|

시장보고서

상품코드

2066447

그래핀 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Graphene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

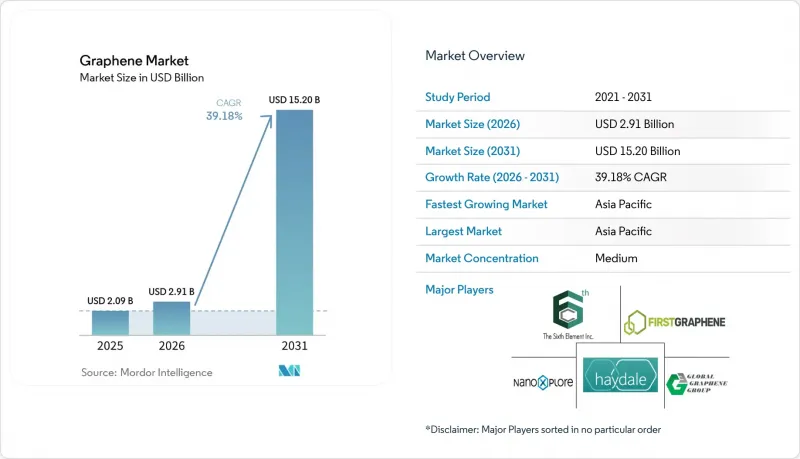

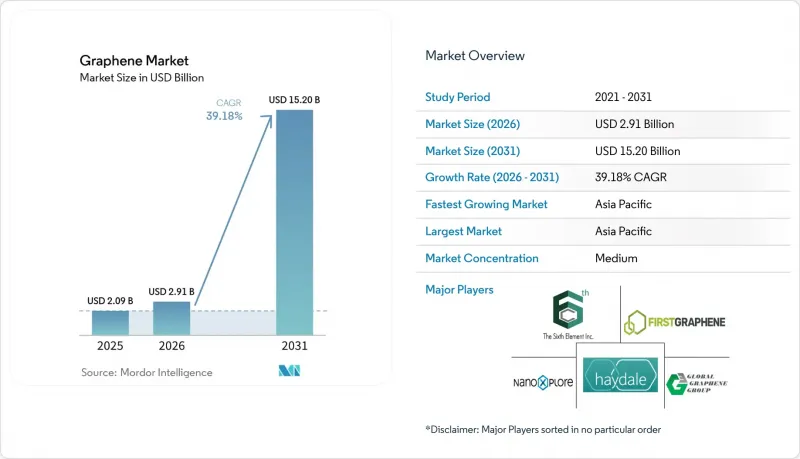

Mordor Intelligence에 의하면, 그래핀 시장 규모는 2025년에 20억 9,000만 달러로 평가되었습니다. 2026년 29억 1,000만 달러에서 2031년까지 152억 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 39.18%를 나타낼 전망입니다.

본 보고서는 제품 유형(그래핀 시트 및 필름, 나노플레이트릿, 기타), 용도(복합재료, 생의학·헬스케어, 기타), 최종 사용자 산업(전자·통신, 생의학·헬스케어, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 그래핀 시장 동향 및 인사이트

항공우주 산업에서의 그래핀 활용 확대

항공기 OEM 업체들은 탄소섬유 프리프레그에 그래핀 나노플레이틀릿을 내장하여 구조 중량을 15-20% 줄이고 있습니다. 이는 기존 와이드바디 항공기에 비해 연료 소비량을 25% 개선하는 데 필요한 기준치입니다. 보잉사의 2025년판 공급업체 문서에서는 777X의 2차 구조에 그래핀 복합재 사용을 의무화하고 있으며, 그 이유로 알루미늄 허니콤보다 40% 우수한 낙뢰 방전 성능을 꼽고 있습니다. 에어버스는 A350의 제어 패널에 산화 그래핀 표면 코팅을 시험적으로 도입하여, 습도가 높은 해안 기후에서 발생하는 갈바닉 부식을 억제하고 있습니다. 이는 장거리 운항 사업자들에게 오랫동안 유지보수상의 과제로 남아 있습니다. 방위 관련 계약도 이러한 추세를 뒷받침하고 있습니다. 미국 공군 연구소는 2025년, 6세대 전투기 프로토타입의 X-밴드 대역에서 레이더 반사 단면적을 줄여주는 레이더 흡수성 그래핀 적층재 개발에 1,800만 달러의 보조금을 지원했습니다. 그러나 AS9100 프로토콜에 따른 인증 절차에는 평균 18-24개월이 소요되므로, 중소 공급업체의 경우 수익 인식이 지연되고 고가 정책이 유지될 수밖에 없습니다.

그래핀을 활용한 에너지 저장 용도의 확대

전력 회사는 2018년부터 2022년 사이에 설치된 리튬 이온 배터리 어레이를 그래핀 강화형 음극으로 개조하고 있습니다. 이를 통해 충전 수용 능력이 35% 향상되어, 규제 완화된 전력 풀에서 수익성이 높은 주파수 조정 서비스를 제공할 수 있게 됩니다. 2025년 3월 NanoXplore가 체결한 4,200만 달러 규모공급 계약은 미국 5개 주에 걸쳐 500 MWh 규모의 이러한 업그레이드를 대상으로 하며, 이는 현재 시점에서 최대 규모의 상용 도입 사례가 됩니다. 스마트폰 제조업체들도 이와 동시에 이익을 추구하고 있습니다. 그래핀 슈퍼커패시터와 100와트 충전기를 결합하면, 실온에서 발생할 수 있는 열 폭주 위험을 방지할 수 있습니다. 삼성은 이 기능을 2026년 플래그십 모델에 상용화할 예정입니다. 미국 에너지부(DOE)의 Battery500 컨소시엄이 실시한 장기 조사에 따르면, 현재 기준치의 2배에 해당하는 500 Wh/kg의 셀을 목표로 하고 있으며, 그래핀은 리튬 이후의 화학 계열로 넘어가는 중요한 가교 역할을 하는 것으로 평가받고 있습니다.

높은 제조 비용

화학기상증착법(CVD)을 통해 제조된 그래핀 시트는 1kg당 200-500달러로 가격이 비싸지만, 이에 비해 탄소나노튜브는 10-20달러, 카본블랙은 2-5달러에 불과하기 때문에 많은 대량 용도에서 경제적 장벽이 되고 있습니다. 나노 플레이트렛의 주력 공정인 액상 박리법에서는 용매 회수만으로도 40-60kWh/kg을 소비하며, 산업용 요금을 적용할 경우 80-120달러의 에너지 비용이 추가로 발생합니다. 퍼스트 그래핀의 2025년 실적에 따르면, 평균 매출총이익률은 38%에 그쳐 특수 화학제품의 55-65%보다 낮은 수준이며, 이는 생산 능력에 대한 재투자를 제약하고 있습니다. 규모 확대는 부분적인 개선을 가져오지만, 처리 능력을 두 배로 늘려도 1kg당 비용 절감률은 고작 12-15%에 그쳐, 리튬 이온 배터리나 태양광 발전이 보여준 학습 곡선의 선례를 훨씬 밑돌고 있습니다. 수요 전망이 불투명한 상황에서 설비 공급업체들은 연간 생산 능력 500 tpa를 초과하는 반응 장치에 대해 18-24개월의 리드타임을 유지하고 있어, 공급 측의 유연성 개선이 더딘 실정입니다.

부문별 분석

그래핀 나노 플레이트릿(GNP)은 2025년 매출의 56.14%를 차지했습니다. 이는 폴리머 컴파운더에게 친숙한 이축 스크류 압출기나 3롤 밀과의 원활한 통합을 반영한 것입니다. 이러한 경쟁 우위는 제품 차원의 그래핀 시장 규모를 뒷받침하는 기반이 되고 있으며, 중국의 단가가 80달러/kg 아래로 떨어짐에 따라 2031년까지의 예상 침투율은 연평균 성장률(CAGR) 44.63%로 확대될 것으로 전망됩니다. 1-3 wt% 농도로 분산된 나노 플레이트렛은 인장 탄성률을 최대 300% 향상시켜, 자동차 제조업체가 2027년 충돌 안전 기준을 충족하면서 언더바디 실드의 질량을 12-15% 줄일 수 있게 됩니다. Sixth Element(창저우)는 2025년에 나노 플레이트렛 매출로 8,500만 달러를 기록하며 전년 대비 62% 증가를 달성했습니다. 이는 그래핀 시장에서 중국의 비용 우위를 여실히 보여주고 있습니다. 기능화 유도체는 용도를 확대합니다. Perpetuus사가 출시한 카르복실화 변형 제품은 에폭시 수지의 강도를 35% 향상시키고, 항공우주용 허니콤 코어의 층간 박리를 줄여줍니다.

필름 및 시트는 여전히 1제곱미터당 800-1,200달러 수준의 가격대를 형성하는 프리미엄 틈새 시장이지만, 그 광학 투명도(98%)와 전도도(10^6 S/m 이상) 덕분에 폴더블 디스플레이 OEM 제조업체들의 관심을 끌고 있습니다. LG디스플레이는 2027년까지 연간 10만 m² 규모의 생산 체제를 구축할 전망이며, 이는 7인치 화면 5,000만 개에 해당합니다. 이로써 투명 전도체는 그래핀 시장에서 10자리 규모의 하위 부문으로 자리매김하게 될 것입니다. 산화물 플레이크는 시장 점유율은 작지만, 항체와의 공유 결합이 펨토몰 수준의 바이오센서 감도를 뒷받침하는 등, 생의학 분야의 혁신을 위한 기반이 되고 있습니다. 양자점과 에어로겔은 여전히 연구 개발 단계에 있지만, 보조금의 중점은 광촉매를 이용한 수소 생산과 기가헤르츠파 흡수에 맞추어져 있어, 향후 가치의 집중 대상이 변화할 가능성에 대비하고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 45.23%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 45.69%를 나타낼 것으로 전망되어, 그래핀 시장에서 가장 규모가 큰 지역 거점으로서의 입지를 계속 유지할 것으로 확실시되고 있습니다. 중국은 헤이룽장성의 천연 흑연 채굴부터 창저우의 연간 3,000톤 규모 나노플레이트릿 분산액 생산에 이르는 ‘크래들-투-게이트(cradle-to-gate)’ 통합 생산 체계를 통해 공급 단가를 kg당 60-80달러로 낮췄으며, 이는 유럽 평균 가격의 절반 수준에 해당해 폴리머 컴파운딩 및 배터리 첨가제 분야의 상품화를 가속화하고 있습니다. 대만의 TSMC는 2nm 테스트 웨이퍼에서 신호 지연 시간을 18% 단축하는 그래핀 상호 연결 기술을 검증함으로써, 해당 지역에 대한 투자를 뒷받침하는 반도체 수요 증가를 입증했습니다. 인도는 2025년, 정수용 막에 초점을 맞춘 ‘국가 그래핀 미션’에 500카롤 루피(6,000만 달러)를 배정함으로써, 기후 변화 적응형 인프라와의 정책적 일관성을 보여주었습니다.

북미의 매출은 미국 에너지부(DOE)가 자금을 지원하는 음극재 생산 라인과 항공우주용 복합재료 수요에 힘입어 성장하고 있습니다. ‘초당파 인프라법’에 따라 그래핀을 활용한 리튬 이온 배터리 제조에 1억 4,000만 달러가 배정되어, 국내 배터리 제조업체들에게 안정적인 공급 경로가 확보되었습니다. NanoXplore사가 2025년 3분기에 몬트리올 공장의 생산 능력을 연간 4,000톤으로 확대함에 따라, 전기자동차 배터리 공급권 내 500마일 이내의 물류 비용이 절감될 것입니다. 한편, 캐나다의 전략적 혁신 기금은 Grafoid사의 의료용 산화 그래핀 시범 사업에 3,000만 캐나다 달러(2,200만 달러)를 투자함으로써, 오타와 정부가 수익성이 높은 의료 틈새 시장에 주력하겠다는 의지를 보여주고 있습니다. 멕시코는 프린트 전자 분야의 거점으로 입지를 다지고 있으며, 국경을 넘어 자동차 업계 고객들에게 서비스를 제공하는 Vorbeck사의 200만 m² 규모의 잉크 공장이 이곳에 자리 잡고 있습니다.

2025년 유럽의 매출은 그래핀 플래그십 프로그램이 제공하는 10억 유로의 자금 지원에 힘입어, 항공우주용 복합재료 및 해수 담수화용 코팅 분야의 호조에 힘입어 견조한 추세를 보였습니다. 플래그십 기금으로부터 800만 유로의 지원을 받은 Versarien사의 영국 시범 생산 라인은 갈바닉 부식을 억제하기 위해 에어버스 A350의 제어면용 수지 개발을 목표로 하고 있습니다. 독일의 프라운호퍼 연구소는 배터리식 전기자동차에서 인버터 접합부의 온도를 20% 낮추고 구동계의 내구성을 향상시키는 것을 목표로 하는 그래핀 열 인터페이스 재료를 공동 개발하고 있습니다. REACH 사전 등록으로 인해 중견 기업들 사이에서 구조조정이 진행되면서 15건의 철수 및 통합이 촉진되었고, 지역 그래핀 시장 규모는 더욱 집중된 상태로 나아가고 있습니다. 남미와 중동은 뒤처져 있지만, 용도별 관심은 높아지고 있습니다. 사우디아라비아의 해수 담수화 플랜트에서는 그래핀 코팅을 적용해 부식을 70% 줄였으며, 브라질 미나스제라이스주의 연구소에서는 광산 지역의 붕괴 위험을 완화하기 위해 그래핀으로 보강된 광미 댐의 시범 운영을 진행하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the graphene market size was valued at USD 2.09 billion in 2025 and is estimated to grow from USD 2.91 billion in 2026 to reach USD 15.20 billion by 2031, at a CAGR of 39.18% during the forecast period (2026-2031).

This report is Segmented by Product Type (Graphene Sheets and Films, Nanoplatelets, and Others), Application (Composites, Biomedical and Healthcare, and Others), End-User Industry (Electronics and Telecommunications, Biomedical and Healthcare, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Graphene Market Trends and Insights

Increasing Usage of Graphene in the Aerospace Industry

Aircraft OEMs embed graphene nanoplatelets into carbon-fiber prepregs to secure 15-20% structural weight reductions, a threshold needed to reach 25% fuel-burn improvements over legacy wide-body fleets. Boeing's 2025 supplier documents mandate graphene composites in the 777X secondary structures, citing lightning-strike dissipation that exceeds aluminum honeycomb by 40%. Airbus is piloting graphene oxide surface coatings on A350 control panels to curb galvanic corrosion in humid coastal climates, a persistent maintenance driver for long-haul operators. Defense contracts reinforce the trend: the US Air Force Research Laboratory awarded USD 18 million in 2025 to develop radar-absorbing graphene laminates that lower X-band signatures on sixth-generation fighter prototypes. Qualification cycles, however, average 18-24 months under AS9100 protocols, delaying revenue recognition for smaller suppliers and sustaining premium pricing.

Expansion of Energy-Storage Applications Utilizing Graphene

Utilities are retrofitting lithium-ion arrays installed between 2018 and 2022 with graphene-enhanced anodes that raise charge acceptance by 35%, enabling lucrative frequency-regulation services in deregulated power pools. A USD 42 million supply deal inked by NanoXplore in March 2025 covers 500 MWh of such upgrades across five US states, the largest commercial deployment to date. Smartphone vendors pursue parallel gains: graphene supercapacitors paired with 100-watt chargers eliminate thermal-runaway risks at room temperature, a feature Samsung plans to commercialize in 2026 flagships. Longer-term research from the DOE's Battery500 Consortium targets 500 Wh/kg cells, double present benchmarks, positioning graphene as a vital bridge to post-lithium chemistries.

High Production Cost

Chemical-vapor-deposition sheets command USD 200-500 /kg, compared with USD 10-20 for carbon nanotubes and USD 2-5 for carbon black, keeping many high-volume uses financially out of reach. Liquid-phase exfoliation, the workhorse process for nanoplatelets, consumes 40-60 kWh/kg in solvent recovery alone, adding USD 80-120 in energy overheads at industrial tariffs. First Graphene's 2025 results revealed average 38% gross margins versus 55-65% for specialty chemicals, constraining reinvestment in capacity. Scaling offers partial relief-doubling throughput shaves merely 12-15% off cost per kilogram-far below learning-curve precedents set by lithium-ion or photovoltaics. Equipment suppliers, facing uncertain demand visibility, maintain 18-24 month lead times on reactors exceeding 500 tpa, delaying supply-side elasticity.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand in Electronics and Semiconductors

- Commercialisation of Graphene EMI-Shielding Foams for 5G Infrastructure

- Availability of Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Graphene Nanoplatelets (GNP) captured 56.14% of 2025 revenue, reflecting their seamless integration into twin-screw extruders and three-roll mills long familiar to polymer compounders. This dominance anchors the graphene market size at the product level, with forecast penetration expanding at a 44.63% CAGR to 2031 as unit pricing slides below USD 80/kg in China. Nanoplatelets dispersed at 1-3 wt% lift tensile modulus by up to 300%, enabling automakers to shave 12-15% off underbody shield mass while meeting 2027 crash standards. Sixth Element (Changzhou) booked USD 85 million in nanoplatelet sales in 2025, up 62% year-over-year, underscoring China's cost leverage in the graphene market. Functionalized derivatives extend utility: carboxylated variants launched by Perpetuus strengthen epoxies by 35%, reducing delamination in aerospace honeycomb cores.

Films and sheets remain a premium niche, priced at USD 800-1,200/m2, yet their optical clarity (98%) and conductivity (more than 10^6 S/m) attract foldable display OEMs. LG Display expects to convert 100,000 m2 per year by 2027, adequate for 50 million 7-inch screens, positioning transparent conductors as a 10-figure sub-segment of the graphene market. Oxide flakes, though holding a smaller slice, anchor biomedical innovations where covalent bonding with antibodies underpins femtomolar biosensor sensitivity. Quantum dots and aerogels linger in R&D, but grant funding focuses on photocatalytic hydrogen production and gigahertz-wave absorption, hedging against future value-pool shifts.

Geography Analysis

Asia-Pacific anchored 45.23% of 2025 revenue and is on track for a 45.69% CAGR through 2031, ensuring it remains the largest regional node of the graphene market. China's cradle-to-gate integration, from natural-graphite mining in Heilongjiang to 3,000 tpa nanoplatelet dispersion in Changzhou, cuts delivered cost to USD 60-80/kg, half European averages, catalyzing commoditization in polymer compounding and battery additives. Taiwan's TSMC validated graphene interconnects that lower signal delay by 18% in 2 nm test wafers, demonstrating semiconductor pull that anchors regional investment. India earmarked INR 500 crore (USD 60 million) in 2025 for a National Graphene Mission focused on water purification membranes, illustrating policy alignment with climate-adaptation infrastructure.

North America's revenue is buoyed by DOE-funded anode lines and aerospace composite demand. The Bipartisan Infrastructure Law assigns USD 140 million to graphene-enhanced lithium-ion manufacturing, creating a protected corridor for domestic cell makers. NanoXplore's Montreal expansion to 4,000 tpa in Q3 2025 lowers logistics costs within a 500-mile EV-battery supply radius, while Canada's Strategic Innovation Fund injected CAD 30 million (USD 22 million) into Grafoid's biomedical-graphene oxide pilot, signaling Ottawa's tilt toward high-margin healthcare niches. Mexico gains traction as a printed-electronics hub, hosting Vorbeck's 2 million m2 ink plant that services cross-border automotive customers.

Europe's revenue in 2025 was retained with momentum in aerospace composites and desalination coatings supported by the Graphene Flagship's EUR 1 billion funding envelope. Versarien's UK pilot lines, backed by EUR 8 million of Flagship funds, target Airbus A350 control-surface resins to tame galvanic corrosion. Germany's Fraunhofer Institute co-develops graphene thermal interfaces that promise 20% inverter-junction-temperature cuts in battery electric vehicles, chasing extended drivetrain durability. REACH pre-registration triggered a mid-tier shakeout, prompting 15 exits or consolidations and nudging the regional graphene market size toward higher concentration. South America and the Middle East trail yet signal application-specific interest: Saudi Arabia's desalination plants logged 70% corrosion reductions using graphene coatings, and Brazil's Minas Gerais institute pilots graphene-reinforced tailings dams to mitigate collapse risk in mining regions.

- ACS Material

- Cabot Corporation

- Cheap Tubes

- Directa Plus S.p.A.

- First Graphene Ltd

- G6 Materials Corp.

- Global Graphene Group

- Grafoid Inc

- Graphene Manufacturing Group Ltd

- Graphenea

- Haydale Graphene Industries plc

- NanoXplore Inc.

- Perpetuus Advanced Materials

- Talga Group

- The Sixth Element (Changzhou) Materials Technology Co.,Ltd

- Thomas Swan & Co. Ltd

- Universal Matter Inc

- Versarien plc

- Vorbeck Materials Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing usage of graphene in the aerospace industry

- 4.2.2 Adoption of graphene anti-corrosion coatings in desalination infrastructure

- 4.2.3 Expansion of energy-storage applicationsutilizing graphene

- 4.2.4 Growing demand in electronics and semiconductors

- 4.2.5 Commercialisation of graphene EMI-shielding foams for 5G infrastructure

- 4.3 Market Restraints

- 4.3.1 High production cost

- 4.3.2 Availability of substitutes

- 4.3.3 Nanotoxicology & regulatory uncertainty

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Graphene Sheets and Films

- 5.1.2 Graphene Nanoplatelets (GNP)

- 5.1.3 Graphene Oxide (GO)

- 5.1.4 Nanoplatelets

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Composites

- 5.2.2 Energy Storage and Harvesting

- 5.2.3 Printed and Flexible Electronics

- 5.2.4 Biomedical and Healthcare

- 5.2.5 Coatings and Paints

- 5.2.6 Others

- 5.3 By End-user Industry

- 5.3.1 Electronics and Telecommunications

- 5.3.2 Aerospace and Defense

- 5.3.3 Energy and Power

- 5.3.4 Biomedical and Healthcare

- 5.3.5 Others(automotive, Chemical and Coatings)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 South Korea

- 5.4.1.4 India

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 ACS Material

- 6.4.2 Cabot Corporation

- 6.4.3 Cheap Tubes

- 6.4.4 Directa Plus S.p.A.

- 6.4.5 First Graphene Ltd

- 6.4.6 G6 Materials Corp.

- 6.4.7 Global Graphene Group

- 6.4.8 Grafoid Inc

- 6.4.9 Graphene Manufacturing Group Ltd

- 6.4.10 Graphenea

- 6.4.11 Haydale Graphene Industries plc

- 6.4.12 NanoXplore Inc.

- 6.4.13 Perpetuus Advanced Materials

- 6.4.14 Talga Group

- 6.4.15 The Sixth Element (Changzhou) Materials Technology Co.,Ltd

- 6.4.16 Thomas Swan & Co. Ltd

- 6.4.17 Universal Matter Inc

- 6.4.18 Versarien plc

- 6.4.19 Vorbeck Materials Corp.

7 Market Opportunities & Future Outlook

- 7.1 Development of graphene nanodevices for DNA sequencing

- 7.2 Adoption of graphene into photodetectors

- 7.3 White-space & Unmet-need Assessment