work Directive set a December 2026 transposition deadline, which increases the need for documented contractor relationships and clearer legal structures. The United Kingdom remains adjacent through IR35-style scrutiny, while South America, the Middle East, and Africa are earlier-stage regions with growing demand pockets in Brazil, the UAE, and South Africa. E-invoicing mandates in Germany, Belgium, and France also push contractor payment workflows toward structured data, favoring vendors with stronger compliance infrastructure.

- Global Contractor Management Solutions Pty Ltd

- MBO Partners, Inc.

- Worksome ApS

- Worksuite Inc.

- Papaya Global Ltd.

- Oyster HR, Inc.

- Remofirst, Inc.

- Lano Software GmbH

- TalentDesk Services Limited

- Transformify Ltd

- Pilot Platform Inc.

- AllWork, Inc.

- SafeGuard World International Limited

- GoGlobal K.K.

- YunoJuno Limited

- Remote Technology, Inc.

- FoxHire

- Mercans

- INS Global

- Wisemonk

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Cross-Border Remote Contractor Hiring

- 4.2.2 Tighter Worker Misclassification Enforcement

- 4.2.3 Enterprise Shift Toward Blended Workforce Models

- 4.2.4 Demand For Unified Contractor Onboarding, Tax, And Payment Workflows

- 4.2.5 OECD Permanent Establishment Monitoring For Borderless Workforces

- 4.2.6 Country-Level E-Invoicing And Tax Documentation Complexity

- 4.3 Market Restraints

- 4.3.1 Buyer Confusion Between AOR, EOR, And Payment-Only Tools

- 4.3.2 Fragmented Local Labor And Tax Rules Across Jurisdictions

- 4.3.3 EU Platform Work Directive Compliance Spillover

- 4.3.4 IP Assignment, Data Residency, And AML Friction In Contractor Onboarding

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Comptetive Rivalary

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Compliance and Worker Classification Management

- 5.1.2 Contractor Onboarding and Contract Administration

- 5.1.3 Global Contractor Payments and Tax Documentation

- 5.1.4 Insurance, Liability and Risk Mitigation

- 5.1.5 Contractor Lifecycle Management

- 5.1.6 Workforce Analytics and Reporting

- 5.2 By End User Enterprise Size

- 5.2.1 Small and Medium-Sized Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Deployment Model

- 5.3.1 Cloud-Based

- 5.3.2 Hybrid

- 5.3.3 On-Premises

- 5.4 By Workforce Type

- 5.4.1 Independent Contractors and Freelancers

- 5.4.2 Cross-border Contractors

- 5.4.3 Contingent Workforce

- 5.4.4 SOW Contractors

- 5.4.5 Distributed Project Teams

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecom

- 5.5.4 Retail and E-commerce

- 5.5.5 Industrial Manufacturing

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Netherlands

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Global Contractor Management Solutions Pty Ltd

- 6.4.2 MBO Partners, Inc.

- 6.4.3 Worksome ApS

- 6.4.4 Worksuite Inc.

- 6.4.5 Papaya Global Ltd.

- 6.4.6 Oyster HR, Inc.

- 6.4.7 Remofirst, Inc.

- 6.4.8 Lano Software GmbH

- 6.4.9 TalentDesk Services Limited

- 6.4.10 Transformify Ltd

- 6.4.11 Pilot Platform Inc.

- 6.4.12 AllWork, Inc.

- 6.4.13 SafeGuard World International Limited

- 6.4.14 GoGlobal K.K.

- 6.4.15 YunoJuno Limited

- 6.4.16 Remote Technology, Inc.

- 6.4.17 FoxHire

- 6.4.18 Mercans

- 6.4.19 INS Global

- 6.4.20 Wisemonk

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment