|

시장보고서

상품코드

2072708

매니지드 HR 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Managed HR Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

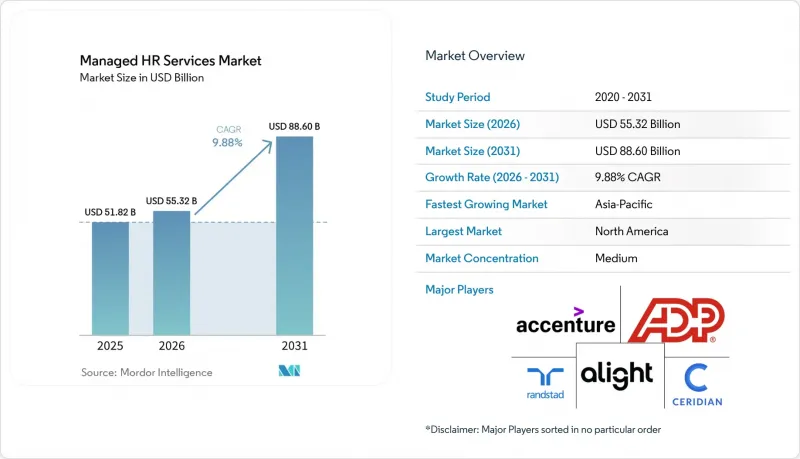

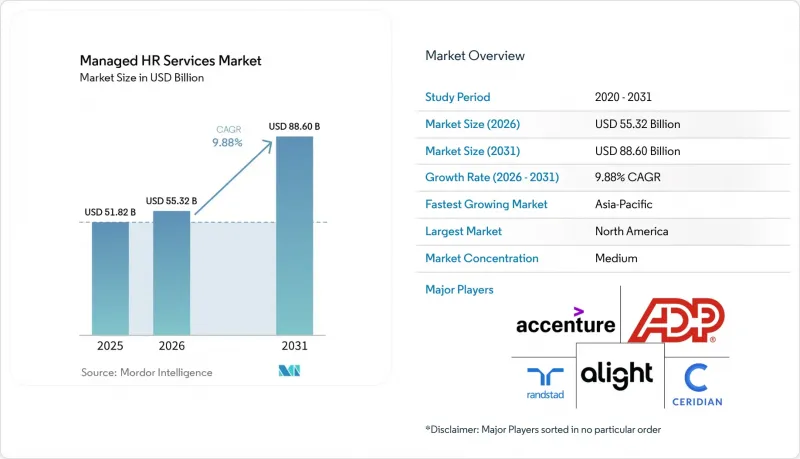

Mordor Intelligence에 의하면, 매니지드 HR 서비스 시장 규모는 2025년 518억 2,000만 달러로 평가되었고, 2031년까지 553억 2,000만 달러에서 886억 달러로 확대될 전망이며, 2026-2031년 CAGR 9.88%를 나타낼 것으로 예측됩니다.

본 보고서는 서비스 유형별(채용 프로세스 아웃소싱(RPO), 급여 및 복리후생 관리 서비스 등), 제공 모델별(클라우드, 하이브리드, 온프레미스), 기업 규모별(대기업, 중소기업), 최종 사용자 산업 분야별(은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 매니지드 HR 서비스 시장 동향 및 인사이트

핵심 인사 업무의 아웃소싱 증가

기업들이 급여 계산, 복리후생, 인사 업무 및 기술 지원을 소수 공급업체에 집중함에 따라, 매니지드 HR 서비스 시장은 전체 프로세스 아웃소싱으로 더욱 전환되고 있습니다. 인사 업무는 데이터 의존도가 높아지고, 규정 위반 위험에 노출될 가능성도 커지고 있기 때문에 구매 기업들은 현재 인사 업무의 외부 위탁을 단기적인 비용 절감 방안이 아닌 운영 모델의 한 가지 선택지로 보고 있습니다. 서비스 수준은 급여 계산의 정확성, 규정 준수율, 그리고 직원 경험과 점점 더 밀접하게 연결되어 있으며, 그 결과 인력 차익 거래에만 의존하는 공급업체의 매력은 떨어지고 있습니다. 2026년 4월 현재, 140개국 이상에 걸쳐 110만 개 이상의 기업이 주요 인사·급여 플랫폼을 이용하고 있으며, 이는 매니지드 HR 서비스 시장에서 대규모 플랫폼 제공업체가 지닌 규모의 경제를 여실히 보여주고 있습니다. 이러한 규모가 중요한 이유는 중견 기업의 구매 담당자가 사내에서 도구를 구축하는 대신, 아웃소싱 계약을 통해 이직률 모니터링, 급여 벤치마킹, 인력 계획 등의 분석 기능을 활용할 수 있기 때문입니다. 그 결과, 매니지드 HR 서비스 시장에서는 멀티타워형 제휴에 대한 수요가 높아지고 있는 반면, 핵심 HR 업무별로 개별 공급업체를 관리하려는 구매 기업은 줄어들고 있습니다.

다국적 급여 계산의 표준화 필요성

매니지드 HR 서비스 시장은 여러 세제, 신고 및 복리후생 시스템에 걸쳐 급여 계산을 운영하기가 어렵다는 점에 의해서도 형성되고 있습니다. 2025년에는 36% 이상의 조직이 6개국 이상에서 급여 계산을 처리하고 있었으며, 7%의 조직은 51개 이상의 지역에서 사업을 전개하고 있었습니다. 이처럼 광범위한 상황에서는 특히 직원 수, 이직률, 보상 분석을 위해 급여 데이터가 필요한 경우, 사내 급여 계산의 표준화를 관리하기가 어렵습니다. 2026년 5월에 출시된 'Workforce AI'를 탑재한 급여 계산 플랫폼은 예외 사항에 대해서는 사람의 확인을 유지하면서 급여 계산 처리를 '며칠'에서 '몇 시간'으로 단축되도록 설계되어 있으며, 이는 구매자의 기대가 어디로 향하고 있는지를 반영하고 있습니다. 실시간 신고 규정, 임금 투명성 의무화, 사회보험료 변경 등이 각국에서 점점 더 복잡해지고 있습니다. 매니지드 HR 서비스 시장에서 원생 다국어 지원 기능을 갖춘 서비스 제공업체는 지연을 줄이고, 업무 인계를 최소화하며, 급여 계산 업무 전반에 걸친 데이터의 일관성을 높이기 때문에 뚜렷한 우위를 점하고 있습니다.

데이터 개인정보 보호 및 직원 정보의 보안 위험

데이터 보호는 매니지드 HR 서비스 시장의 추가적인 성장을 가로막는 가장 뚜렷한 제약 요인 중 하나로 남아 있습니다. 아웃소싱된 HR 환경에는 대규모 직원 그룹의 급여 기록, 은행 계좌 정보, 복리후생 데이터, 개인 식별 정보가 보관되어 있어 랜섬웨어나 데이터 도난의 주요 표적이 됩니다. 현재 구매자는 공급업체를 평가할 때 서비스 범위뿐만 아니라, 접근 제어, 감사 대응 체계, 사고 대응, 그리고 정보 유출 시 통지에 관한 조치에 대해서도 검토하고 있습니다. 2025-2026년 이루어진 개인정보 보호 규정 변경은 아웃소싱 계약상의 책임 분배 및 리스크 관리 방식에 영향을 미쳤습니다. 이로 인해, 특히 규제가 엄격한 업계나 국경을 넘는 거래에서 공급업체 선정에 드는 비용과 시간이 증가하고 있습니다. 따라서 매니지드 HR 서비스 시장에서는 단순히 폭넓은 서비스 메뉴를 제공하는 것뿐만 아니라, 성숙한 보안 관리 체계, 공동 처리자로서의 규정 준수, 그리고 재현 가능한 거버넌스를 입증할 수 있는 제공업체가 선호되는 추세입니다.

부문별 분석

2025년, 급여 및 복리후생 관리는 매니지드 HR 서비스 시장의 32.47%를 차지했으며, 이 부문의 주요 수익원으로 자리매김했습니다. 급여 지급은 지연이 허용되지 않으며, 규정 준수상의 오류가 고용주에게 직접적인 재정적·법적 위험을 초래할 가능성이 있기 때문에 이 부문은 여전히 필수적입니다. 따라서 기업들은 비용 절감이나 업무 간소화를 위해 다른 서비스 분야를 재검토하고 있는 경우에도, 급여 업무를 사내에서 재구축하는 데는 소극적인 태도를 보이고 있습니다. 채용 프로세스 아웃소싱은 채용 인원이 변동적이고 채용까지의 기간이 상업적으로 중요한 BFSI(은행 및 금융 및 보험) 및 기술 분야에서 안정적인 수요를 유지했습니다. 또한, 직원 기록, 서비스 요청, 문서 관리, 일상적인 사무 처리에서 표준화된 업무 흐름을 원하는 구매자들에게 있어 인사 업무 아웃소싱도 여전히 중요한 위치를 차지했습니다.

HR 기술 관리 서비스는 2026-2031년 연평균 성장률(CAGR) 12.86%를 나타낼 것으로 예측되며, 매니지드 HR 서비스 시장에서 가장 빠르게 성장하는 서비스 부문이 될 전망입니다. 이러한 성장을 주도하고 있는 것은 대규모 사내 지원팀보다는 Workday, SAP SuccessFactors, Oracle HCM Cloud를 활용해 성과 중심의 관리를 선호하는 기업들입니다. 2025 회계연도 전체 기간 동안, HR 및 재무 프로세스 관리 업무 전반에 걸친 데이터, AI, 에이전트형 솔루션을 바탕으로 첨단 기술 솔루션의 매출이 17% 증가했습니다. 또한, 2026년 5월 AI 기반 인력 관리 플랫폼이 출시됨에 따라, 급여 계산, HR 워크플로우, 근태 관리, 복리후생 관리가 중소기업을 대상으로 단일 서비스로 통합되고 있음이 드러났습니다. 학습 및 인재 관리 서비스는 자문 및 규정 준수 지원과 결합되어, 고객이 재교육, 정책 보장 및 보다 원활한 데이터 흐름을 요구하는 가운데, 보다 광범위한 매니지드 HR 서비스 업계 전반에서 그 중요성이 더욱 커졌습니다.

2025년에는 클라우드 기반 관리형 서비스가 매출의 63.29%를 차지했으며, 이 모델이 매니지드 HR 서비스 시장에서 가장 큰 점유율을 기록했습니다. 이 방향은 자동 갱신, 유연한 용량, 신속한 보고서 작성을 지원하는 클라우드 네이티브 HR 플랫폼으로의 장기적인 전환을 반영하고 있습니다. 또한, 구매 기업은 급여, 복리후생, 근태, 사례 관리 등의 데이터를 연동되지 않은 여러 도구에 분산시키지 않고, 단일 운영 모델로 통합할 수 있다는 점을 중요하게 여기고 있습니다. 클라우드를 통한 제공은 특히 분석, 직원용 셀프 서비스, 워크플로우 자동화 분야에서 새로운 기능의 도입 속도를 높이는 경우가 많습니다. 그렇다고는 해도, 모든 기업이 기밀성이 높은 직원 데이터를 모두 완전한 퍼블릭 클라우드 환경으로 이전할 수 있는 것은 아닙니다.

하이브리드형 도입은 2031년까지 연평균 성장률(CAGR) 11.72%로 확대될 것으로 예측되며, 매니지드 HR 서비스 시장에서 가장 빠르게 성장하는 도입 형태가 될 전망입니다. 금융 서비스 및 헬스케어 업계의 도입 기업들이 주요 원동력이 되고 있습니다. 이러한 업계에서는 기밀성이 높은 기록이나 레거시 시스템에 대한 관리 권한을 잃지 않으면서도 클라우드의 유연성이 필요한 경우가 많기 때문입니다. 2026년 5월에 발표된 '자율형 HCM'이 프레임워크는 클라우드와 온프레미스의 각 계층에 걸친 AI 오케스트레이션을 지원하며, 하이브리드 환경의 지속이 더 이상 일시적인 단계가 아니라 설계상의 전제가 되었음을 시사합니다. 온프레미스 지원은 여전히 주권적 스토리지 규제나 장기 계약이 유지되고 있는 남미 및 중동 일부 지역의 정부 기관과 정부 산하 기관에 도움이 되고 있습니다. 매니지드 HR 서비스 시장이 고르지 않은 현대화 주기를 거치는 가운데, 이 세 가지 모델을 모두 아우를 수 있는 서비스 제공업체는 고객의 지출을 유지하는 데 있어 더 유리한 입장에 있습니다.

지역별 분석

2025년, 북미는 매니지드 HR 서비스 시장 점유율의 38.92%를 차지했으며, 지역별로는 가장 큰 기여도를 보였습니다. 이 지역은 폭넓은 고객 기반, 대규모 다국적 기업의 본사, 그리고 대규모 자체 관리형 HR을 유지하기 어렵게 만드는 규제 환경과 같은 장점을 갖추고 있습니다. 2026년 4월 현재, 140개국 이상에 걸쳐 110만 개 이상의 기업이 주요 인사 및 급여 플랫폼을 이용하고 있으며, 이는 매니지드 HR 서비스 시장에서 미국 시장의 핵심 부문이 지닌 규모와 성숙도를 여실히 보여주고 있습니다. 대규모 인수를 통해 중견 시장으로의 진출 범위가 확대되었으며, 소규모 조직을 위한 HCM 기능이 강화되었습니다. 한편, 멕시코와 캐나다에서는 국경을 넘는 고용, 제조, 물류에 필요한 통합 급여 계산 및 규정 준수 워크플로우에 대한 수요가 증가하고 있습니다.

유럽은 막대한 수요와 엄격한 노동 규제가 맞물리면서, 매니지드 HR 서비스 시장에서 여전히 큰 비중을 차지하고 있습니다. 독일, 영국, 프랑스, 네덜란드가 도입을 주도하고 있지만, 근로자 대표 위원회, 아웃소싱 관행, 현지 고용 규정이 통일되어 있지 않아 구매자의 요구 사항은 국가마다 다릅니다. 영국에서는 순수하게 비용 위주의 계약에서 기술을 활용한 성과 기반 모델로 전환되고 있으며, 이를 통해 전 세계의 서비스 제공업체와 지역 전문 기업 모두에게 활약의 무대가 마련되고 있습니다. AI를 활용한 채용 분석과 북유럽 및 중부 유럽 전역에 걸친 다국적 급여 계산 서비스 제공은 지역에 뿌리를 둔 기업이 대형 플랫폼에 맞서 어떻게 입지를 지켜내고 있는지를 보여줍니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 15.36%로 확대될 것으로 예상되며, 매니지드 HR 서비스 시장에서 가장 빠르게 성장하는 지역 부문으로 꼽히고 있습니다. 인도는 전 세계 공급업체들에게 주요 서비스 제공 거점인 동시에, Global Capability Center(GCC)의 활동이 확대됨에 따라 성장을 거듭하는 구매자 시장으로서도 이중적인 역할을 수행하고 있습니다. 중국, 동남아시아, 일본, 한국, 호주, 뉴질랜드 역시 현대화 프로그램, 노동력의 고령화, 성숙한 아웃소싱 생태계를 통해 지역 성장을 뒷받침하고 있습니다. 중동 및 아프리카은 현재로서는 규모가 작지만, 사우디아라비아의 노동력 자국화 정책과 남아프리카공화국 및 나이지리아의 고용 관행 제도화가 규정 준수 및 급여 계산 관련 전문 서비스에 대한 수요를 뒷받침하고 있습니다. 남미는 여전히 새로운 기회가 있는 시장이며, 빈번한 노동 규제 변경, 통화 변동 압력, 그리고 여러 관할 구역에 걸친 급여 계산의 필요성으로 인해, 기술 예산이 제한된 상황에서도 매니지드 HR 서비스 시장의 중요성은 여전히 유지되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the managed HR services market size is projected to expand from USD 51.82 billion in 2025, USD 55.32 billion to USD 88.60 billion by 2031, registering a CAGR of 9.88% during 2026-2031.

This report is Segmented by Service Type (Recruitment Process Outsourcing (RPO), Payroll and Benefits Administration Services, and More), Deployment Model (Cloud, Hybrid, and On-Premise), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Managed HR Services Market Trends and Insights

Rising Outsourcing of Core HR Operations

The managed HR services market is moving further toward full-process outsourcing as enterprises combine payroll, benefits, HR operations, and technology support under fewer vendors. Buyers now treat external HR delivery as an operating model choice rather than a short-term cost program, because HR has become more data-intensive and more exposed to compliance failures. Service levels are increasingly tied to payroll accuracy, compliance pass rates, and employee experience, thereby reducing the appeal of providers that rely solely on labor arbitrage. More than 1.1 million clients across 140-plus countries relied on a major HR and payroll platform as of April 2026, which shows the scale advantage large platform providers hold in the managed HR services market. This scale matters because mid-sized buyers can access analytics such as attrition monitoring, pay benchmarking, and workforce planning through outsourced contracts rather than building those tools internally. As a result, the managed HR services market is seeing more demand for multi-tower relationships and fewer buyers willing to manage separate point vendors across core HR tasks.

Need for Multi-Country Payroll Standardization

The managed HR services market is also being shaped by the difficulty of running payroll across multiple tax, filing, and benefits systems. More than 36% of organizations handled payroll in 6 or more countries, and 7% operated across 51 or more territories in 2025. That level of spread makes internal payroll standardization hard to manage, especially when payroll data is also needed for headcount, turnover, and compensation analysis. A payroll platform with Workforce AI launched in May 2026 was designed to cut payroll processing from days to hours while keeping human review for exceptions, which reflects where buyer expectations are moving. Real-time filing rules, wage transparency mandates, and social contribution changes have continued to add complexity across countries. In the managed HR services market, providers with native multi-country capability have a clear advantage because they reduce latency, cut handoffs, and improve data consistency across payroll operations.

Data Privacy And Employee Information Security Risks

Data protection remains one of the clearest limits on faster expansion in the managed HR services market. Outsourced HR environments store payroll records, bank details, benefits data, and personal identifiers for large employee groups, making them attractive targets for ransomware and data theft. Buyers now evaluate vendors not only on service scope but also on access controls, audit readiness, incident response, and breach notification commitments. Changing privacy rules during 2025-2026 affected how outsourcing contracts allocate responsibility and manage risk. This adds cost and time to vendor selection, especially in regulated sectors and cross-border engagements. The managed HR services market is therefore favoring providers that can show mature security controls, shared-processor compliance, and repeatable governance rather than broad service menus alone.

Other drivers and restraints analyzed in the detailed report include:

- Rising Compliance Burden Across Labor Jurisdictions

- Expansion of AI-Enabled HR Workflow Automation

- Fragmented Country-Specific Labor Regulation Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Payroll and benefits administration accounted for 32.47% of the managed HR services market in 2025, making it the revenue anchor for the category. The segment stays essential because payroll cannot be delayed, and compliance errors can create direct financial and legal exposure for employers. This makes enterprises less willing to rebuild payroll operations internally, even when they review other service towers for savings or simplification. Recruitment process outsourcing maintained steady demand in BFSI and technology settings, where hiring volumes fluctuate and time-to-fill remains commercially important. HR operations outsourcing also remained important for buyers seeking standardized workflows for employee records, service requests, document handling, and routine administration.

HR technology managed services are projected to grow at a 12.86% CAGR from 2026 to 2031, making it the fastest-moving service category in the managed HR services market. Growth is being pulled by companies that prefer outcome-based management with Workday, SAP SuccessFactors, and Oracle HCM Cloud rather than large internal support teams. Advanced technology solutions revenue rose 17% in full-year 2025, supported by data, AI, and agentic solutions across HR and finance process management work. The launch of an AI-led workforce platform in May 2026 also showed how payroll, HR workflows, time tracking, and benefits administration are being combined into a single offering for smaller businesses. Learning and talent management services, along with advisory and compliance support, gained importance as buyers sought reskilling, policy assurance, and cleaner data flows across the broader managed HR services industry.

Cloud-enabled managed services held 63.29% of revenue in 2025, giving this model the largest share of the managed HR services market. The lead reflects a long migration toward cloud-native HR platforms that support automatic updates, elastic capacity, and faster reporting. Buyers also value the ability to unify data from payroll, benefits, time, and case management into a single operating model rather than across disconnected tools. Cloud delivery often improves rollout speed for new capabilities, especially in analytics, employee self-service, and workflow automation. Even so, not every enterprise can move all sensitive employee data into a fully public cloud setup.

Hybrid delivery is projected to expand at an 11.72% CAGR through 2031, making it the fastest-growing deployment path in the managed HR services market. Financial services and healthcare buyers are major drivers because they often need cloud flexibility without losing control over sensitive records or legacy systems. An Autonomous HCM framework presented in May 2026, with support for AI orchestration across cloud and on-premise layers, signaled that hybrid persistence is now a design assumption rather than a temporary stage. On-premise support still serves governments and state-linked organizations in parts of South America and the Middle East where sovereign storage rules and long contracts remain in place. Providers that can bridge all 3 models are better positioned to retain spend as the managed HR services market navigates uneven modernization cycles.

Complete Report Scope:

- By Service Type

- Recruitment Process Outsourcing (RPO)

- Payroll and Benefits Administration Services

- HR Operations Outsourcing (HRO)

- Learning and Talent Management Services

- HR Technology Managed Services (AMS/MSP)

- Advisory and Compliance Services

- By Deployment Model

- Cloud

- Hybrid

- On-Premise

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Information Technology and Telecom

- Retail and E-commerce

- Industrial Manufacturing

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America accounted for 38.92% of the managed HR services market share in 2025, making it the largest regional contributor. The region benefits from a deep buyer base, large multinational headquarters, and a rule environment that makes self-managed HR harder to sustain at scale. More than 1.1 million clients across 140-plus countries relied on a major HR and payroll platform in April 2026, which highlights the scale and maturity of the U.S. core in the managed HR services market. A major acquisition expanded the mid-market's reach and strengthened HCM capabilities for smaller organizations, while Mexico and Canada add demand for unified payroll and compliance workflows required by cross-border employment, manufacturing, and logistics.

Europe remains a large part of the managed HR services market because the region combines substantial demand with dense labor regulation. Germany, the United Kingdom, France, and the Netherlands lead adoption, but buyer needs differ by country because works councils, outsourcing norms, and local employment rules are not uniform. The United Kingdom has moved away from pure cost-driven contracts and toward technology-enabled, outcome-based models, creating space for both global providers and regional specialists. AI-powered recruiting analytics and multi-country payroll delivery across Northern and Central Europe show how regionally embedded firms defend their position against larger platforms.

Asia-Pacific is projected to expand at a 15.36% CAGR through 2031, which makes it the fastest-growing regional segment in the managed HR services market. India plays a dual role: it is both a major delivery hub for global providers and a growing buyer market as Global Capability Center activity scales. China, Southeast Asia, Japan, South Korea, Australia, and New Zealand also support regional growth through modernization programs, aging workforces, and mature outsourcing ecosystems. The Middle East and Africa are smaller today, but Saudi Arabia's workforce nationalization policies and the formalization of employment practices in South Africa and Nigeria are supporting demand for specialist compliance and payroll services. South America remains an emerging opportunity where frequent labor rule changes, currency pressure, and multi-jurisdiction payroll needs keep the managed HR services market relevant even when technology budgets are tight

- Automatic Data Processing, Inc.

- Accenture plc

- Alight, Inc.

- Aon plc

- Capita plc

- CGI Inc.

- Ceridian HCM Holding Inc.

- Genpact Limited

- IBM Corporation

- Infosys Limited

- International Business Machines Corporation

- Kronos Incorporated

- Mercer LLC

- NGA Human Resources Inc.

- NorthgateArinso N.V.

- Paychex, Inc.

- Randstad N.V.

- Tata Consultancy Services Limited

- Ultimate Kronos Group, Inc.

- Wipro Limited

- Zalaris ASA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Outsourcing of Core HR Operations

- 4.2.2 Need for Multi-Country Payroll Standardization

- 4.2.3 Rising Compliance Burden Across Labor Jurisdictions

- 4.2.4 Expansion of AI-Enabled HR Workflow Automation

- 4.2.5 Shift Toward Employee Experience-Led Service Models

- 4.2.6 Growth of Distributed and Remote Workforces

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Employee Information Security Risks

- 4.3.2 Fragmented Country-Specific Labor Regulation Complexity

- 4.3.3 High Switching Costs During Legacy HR Transformation

- 4.3.4 Under-Reported Risk, Dependence on Clean Master Data and HR Record Quality

- 4.4 Industry Value and Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Recruitment Process Outsourcing (RPO)

- 5.1.2 Payroll and Benefits Administration Services

- 5.1.3 HR Operations Outsourcing (HRO)

- 5.1.4 Learning and Talent Management Services

- 5.1.5 HR Technology Managed Services (AMS/MSP)

- 5.1.6 Advisory and Compliance Services

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 Hybrid

- 5.2.3 On-Premise

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Information Technology and Telecom

- 5.4.4 Retail and E-commerce

- 5.4.5 Industrial Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.5 Automatic Data Processing, Inc.

- 6.6 Accenture plc

- 6.7 Alight, Inc.

- 6.8 Aon plc

- 6.9 Capita plc

- 6.10 CGI Inc.

- 6.11 Ceridian HCM Holding Inc.

- 6.12 Genpact Limited

- 6.13 IBM Corporation

- 6.14 Infosys Limited

- 6.15 International Business Machines Corporation

- 6.16 Kronos Incorporated

- 6.17 Mercer LLC

- 6.18 NGA Human Resources Inc.

- 6.19 NorthgateArinso N.V.

- 6.20 Paychex, Inc.

- 6.21 Randstad N.V.

- 6.22 Tata Consultancy Services Limited

- 6.23 Ultimate Kronos Group, Inc.

- 6.24 Wipro Limited

- 6.25 Zalaris ASA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment