|

시장보고서

상품코드

2066602

바나듐 레독스 플로우 배터리(VRFB) 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Vanadium Redox Flow Battery (VRFB) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

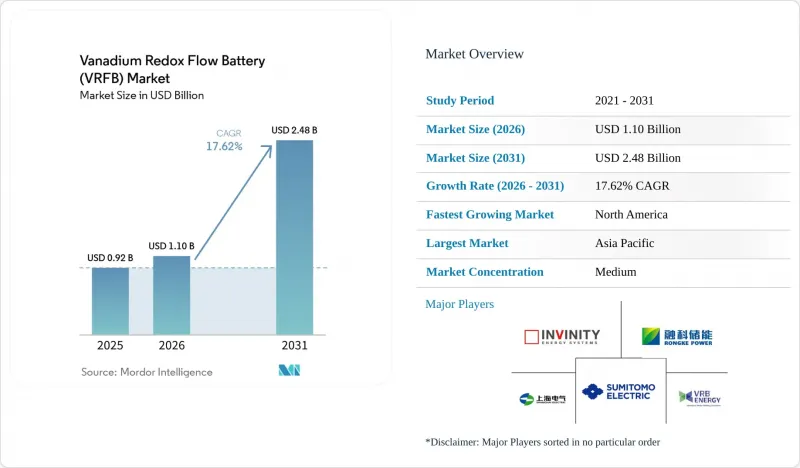

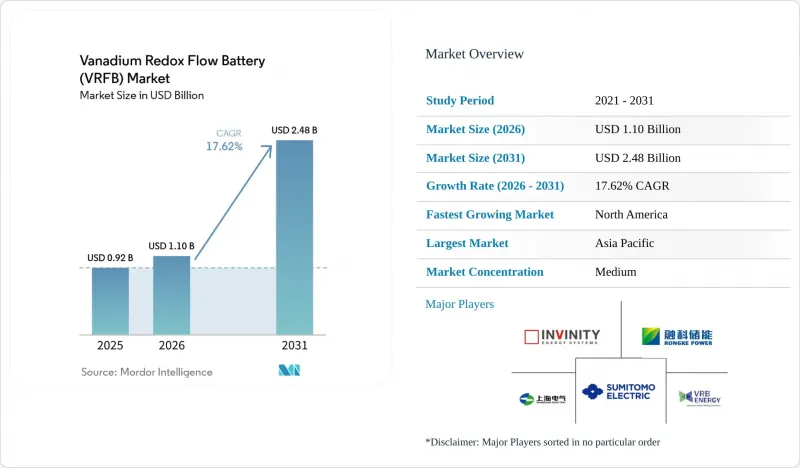

Mordor Intelligence에 의하면, 바나듐 레독스 플로우 배터리 시장 규모는 2025년 9억 2,000만 달러로 평가되었고, 2026년 11억 달러로 추정되고, 2031년까지 24억 8,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 17.62%를 나타낼 전망입니다.

본 보고서는 제품 유형별(컨테이너형 시스템 및 캐비닛/랙형 시스템), 구성 요소별(전해액, 셀 스택, 멤브레인), 정격 출력별(100 kW 미만, 100-500 kW, 100 kW 이상), 시스템 규모별(대규모, 중규모, 기타), 용도별(재생에너지 통합 등), 최종 사용자별(전력 회사 등), 지역별(북미, 유럽, 아시아태평양 등)로 분류되어 있습니다.

세계의 바나듐 레독스 플로우 배터리(VRFB) 시장 동향 및 분석

중국과 미국에서 4시간 이상의 그리드 저장 프로젝트가 급속히 확대되고 있습니다.

중국의 State Grid는 2024년부터 2025년에 걸쳐 하미 회랑을 따라 위치한 풍력 발전 출력을 안정화하기 위해 200 MW/1 GWh 규모의 짐사르 어레이를 핵심으로 하여, 375 MW/1.5GWh 규모의 흐름형 에너지 저장 설비를 전력망에 연결했습니다. 미국에서는 2025년에 신설될 에너지 저장 장치 중 지속 시간이 4시간을 초과하는 것은 고작 3%에 불과했으며, 이러한 격차를 해소하기 위해 캘리포니아주에서는 1GW 규모의 장기 지속형 에너지 저장 장치 설치 의무화를, 연방 정부에서는 독립형 에너지 저장 설비에 대해 30%의 세액 공제를 도입하고 있습니다. 스미토모 일렉트릭이 샌디에이고 가스 앤 일렉트릭(San Diego Gas & Electric)과 공동으로 진행한 4 MW/16 MWh 규모의 프로젝트에서는 7년 동안 왕복 효율 68% 이상을 기록했으며, 매일 충전 및 방전 주기를 반복하는 조건에서도 연간 용량 저하율이 0.5% 미만임을 입증했습니다. 시스템 운영 사업자는 15년간의 보증을 요구하고 있기 때문에 이러한 긴 수명은 7년이 지난 후 고액의 성능 보강이 필요한 리튬계 시스템에 비해 결정적인 우위를 제공합니다. 새로운 세액 공제로 인해 프로젝트에 필요한 내부수익률(IRR)이 12%에서 약 8%로 낮아지면서, 재무적 수익률이 유틸리티급 태양광 발전과 동등한 수준에 이르렀고, 텍사스주와 애리조나주에서 프로젝트 수주 건수가 가속화되고 있습니다.

유럽에서 바나듐 전해액 임대 모델을 통한 설비 투자(CapEx) 절감

Bushveld Energy의 남아프리카공화국 시범 사업에서는 전해액의 소유권을 시스템 하드웨어와 분리함으로써 초기 투자를 28% 절감하고, 기존 구조에서는 6.5%였던 차입 금리를 4.2%로 낮출 수 있음이 입증되었습니다. Invinity는 7 MW/30 MWh 규모의 옥스퍼드 프로젝트에서 이 방식을 재현하고, Glencore가 지원하는 펀드를 활용해 전해액 비용을 충당함으로써, 기존 플로우형 프로젝트에서는 충족하지 못했던 유럽투자은행(EIB)의 커버리지 비율을 충족시켰습니다. 판지후아 지방공사도 2024년에 50 MW 규모의 프로젝트에서 이와 유사한 접근 방식을 채택하여, 성의 부채 한도를 초과하지 않고 이를 실현했습니다. 사용 후 전해액의 2차 시장이 부상하고 있습니다. 이는 바나듐이 20년이 지난 후에도 95%의 잔존 가치를 유지하기 때문이며, ESG를 중시하는 펀드에 있어 매력적인 순환형 경제의 인센티브를 창출하고 있습니다.

바나듐 가격 변동은 철강 수요와 연동됩니다.

중국의 철근 생산량이 8% 감소함에 따라, 바나듐 오산화물 가격은 2022년 9달러/파운드에서 2024년에는 4-5달러/파운드로 하락하여, 2026년까지의 선물 노출분의 60%를 헤지하고 있던 Largo Clean Energy와 같은 수직 통합형 공급업체에 압박을 가했습니다. 2024년 유럽의 페로바나듐 가격은 1kg당 30유로 전후로 거래를 마감하며 2022년 최고점 대비 40% 하락했으나, 선물 시장은 여전히 콘탱고 상태를 유지하고 있어, 트레이더들이 중국의 경기 부양책으로 건설 수요가 회복될 경우 공급이 부족해질 것으로 예상하고 있음을 시사하고 있습니다. 2023년 중국 정부가 부과한 수출 할당량으로 인해 6주간의 납기 지연이 발생했고, Invinity는 18개월 분량의 전해액 재고를 예정보다 앞당겨 구매할 수밖에 없게 되었습니다. 리스 계약 구조는 가격 변동의 일부를 상쇄하지만, 바나듐 현물 가격이 계약상 가격대(컬러)를 초과할 경우, 리스 제공업체는 결국 비용을 전가하게 되므로 최종 사용자는 부분적으로 위험에 노출되게 됩니다.

부문별 분석

컨테이너형 유닛은 2025년 매출의 67.0%를 차지했으며, 전력 변환 및 소화 기능을 통합한 40피트 턴키 모듈에 대한 전력 회사 수요가 높음을 입증하고 있습니다. 컨테이너형 시스템의 바나듐 레독스 플로우 배터리 시장 규모는 2025년에 7억 4,000만 달러에 달할 것으로 예상되며, 중국과 미국에서 진행 중인 수 기가와트 규모의 조달 프로그램에 힘입어 앞으로도 계속 확대될 전망입니다. 짐사르의 200 MW/1 GWh 규모 건설 프로젝트에서는 250개의 동일한 컨테이너가 사용되어 단계적인 시운전이 가능해졌습니다. 이를 통해 후속 제품군이 공장 입고 검사를 완료하는 동안에도 조기에 수익을 인식할 수 있었습니다. 캐비닛형 및 랙형은 공간이 제한된 설치 장소에 적합하며, 2031년까지 연평균 성장률(CAGR) 21.1%로 성장할 것으로 전망됩니다. 이는 외부 펌프가 필요 없고 유지보수 비용을 35% 절감하는 Vanevo의 중력식 10 kW/40 kWh 설계를 기반으로 합니다. 이러한 변화는 통신 및 데이터센터 분야의 그리드 엣지 동향을 반영한 것이지만, 전력 전자 분야의 규모의 경제로 인해 메가 프로젝트에서는 컨테이너형 제품이 계속해서 주류를 이룰 것으로 보입니다.

컨테이너의 이동성은 EPC의 효율화를 실현하며, 모듈은 공장에서 시험을 마친 후 납품되므로 현장 작업은 최소한으로 끝낼 수 있습니다. 또한, 2단 적재가 가능하기 때문에 토지 이용 면적은 1MWh당 15m²로 제한됩니다. 반면, 이 캐비닛은 19인치 랙에 들어맞으며 표준 개폐 장치 뒤쪽에 설치할 수 있어 상업시설이나 산업 시설의 개보수에 가장 적합합니다. Redflow의 핫스왑 지원 200kWh 포드는 모듈화를 통해 가동 중단 시간을 2시간으로 단축할 수 있음을 보여주고 있으며, 데이터센터에서는 1시간의 정전을 방지할 때마다 5만 달러의 가치가 있는 것으로 평가되고 있습니다. 예측 기간 동안 컨테이너 운송을 통한 출하량은 여전히 전체 용량의 60% 이상을 차지할 것으로 보이지만, 캐비닛 판매 대수가 크게 증가함에 따라 2031년까지 모듈식 솔루션의 납품 대수는 전체의 3분의 1 가까이까지 확대될 전망입니다. 따라서 바나듐 레독스 플로우 배터리 시장은 전력 회사를 대상으로 한 대용량 저장 및 분산형 고객을 위한 유연한 폼 팩터라는 두 가지 방향으로 전개될 것입니다.

2025년에는 전해액이 부품 매출액의 43.3%를 차지했습니다. 이는 바나듐이 비용의 35-40%를 차지한다는 점과, 재사용을 통해 확보된 가치를 반영한 것입니다. 고순도 VPURE+ 배합은 가격이 다소 비싸지만, 재조정 주기를 12개월 연장하여 1MWh당 연간 8,000달러의 O&M 비용을 절감합니다. 멤브레인 시장은 2031년까지 연평균 성장률(CAGR) 18.4%를 나타낼 것으로 전망됩니다. 이는 바나듐 가격이 반등하더라도 저비용의 PBI 및 PFSA 옵션이 매출총이익률의 여지를 확대하기 때문입니다. 스택 및 멤브레인의 비용이 더욱 빠르게 하락함에 따라, 바나듐 레독스 플로우 배터리 시장에서 전해질의 점유율은 2031년까지 38%로 떨어질 것으로 예상되지만, 리스 계약을 통해 자본 지출 항목이 예측 가능한 서비스 요금으로 전환됨에 따라 전해질의 전략적 중요성은 더욱 높아질 것입니다.

스택 비용의 추이도 마찬가지로 급격합니다. 다롄 공장에 자동화된 카본 펠트 및 프레스 성형 양극판을 도입함에 따라, 2025년까지 단가는 1kW당 150달러가 되어 2022년 대비 45% 하락할 전망입니다. 이에 따라 스택은 이익률 압박과 관련해 다음으로 주목해야 할 대상이 됩니다. 퍼시픽 노스웨스트 국립연구소가 개발한 고밀도 전해액 덕분에 탱크 용적을 40% 줄일 수 있어, 옥상 설치형 및 컨테이너형 시스템의 플랜트 부대 설비 비용을 절감할 수 있습니다. 이 모든 요소를 종합해 보면, 멤브레인 및 스택의 비용 절감은 시스템 전체의 설비 투자(CAPEX)를 줄여주며, 원자재 가격 변동과 프로젝트의 현금 흐름을 분리하는 서비스형 비즈니스 모델의 도입을 촉진합니다.

지역별 분석

중국이 30GW의 에너지 저장 목표를 추진하며, 현재 전 세계 VRFB 용량의 40%를 차지하는 우시(Wushi) 및 짐사르(Jimsar) 두 시설을 가동한 결과, 2025년 매출의 48.7%를 아시아태평양이 차지했습니다. 일본은 8 MWh 규모의 구마모토 사이트에 대해 사상 첫 VRFB 보조금을 승인했습니다. 이는 태양광 발전의 보급률이 국내 발전량의 12%를 넘어선 데 따라, 정책이 일관성을 보이고 있음을 반영한 것입니다. 인도의 ‘국가 에너지 저장 프레임워크’ 초안에서는 6시간 이상의 시스템에 요금 프리미엄이 부여되며, 2030년까지 10 GW 규모의 계획 중 15-20%를 VRFB가 차지할 것으로 전망됩니다.

북미는 연방 정부의 30% 단독 세액 공제와 캘리포니아주의 1GW 규모 장주기 에너지 저장(LDES) 시스템 입찰에 힘입어, 2031년까지 연평균 성장률(CAGR) 22.5%로 성장을 주도할 전망입니다. San Diego Gas & Electric이 장기간 운영해 온 4 MW/16 MWh 규모의 발전 설비는 연간 성능 저하율이 0.5% 미만인 것으로 확인되어, 미국 금융 기관에 대해 신뢰할 수 있는 성능을 입증하고 있습니다. 캐나다의 ‘청정 전력 규정’에 따라 전력 사업자들은 2035년까지 탄소 중립을 달성해야 하므로 도입이 가속화되고 있으며, 앨버타주와 서스캐처원주에서는 500 MW 규모의 장주기 에너지 저장(LDES) 시스템 조달이 진행되고 있습니다. 멕시코 소노라주의 태양광 회랑에서는 CFE의 2024년 입찰에서 고온 운전이 가능한 유동형 화학 시스템을 우선적으로 고려하여, 6시간 동안 전력을 저장할 수 있는 300 MW 규모의 시스템이 요구되고 있습니다.

2025년, 유럽 시장 점유율은 약 18%를 차지했습니다. 영국 옥스퍼드에서는 전해액 리스 방식을 도입하여 부채 상환 배율을 1.5배로 높이고, 설비 투자를 28% 절감했습니다. 독일의 ‘EEG 2023’에서는 4시간 이상의 전력 저장 시 kWh당 0.10유로의 보너스가 제공되며, 2024년부터 2025년에 걸쳐 80 MW 규모의 VRFB(납산 흐름 전지)가 채택되었습니다. 스페인에 도입된 1.1 MW/8.8 MWh 규모의 시스템을 통해 카스티야-이-레온 주의 태양광 발전소에서 출력 제한이 9% 감소했습니다. 북유럽의 전력 회사들은 겨울철 피크 수요가 여름철 태양광 발전량을 60% 상회한다는 점을 감안하여 계절적 이점을 검토하고 있으며, 200 MW 규모의 플로우형 에너지 저장 시스템이 주목을 받고 있습니다.

중동 및 아프리카는 매출의 8%를 차지했습니다. 두바이는 주변 온도가 45℃ 이하인 환경에서의 안전성을 이유로, 모하메드 빈 라시드 알 막툼 공원을 대상으로 300 MW/2.4GWh 규모의 8시간 에너지 저장 시스템 입찰을 공고했습니다. 사우디아라비아의 NEOM 기가 프로젝트에서는 간헐적인 태양광 발전의 불균형을 상쇄하기 위해 최소 1GW 규모의 VRFB가 필요하며, 남아프리카공화국의 Eskom은 6MW 규모의 시범 사업이 성공함에 따라 현재 피크 대응 용도를 위한 흐름 전지의 화학 조성을 평가했습니다. 남미에서는 아직 도입 초기 단계이지만, 브라질의 2024년 입찰 지침에서는 설계 수명 20년 이상이 권장되고 있으며, 이 기준은 VRFB의 강점을 살릴 수 있는 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the vanadium redox flow battery market size is projected to expand from USD 0.92 billion in 2025 and USD 1.10 billion in 2026 to USD 2.48 billion by 2031, registering a CAGR of 17.62% between 2026 to 2031.

This report is Segmented by Product Type (Containerised Systems and Cabinet/Rack Systems), Component (Electrolyte, Cell Stack, and Membrane), Power Rating (Below 100 KW, 100 To 500 KW, and More), System Size (Large-Scale, Medium, and More), Application (Renewable Energy Integration, and More), End-User (Utilities, and More), and Geography (North America, Europe, Asia-Pacific, and More).

Global Vanadium Redox Flow Battery (VRFB) Market Trends and Insights

Rapid Build-Out of above 4 h Grid-Storage Projects in China & U.S.

China's State Grid connected 375 MW/1.5 GWh of flow storage between 2024 and 2025, anchored by the 200 MW/1 GWh Jimsar array that stabilizes wind output along the Hami corridor. In the United States, only 3% of 2025 battery additions exceed four-hour duration, leaving a gap that California's 1 GW long-duration mandate and the federal 30% standalone storage tax credit are designed to close. Sumitomo Electric's 4 MW/16 MWh project with San Diego Gas & Electric logged round-trip efficiencies above 68% over seven years, confirming sub-0.5% annual capacity fade even under daily cycling. Because grid operators demand 15-year warranties, this longevity offers a decisive edge over lithium systems that require costly augmentation after year seven. The new tax credit lowers required project IRRs from 12% to roughly 8%, bringing financial returns in line with utility-scale solar and accelerating procurement pipelines in Texas and Arizona.

Vanadium Electrolyte Leasing Models Lowering CapEx in Europe

Bushveld Energy's South African pilot proved that separating electrolyte ownership from system hardware cuts upfront capital by 28% and secures debt at 4.2%, versus 6.5% for traditional structures. Invinity replicated the construct at its 7 MW/30 MWh Oxford project, using a Glencore-backed fund to cover electrolyte and thereby meet European Investment Bank coverage ratios that flow projects had previously missed. Municipal utilities in Panzhihua adopted the same approach for 50 MW in 2024 without breaching provincial debt ceilings. A secondary market for spent electrolyte is emerging, because vanadium retains 95% residual value after two decades, creating a circular-economy incentive that appeals to ESG-focused funds.

Vanadium Price Volatility Tied to Steel Demand

Vanadium pentoxide prices fell from USD 9/lb in 2022 to USD 4-5/lb in 2024 as Chinese rebar production slid 8%, squeezing vertically integrated suppliers such as Largo Clean Energy, which hedged 60% of its forward exposure through 2026. European ferrovanadium settled near EUR 30/kg in 2024, 40% below 2022 peaks, yet futures remain in contango, signaling trader expectations of supply tightness once China's stimulus revives construction demand. Export quotas imposed by Beijing in 2023 created six-week delivery delays that forced Invinity to pre-purchase 18 months of electrolyte inventory. Leasing structures absorb some volatility, but lessors ultimately pass costs through when spot vanadium exceeds contracted collars, leaving end-users partially exposed.

Other drivers and restraints analyzed in the detailed report include:

- Surging Demand for Long-Duration Storage to Firm Solar in MENA

- Technology Breakthroughs in Membrane and Electrolyte Efficiency

- Lack of Bankability Standards for VRFB Projects

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Containerised units commanded 67.0% of 2025 revenue, underscoring utility appetite for turnkey 40-foot modules that integrate power conversion and fire suppression. The vanadium redox flow battery market size for containerised systems reached USD 740 million in 2025 and is projected to expand in line with multi-gigawatt procurement programs in China and the United States. Jimsar's 200 MW/1 GWh build used 250 identical containers, enabling phased commissioning that brought early revenue online while later strings completed factory acceptance tests. Cabinet and rack formats address space-constrained sites and will grow at a 21.1% CAGR through 2031, supported by Vanevo's gravity-fed 10 kW/40 kWh design that removes external pumps and trims maintenance by 35%. The shift mirrors grid-edge trends in telecom and data centers, but economies of scale in power electronics will keep containerised offerings dominant for mega-projects.

Container mobility unlocks EPC efficiencies, modules arrive factory-tested and require minimal on-site labor, while the ability to stack them two-high reduces land use to 15 m2 MWh-1. In contrast, cabinets slot into 19-inch racks and fit behind standard switchgear, appealing to commercial and industrial retrofits. Redflow's hot-swappable 200 kWh pods illustrate how modularity shortens downtime to two hours, a metric valued by data centers at USD 50,000 per avoided outage hour. Over the forecast, containerised shipments will still account for more than 60% of capacity, but high-volume cabinet sales lift modular solutions to almost one-third of delivered units by 2031. The vanadium redox flow battery market will therefore display a two-track dynamic: bulk storage for utilities and flexible form factors for distributed customers.

Electrolyte generated 43.3% of component revenue in 2025, reflecting vanadium's 35-40% cost share and the value locked in secondary reuse. High-purity VPURE+ formulations demand a premium yet extend rebalancing intervals by 12 months, lowering O&M by USD 8,000 MWh-1 yr-1. Membranes will post an 18.4% CAGR to 2031 as low-cost PBI and PFSA options widen gross-margin headroom even when vanadium prices rebound. The vanadium redox flow battery market share of electrolyte is projected to fall to 38% by 2031 as stack and membrane costs compress faster, but electrolyte will grow in strategic importance because leasing converts a capital line item into a predictable service fee.

Stack cost trajectories are equally aggressive: automated carbon-felt and stamped bipolar plates in Dalian plants drove unit prices to USD 150 kW-1 by 2025, down 45% from 2022, making stacks the next focus for margin pressure. Pacific Northwest National Laboratory's higher-density electrolyte permits a 40% reduction in tank volume, shrinking balance-of-plant expenses for rooftop and shipping-container footprints. Together, falling membrane and stack costs ease total system capex and strengthen the case for service-based business models that decouple commodity volatility from project cash flows.

Geography Analysis

Asia-Pacific generated 48.7% of 2025 revenue as China pursued a 30 GW storage target and commissioned both Wushi and Jimsar, which now represent 40% of global VRFB capacity. Japan green-lit its first VRFB subsidy for the 8 MWh Kumamoto site, reflecting policy alignment as solar penetration crosses 12% of national generation. India's draft National Energy Storage Framework assigns tariff premiums to >6-hour systems, positioning VRFBs for 15-20% of a 10 GW pipeline by 2030.

North America will lead growth at a 22.5% CAGR to 2031, underpinned by the federal 30% standalone credit and California's 1 GW long-duration solicitation. San Diego Gas & Electric's long-running 4 MW/16 MWh unit verified less than 0.5% annual fade, demonstrating bankable performance to U.S. lenders. Canada's Clean Electricity Regulations accelerate adoption as utilities must reach net-zero by 2035, driving 500 MW of long-duration procurement in Alberta and Saskatchewan. Mexico's Sonora solar corridor seeks 300 MW of six-hour storage under CFE's 2024 tender that favors flow chemistries for high-temperature operation.

Europe held roughly 18% market share in 2025. The United Kingdom showcased electrolyte leasing at Oxford, raising debt-service coverage to 1.5X and reducing capex by 28%. Germany's EEG 2023 offers a EUR 0.10 kWh-1 bonus for >4-hour storage, prompting 80 MW of VRFB awards between 2024 and 2025. Spain's 1.1 MW/8.8 MWh install cut curtailment at a Castilla y Leon solar farm by 9%. Nordic utilities weigh seasonal benefits as winter peaks exceed summer solar by 60%, making 200 MW of flow storage attractive.

The Middle East and Africa held 8% of revenue. Dubai tendered 300 MW/2.4 GWh of eight-hour storage for its Mohammed bin Rashid Al Maktoum park, citing safety under 45 °C ambient temperatures. Saudi Arabia's NEOM giga-projects call for at least 1 GW of VRFB to balance intermittent solar, and South Africa's Eskom now evaluates flow chemistries for peaking capacity after a successful 6 MW pilot. South America remains nascent, but Brazil's 2024 auction framework favors >20-year design life, a criterion that plays to VRFB's strengths.

- Invinity Energy Systems plc

- VRB Energy

- Sumitomo Electric Industries Ltd.

- CellCube Energy Storage Systems

- RedT Energy

- VanadiumCorp Resource Inc.

- Bushveld Energy

- Largo Clean Energy

- ESS Tech Inc. (Iron-based comparator)

- Primus Power Corp.

- Redflow Ltd.

- Vionx Energy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Build-out of Above 4 h Grid-Storage Projects in China & U.S.

- 4.2.2 Vanadium Electrolyte Leasing Models Lowering CapEx in Europe

- 4.2.3 Surging Demand for Long-Duration Storage to Firm Solar (MENA)

- 4.2.4 Technology Breakthroughs in Membrane and Electrolyte Efficiency

- 4.3 Market Restraints

- 4.3.1 Vanadium Price Volatility Tied to Steel Demand

- 4.3.2 Lack of Bankability Standards for VRFB Projects

- 4.3.3 Competition from Below USD 250 kWh Li-ion for Less than 4 h Services

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Containerised Systems

- 5.1.2 Cabinet/Rack Systems

- 5.2 By Component

- 5.2.1 Electrolyte

- 5.2.2 Cell Stack

- 5.2.3 Membrane

- 5.3 By Power Rating

- 5.3.1 Below 100 kW

- 5.3.2 100 to 500 kW

- 5.3.3 501 kW to 5 MW

- 5.4 By System Size

- 5.4.1 Large-Scale (Above 10 MWh)

- 5.4.2 Medium (1 to 10 MWh)

- 5.4.3 Small-Scale (Below 1 MWh)

- 5.5 By Application

- 5.5.1 Renewable Energy Integration

- 5.5.2 Grid-Peaking/Load-Shifting

- 5.5.3 Microgrids and Off-Grid

- 5.6 By End-User

- 5.6.1 Utilities

- 5.6.2 Commercial and Industrial

- 5.6.3 Residential

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 Germany

- 5.7.2.3 France

- 5.7.2.4 Spain

- 5.7.2.5 Nordic Countries

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 ASEAN Countries

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Colombia

- 5.7.4.4 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 South Africa

- 5.7.5.4 Egypt

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Invinity Energy Systems plc

- 6.4.2 VRB Energy

- 6.4.3 Sumitomo Electric Industries Ltd.

- 6.4.4 CellCube Energy Storage Systems

- 6.4.5 RedT Energy

- 6.4.6 VanadiumCorp Resource Inc.

- 6.4.7 Bushveld Energy

- 6.4.8 Largo Clean Energy

- 6.4.9 ESS Tech Inc. (Iron-based comparator)

- 6.4.10 Primus Power Corp.

- 6.4.11 Redflow Ltd.

- 6.4.12 Vionx Energy

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment